The independent insurance agency industry is being disrupted, but the disruption is not necessarily coming from the place everyone fears, which is technology. The sustained boom in agency acquisitions by large national brokers, regional agencies and especially private equity organizations is, in effect, hollowing out the middle of a traditional industry. In fact, my recent discussions with industry experts suggest that if the pace of recent agency acquisition continues, the remaining “investable” agencies could be depleted in just four years.

The acquirers are bringing increasing financial sophistication and technological capability to the industry to earn a return on the increasingly high prices they are paying for the underlying asset. This fact has important implications for agency owners who are interested in preserving the legacy of their business by not selling to a larger organization: To remain competitive and maintain traditional profitability levels, locally owned independent agencies must match the big organization’s sophistication.

The biggest difference between private equity or other acquirers fueled by the stock market and locally owned agencies is their ability to gather, analyze, manipulate and use data to improve their operations, cost structures and organic growth. There are two pieces that agency owners need to understand. The first is the human capital capability for analysis and decision making; the second is the systems, software and other capabilities these organizations invest in to provide the data and analytics they need. Let's begin there.

Data-Driven Change

For an agency to grow beyond a couple of million dollars of revenue, it needs a deeper understanding of the books of business and clients. As agencies grow, they tend to make increasing use of their fundamental software system, the agency management system (AMS). However, that is just the beginning point for an agency fueled by private equity. Such agencies also use software like Risk Match, which tells them at the account level what carriers will pay them for the business they're writing and how individual accounts will afect profit sharing. This granular data and analysis helps large agencies make very sophisticated decisions about the business that they will and will not write, as well as where they place it in the companies they represent.

Systems like this also give tremendous insight into carrier compensation, which increasingly sophisticated operations are able to use to negotiate arrangements that are tailored to their individual operations. These software tools not only assist the agency’s organic growth but also facilitate reductions in expenses through greater marketing efficiency.

Private equity-owned and similar organizations also use sophisticated customer relationship management (CRM) programs customized for their operations. These programs manage sales teams and prospecting activities much more intensively than small agencies and gather data to reach potential clients with very targeted marketing messages. This capability, along with flexible teamwork, improves client acquisition.

Increasingly, private equity-funded agencies are also purchasing services and software that until recently were only the purview of carriers. The agencies are able to purchase data and analytics from third-party providers to gain additional insight into their existing books of business and also opportunities in the niche markets they choose to serve.

These firms are also investing huge sums of money to give clients what they want, which increasingly is the ability for self-service. While many independent agencies are using off-the-shelf capabilities provided by their AMS, the private equity firms are opting for a bespoke approach with the understanding that the incremental capability they are able to deliver clients will help them increasingly win and retain business.

In addition to opting for self-service technologies, larger agencies are rapidly adopting what many local independent agencies continue to shun. That is the use of account servicing technologies like CSR 24/7, insurance operations and business process solutions providers like Resource Pro and even company service centers to drive down expenses. These large agencies recognize they must take an aggressive approach to cost-cutting to generate the profits necessary for an adequate return on their investment. Once the returns have been realized, these efficiencies contribute to capital and the capability to acquire even more business.

Finally, large, well-funded private equity groups are able to bring to the party sophisticated human resources required to make the best use of this technology from an analytical point of view. Simply put, because of their size, these groups can hire data scientists and data experts to inform better, more sophisticated decisions. The groups expect staff in the acquired agency to use the technology, the data and analytics; increasingly, those who don't will have no place in these organizations.

The Agency Bottom Line

What all of this implies for the independent agency that intends to remain independent is the need to make increasing investments in similar capabilities. The challenge for smaller organizations is the cost of these human and technical capabilities, which is exacerbated by the fact that the technical capabilities are expanding at an exponential rate and that agencies can no longer assume that software they purchase will have a useful life beyond the time it takes to pay for it.

Increasingly, to remain competitive, agencies will have to make investments, not knowing in advance what the return will be. The good news is that, for the vigilant and adaptable organization, much of this technology will become increasingly less expensive. However, the fundamental choice remains for agencies: Are you willing to adapt at a rapid rate to remain competitive with much larger organizations that have a local presence in your community, or will you attempt to grow your business by either moving down market or reducing your historical profitability?

In many ways, the independent insurance agency industry has not fundamentally changed in the last 100 years. Yes, we are using computers to do faster what we did with typewriters 50 years ago, and by hand before that. But we are still doing things essentially the same way. Today, though, sophisticated data analytics, automated submission systems, outsourced service capabilities, dynamic self-service and other technologies — along with increasingly sophisticated human capabilities — being brought to the industry by private capital are making fundamental changes to the traditional industry.

Agency owners are, therefore, increasingly faced with the difficult choice of selling to one of these organizations and giving up their traditional independence, accepting lower profit margins in an attempt to hang on or embracing similar technologies in a renewed effort to compete in a changing business. For agencies, the question is: Which choice will you make?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

It’s been a tumultuous year. In just the span of a few weeks, COVID-19 emerged unexpectedly and abruptly altered almost every corner of the commercial insurance space. Stock market and GDP forecasts have whipsawed as economists and investors have tried to make sense of frequently shifting news. Now we’re in a contentious and unpredictable election cycle.

Divining the future is always a challenge, but lately it’s become especially difficult. During periods of intense change, traditional patterns and precedents lose their predictive power. Regression-style tools that provide data extrapolations become a useless blur. The average workers' comp claim duration of 2019, for example, will look very different than it will in 2020. Litigation and fraud may emerge in new forms, with most new types passing undetected by screens developed from prior data.

One approach that can help companies navigate the uncertainty is artificial intelligence (AI), which is highly sensitive to new data and tends to react immediately, creating a dynamically updated vision of the future. While much of the world has been focused on COVID-19 and the related economic challenges, the underlying technologies behind AI have continued to accelerate in speed, efficiency and predictive accuracy. For organizations looking to become more resilient, it’s an ideal time to consider integrating machine learning, natural language processing and other AI techniques into their operations.

While the promise of AI is great, so, too, is the hype. As a result, many people have a misconception of what AI actually is — and what it is not. Let’s take a look at how it really functions, what it can and cannot do and how it can help future-proof commercial insurance.

Two Types

AI is typically viewed in two fundamentally different ways. There is the futuristic “AI-is-taking-over” version (think Skynet or similar concepts brought to life by Hollywood). This form understandably makes people a little nervous that machines will grow to dominate society (or at least replace jobs at a time when we’re already seeing unemployment lines expand).

Then there is a more prosaic version in which AI complements what humans do. Think of how Google automatically surfaces structured answers to questions you type in or how Amazon knows which product you might want to buy next. In these cases, AI extends your capabilities while leaving you in the driver’s seat. It is this more practical version that will get organizations and teams excited about modern AI-based applications and is the game-changing application in the commercial insurance space.

AI that augments human capability is especially valuable in businesses like insurance, where there is simply too much data coming in quickly for people to keep up. Image and language processing can be applied to the dozens of structured documents typically associated with a claim but can also be used to interpret unstructured information, such as handwritten doctors' notes. Often, this approach finds important information — diagnostic codes that were considered, for example, but not officially associated with the case. Subtle cues can be detected across a wide range of files to create insights that would otherwise go unnoticed. Alerts bring those insights to adjusters’ attention, helping them take prompt action that can make all the difference in a claim.

In this way, AI becomes a kind of superpower for the adjuster. It helps adjusters see through the clutter and make decisions with speed, precision and scale. This helps adjusters become more productive and better able to focus on the claims that matter most. It also frees them up to handle the types of challenges that humans are uniquely suited for, such as detecting the hidden concern in a claimant’s words or enabling them to feel listened to during a challenging period.

AI can end up reshaping not just a single claim but how a business is managed. Claims leaders can now use it to optimize organizational practices, team performance and even partner networks. AI can score healthcare providers, for example, so carriers can direct claimants to highly rated doctors and even identify new ones to bring into the network. Carriers can also use AI to evaluate the effectiveness of their attorney panels based on specific outcomes. These are just a few examples of substantial business decisions that can now be driven by data and intelligence.

Despite the complexities and considerable challenges brought about by COVID-19 and other events this year, the insurance industry sits at a breakthrough moment. New uses for AI such as those highlighted above will continue to be identified and implemented, resulting not only in more efficient operations and empowered employees but also in better, faster, more valuable service to claimants.

Gary has been a leader in the technology industry for over 21 years, with a deep focus on building AI & Machine Learning applications for the Enterprise market. Over the span of his career, he has raised over $1.2B in debt and equity and helped create over $7.5B in enterprise value through 2 IPOs and 4 M&A exits. Gary holds an M.B.A. from the Marshall School of Business at the University of Southern California, where he was named Sheth Fellow at the Center for Communications Management. He also holds a B.A. with honors in Business from Arizona.

Are you a founder or corporate innovator who is seeking to demonstrate the potential of your concept by constructing a detailed five- or even 10-year profit and loss (P&L) statement with associated outlooks for key business drivers? Are you developing exhaustive business cases for your nascent concept, using models borrowed from mature business lines?

Too many potentially worthy innovation investments are defeated when characterized by the wrong metrics. Metrics that, through their very precision, convey expectations of predictable year-over-year returns are, frankly, nonsensical for an emerging concept where in-market experience will first be needed to gauge how the business model might perform. And CEOs and CFOs who apply traditional key performance indicators to emerging opportunities unwittingly set these innovations up to fail.

Using legacy performance measures to assess concepts that may have little resemblance to established products and services, or just treating innovation as immeasurable -- both undermine potential opportunities. Why?

They are based on patterns of customer behavior that drive a business model that may bear no resemblance to yours.

They run the risk of missing the customer behaviors that would drive your business model.

They establish evaluative criteria that may be irrelevant to how your innovation’s potential should be assessed, therefore misleading your product and sales efforts.

The good news is that innovation is measurable. Any innovator using resources should be held accountable to establish and deliver on performance expectations, and there are disciplined ways to introduce effective innovation metrics. Given the rate and degree of change happening across all sectors of the economy, now is the time to develop metrics that monitor and accelerate the conversion of insights and ideas into new sources of stakeholder value.

CEOs need to assign new metrics that can nurture their investments and judge them appropriately.

To that end, innovation metrics choices should meet three criteria:

Be built on an understanding of the user and buyer behaviors that drive the business’ financials — these are the most important key performance indicators (KPIs) to identify, understand and manage.

Be reasonable for the evaluation of potentially unprecedented offerings.

Be able to hold their own even in zero-sum resource allocation processes.

Early in my career, when I was seeking seed funding for a new concept, an executive gave me valuable advice that has stuck with me. My team and I shared copious financial analyses, including five years’ of P&Ls carried out to the penny. He waved aside our spreadsheets and, laughing, told us, “Don’t seek a level of precision that cannot be possible when you are looking at something so new.”

Instead, executive teams can adopt common-sense approaches to ensure discipline — the right kind of discipline — for evaluating and monitoring emerging business models.

For an early stage, new-to-market concept, what is most important is to ask the right questions, be confident in relying on judgment where facts simply do not exist, seek metaphors from other sectors or markets and accept good enough data that can be refined along the way. Smart questions answered in fast test-and-learn cycles can help a team to derive the relevant metrics and keep innovation projects moving closer to success, or to the set-aside pile.

There is comfort in hard data. It is reassuring to see numbers in organized columns and rows with optimistic trends demonstrating success. But innovation is messy, and it’s vital to explore, listen and dig into qualitative insights that could be important signals that are just too raw to quantify.

Here are questions to consider when determining the right metrics for your innovation:

1. How Big is the Addressable Market?

As soon your team can characterize the potential audience, they can begin to estimate how many users and buyers exist. How big is the audience, in your geography, of people who represent the demographics, have purchasing ability and are reachable by your brand?

Once you have this estimate, do a gut check by taking the 1% test: Would a good result be to earn 1% share of the market? 1% market share is not easily earned. Your answer to this question is an early stage read on how valuable an opportunity you think this is, whether you want to forge ahead or rethink your vision.

2. What Would You Have to Believe?

In the absence of a rearview mirror’s worth of history, it’s better to look forward and envision market, customer, operational and other basics that would need to exist for a concept to appear reasonable.

For instance, what does the intensity of user reaction to prototypes reveal? Are you solving a functional problem, or are you also hitting an emotional chord with your audience, suggesting a willingness to change behavior? What breakthroughs can you discern by examining what is happening in other markets or sectors?

Useful answers to these questions assume the team’s ability to avoid clouding the future view of what is possible with too much knowledge of precedents that may now be irrelevant.

3. What Are the Key Drivers of Revenue and Expenses?

In early iterations, set aside the spreadsheets and sophisticated models. Think conceptually about your preliminary assumptions regarding the business model. What appear to be the primary revenue drivers? What do your assumptions suggest about potential expense drivers?

Perhaps, early on, each of these will only be assigned “high,” “medium” or “low” designations to indicate importance, but not be any more quantifiable without alpha or beta test results.

4. Can You Figure Out the Unit Profit Model?

Looking at your financials at the level of one customer or one unit of product sold will force a focus on the details in a way that aggregate data simply will not. So, factor into early tests, as you refine your prototype and begin to engage potential users, gathering insight to determine the unit profit model and how comfortable the team is that it can be delivered. Make this the focus of your efforts so you can establish the viability of the business model.

5. What Is the Potential to Scale?

With the confidence that you understand unit-level profitability dynamics, test for the path to scale. What will it take to attract each new customer or dollar of sales, for example, and how steep might the growth curve be? Your assumptions will need to be supported by investment in the product road map and sales and marketing efforts reflected in your financials. They should also continue to align with the market dynamics — number of customers, sales per customer and so on.

Reframing — the ability to set aside beliefs and see concepts with a fresh eye — is a critical behavior to practice and perfect as you develop the right metrics for your organization’s innovation program. Executives who are able to reframe how they approach developing and applying metrics stand to increase their organizations’ innovation effectiveness.

Moreover, they will energize members of the organization who are drawn to creating the future because the right metrics can themselves be powerful motivators and enablers, just as the wrong metrics can demoralize a team of innovators and derail or diminish the important work they are pursuing.

You can find this article originally published here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Amy Radin is a strategic advisor, keynote speaker, and Columbia University lecturer focused on why transformation succeeds or stalls in large, complex organizations.

Drawing on senior leadership roles at Citi, American Express, and AXA, including one of the world’s first corporate chief innovation officer roles, she helps leaders build the capabilities required to absorb, scale, and sustain change.

As we approach 2021, we are still adjusting to the many ways the COVID-19 pandemic is disrupting just about every aspect of our lives. Many are asking -- How has COVID-19 affected workplace wellbeing? Are we facing a “perfect storm” of risk factors for suicide, or are there aspects of this crisis that give us hope in our resilient human spirit? What can workplaces do during this time to support workers and their families?

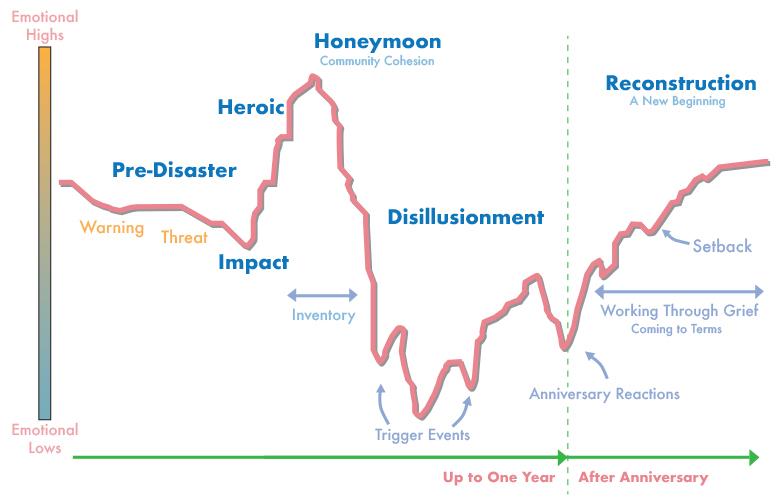

Drawing from a training manual for mental health during major disasters, the Substance Abuse Mental Health Services Administration (SAMHSA) offers this “Phases of Disaster” stress curve to help us make sense of why we are experiencing certain emotional states since the pandemic started. In the “pre-disaster phase” — for most of us in the U.S. this phase occurred in February and early March 2020 -- we experienced anticipatory anxiety as we noticed how the pandemic was hitting other countries. Some had a feeling of impending doom and loss of control while others shrugged off the forecasts as false. Many engaged in strange behavior, like hoarding toilet paper and standing in line at Costco for hours.

By mid-March, we started the “impact phase,” where we felt shock, confusion and even panic followed by a narrowed focus on protecting ourselves and family. While intense, the phase was relatively brief. Shortly after the abrupt shutdown of many parts of the U.S., we started to notice what people have labeled “the heroic phase,” when we celebrated our essential workers and made masks for one another. This altruism gave way to a brief “honeymoon phase,” when we started to feel as though we were pulling together. We were looking out for our neighbors and bringing food to our elders. Musicians sang from their balconies in Italy. We felt a glimmer of hope and optimism that our kindness and compassion would prevail.

Since late May, however, we seem to be in a downward spiral of the “disillusionment phase,” filled with conflict, divisiveness and discouragement. With the added layers of economic impact, violent social unrest and countless natural disasters, the mounting stress has led many to feel overwhelmed and desperate.

Let's hope the rest of the crisis curve will come to fruition. Someday in the future, we will experience “reconstruction phase” and will find pathways to reconciliation. If history repeats itself, at some point people will begin to rebuild and grow through the lessons learned from the multiple disasters of 2020.

Should we be worried about the impact of all of these prolonged stressors on the risk for suicide? Some have written that COVID-19 is a perfect storm of risk factors. Economic disruption, social isolation, decreased access to healthcare and forms of support (e.g., faith communities) are all strong risk factors for suicide. We have good reason to be concerned, as many leading indicators are showing warning signs of deteriorating mental health.

The Bad News: Leading Indicators

Here are worrisome trends:

Financial hardship:The fluctuation in unemployment not only affects whether people can pay the bills, it affects access to healthcare and housing. Women, immigrants young adults and unpaid care givers are some of our most affected workers. Economic stressors and the loss of one’s identity as “provider” are key drivers of our “deaths of despair” trend.

Family violence:Intimate partner violence calls have dropped — not because the violence dropped but because people were locked at home and could not safely access services.

Children and trauma: Kids and young adults are missing important social connections needed for development. Additionally, despite evidence that child abuse and neglect have been on the rise during COVID-19, many states initially reported significant decreases in reports to child maltreatment hotlines — largely because kids were no longer at schools, where the abuse and neglect was being identified.

Elder neglect:Older adults, many of whom were already facing loneliness in epic proportions have been the hardest hit by the isolation caused by the response to COVID-19. While many younger adults were already accustomed to digital connections, older adults often have more challenges engaging with new technologies and are not always able to benefit in the same way.

Access to lethal means: Gun sales have also spiked. NPR reported that people have bought 3 million more guns than normal between March and July in 2020, and almost half of all those sales are to first-time gun owners. While owning a gun does not make someone more suicidal, if you are suicidal, and you have access to a gun, you are far more likely to die.

As a mental health and suicide prevention speaker and consultant, I am routinely asked if our nation is facing a surge in suicide deaths. Given all of the increased risk factors and warning signs, why are we not making this prediction? Well, for one reason, we have actually seen a dip in suicide deaths during periods of our history when we faced great adversity. For instance, our suicide rate decreased immediately after the 9/11 terrorist attacks, and over the course of history (most recent conflicts aside) suicide rates during wartime decreased because people pulled together.

Another reason is – sometimes when we predict trends, we run the risk of creating a self-fulfilling prophecy. That is, when we predict people can’t cope, they don’t; when we drive a culture of care instead, that is the narrative that plays out.

So, we all need to prepare for the worst and set ourselves up for the best.

10 Steps Employers Can Take That Make a Difference

Community:Remind workers that “we’re all in this together” as a workplace community. Share stories of how you’ve pulled together during tough times in the past. Call out examples of when employees are taking care of one another. While it seems like this will go on forever, one day we will look at it from another side – how would we like to look back at ourselves?

Validation:Normalize and validate workers’ emotional experiences. A range of emotions is to be expected -- anxiety, anger, frustration and grief to name a few. Give workers grace, and encourage them to forgive mistakes without judgment. Offer them permission to give themselves a break for being a “good-enough” parent, partner or worker. People bring their whole selves to work, so remember that when they show up for work duties they are still worried about their kindergartener’s ability to learn from a screen or about their great aunt who has been in lockdown for months.

Right-size expectations: Given the level of disruption and distraction, what can be done to adapt expectations? Can workers be honest with their managers about capacity? Encourage workers to ask for help when they need it. Ask yourself the 10-10-10 questions – will this matter in 10 days, 10 months or 10 years? Prioritize, and let some things go.

Prioritize wellness:Routine and structure can be helpful in getting us grounded. Frontload workdays with opportunities for wellness – walking meetings, yoga breaks, meditation sessions. Suggest that workers take frequent short breaks to go outside and get sun on their faces. Remind them to prioritize sleep and exercise as key ways to avoid burnout.

Limit media exposure:The constant distressing news coming to us from our phones, computers and televisions can not only overwhelm us, it increases our risk for vicarious trauma. When we are bombarded by images, sounds and storylines of highly distressing information, we can develop anxiety, hopelessness and even post-traumatic stress – even when we haven’t experienced the trauma directly. Suggest that employees take breaks from the news and fill their viewing feed with stories that bring them joy and inspiration.

Celebrate people: What gives us hope more than anything? The triumph of the human spirit. At work, share stories of people overcoming obstacles. Lift up examples of people who are creatively solving problems. Recognize and reward those who are unselfishly going above the call of duty to help others succeed. Tell their stories with relish.

Frequent check-ins:Expand your culture of care by encouraging workers to check in with one another. This practice of reciprocity drives the experience that workers have each other’s backs. For instance, suggest they send what we call “non-demand caring contacts” to one another. These contacts are brief forms of communication, like unconditional little messages of support they give one another. For example, a coworker can text someone from their team, “I am thinking of you today and wishing you well,” or a manager can leave a voicemail to a direct report, “I see how strong you are during this difficult time.” Make a game out of how workers can perform intentional acts of kindness with one another.

Find the fun: Bring in micro joys like surprising workers with donuts or an on-line trivia game. Start a meeting with a funny movie clip that makes a point. Give out silly awards for creative ways people are coping.

Provide community service: Whenever we think we are struggling, it’s always helpful to connect to others who would benefit from kindness. Find opportunities for workers to contribute to something larger than themselves. This effort could be a clothing drive for a youth homeless shelter or a time together to clean up a community park. The “helper effect” is a real thing -- when we help others, we help ourselves.

Bring resources to life: It’s not enough to post hotlines and mental health resources on your webpage. Bring them to life by having representatives talk to workers about what to expect or have users of the services share their experiences. Promote a buffet of resources in addition to your employee assistance program. Be sure to offer on-line telehealth options and 12-step groups. Crisis resources like the Disaster Distress Helpline (800-985-5990), the Crisis Text Line (Text HELLO to 741741) and the National Suicide Prevention Lifeline (800-273-8255) are free, anonymous and available 24/7.

Sally Spencer-Thomas is a clinical psychologist, inspirational international speaker and impact entrepreneur. Dr. Spencer-Thomas was moved to work in suicide prevention after her younger brother, a Denver entrepreneur, died of suicide after a battle with bipolar condition.

The new cool lingo and title for producers is "risk manager." When I interview these "risk managers," most cannot tell me what risk management actually is -- but the title helps increase sales.

Somewhere along the line I've realized that many people in the industry do not really understand what insurance does! "It protects in case of an accident" is the most common answer. But what does it "protect" in case of an accident?

Insurance is a subset of risk management. Risk management can be done quite well without any insurance, but insurance can't really be done well, correctly, without some level of risk management. Insurance is usually sold without any risk management efforts due to many factors, including lack of knowledge among consumers, the difficulty of explaining insurance coverages, laziness on the part of insurance distributors and consumers, incompetency and the fact that selling a complex product like insurance is difficult unless the seller makes it seem excessively simple -- hence cartoon animals and bumbling morons selling insurance, and selling it successfully!

Since time began, risk management has always existed, whether definitively or intuitively, in human endeavors. Modern insurance was created when risk managers for banks decided that a financial risk management tool was required to protect the loans they made to ship owners/builders. The banks needed a way to shift the risk of loans not being repaid in the event the ship sank or was pirated. The banks decided they could not cause enough cannons to be added (cannons were the original risk management tool against pirates), nor could the ships of the day be adequately engineered to overcome Mother Nature. So, some people in London created insurance.

Today, most property insurance serves the same function. People buy homeowners insurance policies to satisfy their mortgage company's requirement. This is why so many people naively quit buying homeowners insurance when they've paid off their mortgage, because some insurance agent failed to explain the importance of liability insurance.

Risk management is designed to minimize risk, particularly probable risks. If you look at a normal curve of risk frequency, the large area in between the two ends is where straight, non-insurance risk management solutions shine. For example, in certain environments, the probability of someone slipping and falling is high. Insurance is not the best solution. Fixing the flooring is the best solution.

Insurance is the best solution for known risks that are highly unlikely to occur. Insurance is not designed to be a maintenance policy. Maintenance is known and expected. Insurance is designed for the unexpected and unlikely. Insurance companies would quickly go out of business if insurance covered the expected and likely because their claims would exceed their revenues or the price would be so high no one would buy the policies.

This reality of insurance leads to huge frustration among consumers because they don't get to "use" their insurance. Who wants to buy something expensive to protect their property from an event that is highly unlikely and unexpected to occur? (Life insurance and health insurance are true exceptions to the unlikely and unexpected rule because death is highly likely. Life insurance is a death timing insurance for your death occurring at an unlikely, and therefore unexpected, time. Health insurance has morphed into an almost unrecognizable distant cousin of true insurance.)

Most agents do not adequately explain that buyers "use" their insurance daily. Insurance enables them to use their house immediately rather than waiting until they can purchase the house in cash. People get to drive, they get to bid on construction jobs, they get to protect their families. It's hard to explain these benefits in jingles.

If a person is only selling P&C insurance, then, using a normal curve as an example, they are only addressing around 5% of a company's risk. The other 95% encompasses more straight risk management solutions outside of insurance. If you call yourself a risk manager when you are really only selling insurance, are you representing yourself truthfully only 5% of the time?

Chris Burand is president and owner of Burand & Associates, a management consulting firm specializing in the property-casualty insurance industry.

Six Things Newsletter | October 20, 2020

In this week's Six Things, Paul Carroll recaps a panel discussion between Insurance CEOs at the International Insurance Society annual forum. Plus, the hyper-personal future of insurance; how to unlock a 'Customer 360' view; and more.

In this week's Six Things, Paul Carroll recaps a panel discussion between Insurance CEOs at the International Insurance Society annual forum. Plus, the hyper-personal future of insurance; how to unlock a 'Customer 360' view; and more.

At the International Insurance Society’s annual forum last week, several CEOs of major insurers said they foresee a very different world post-pandemic — one where trust in insurers not only needs to increase but must take a different form; one where work happens in different places at different times in different organizational structures, all at far greater speeds; one where the challenges increase, but the opportunities do, too... continue reading >

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

The business strategy sets the direction and targets of the company, but the operating environment changes constantly.

To succeed, insurers must have an operational model with adequate flexibility and agility to follow market fluctuations.

A new target operating model based on a set of design principles necessitated by the pandemic must be designed for the insurer

It’s time to outsource all non-core activities.

Crafting the strategy for a successful future for the insurer is one thing, creating an operating model that is capable of delivering the strategy is another. Even the greatest strategy will just remain as a document if it not put into action – and this can only be done by the organization through a dedicated and reinvented target operating model.

Executing on a strategy requires an organization, systems and processes designed with the strategic purpose in mind, a target operating model. This article discusses how to translate the strategy set by the insurer into an actionable target operating model that enables the strategy to be implemented in the best possible way.

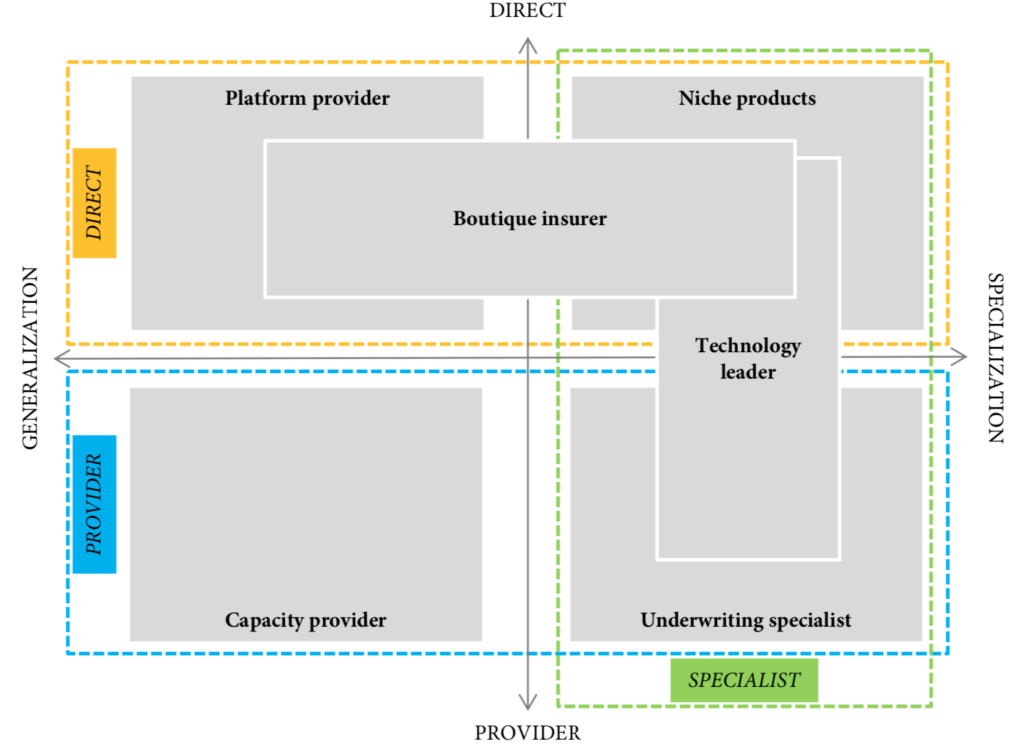

For a discussion on what strategy the insurer should target, please refer to the white paper Future of Insurance, that discusses different strategies that insurers can pursue to remain relevant and profitable in the future, aiming for one of the strategic positions shown in Figure 1 on the next page.

Figure 1: Six future strategy options for insurers to keeping relevant and profitable

It is important to understand that while the strategy sets the future direction of the insurer, the strategy itself must be broken down into actionable elements so the organization is capable of implementing the strategy.

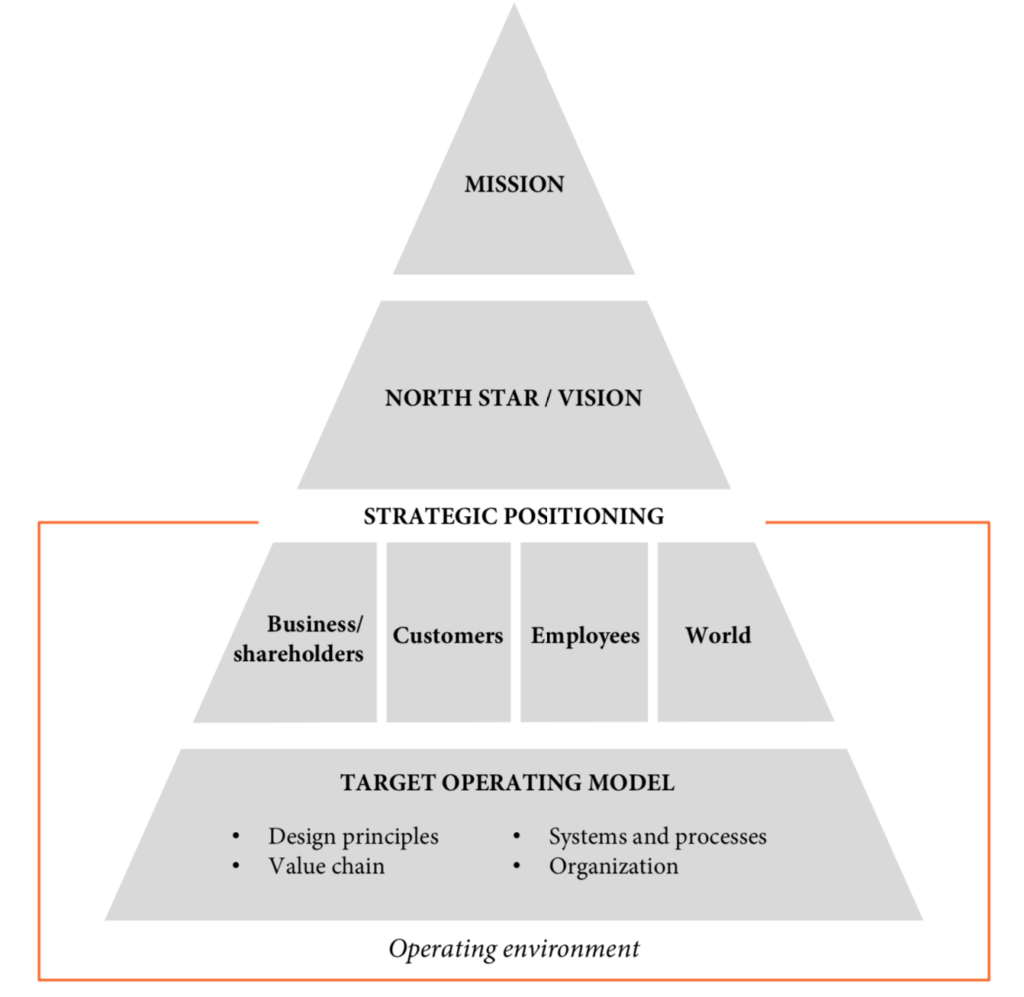

The final strategy should be a derivative of the insurer's overarching mission and vision and ensure that successful implementation delivers on these values. The mission is the insurer's reason to be and should not change over the lifetime of the company, where the vision is the three- to five-year targets that the insurer is pursuing.

Having a solid mission, a guiding North Star, is particularly important during turbulent times as the mission statement helps the company keep focus on the longer-term targets and hence keeps the direction in a volatile and fluctuating environment.

The strategy for the year – or years – is formed based on the vision and seeks to position the insurer:

In the market; which one of the six possible strategies is the right one for the insurer, given the mission, vision and shareholders’ expectations and requirements?

With the customers; which customer segments are we focusing on, and what special value will our strategy bring to our customers; how can we use this to differentiate ourselves in the market?

For the employees; what differentiates us from other employers, and how do we intend to develop our talent to keep them skilled, motivated and engaged?

...and in the world; how do we set out to affect the world and environment around us?

Strategic choices for the business, customers, employees and impact on the world should ultimately decide the target operating model for the insurer. A target operating model describes the principles of how the organization will operate given these choices, taking the operating environment into consideration.

Figure 2: Successful strategy implementation relies on a well-defined and well-functioning operating model

The operating environment is a holistic view on where the insurer operates and covers the current situation as well as the expected development of the political environment, shareholders, competitors, customers, employees and partners.

A successful operating model is built on a deep understanding of the fluctuations and developments in the operating environment – the insurer needs an operating model that is flexible and agile enough to respond to changes in the environment, and the more volatile the environment is, the more flexible and agile the operating models needs to be.

There will often be many unknown elements of the operating environment, so identifying let alone predicting the future development of them can be difficult, but it nevertheless has to be done if the insurer is to create a viable strategy.

For further reading on this topic, a method to understanding and predicting the development of the operating environment can be found in this white paper.

Broadly, four main topics can cover what is required to build a future operating model, enabling the insurer to be responding to market changes when needed:

Design principles — overarching principles that permeate all elements in the target operating model and act as design foundation for the target operating model

The value chain— description of the end-to-end value chain and analysis of what non-core elements can be considered outsourced/offshored to increase the insurer's agility and flexibility.

Systems and processes — (re)design of systems and processes throughout the organization to meet the strategic requirements

Organization— construction of the organizational roles, targets and responsibilities so the organization is enabled to deliver what’s needed to reach the strategic targets

More than ever, the future of business and countries in the world is uncertain, so insurers need an operating model capable of following fluctuations in customer demands and market developments. This is the only way they can to stay relevant in the New Normal and beyond, and therefore an important starting point when analyzing the elements in the target operating model.

The days of slow evolution and predictable market developments are gone, and insurers must design their target operating model to cope with this.

Design principles

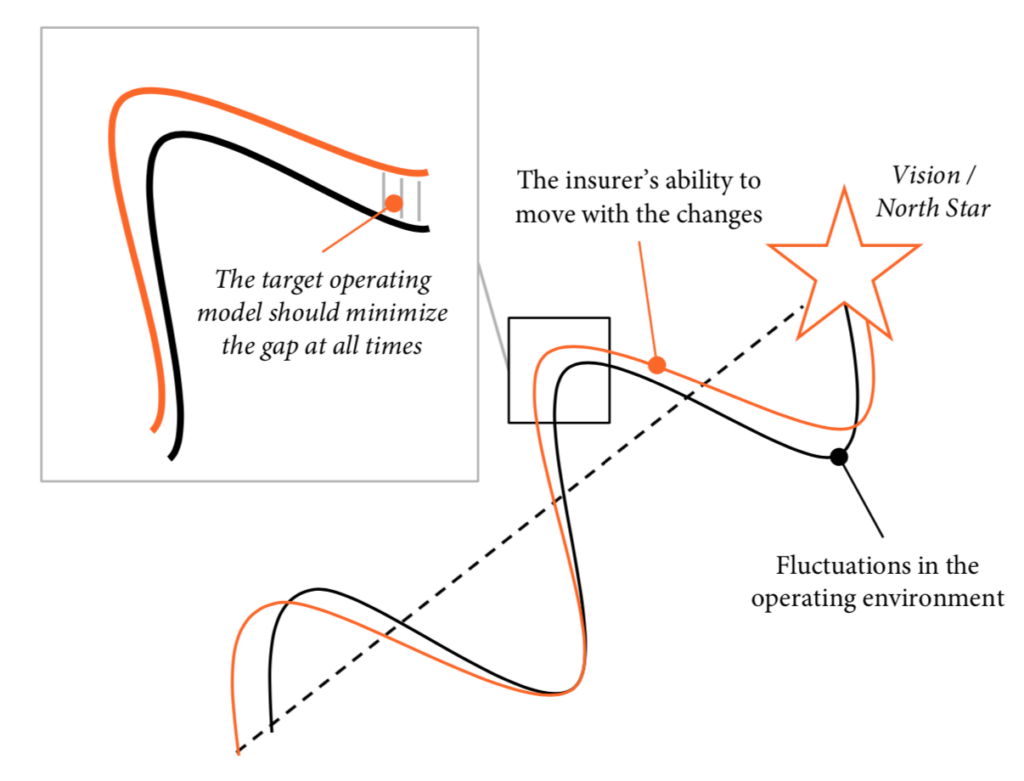

The overarching design principle for the target operating model is to enable the insurer to follow the fluctuations in the operational environment in the optimal way, i.e. being able to respond to relevant market changes (theoretically) as fast as they happen.

Execution of the strategies toward the vision should in other words be open and adjustable enough to facilitate deviation from the straight line (see figure 3), as it would be unwise assuming the market developments will be straightforward and follow a path that is easy to predict.

Figure 3: The target operating model should enable the insurer to close the gap between the market development and the insurer’s ability to follow

Designing the target operating model should therefore be done with the "closing of the market development and insurer response gap" as highest priority.

Maximum virtuality and digital workflows

A key design element of the target operating model is to maximize the virtuality of everything, from processes over partner collaboration to teamwork across the organization – the COVID-19 pandemic forced the world to be virtually and digitally competent in a very short time span, and it is important that the target operating model supports and expands on this.

The more virtual and digital competent the insurer is, the more flexibly the employees will be able to work with partners, customers and each other – and the easier it will be to adapt to future catastrophes and serious market changes.

Digitizing the workflows is another design principle that must be followed to increase the agility and flexibility of the insurer – this is not just making internal processes faster and simpler, but also supports the insurers’ ability to function with the workforce (and partners) working remotely, as there will literally be no need for physical exchange of documents or face-to-face meetings, parts of the claims processes excluded (on-site loss adjustments, repairs, hospitalization, etc.).

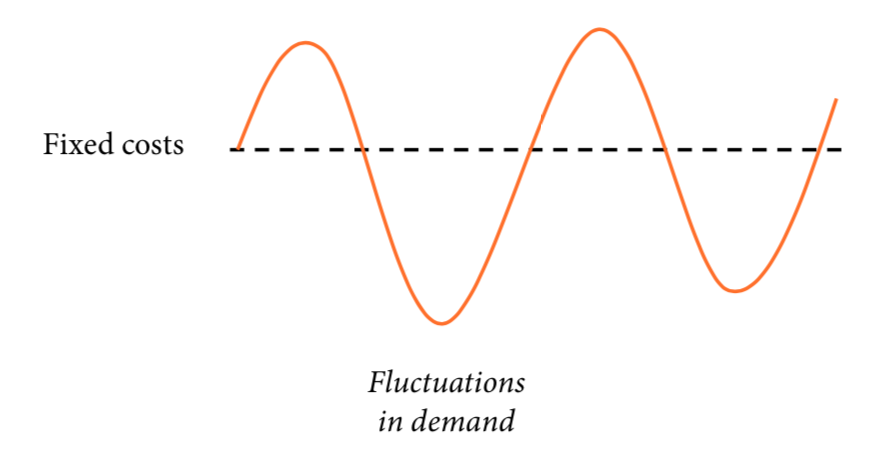

Extreme cost flexibility/minimal fixed costs

Most companies and insurers were caught off- guard by the pandemic, leaving them with a significant drop in demand but with the same, high fixed-cost base. It goes without saying this has hit the financial performance as the fixed costs, being fixed – or long-term commitments – by nature could not (can not) be easily and adjusted to follow the market movements.

If an insurer is to stay profitable in turbulent markets and times, it is necessary to convert the fixed cost base into a significantly more flexible cost base that can move up and down with the market movements. This will allow the costs to fluctuate with premiums and increase the profits or reduce the losses.

Figure 4: Fixed costs cannot follow the fluctuations in market demand and risks eroding the insurers’ profit

A more flexible cost base can be created by outsourcing or offshoring non-core activities and making the payments depending on "units produced"; i.e. claims handled, data operations performed, reports generated, invoices sent, etc.

Apart from offshoring/outsourcing non-core activities, it can be worthwhile looking at office rent and overhead costs. COVID-19 has enabled literally everyone to work from home, and insurance companies have proven themselves to be capable of operating almost fully remotely. Only certain loss adjustments must be done physically; everything else can be managed remotely and virtually/digitally.

By arranging a rotational remote work system, insurers will be able to reduce their rent – a major fixed cost – significantly. Just imagine the impact of reducing workspace requirements by 30%! This number can go even higher if the insurer is following a serious outsourcing strategy, as the direct and indirect cost of employees would be moved from the insurer to the outsourcing partner.

The value chain

A practical starting point for creating the target operating model, especially with focus on reducing fixed costs and increasing the flexibility and agility of the insurer, is the value chain.

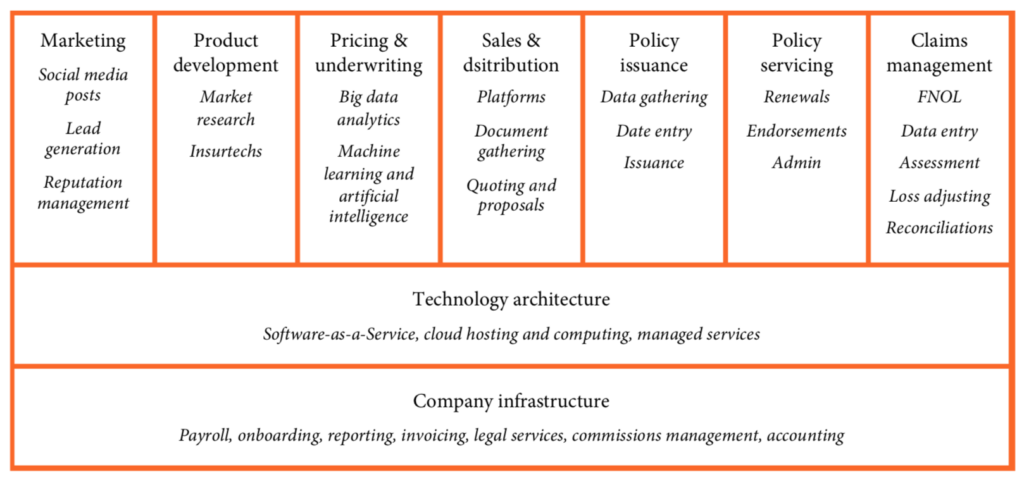

The value chain allows for a detailed walk-through of the operations, so it is possible to define (decide?) what areas of the business are core and non-core. Figure 5 illustrates the typical elements of an insurance value chain with examples of activities that can be considered for outsourcing or offshoring.

Figure 5: Examples of outsourcing potential non-core activities in the insurance value chain

For marketing activities, the insurer can consider outsourcing the planned social media posts and other branding or lead-generation activities like data collection for quoting, initial e-mail marketing and social media activities (competitions, lucky draws, etc.). Outbound calling to potential leads is also a typical marketing activity that can be managed offshore.

Reputation management can also be managed by a third-party partner – reputation management is constant monitoring of news and social media to listen for positive and negative mentions of the insurer, and react to these mentions, whether to prevent reputational damage, to answer questions or to thank for positive mentions.

Proper product development relies on market research, and that, too, can easily be outsourced to a third-party. Another, more radical, approach to product development can be partnering with insurtechs to leverage on their products and services, that are typically innovative – the white paper, Insurtechs, a part of insurers’ digital transformation?, discusses how insurers can fast-track parts of their product offerings by partnering with insurtechs.

Setting the right premium for individuals is most often heavily relying on data analysis, and the abundance of data enables very detailed pricing and underwriting. However, few insurers have the in-house experience and capabilities to leverage the vast amount of data available

It’s possible to work with partners to get big data analytics done, and the same partners could refine the results further by applying machine learning and artificial intelligence to the underwriting and provide a very individualized pricing and underwriting model for the insurer.

Platforms are already being widely used as sales and distribution channels today, as are, of course, the agents and brokers. Gathering of documents on behalf of the customer – digitally or physically – can be a time-consuming task that can be outsourced to a partner, which in turn could also use the data gathered to generate quotes and proposals, based on the models created by the big data analytics and machine learning activities.

Along the same lines, policy issuance can be handled by external partners, mainly when it comes to data gathering and data entries (where it’s not yet automated), and the actual issuance of the policy can also be done externally, on behalf of the insurer.

During the active policy period, policy servicing is another area that is typically not a core function of the insurer and could be managed by an outsourced partner. This could be managing renewals, handling endorsements and other administrative functions like basic changes to customer data (phone number, home address, etc.).

Claims management, a large and critical element of any insurer’s value chain, has several areas where outsourcing of services can be very relevant, ranging from first notice of loss, claims data entries, damage assessments, loss adjustments to general claim inquiries, reconciliations and workman’s compensation data entries.

A growing trend is for insurers to use fully outsourced claims management services, the third-party administrators. TPAs are responsible for the complete claims process and are typically providing these services to multiple insurers, allowing economies of scale to reduce the cost per claim as well as the actual claims cost, too.

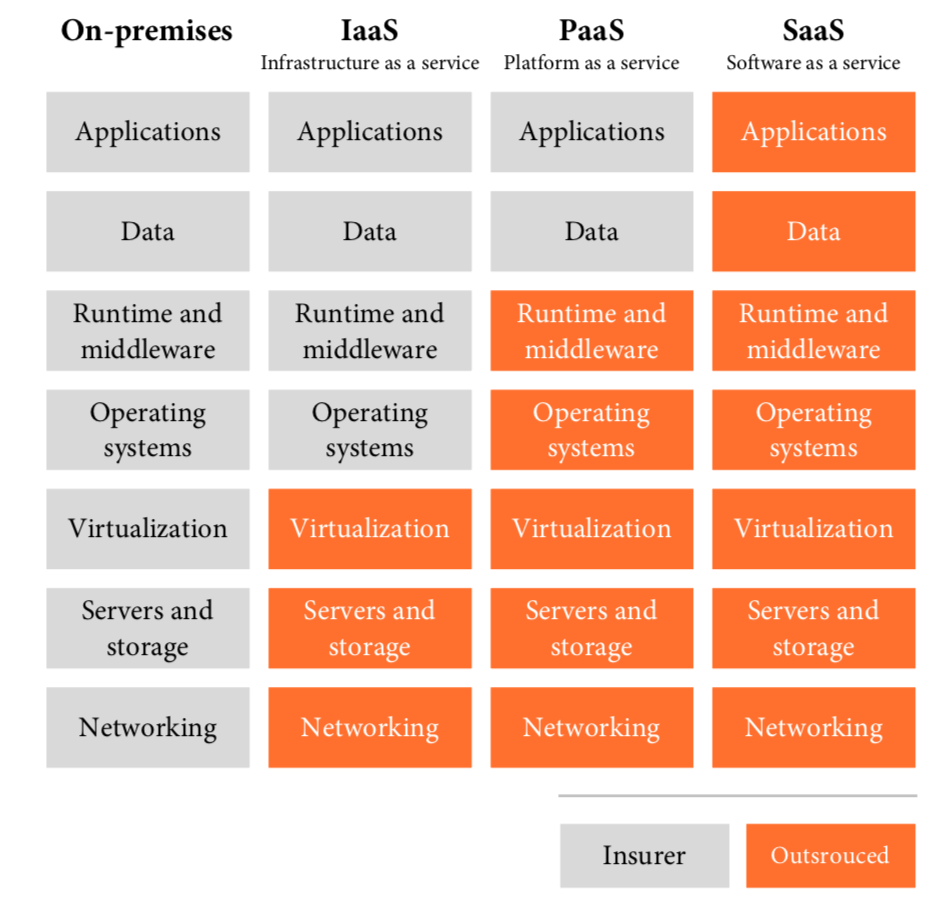

Behind it all sits the technology architecture and IT infrastructure that also have significant opportunities for outsourcing, ranging from hosting services in the cloud over managed services to actively using new(er) solutions like software-as-a-service and platforms-as-a-service.

When analyzing the tech architecture, it is important to look at not only how and where the digital environment is handled, but also who is managing the company’s application development – there may significant opportunities in offshoring large parts of the application development, too, leaving key developers and software architects with the insurer to overlook and manage the remote development.

Figure 6: The differences between various technological architecture hosting models (source: bmc)

When analyzing the tech architecture, it is important to look at not only how and where the digital environment is handled, but also who is managing the company’s application development – there may be significant opportunities in offshoring large parts of the application development too, leaving key developers and software architects with the insurer to overlook and manage the remote development.

There are several elements of the company infrastructure that can be managed by partners, as well, ranging from payroll management, employee onboarding processes, invoicing and accounting to legal services and commissions management.

Many of the reports being generated today are still to a large extent done manually, so that is an obvious area for outsourcing, at least until the report generation has been automated. The same goes for the resource demanding commissions calculations and payments and a wide range of the practical aspects of onboarding new employees.

Important considerations while evaluating outsourcing opportunities

Outsourcing or offshoring non-core activities is more complex than it may seem from the above discussion. There are many aspects and considerations that have to be taken into account when planning, to delink the activities from the insurer.

Customer experience — for customer-facing functions, it’s imperative that the customers are receiving the same or even better service than before, and that they experience a seamless interaction with the insurer. Customers should not feel – or maybe even be aware of – that they are dealing with a third party at all.

Compliance — any outsourcing partner must comply fully with regulatory instructions.

Quality — the quality of the services, from data entry to claims management and repairs, should be of the same standard, or higher, than the insurer has been providing.

Costs — it goes without saying that there should be a cost-efficiency in outsourcing. However, it is worth noting that the sheer flexibility gained by outsourcing can be enough, so the insurer may be willing to pay the same price, just with the added flexibility on cost.

Management — how will partners be managed, and how will an escalation matrix look, to ensure that customers and partners are receiving the same quality of service and interaction?

Service level agreements (SLAs) are used to manage the above considerations. The SLAs are made with detailed service levels (customer satisfaction, average repair cost, handling times, etc.) that are closely monitored and acted upon if they fall outside the agreed scope

Core versus non-core activities

During the discussions, primarily non-core activities should be in focus when looking at outsourcing/offshoring opportunities, so a distinction between core and non-core activities would be relevant.

The notion of core and non-core activities goes all the way back to the introduction of the term core competencies, which Prahalad and Hamel defined as “a harmonized combination of multiple resources and skills that distinguish a firm in the marketplace.” This idea can act as a guide to understand what the insurer does or offers that really sets the products and services apart from the other insurers in the market.

This could be special agreements with car repair workshops that enable the insurer to offer customers a strong value proposition for car insurance. It can be distribution agreements with key partners (banks, digital platforms, brokers, etc.) or a strong brand that is trusted by the customers – or anything else.

Non-core activities are therefore activities that do not – as standalone activities – play an important role in enabling the insurer to offer differentiated products to the customer. Please note that the combination of activities can be a differentiator in itself, and that outsourcing can actually build such a distinct advantage.

Imagine outsourcing a series of processes that, combined, provide a significant improvement in customer service or claims management, allowing the insurer to leverage this to create differentiated market offerings.

Faced with outsourcing, unit leaders and management would be expected to push back and claim that most of their unit’s activities are core activities – it is up to executive management to question this, as it is rarely the case. Typically, a company only has four to five activities that are truly setting the company apart from the competition.

It is therefore necessary to scrutinize processes and activities to ensure that no stone is left unturned – a claim would be that up to 80% of the insurer’s activities are non-core and could potentially be outsourced!

Systems and processes

Following the decisions on what activities to outsource are the systems and processes around the activities. The systems and processes are what tie the activities together and enable the insurer to operate – and in many insurers’ case, the systems and processes are still based on decades-old operating principles. “It has been working so far, so why change?”

However, there should be little doubt that now is the time to change, so it is necessary to relook at how the systems and processes in the organization work, and how they have to be changed to adjust to the expected development of the markets.

Revisiting the current systems and processes should be done in a pragmatic and very structured manner, starting by mapping all processes as they are today, the as-is processes. Based on this mapping, the teams will discuss a future, to-be process and during the discussion identify what needs to change to implement the new processes.

While mapping the current as-is processes, it is expected that the team will identify several non-core activities that can be automated or outsourced, but, before planning to do so, it is necessary to analyze whether the non-core activity is required at all as the new, to-be process may eliminate the need for that specific activity.

There are two principles that are especially useful when mapping the to-be processes: user stories created by design thinking and the concept of straight-through processing.

The user stories are a way of describing the customers’ perspective of dealing with the insurer and take a starting point with the customer, and not the insurer. User stories provide a simple way of mapping the stages the customer has to go through to solve a problem (buy a policy, file a claim, answer a question) irrespective of the units and departments involved at the insurer.

Figure 7: Simplified user story for buying an insurance policy

The user story is used as the foundation for the redesign of the process, which typically will reach across various units and departments. This may require changes to the organizational structure as successful change of the processes requires process ownership in the organization as opposed to business unit ownership – in other words, a responsible person for the processes is introduced into the organization and has the authority to change processes within the various business units.

Think about the many processes and units involved in the simplified user story depicted in Figure 7, from marketing over call center and branches to underwriting, administration and finance – all these units must be aligned across one to-be process, following the user story, the customer’s journey toward buying a policy.

Straight-through processing that is used to speed the transaction by streamlining the information through multiple points – this could be an invoicing process where the information is made readily available to all stakeholders in the process, thereby speeding up the evaluation and approval processes.

This is the underlying functionality of all redesigned processes, as straight-through processing is required to automate and simplify all processes, from underwriting to claims and invoicing and administration. For the new processes to be effective, relevant data for decision making should be made available throughout the process.

Any successful operating model needs an organization to execute on the processes and systems designed for the operating model – and designing a target operating model also means designing a new organizational model to cope with the operating model.

The topics discussed in this article have identified at least two major areas that must be incorporated into a new organizational structure: the ability to handle a massive outsourcing of non-core activities and the introduction of process ownership to manage the redesigned processes across units and departments.

Outsourcing, or offshoring, significant elements of the insurer’s value chain adds a new set of requirements to the organization and the employees who handle the outsourced activities – managing an outsourced team is different than working directly with colleagues in the same company, so employees have to be aware of this and know how to ensure that the outsourced partnership is a success.

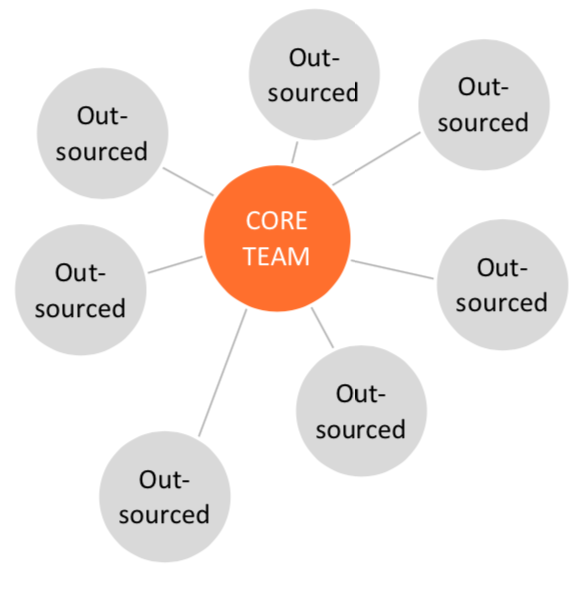

In essence, the core team will be insurance, process and systems experts from the insurer, responsible for managing the daily partnerships with the external partners. The core team will manage the core activities, ensuring seamless connection and collaboration with the external managed non-core activities.

The core teams will be guardians of the insurer’s intellectual property and are responsible for the constant development of these core competences, ensuring that the insurer is on the right strategic path and constantly developing the core activities to keep and evolve the differentiation in the market.

Figure 8: The core team holds the insurer’s intellectual property (core competences) and coordinates closely with the outsourced teams

Along the same lines, the core team is directly responsible for constantly monitoring and following up on the service level agreements set between the parties and act immediately if deviations happen.

A great starting point for the outsourcing process is to relocate existing employees to outsourcing partners and by doing so secure knowledge transfer and continuity in the operations – this also eases the difficult decision of letting a large number of employees go.

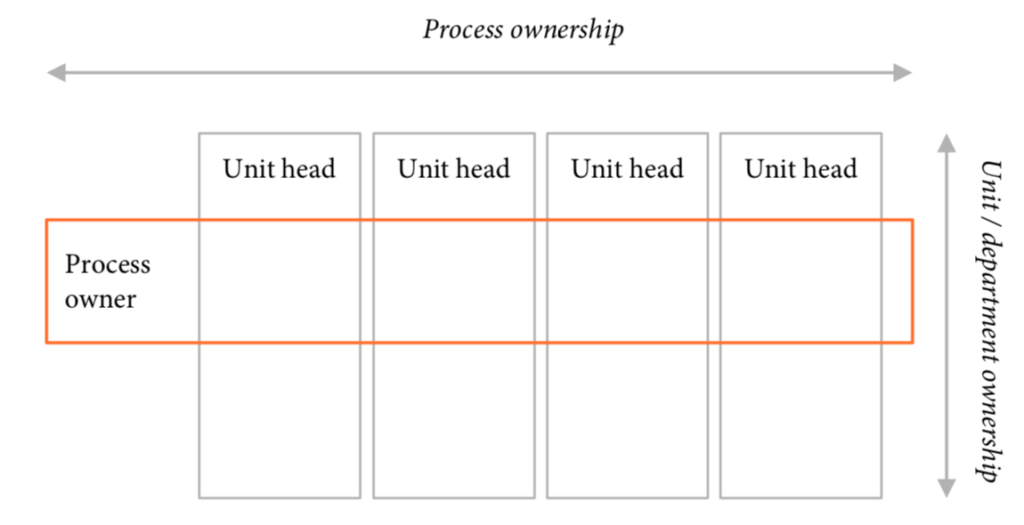

Changing from unit/department ownership to process ownership is necessary to make several of the newly established, cross-functional processes operate optimally. This can be difficult to implement as it will most likely mean significant changes in decision making authority, as unit/department owners now have to coordinate with the process owner to ensure that the processes are as smooth and effective as possible.

Figure 9: Changing processes to focus across units and departments will also change the internal organizational decision- making authority

A key element here is to ensure that the process owner and the unit/department head is measured by the same targets and performance indicators. Shared targets will enable closer cooperation and ease the change from the vertical accountability to the shared accountability across functions.

Final thoughts

Changing an insurer’s operating model is no easy task – it requires coordination and involvement from all stakeholders in the organization, and most often also participation from the board, simply because of the magnitude of changes involved.

Adding outsourcing of non-core activities to this just increases the number of tasks at hand – nevertheless, it is a job that has to be done if the insurer is to maintain a competitive position in a future world expected to be even more volatile and complex than seen so far.

It is for sure a challenging project that lies ahead – as always, it begins with a small, first step.

I hope yours was reading this article. Good luck.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

At the International Insurance Society's annual forum last week, several CEOs of major insurers said they foresee a very different world post-pandemic -- one where trust in insurers not only needs to increase but must take a different form; one where work happens in different places at different times in different organizational structures, all at far greater speeds; one where the challenges increase, but the opportunities do, too.

Amanda Blanc, group CEO at Aviva, said on the opening CEO panel that the "one overriding challenge" she sees is "trust, and the reputation of the industry. I’d say it’s fair to say the industry has had sort of a mixed record over the past six months."

Others agreed, though Dan Glaser, president and CEO of Marsh & McLennan, added that trust has long been a problem. "It may be at a low now," he said, "but it wasn’t coming from a high."

Dean Connor, president and CEO of Sun Life, said he thinks the industry needs to generate a new sort of trust. "100 years ago," he said, "the question was, If I give you my money, will you be around in 50 years to give it back? So, we expressed our brands as beautiful, big buildings. But now, the question is, What are you doing with my data? We really need to pay attention to client data."

Glaser said he thought that, broadly speaking, while cybersecurity was something that people "weren't really talking about a decade ago, it's the No. 1 risk right now. Imagine what a firm would be like if you couldn’t talk to your employees or your clients.... The idea of a cyber hurricane looms for the entire industry, where you might have multiple events in multiple countries at the same time."

Gabriele Galateri, chairman of Generali, agreed that cyber has become a huge issue but noted the opportunities that come along with the increased digitalization of the industry. "On the other side," he said, "the impact of the technology on all our processes and products is just extraordinary -- the way we can be more flexibility and creative and make our products much more personalized."

Connor said he's seen a "step change in productivity that’s not going to go away," as well as an acceleration in decision making. He said that, back in the spring, Sun Life went right to market with a product that in the past would have first involved extensive back-and-forth with brokers. "Instead, we just put it out there, and, boom, 500,000 Canadians signed up for health care." He said he wants that sort of speed to continue.

At Generali, Galateri said, he couldn't believe how fast the company could go digital. He said he's seen in weeks or months the kind of progress that could have taken five to 10 years, though he said that "reskilling" and "upskilling" remain big challenges and that structural changes to the business will be needed to take full advantage of digitalization.

At Aviva, Blanc said she's spending a lot of time thinking about how to design the workplace of the future, how to design a collaborative work space that fosters the right culture. "The workplace of the future will be very different than the workplace of the past," she said. For the moment, she added, "while people used to talk about working from home, now they may say they're living at work."

Whatever results, Connor said, will involve a flatter organization structure, because of what businesses have learned during work-from-home during the pandemic. "COVID has flattened organizations," he said. "CEOs don't just talk to their leadership team. They can talk to everyone." The question, he said, is: "How do we use this time as an accelerant?"

The panelists singled out low interest rates, now cemented in place by the economic crisis that the pandemic has caused, as a hurdle for the industry. Any company that depends heavily on returns on investments will find those hard to come by, perhaps for years, and will have to be much more accurate in its underwriting.

But Connor said, "You could also flip that around and say there’s an opportunity. How do you construct a retirement plan" when interest rates are so low? Companies that can help clients do that will win, he said. He added that COVID has heightened awareness of health and mortality. "Our clients need what we do," he said.

He's broadly optimistic, too, about how 2020, as crazy as it's been, could help produce needed social change, such as on racial inequality, and sees a role for the insurance industry.

"Look at all the change that can happen in just a generation or two," he said. "Think of smoking cessation, drinking and driving, all the millions in Asia who’ve been pulled out of poverty and into the middle class. The Me Too movement has had a profound effect.

Glaser said that "maybe a silver lining of COVID is that while we are all at home watching our screens, some things that happened in the world were unavoidable." He cited the killing of George Floyd by a police officer who knelt on his neck for nearly nine minutes as an event that made him rethink assumptions about "inequality in general, about health outcomes, about access to education. People, me included, are used to the idea of unequal outcomes in a capitalist world. What's clearer now is the extent of the unequal opportunities."

The panelists committed to doing their part through hiring and training to reduce inequities, as they prepare for a post-pandemic world where they have to forge new types of trust relationships with clients, where the work environment will be different and where the challenges and opportunities will change.

"There's more to be optimistic about than to worry about," Glaser said.

Or, as Blanc put it: "I think the insurance industry is incredibly adaptable, and I look forward to seeing what we can do."

Stay safe.

Paul

P.S. To watch the video of the CEO panel or to learn more about the forum, you can check out the IIS site here.

P.P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

Customers are rushing to embrace the digital space. Is your business prepared?

Even before the pandemic, insurance customers were moving to digital channels and demanding the kind of smooth experience they get with Google and Amazon. With customers demanding new types of interactions and agencies and companies needing to increase leads in a world that’s gone from face-to-face to zoom, technology doesn’t have to be intimidating.

Watch this complimentary webinar and learn how to:

understand your customers’ expectations

expand the ways you connect

streamline your communication channels

attract and service customers digitally

Don't miss this free on demand panel discussion. Space is limited, so register today!

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Every year, financial crime becomes more sophisticated, new malware emerges and fraud losses rise. Top that problem up with continuously evolving regulations and hefty non-compliance penalties, and financial institutions are facing an increasingly complex risk landscape.

To compete in the new environment, banks, insurance companies, asset managers and other industry players need to rethink how they approach financial risk management. That’s where artificial intelligence can lend a helping hand. With advanced analytical capabilities, AI can augment human-led risk management activities to drive better outcomes much faster. It is estimated that through better decision-making and improved risk management, AI could generate more than $250 billion in the banking industry.

Insurance companies, banks and fintech startups alike are starting to integrate AI-driven analytics into their financial risk management software. Here’s a roundup of three practical use cases to give you the idea of AI potential.

Accurate fraud detection

The complexity and visibility into multi-channel fraud prevention is a major challenge for financial institutions. Scammers are getting more sophisticated and quickly find creative ways to steal from banks and their customers. Each year, fraud costs over $5 trillion, a sum more than 80% greater than the U.K.’s entire GDP.

To stay agile and quickly respond to threats, banks are augmenting their fraud detection toolkit with machine learning capabilities. The idea behind ML-driven fraud analytics is that fraudulent transactions have telltale signs that algorithms can uncover much more effectively than rule-based monitoring systems. By processing customer, transactional and even geospatial data, they can even spot patterns that seem unrelated and simply go unnoticed by human data analytics.

As a rule, ML algorithms leverage supervised or unsupervised learning techniques for fraud detection. The difference between these two types is that supervised learning-based algorithms heavily rely on explicit labels, meaning that machines need to be repeatedly trained on what a legitimate versus fraudulent transaction is. Unsupervised learning models, in contrast, do not need prior labeling to recognize abnormal activity, so they can continuously update their datasets and detect even previously unknown fraud and abuses.

Credit risk prediction

In simple terms, credit risk refers to the risk of financial loss when a borrower fails to meet financial commitments. And as these non-performing assets continue to grow, it has become imperative for banks to find better and more robust mechanisms to manage default risks.

Advanced ML-driven analytics can do just that. By analyzing a vast amount of financial and non-financial data, trained machine learning algorithms can model credit risk and predict default with a much higher degree of accuracy than traditional methods.

There is no shortage in up-and-coming startups that work on AI-powered credit scoring solutions to help the financial industry fight high delinquency rates. One such example is British startup SPIN Analytics, which has developed its RiskRobot to optimize credit decisions. The solution leverages advanced analytics to forecast credit behavior and credit losses of individual customers and entire credit portfolios.

Effective regulatory compliance

Over the years, the number of rules and regulations that banks and financial organizations need to adhere to has multiplied — EMIR, SFTR, MiFID II/MiFIR, MMF, GDPR. With this raft of regulatory bodies, updates are issued every seven minutes. And, with hefty fines and penalties, non-compliance is not an option.

Handling the overwhelming volume of regulatory change is no easy feat. But recent advancements in natural language processing (NLP), an AI subfield, are bringing us closer to effectively solving the compliance puzzle. With the ability to understand the human language, NLP-based solutions can scan and analyze millions of lines in regulatory content, including legal documents, commentary, guidance, legal cases, to spot applicable requirements much faster — that’s what London-based Waymark offers its corporate clients.

Another prominent regtech player is IBM, which offers its cognitive computing platform Watson to drive down regulatory compliance costs. Trained with the help of Promontory, Watson identifies and tags obligations, guides and controls to facilitate regulatory change management.

The bottom line

The financial risk landscape is changing fast. Staying on top of emerging fraud threats, credit risk and rapid regulatory changes requires a superhuman effort.

AI can augment human intelligence with rich analytics and pattern prediction capabilities to drive fraud and credit risk detection with higher accuracy and at a larger scale. In the regtech space, AI-fueled analytics solutions can significantly accelerate compliance procedures while reducing the costs.

Get Involved

Our authors are what set Insurance Thought Leadership apart.