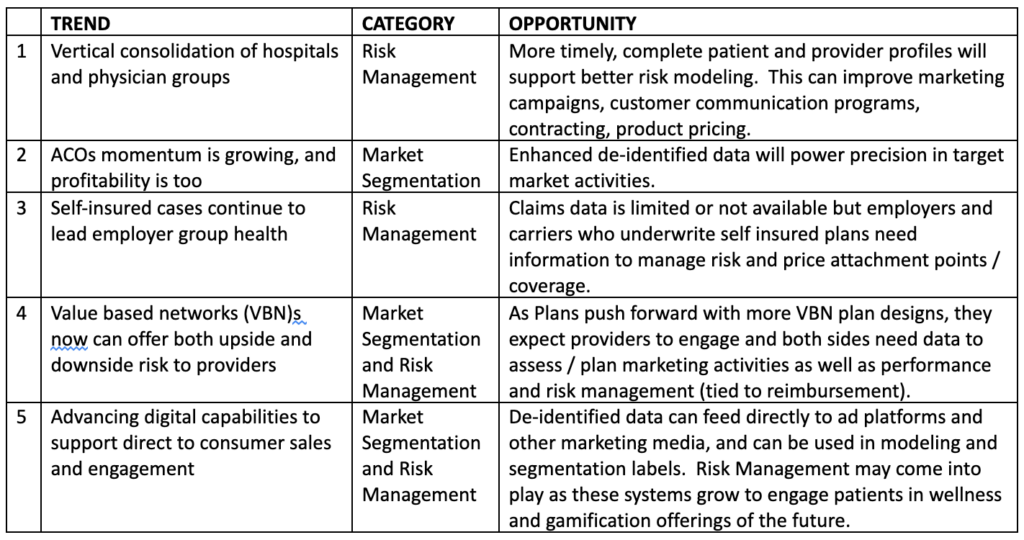

Good people, friends and former colleagues, are losing their jobs as big insurance companies lay off staff. The sliced tether to the mothership has some considering making the jump to insurtech. As a co-founder in the insurtech space with a corporate background, I’ve been getting a lot of calls, and answering the same set of questions: What is the startup scene like, who is hiring, how to get started?

These are logical questions. I even have some decent answers.

These are also the wrong questions. They’ll help you find a job, but they won’t help you understand if you’re going to be excited to get out of bed in the morning or whether an entrepreneurial job slowly crushes you into desiccated powder.

The right question isn’t about logistics – it’s about the internal transition you’ll need to make, and whether you want to live that change.

The right question is: Who do I need to become to thrive in insurtech? (Or really, any corporate to entrepreneurial transition.)

By thrive, I don’t mean start a unicorn. If we knew the steps to do that, 75%-plus of venture capital funds would not fail to make a profit for their investors. I also don’t mean wantrapreneuring – turning not doing into a career. Wantrapreneuring is skating from meetup to meetup, asking for lots of advice about what to do (then pushing back with a strong opinion of how it should be done, all the while not… doing).

I mean, doing the work. Finding an idea. Talking to customers. Convincing a co-founder or two and a team to join you. Or joining the team. Designing the product. Checking the font on every piece of customer communication. Figuring out why your freaking payroll vendor’s system doesn’t just WORK.

And enjoying it. Coming into yourself in this space. Feeling like every challenge stretches you in a new direction. All the while handling the emotional extremes (which I guarantee are rawer and realer than corporate).

So, having had a corporate career before becoming an entrepreneur, here’s my read on the person you’ll need to become:

A shipper, not a soother

You know all those meetings to get opinions on a project before you actually start it? Aimed a little at understanding what your colleagues know, and a lot at tamping down later aggressive politics from people who feel left out?

Just stop.

Draft something, share it with your teammates, tear it up and make it better with their feedback and SHIP IT!

The scales tip the other way here – the issue isn’t that you might offend by putting something on paper, it’s that you’ll never get to your destination if you don’t complete anything. (See wantrapreneur, above).

See also: COVID-19: Technology, Investment, Innovation

I promise you it’s leftover corporate-induced anxiety that’s preventing you from shipping. And you 100% need to find a way to force through it in the entrepreneurial environment. So ship the pitch deck, the blog post, the story, the code. Relentlessly focus on your own output.

(Also, if you don’t write it down, or type it, or draw it, or record it, it doesn’t count. In your head is not done. So do it.)

A no-seeker, not a yes-orchestrator

You know the pre-meetings? The ones you do with your boss’s seven peers to get their input and objections before the big leadership meeting? Your goal is to avoid a no from the big boss, so at least you can keep moving.

That’s not a model for a startup.

Of course you should get lots of feedback (mostly from customers), and of course you should take your partners’ politics into account.

However, the biggest gift in startup life is a quick no.

The biggest gift in startup life is a quick no. (I said it again – this one took me too long to learn.)

And it’s amazing how many people won’t have the decency or understanding to give it to you. A maybe is not a yes. A maybe does nothing but eat up runway. When you’re small, you’re surviving on a shoestring and updrafts of hope. You need to find all-in, strong-yes partners.

And if you’re working hard for the yes that’s not coming, these aren’t your people. Sorry.

A lightning rod, not a moderator

In corporate life, being someone with a “strong personality” will show up in your performance review. “Tone it down,” they say. “Watch the humor,” they say, until you realize you’ve risen in the ranks by sanding down every corner that makes you, well, you. Your personality, your opinions and your willingness to argue something from the heart are the cost of fitting in.

In the startup world, nobody funds boring. Nobody joins boring. Nobody takes a chance on boring. Average gets you nowhere. Inoffensive is a lack of conviction.

Be prepared to own your ideas, your journey, your very self and argue them strongly. Don’t play to the crowd. Better to irritate a few people if it means pulling the ones who can help you into your slipstream.

A doer, not a delegator

Early stage, there’s just too much work and nobody to do it. You can’t set up half your payroll system, design just the principles of a user experience or draft an outline of a letter to a customer – these aren’t partially done – they are an absolute waste of time precisely because they are incomplete, and therefore unusable.

You can’t delegate completion when there’s nobody to delegate to. Do your work all the way to the end. Let go of the perfection of corporate life and the 87 rounds of reviews, and content yourself with a customer letter you think you’d understand and with a quick proofreading.

Oh, and delegate complete tasks, not fragments. You need a team that can also finish their work.

See also: Step 1 to Your After-COVID Future

Transition means change

I don’t buy the arguments that people are either successful in corporate environments or in entrepreneurial environments. That’s accepting a world in which none of us can learn and grow, and in which we’ll never succeed at anything we didn’t try in our 20s. It’s nothing but a package of hubris and negativity all mixed up together.

It is true, though, that corporate and entrepreneurial environments test us in different ways. If you have a corporate job and you want to work at or start a startup, can you find a job or can you start a company? Of course you can, given time and resources.

But can you thrive? You need to be willing to change.

Becoming an entrepreneur is just that, a becoming.

Entrepreneurship strips away our masks, for founders and for team members, both. The fate of the business is in your hands. Your work stands for itself. You stand up for yourself.

So, don’t overweight your thinking to whether you can find a job in the entrepreneurial world. Think about who you’ll need to become to thrive in that space. Does your heart sing with delight when you think about becoming that person?

You, and the people you will work with, deserve that.