I guess you could say growing up in Minnesota and spending most of my life in a climate that is exposed to winter weather almost half of the year has made me an expert in how winter weather can affect the insurance industry.

There is no denying that the recent Arctic outbreak was severe and historic meteorologically. The list of records and stats is very impressive and too long to list here, so I’ll just reference a good tweet thread by Alex Lamers, who is a meteorologist at NOAA weather prediction center.

The main point the insurance industry needs to understand with this extreme cold is that it occurred in the middle of February, which makes it climatologically that much more impressive, because the cold was topping records and stats that usually occur in late December or early January. The other impressive nature of this Arctic outbreak is the duration, which when combined with the time of year makes it that much more important an event.

We know the Deep South can get severe cold, but the prolonged nature of the cold this late into the winter season is a tail event meteorologically.

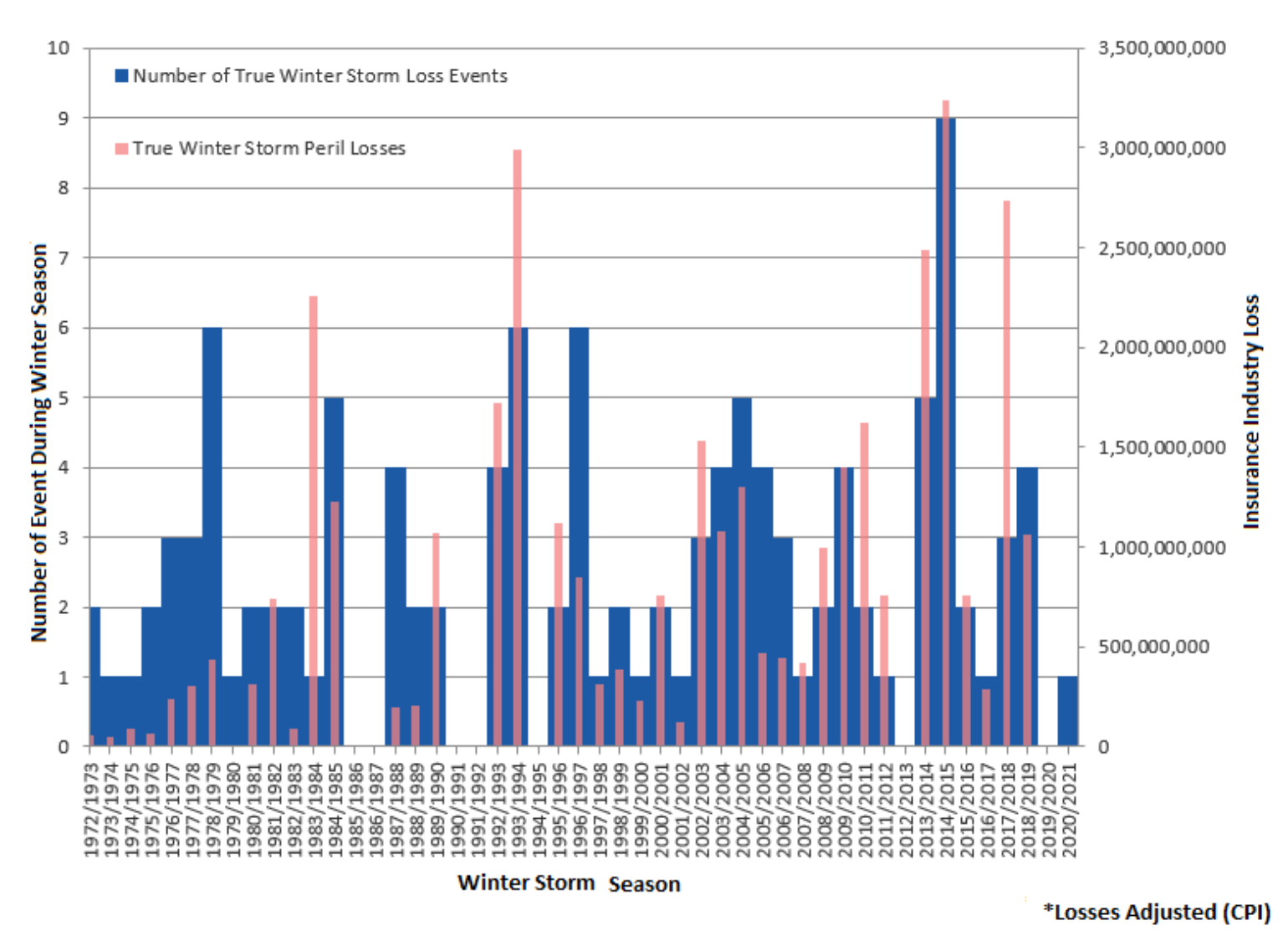

You might have seen several different sources of winter storm loss trends shared across different insurance publications, but one needs to use caution in truly understanding winter storm losses. The best example I like to use is the superstorm of 1993, which lasted from March 11 to 14 and which is often used as a benchmark winter storm loss event for the insurance industry.

It is classified as a winter storm due to its large impacts on the Northeast states with winter weather as the storm developed into a powerful nor’easter. However, over 40% of the loss came from severe weather that occurred in Southern states from a very strong cold front. The largest event loss (35%) impacts occurred across the state of Florida from numerous tornadoes. Although many in the insurance industry reference the inflation-adjusted loss of over $3 billion for the 1993 superstorm, social economics mean the loss was much larger.

BMS RE view of Winter Storm seasonal losses that exclude events with severe weather. You can easily see the current deep freeze will clearly be in a league of its own in terms of true winter weather losses

BMS has taken steps to truly understand trends in winter weather events that only look at flooding, freezing temperatures, ice, snow and wind as possible causes of loss, as shown above.

Only two recent periods meteorologically would be comparable cold weather-related loss events, Dec. 17-31, 1983 and Dec. 21- 26, 1989. Today, these events would have resulted in $2 billion and $1 billion in insured losses, respectively, after adjusting for inflation, with no way really to understand how social-economic factors might have played a role if that type of cold occurred today. The current loss development with the 2021 Arctic blast seems to be several times the magnitude of any cold-weather loss the insurance industry has ever experienced.

This is largely a result of the insurance industry taking the brunt of a compounding event, which will be one of the topics at this year's Virtual Reinsurance Association Cat Risk Management Conference. This winter storm is the latest example of a compounding event to affect the insurance industry, resulting in much higher losses than what should likely be expected from an event.

The cold was historic. It was also the trigger for power outages that resulted in the inability to heat and move water, which resulted in water outage. This compounded into many other impacts, like internet outages and even trash collection delays, making the already miserable situation even worse, and likely a worse insurance industry loss.

If the power had stayed on and the demand could have been met, the losses would not be nearly this bad. Time and time again, we see the long-term lack of electricity compounds the overall insured loss. Hurricane Maria’s impact on Puerto Rico or the compounding impacts of the Tohoku Earthquake in 2011 come to mind as recent examples where the lack of power for a prolonged period had very large compounding impacts on insurance industry loss.

Therefore, is it time for the insurance industry to take a much larger role in the vested interest in helping ensure power grids around the world are reliable during times of disasters? Some might say the opposite is happening due to environmental, social governance impacts. The American Society of Civil Engineers rated U.S. infrastructure a D+.

Maybe in the future, the insurance industry can be at the table during discussions around critical infrastructure, which seems to have a clear impact on insured losses.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Andrew Siffert is vice president and senior meteorologist within BMS Re U.S. catastrophe analytics team. He works closely with clients to help them manage their weather-related risks through catastrophe response, catastrophe modeling, product development and scientific research and education.

For me, one of the best songs by the rock band Queen was "Under Pressure," co-written by David Bowie. The story is that the collaboration was creatively different as the vocal was constructed in a very novel way in one night, where they all contributed different pieces of the song musically and vocally and then put it together to create what is considered one of the greatest hits!

While I love the music, the title reflects what companies are increasingly facing … pressure. How they respond and what they do will define their future.

There are all kinds of “pressure cookers” driving innovation, and they are proving how organizations with foresight are solving issues with rapid planning and prioritization.

Take Instant Pot -- a literal pressure cooker. When Robert Wang developed it, his background in software gave him a model for quick development and for rapid iterations that would perfect the technology quickly. According to an interview with Wang, Instant Pot adopted “continual innovation and highly disciplined product launch cycle (12-18 months), more typical of software development than consumer goods.” Wang had the foresight to integrate the fixed timelines with an aggressive customer feedback loop. This would place pressure on the company to innovate and stay ahead of the competition.

Then consider GM. In September 2020, California’s governor, Gavin Newsom, issued an executive order “requiring sales of all new passenger vehicles (in the state) to be zero-emission by 2035.” Whether it was a coincidence or not, GM announced on Jan. 28, 2021, that “GM would phase out petroleum-powered cars and trucks and sell only vehicles that have zero tailpipe emissions by 2035.” So…a timeline has been set. The race is on. These two announcements will rapidly disrupt an industry, reinventing supply chains and even affecting insurance.

Finally, COVID-19. It has accelerated the need for digital transformation at the same time that it has sent a warning signal to insurers to be ready to adapt to anything. In the Dec. 26 Wall Street Journal article, “Covid-19 Propelled Businesses Into the Future. Ready or Not,” Loren Padelford, vice president at Shopify, summed up the pressure with this comparison:

“Covid has acted like a time machine: It brought 2030 to 2020. All those trends, where organizations thought they had more time, got rapidly accelerated.”

Changes that normally might have taken years unfolded in months, and shifts that began as temporary fixes are likely to become permanent. The disruption of 2020 creates significant opportunities for those in the insurance industry to accelerate their digital transformation, from new customer experiences to new products and services, channels and business models … if we embrace the disruption.

COVID-19 has all of the elements of the pressure-cooker environment that requires foresight, innovation and prioritization. In the case of the insurance industry, transformation to a digital insurance business model is an imperative.

Are Insurer Responses a Mismatch with Industry Pressures?

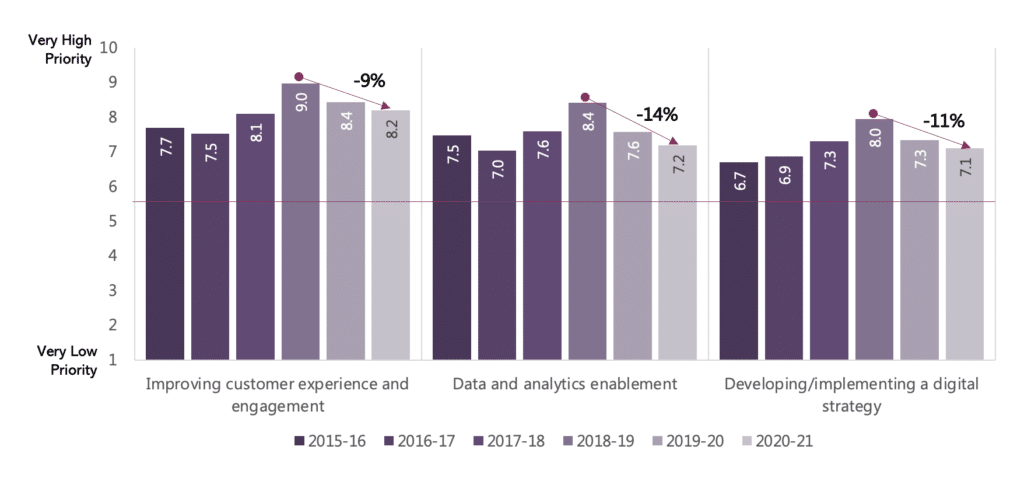

As we explore in our latest thought-leadership report, Strategic Priorities 2021, some insurers have responded to COVID by delaying or stopping strategic initiatives that will drive the future of their business. Fear and uncertainty have resulted in less action and more waiting. Insurers pulled back from previous years with regard to key strategic initiatives crucial for digital transformation. Among 11 initiatives tracked over time, seven show declines (six with double-digit percentage drops) from their peak ratings in 2018-19.

While Improving customer experience remains the top-rated priority, it dropped by 9% (Figure 1). Data and analytics and Digital strategy ranked third and fourth in priority this year but showed even larger declines. This is concerning, given that most insurers are only beginning a digital transformation. They still retain old “portals” to engage customers rather than next-gen customer experience solutions and do not have data foundations to leverage new sources of data that will be required for new products and services, enhanced underwriting and customer experiences. If 2020 taught us anything, it is that digital priorities like these must be accelerated rather than stalled or slowed.

Figure 1: Declining trends in priority of strategic initiatives

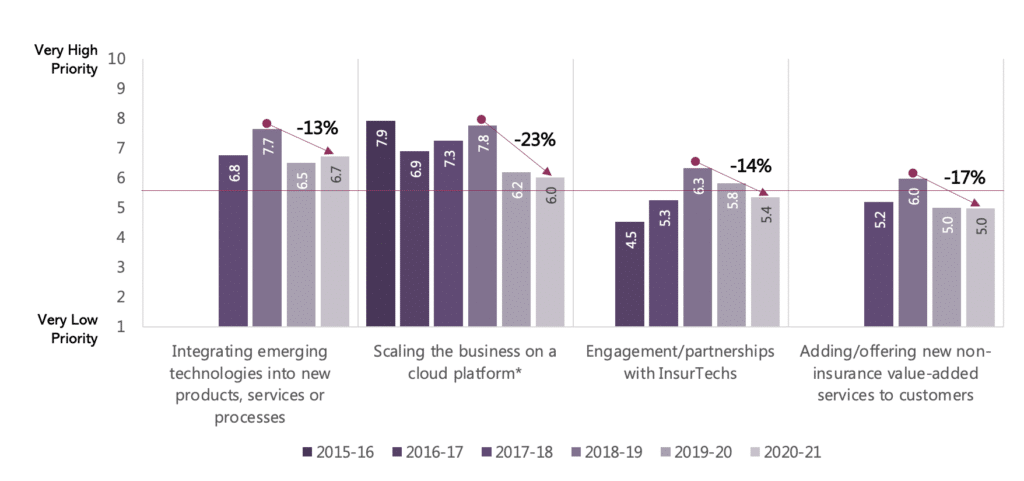

Surprisingly, the largest decline in priority was Scaling the business on a cloud platform, particularly given that cloud became the mantra and requirement for businesses to successfully operate virtually --- from Zoom and Teams to Salesforce, Workday and other crucial systems. The decline is consistent with the historically low legacy replacement activity in the past year and expectations for the next three years. Our research on core systems last year showed that legacy transformations over the last five to 10 years have been to non-platform modern core systems implemented on-premise, rather than cloud and API-enabled platforms. Non-platform solutions do not have the breadth of capabilities needed to digitally transform the business and respond rapidly to market opportunities or changes. Because of this, insurers are recognizing that they must replace these again to optimize the existing business or in some cases stand up a new cloud-enabled core platform to launch products, enter new markets and create a new business model.

These initiatives are four of five (Cost containment, covered below, is the fifth) that define Modernize and Optimize in the two-speed strategy for business transformation. While the overall decline is a discouraging development, particularly in light of the rapid market shifts that COVID has accelerated, when you separate out Leaders from Followers and Laggards, it becomes apparent that Leaders are adapting and accelerating modernization and optimization of the business while the others continue to fall behind. Followers and Laggards must place a higher priority on these initiatives than ever before to remain relevant.

Figure 2: Declining trends in priority of strategic initiatives

Cost containment has been a top-five priority in all six years of our research, growing 17% since the first survey in 2015-16 and holding relatively steady over the past three years. On the other end of the spectrum, Merger and/or acquisition has consistently maintained the lowest priority spot among the list of initiatives, which is interesting given the continued M&A activity in the industry.

Entering/developing new market segments (+8%) and Accessing new capital markets (+9%) saw slight increases or remained flat as compared with the last two years. Two new innovation-themed initiatives added this year showed strong rankings:

Innovation: 7.14, fourth-highest-rated initiative this year

Product innovation for new/changing risks: 6.74, sixth-highest-rated

The strong showing by innovation highlights its continued use as a lever of change within organizations.

Together, these four initiatives define Create a New Business in the two-speed strategy and reflect a positive, growing focus by insurers. Though not shown here, companies that are focused on bringing new products to market rated nearly all the strategic initiatives as higher priority compared with those focused on traditional lines of business for P&C and L&A. This highlights their head start in capturing new markets and customers with new products needed in the future of insurance. The increased priority on developing new products and business models align to customer and market shifts we uncovered in our life and auto customer research last year.

Internal and External Pressures That May Reprioritize Initiatives

Resources from outside the industry, such as Google’s SaaS data and analytics platforms may hasten insurers' adoption of AI and machine learning — effectively re-prioritizing Data and analytics enablement by making it easier to adopt. This is a hallmark of the pressure cooker environment. Which pressures will require insurers to yield, no matter what, and which technologies will simply assert themselves into future planning because they provide simplicity and a ready-made solution?

Another great example of simplification that begs for reprioritization would be the adoption of no code/low code insurance platforms. The internal pressures of IT cost reduction, speed of delivery and talent acquisition make it easy to justify a new model and, hence, should make it easier to make a case for reprioritization.

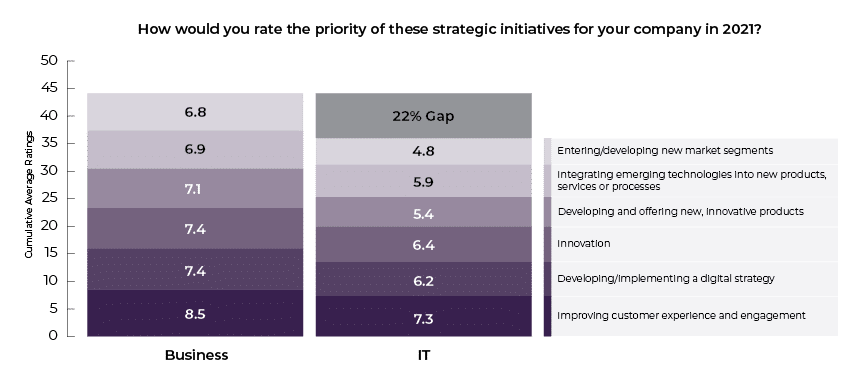

Business and IT Alignment

Accelerating business transformation requires alignment between business and IT more than ever on all of these strategic initiatives. Unfortunately, there is a gap between them by 22% (Figure 3). This gap places insurers at a disadvantage and can affect their ability to innovate and be ready for the future. The gap will drive the business to seek options outside the traditional IT organization, which can create momentum but may also create challenges.

Figure 3: Business-IT gaps in priority of key business transformation initiatives

While these overall planning results are mixed for the industry, the differences between Leaders, Followers and Laggards stand out – highlighting the significant advantages that Leaders have. While many Followers may be keeping relative pace to Leaders with their modernizing and optimizing the existing business, often reflected in strong financials, this is deceiving when considering the future business needed – where Followers and Laggards are falling further behind.

Strategic planning needs to be bold enough to match the velocity and magnitude of the changes the industry faces.

It will no longer be sufficient to allocate most of the resources to maintaining the status quo of the current business. Rather, companies must look to reallocate resources to accelerate in areas they are behind for both speed of operations and speed of innovation. It is not one or the other – it must be both.

If you feel the pressure, we encourage you to download and read Majesco’s report, Strategic Priorities 2021, to see how your organizational priorities stack up against others in the industry. and to see if you are a Leader, Follower or Laggard in preparing for the future of insurance.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Moving Forward

We need to look rigorously at past forecasts and decisions to calibrate how good we are (or, often, aren't), so we can continually improve.

How old do you think Martin Luther King Jr. was when he was assassinated?

That question has been used to help gauge how good people are at making predictions and to help them get better. I'm going to try to build on it here to make a point about the need to look rigorously at past forecasts and decisions to calibrate how good we are (or, often, aren't), so we can continually improve.

The question about MLK is deliberately unfair. How can we be expected to know his exact age? So, pick an age, then give yourself a range, expanding in both directions until you figure you have a 90% chance of having his actual age fall within that range. (Go ahead and write it down. I'll wait.)

The answer: He was 39 years old when he was assassinated on April 4, 1968, in Memphis, Tenn.

Don't feel bad if you didn't realize he was so young: When a group called the Good Judgment Project asked a series of such questions to a broad array of research subjects, it found that people were typically right less than half the time even though they thought they'd given themselves a 90% chance of being correct.

A recent New York Times article described how professionals are not only consistently wrong, like the rest of us, but can be biased. The article looked at the last 15 years of forecasts by top economists about GDP growth in the U.S., made two years in advance. Twelve of the 15 consensus views were too enthusiastic, and the eight biggest errors were all on the side of optimism.

We typically don't recognize our fallibility, either. Research for a book I collaborated on a few years ago found that only 2% of high school seniors ranked themselves as below average on leadership skills, while 25% put themselves in the top percentile. Maybe you could just have a chuckle at high school seniors' poor understanding of averages and percentiles, but 94% of college professors rated themselves above average. Among engineers, who really ought to know better, 32% at one company said they were in the top 5% of performers, and 42% at another company put themselves in that top category.

The idea of revisiting predictions has been a pet project of mine ever since I saw that many of the companies extolled in Tom Peters' book "In Search of Excellence" ran into trouble by the mid-1980s, just a few years after the 1981 publication. "Blue Ocean Strategy," published in 2004, caught my eye because the premise was simplistic -- look for opportunity in the blue ocean, where no one else is, rather than the red ocean, where competition is bloody. While the book became a fad, in the many years since I have seen no example of any company using the book's frameworks to score a major success, beyond the case study about a Nintendo game system cited in the book.

As much as I respected the thoroughness of Jim Collins' research for his books, including "From Good to Great," the 11 companies he cited in 2001 weren't all looking so great -- or even good -- a decade later. Circuit City had gone out of business; the Great Recession had crushed Fannie Mae and hurt Wells Fargo badly; and several others had seen their stock prices decline or rise only slightly. Shouldn't that performance raise some questions about the predictive power of the principles laid out in the book?

Readers don't seem to think so -- the book ranked #362 on Amazon's best-seller list this week, nearly 20 years after publication. But I'd bet that Collins hasn't stopped learning and would welcome some do-overs. For instance, while his "Level 5 leadership" is a laudable concept, the idea that a Level 5 leader can pick a Level 5 successor was never very helpful, because it takes too long to see how the successor does. The concept has now taken a real hit because of the collapse at General Electric. Longtime GE CEO Jack Welch was the exemplar of Level 5 leadership, including for his selection of Jeff Immelt as his successor -- but you practically have to stand in line these days to pillory Immelt, now that GE forced him out in 2017.

Our culture certainly doesn't seem to value accountability much. Political experts confidently tell us things day after day even though they're right about as often as a coin flip. Sports experts on TV tell us some team is a sure bet, only to be wrong and then come back with some equally ironclad guarantee the next week.

But we need to make better decisions in business. There's real money on the line, not just some aspiration for our favorite sports team. And we're not all in the 99th percentile as forecasters, or even above average.

Fortunately, there are ways for you to improve, by calibrating successes and failures and learning from them.

One way might be to take up bridge or poker -- which the Good Judgment Project found correlated with better estimating. One reason seems to be that you keep score and have to see over time whether you're winning or losing. Another is that the games encourage you to be analytical about decisions you've made -- my older brother, a Life Master at bridge, could spend hours considering what he might have done better on a single hand. Even if you don't want to take up a new pastime, you can imagine the sort of mental discipline that a good bridge player or poker player applies to problems.

The Good Judgment Project also found that by providing as little as an hour of instruction they improved forecasting by an average of 14%. Training partly consists of some basic concepts -- no, having a coin come up heads five times in a row does not make it more likely to come up tails the next time -- but mostly consists of "confidence questions" like the one I posed about MLK. Once people learn to become more realistic about what they know and what they don't know, their forecasting improves.

At the C-suite level, learning from mistakes is even more important because the dollar amounts are so much higher -- but calibrating still isn't done nearly as much as it should be. Research for another recent book I helped write found that social dynamics within the senior team often prevented them from conducting a thorough analysis. Those hockey stick forecasts of massive growth from last year and the year before and the year before that just got buried in a drawer when the growth didn't materialize, and those making forecasts were allowed to pretty much start fresh in the new budgeting season. Even when companies tried to analyze past forecasts, success tended to be credited to management while underperformance was written off as due to unforeseeable circumstances beyond management's control.

There's no easy solution at the C-suite level, but it will help to maintain the discipline of making very specific predictions and then revisiting them at the appropriate time to see whether they panned out -- while trying to allow for the tendency to write off failure as bad luck.

When Chunka Mui and I conducted research that was the flip side of Jim Collins for a book we published in 2008 -- while he looked at successes, we spent two years with 20 researchers looking at 2,500 strategic failures -- we decided that our lessons learned had to have predictive power, or they were no good. So we started a blog and made predictions for a couple of years about major strategy announcements that we were sure would crater. We were right, too, on something like 49 of the 50 predictions we made. (We gave up on the site years ago, so I can no longer do an exact count.)

So, good for us, right? Well, we were also lucky. We were all set to make our boldest prediction around the time of the book launch but got some really smart pushback. We dropped an attempt to get a national newspaper to publish our thoughts and never even posted them on our blog. Good thing, too -- the deal has been a raging success.

I've still taken the near-fiasco to heart and think of it from time to time as I try to help myself understand where the weaknesses are in how I think. (I've started playing bridge again, too.)

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

First, create a list of questions to ask your HR team.

Before you set up your new work-from-home space or even if you've already left the office to go remote, circle back with your HR team to understand how you’re covered if you experience a work-related issue at home. Start with these questions:

May I take my work equipment with me? If so, what is covered in case of an accident?

What happens if I get injured during my time working from home?

Am I covered through my work?

If so, how do I file a claim?

Start to separate business equipment from your personal electronics.

Typically, headsets, desktops and screens that are owned by your company would not fall under your homeowners insurance -- even if you’re working remotely. However, if you’re doing work on a personal computer for business use and have a theft or loss, there may be limits on personal property coverage.

Enroll in a comprehensive homeowners insurance plan.

Most Americans are required to purchase home insurance with their mortgage, but the home office coverage limit may not cover the range of equipment you’re bringing home from your employer. If you’re going remote, understand what items your company owns and what is a personal item being used for business. Do an inventory of personal items like laptops, monitors, printers and voice headsets to make sure your coverage limit lines up with what your stuff is worth. We’ve found that video logs work great for this.

Or, do a thorough review of your existing homeowners policy.

When you go remote, the occupancy of your home may shift drastically from 30% of your time to 100%. And, during the day, you're up and moving around, while at night you’re usually asleep. The increase in activity could increase the probability of a claim in your home, especially if you’ve got kids home from school.

Request an increase in your personal home office limit (if you need it).

The average homeowners policy in the U.S. has a $2,000 limit for home office equipment. As more people have office setups at home, homeowners can request higher limits, if necessary.

Storage of business inventory could increase your personal limits. If you’re unable to make it into the office and must begin storing your company’s products or materials at your home, then speak to your company first or call your homeowners insurance company to make sure you’re covered before you take on the responsibility of business inventory.

Increases in foot traffic could boost your personal limits.If you’re going to be remote for an extended period and are thinking about bringing clients to your home, then you’re assuming liability for those guests as they come onto your property. Check with your insurance company to make sure you’re covered appropriately.

If remote working turns into a permanent thing.

Home-based businesses usually require more coverage than standard personal limits. If you decide to stay remote, check with your homeowners insurance company on what coverage limits it offers and ask for endorsements.

Remember, adapting to a new work environment takes time.

If you’re already thinking about your insurance coverages, then you’re ahead of the game. But be sure you’ve set up your new working environment in a safe way. Think through the different scenarios that could lead to physical harm or injury, like loose electrical cords or leaving the stove on when you have the ability to cook lunch instead of buying it. New environments take some time to get used to.

Energy costs may go up when your family members are home during a time of day when your home is usually at its lowest point of energy consumption. Try offsetting the drawing of power and energy throughout the entire day with some energy saving devices and LED lights.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

The age of insurtech has brought a wave of new digital experiences and automation in insurance. From websites that instantaneously compare auto insurance quotes to mobile apps that allow us to submit claims directly by snapping a picture of a damaged window, we continue to benefit from significant improvements to the insured experience.

These improvements in distribution and claims are part of an industry-wide appetite for increased accuracy and efficiency, including in underwriting. Personal lines carriers have already made good strides, and carriers see a similar opportunity to improve loss and expense ratios in commercial lines.

For small business policies that involve a high volume of submissions and lower premiums, the challenge is to enable an efficient, high-throughput underwriting process that complies with exacting standards for quality. In the mid-market, the stakes are even higher for underwriters. They must be diligent about selecting high-quality risk against a backdrop of declining capacity and a tsunami of submissions from brokers who remarket risks in search of better rates.

While the goal of shorter time-to-quote is laudable, and addresses a critical frustration for insureds and brokers, the implementation often overlooks the crucial role that underwriters play. By failing to listen to underwriters' needs and play to their strengths as expert assessors of risk, technology providers and insurers alike continue to achieve sub-optimal underwriting outcomes.

Commercial underwriters are at the forefront of some of the most challenging and important work in the industry. They serve a multi-faceted role: developing and fostering relationships with brokers, exhaustively reviewing submissions, validating an insured's business and property information, analyzing exposures and, eventually, rating, quoting and binding policies. Underwriters must bridge the gap between carriers that set aggressive goals for profitable premium growth and brokers who want a quote "yesterday" -- and often pair incomplete submissions with demands for a rapid turnaround.

When underwriters conduct a thorough investigation of the risk – executing online searches, ordering inspections and asking tough questions, they’re invariably perceived as being too slow, inflexible and uncooperative. If they compromise on thoroughness to increase throughput, or if too many submissions are superficially passed through, their book may grow quickly, but the quality and profitability will suffer. All the while, underwriters want to deliver a comprehensive policy that best addresses the insured’s needs and grows the relationship. Reconciling these often-conflicting priorities is difficult but sets the most effective and experienced underwriters apart.

Data analytics, artificial intelligence and machine learning can make a big difference but, for most insurers, have failed to deliver great value within underwriting.

Improving outcomes requires an approach that combines the best of underwriter judgment with machine intelligence.

Specialized, AI-powered software can now do much of the heavy lifting for underwriters, while eliminating frustrating activities. Underwriters who experiment with, and embrace, new technologies are already setting themselves apart from their peers. They stand to improve their individual performance and also help to chart the future course of underwriting within their organizations.

For insurtechs to truly deliver on their collective promise, they need to empower those who are actually performing the work of insurance. Automation and machine learning need to be force multipliers for underwriting excellence – not poor substitutes for it. Getting this right will lead to a better experience for the insured and superior outcomes for the industry.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Within the Biden administration's first weeks, the Office of Science and Technology Policy has been elevated to a cabinet-level position. Biden has appointed Alondra Nelson as deputy director. She is a scholar of science, technology and social inequality. In her acceptance speech, Nelson shared, "When we provide inputs to the algorithm, when we program the device, when we design, test and research, we are making human choices." We can expect artificial intelligence (AI) bias, ethics and accountability to be more significant issues under our new president.

The financial services industry has a long and dark history of redlining and underserving minority communities. Regardless of regulation, insurers must take steps now to address the ethical concerns surrounding AI and data.

Insurers are investing heavily and increasingly adopting AI and big data to improve business operations. Juniper Research estimates the value of global insurance premiums underwritten by AI will exceed $20 billion by 2024. Allstate considers its cognitive AI agent, Amelia, which has more than 250,000 conversations per month with customers, an essential component of its customer service strategy. Swiss Re Institute analyzed patent databases and found the number of machine-learning patents filed by insurers has increased dramatically from 12 in 2010 to 693 in 2018.

There is no denying that AI and big data hold a lot of promise to transform insurance. Using AI, underwriters can spot patterns and connections at a scale impossible for a human to do. AI can accelerate risk assessments, improve fraud detection, help predict customer needs, drive lead generation and automate marketing campaigns.

However, AI can reproduce and amplify historical human and societal biases. Some of us can still remember Microsoft's disastrous unveiling of its new AI chatbot, Tay, on social media site Twitter five years ago. Described as an experiment in "conversational understanding," Tay was supposed to mimic the speaking style of a teenage girl, and entertain 18- to 24-year-old Americans in a positive way. Instead of casual and playful conversations, Tay repeated back the politically incorrect, racist and sexist comments Twitter users hurled her way. In just one day, Twitter had taught Tay to be misogynistic and racist.

In a study evaluating 189 facial recognition algorithms from more than 99 developers, the U.S. National Institute of Standards and Technology found algorithms developed in the U.S. had trouble recognizing Asian, African-American and Native-American faces. By comparison, algorithms developed in Asian countries could recognize Asian and Caucasian faces equally well.

Apple Card's algorithm sparked an investigation by financial regulators soon after it launched when it appeared to offer wives lower credit lines than their husbands. Goldman Sachs has said its algorithm does not use gender as an input. However, gender-blind algorithms drawing on data that is biased against women can lead to unwanted biases.

Even when we remove gender and race from algorithm-models, there remains a strong correlation of race and gender with data inputs. ZIP codes, disease predispositions, last names, criminal records, income and job titles have all been identified as proxies for race or gender. Biases creep in this way.

There is another issue: the inexplicability of black-box predictive models. Black-box predictive models, created by machine-learning algorithms from the data inputs we provide, can be highly accurate. However, they are also so complicated that even the programmers themselves cannot explain how these algorithms reach their final predictions, according to an article in the Harvard Data Science Review. Initially developed for low-stakes decisions like online advertising or web searching, these black-box machine-learning techniques are increasingly making high-stakes decisions that affect people's lives.

Successful AI and data analytics users know not to go where data leads them or fall into the trap of relying on data that are biased against minority and disadvantaged communities. Big data is not always able to capture the granular insights that explain human behaviors, motivations and pain points.

Consider Infinity Insurance, an auto insurance provider focused on offering non-standard auto insurance to the Hispanic community. Relying on historical data, insurers had for years charged substantially higher prices for drivers with certain risk factors, including new or young drivers, drivers with low or no credit scores or drivers with an unusual driver's license status.

Infinity recognized that first-generation Latinos, who are not necessarily high-risk drivers, often have these unusual circumstances. Infinity reached out to Hispanic drivers offering affordable non-standard policies, bilingual customer support and sales agents. Infinity has grown to become the second-largest writer of non-standard auto insurance in the U.S. In 2018, Kemper paid $1.6 billion to acquire Infinity.

Underserved communities offer great opportunities for expansion that are often missed or overlooked when relying solely on data sets and data inputs.

Insurers must also actively manage AI and data inputs to avoid racial bias and look beyond demographics and race to segment out the best risks and determine the right price. As an industry, we have made significant progress toward removing bias. We cannot allow these fantastic tools and technologies to enable this harmful and unintended discrimination. We must not repeat these mistakes.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Nick Frank is a partner with Simon-Kucher, where he leads the North American Insurance practice.

He has more than 20 years of experience helping insurance carriers and producers reimagine sales, product design and revenue models. Frank has worked closely with insurance leaders to implement advanced digital technologies to improve sales funnel ratios, refine customer segmentation and optimize pricing. His expertise spans across property and casualty, life and annuities, reinsurance carriers and producer organizations.

Frank has a BSc in computer engineering and mathematics from the University of Florida.

Wei Ke, Ph.D. is a managing partner at Simon-Kucher. He heads the company's financial services activities in North America. Ke has advised leading financial institutions on many topics.

As we reflect on all that occurred during the turbulent and chaotic year that was 2020, one thing stands out: It was a year of innovation. Virtually every business that survived, and most that thrived, innovated in some fashion, whether it was their business models, efficiency improvements or communications.

These innovations, while necessary to survive pandemic-related economic challenges, are all the more remarkable because the coming decade will represent an even bigger innovation challenge to independent agencies — perhaps more than at any other time in industry history.

Due to the unprecedented volume of owner retirements, consolidations and even startup activity, the composition of the industry is changing rapidly. Agency business models are evolving. Forcing this change are customer demand, new ways of marketing, carrier challenges, talent shortages, a rapidly evolving economy and rapidly evolving technology.

Evolving Technology Investments

The biggest technology challenge to confront agencies this past year was spurred by the need to isolate workforces and virtualize. Many agencies were forced to make unplanned investments in computers, software for managing a distributed workforce and, in many cases, upgraded cyber protection. For more than a few agencies, these unplanned investments were financially painful.

It is also possible — even likely — that the useful life of these investments will be measured in months rather than years. This faster evolution of technology tools is likely to represent a new paradigm for agents who want to maintain their competitiveness. Agents have traditionally been conservative when making capital investments, typically expecting many years of service and utility from them. But those who want to stay on the cutting edge will need to adjust their mindset and acknowledge that instead of 10 years of service from a new investment, they may only see three.

This trend clearly affects an agency’s return on investment, and it will be wise for agents to consider the impact on their bottom line. Agencies will need to grow larger and faster or accept lower margins. One piece of good news is that the technology that agencies need to invest in, whether websites, software or communications technologies, increasingly can be purchased on a per-use basis, or on a software as service basis (SAAS). This trend makes typical capital items, which are fixed costs to the balance sheet, variable expenses to the income statement.

One area where agencies will need to invest significant sums are web portals, websites and web-based communication. With customers demanding self-service capabilities with 24/7/365 communications access, agents can no longer consider a website as just an electronic brochure. Websites must be connected to the agency management system and need to allow customers to serve themselves directly in a variety of ways.

To meet these demands, today’s websites are necessarily more robust and need to be rebuilt more frequently than in the past. Where an agency might have gotten five years of effective use out of a website, in some cases even longer, the future will demand website redevelopment projects every two or three years.

Changing Business Models

As agencies grow ever larger due to consolidation and aggregation, the insurance distribution marketplace must grow more competitive. Agents will be forced to offer products, services and access that they may have avoided up until now, or face losing business at the margins to larger, more relevant competitors.

Again, the choice will be between lower revenue, lower profits due to loss of business or potentially lower margins due to increased investment. This will force agency principals to focus on cost control, efficiency and sound business practices more than ever before. While technology-driven efficiency will lower costs as producers and service employees manage ever larger books of business, agencies will need to acquire new human capital in the form of data scientists, sophisticated business managers and data-driven marketers.

Many observers expect the number of independent agencies to decrease from roughly 35,000 today to between 20,000 and 25,000 within 10 years. This trend is expected due to the factors discussed here, but also, in some cases, because of an agency’s failure to maintain itself as a going concern.

Those agencies that meet the challenges and make this transition will be similar in some respects to today's agencies. They will be serving clients who value the relationships they have and the expertise they bring. But the survivors will need to innovate to be nimbler and more cost-efficient than ever before. They will need to make more frequent investment in changing technology and in staff and become better businesspeople than ever before.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Much of North America is seeing lower interest rates across the board, which bodes well for consumers making large purchases but puts the insurance industry under intense scrutiny. Carriers with bond-heavy portfolios may see a decline in returns and, as a result, lower profit margins. Despite the insurance industry’s overall acceleration toward technology in 2020, carriers of all lines of business will need to move much more quickly – or risk falling even further behind their profit margin.

Insurers should cut unit costs, but not corners.

Insurers must cut costs; however, with more consumers requiring personalized attention from their insurance company, insurers must walk a fine line. Reducing expenses may be necessary, but insurance companies must be careful not to lose their existing customers in the process. Automation -- especially a newer form, called cognitive process automation (CPA) -- allows for reducing costs while still providing the service that customers require.

In some departments, such as underwriting and billing, insurance companies should prioritize responsivity for a more convenient customer experience. This can be done by using process automation to streamline communication between the carrier and the policyholder.

In other departments, such as claims, policyholders will appreciate careful and attentive human interaction. While responsiveness is still paramount, customers will have more trust in the company’s claim-handling process when they have access to a dedicated claims adjuster.

Where resources are scarce, technology is a viable solution.

Even prior to the impact of COVID-19, carriers like Protective Insurance had begun implementing CPA, a more advanced version of robotic process automation (RPA).

Many carriers have at least discussed the features and capabilities of RPA. However, RPA and even intelligent process automation (IPA) products are primarily limited to structured data.

CPA is the new disruptor in both the insurance and automation industries. Combining the repetitive abilities of traditional RPA with artificial intelligence (AI) and machine learning, CPA relies on bots that capture data and scan documents via optical character recognition (OCR) but that also do much more. The bots can fully automate entire underwriting and claims processes, from start to finish, with minimal human intervention.

As an example, policy underwriting has traditionally been considered a manual undertaking, but CPA has demonstrated that underwriting can be largely automated -- everything from policy submission to risk rating and underwriting to issuing declinations and binders. Using CPA, insurers can write more new business, streamline the renewal process and even detect cases of potential fraud with minimal human supervision.

Claims departments can significantly reduce the manpower needed for largely repetitive processes. Bots programmed with CPA can fully automate the first notice of loss (FNOL) process, fraud investigations, benefits calculations and even payments. In fact, time-consuming processes like claims communications can be automated up to 95%.

Employees can instead focus on more engaging tasks and provide better service on edge cases.

Increased efficiency is more remunerative than reduced overhead.

In cutting expenses, the matter of efficiency is sometimes overlooked. If time is money, shouldn’t carriers condense time-consuming processes, as well?

Automation saves time and money. Whenever carriers optimize a process by implementing an automation solution, a precious resource has been created: time.

As the policyholder mindset continues to grow in favor of more personalized experiences, cognitive automation allows insurance carriers to use their best asset – their human workforce – to focus on retention efforts, customer satisfaction and even cross-selling additional lines of business. At its heart, insurance is a people-focused business, and even tech-friendly consumers prefer personalized human interactions.

The takeaway

With lower interest rates threatening profit margins, insurance carriers must target cost reductions – and sooner rather than later. Companies can use new process automation tools, such as RPA and CPA, to cut redundant work often found in underwriting and claims departments. Insurers are then able to reprioritize the focus of their workforce on customer retention, or even scaling for growth.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Chaz Perera is the co-founder and CEO of Roots, a company pioneering the use of AI agents to revolutionize the workplace.

In his 20-year career, Perera has led teams as large as 7,000 people across 50 countries. Before co-founding Roots, he was AIG’s chief transformation officer and also its head of global business services.

Open insurance is about sharing vast and ever-growing volumes of structured data in a digital ecosystem to stimulate the creation of innovative insurance-related propositions for consumers. When customers are made the focal point of new digital business models, new opportunities continuously arise for cross-sectoral partnerships, platforms or collaborative efforts.

This means that it is crucial for insurance companies to allow third parties (e.g. banks, fintech, aggregators, mobility providers, etc.) to access their data, products and services, and also for them to be present – and relevant – in their customers’ digital ecosystems. Like open banking, open insurance initiatives drive API-enabled access to insurance data, products and services.

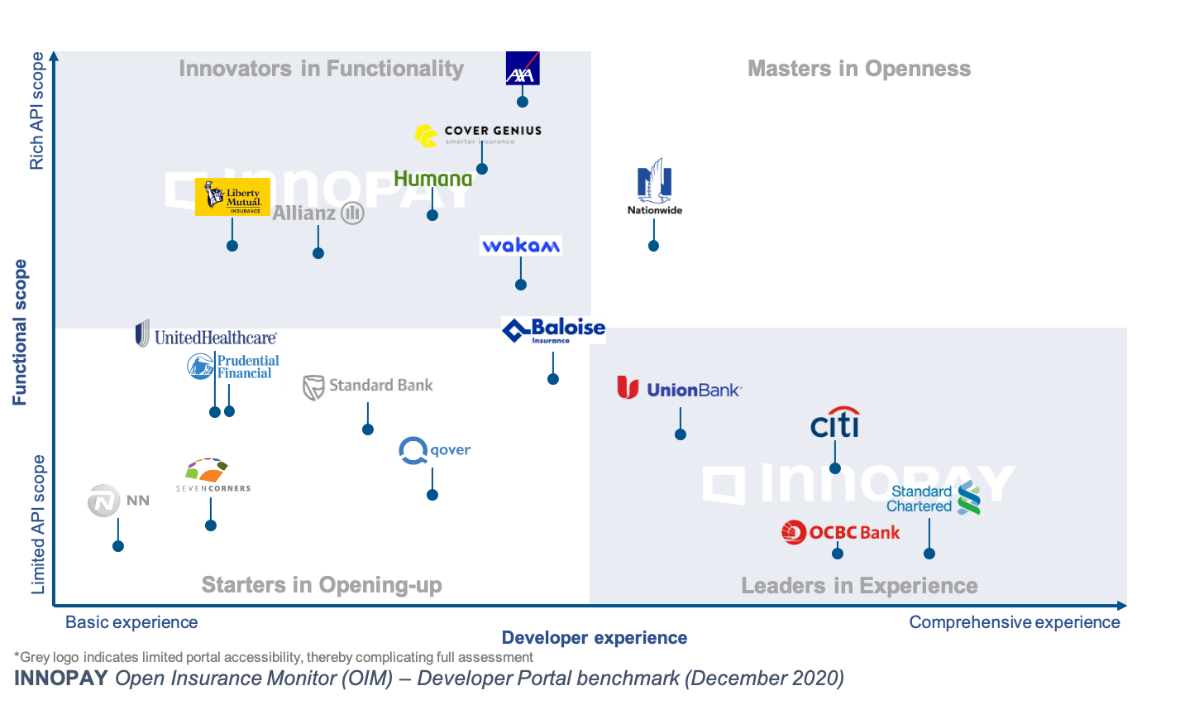

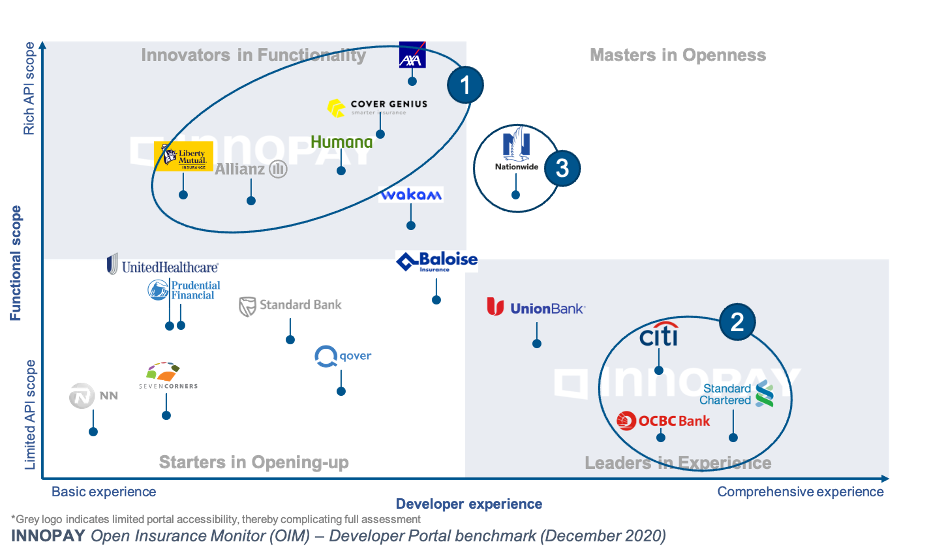

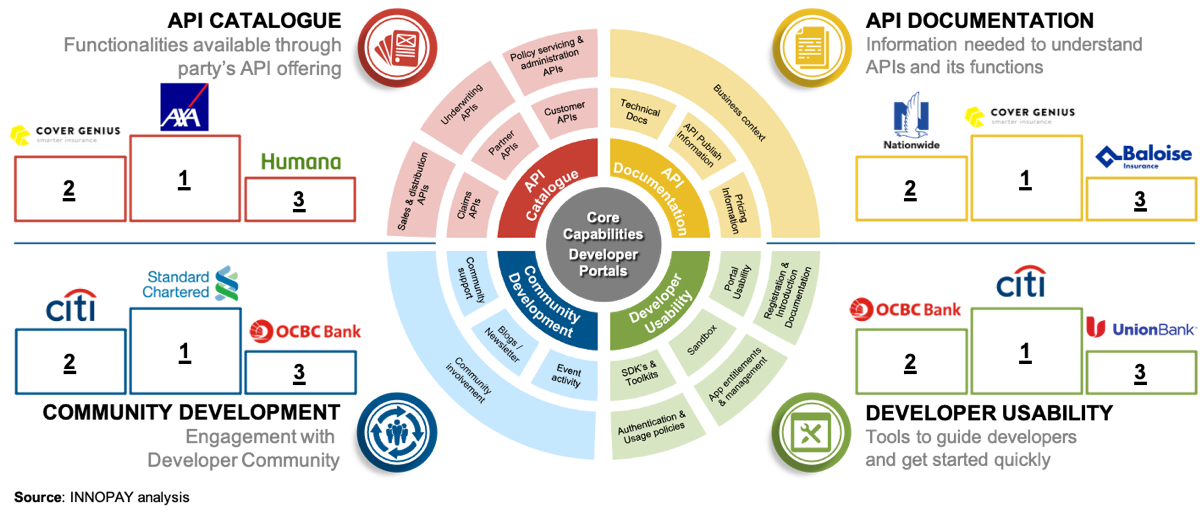

The Open Insurance Monitor presents how the insurance industry is developing towards open APIs

Figure 1: Overview of the Open Insurance Monitor

A rich API portfolio supports the best service provision toward customers and partners within third-party platforms. It is also important for insurers to offer a good developer experience to create the optimal environment for collaborative partnerships and innovation. INNOPAY, a consultancy, has launched the Open Insurance Monitor (OIM) to continuously measure and benchmark this functional scope of APIs and developer experience offered in the insurance landscape (see figure 1). OIM considers organizations around the world that publish insurance APIs via developer portals, including insurers, insurtechs and banks.

Three key insights from the Open Insurance Monitor

Figure 2: Insights from the INNOPAY Open Insurance Monitor

1. Lack of focus on developer experience

The OIM reveals that insurers’ first efforts are mostly aimed at establishing a rich API portfolio with insurance-related functionality, with minimal focus on the developer experience.

The top left corner of Figure 2 shows several insurers leading the way as innovators of functionality. AXA offers a wide variety of functionality in most components of the insurance value chain and for multiple types of insurance products. These services include quoting and selling insurance, claims management and service-provider support during the execution of services to clients. Cover Genius also offers services in multiple components of the value chain, including services for product origination as well as claims management. Health insurer Humana provides a wide variety of API services such as enrollment in medical care programs, retrieval of medical information and supporting functionality for medical professionals during the execution of services.

Analysis reveals that insurers are still only in the early stages in terms of creating the developer experience. Although most insurers have taken initial steps in providing API documentation, there is a strong focus on the technical aspect or specifications of APIs. The developer experience could often be further improved by increasing developer usability (e.g. tools, tutorials) and engaging with the community to spur collaboration and innovation.

Unsurprisingly, the banks included in the OIM offer a more advanced developer experience due to their open banking efforts and investments. Extending their API portfolios with insurance services would further boost their bancassurance models.

The OIM identified a small group of banks that offer insurance services through APIs. This is the next wave of bancassurance and is an interesting revenue model for open banking. Thanks to their open banking capabilities, the banks included all have a solid basis in terms of API documentation and developer usability. Standard Chartered sets itself apart through features for community development such as regularly posting news articles and organizing hackathons and other types of events. OCBC emerges as a good all-round player in all components of developer experience, while Citi stands out in terms of developer usability by supporting fast onboarding and providing instruction guides for calling APIs, authentication and the sandbox environment. However, the scope of insurance-related functionality at these banks is still limited. If they decide to extend their API portfolios with related services, they will move toward becoming masters in openness, which will boost their bancassurance models.

3. Insurers are lagging behind in openness

Benchmarking against the masters in openness (e.g., National Bank of Greece and Deutsche Bank) reveals that insurers still have a long way to go in terms of openness. In fact, out of all the parties analyzed, only one is currently a master in openness: the U.S.-based insurance company Nationwide, thanks to offering a variety of insurance APIs plus enhancing the developer experience through clear documentation and good developer usability.

Nationwide’s extensive API portfolio currently consists of a variety of services for information retrieval, insurance quoting and issuing policies as well as APIs aimed at policy servicing. Portfolio extension could be achieved by including API services for managing claims and supporting service providers. Besides providing clear technical API documentation, Nationwide sets itself apart from other developer portals by emphasizing the business potential of its APIs through feature display and use cases, as well as offering good developer usability.

No overall winner

As with open banking, there is currently no overall winner in the open insurance landscape based on the developer portal capability model, as depicted in Figure 3.

Figure 3: Scoring per capability, based on the INNOPAY Developer Portal capability model

In this week's Six Things, Paul Carroll takes an early look at the International Insurance Society's annual survey of global insurance executives, which found that only 35% had an active, comprehensive plan for innovation -- meaning that two-thirds do not. Plus, 4 connectivity trends to watch in 2021; the intersection of IoT and ecosystems; closing the protection gap; and more.

In this week's Six Things, Paul Carroll takes an early look at the International Insurance Society's annual survey of global insurance executives, which found that only 35% had an active, comprehensive plan for innovation -- meaning that two-thirds do not. Plus, 4 connectivity trends to watch in 2021; the intersection of IoT and ecosystems; closing the protection gap; and more.

The 2020 Global Concerns Survey of insurance leaders by the International Insurance Society contains two major surprises. (I got an early look because ITL collaborated on this latest annual survey.)

The smaller surprise is that COVID-19 ranks only second among the most important issues the executives identified. I had expected that the pandemic would be the top concern, given that 2.4 million people have died worldwide, that economies have been devastated and that insurers face exposure, especially given the recent decision by the U.K. Supreme Court that business-interruption insurance should cover pandemic-related claims.

The bigger surprise is that, while innovation is the top concern, only 35% of respondents said they have an active, comprehensive plan — meaning that two-thirds do not... continue reading >

While the pandemic has greatly accelerated the digitization of the insurance industry — turning years into months — it has also shown us how very far we still have to go. As a rule of thumb, I’ve heard consultants say that 50% of the operating costs need to be driven out of the industry in the next five years.

Blockchain has held out this promise for some time now. It’s lost a bit of its shine because it’s been identified as a hot technology of the year for so many years in a row. But it may be coming into its own, with some uses starting to move into production.

Having explored the possibilities for blockchain in personal lines and commercial lines in P&C, we conclude our webinar series on the technology by taking a look at two use cases in life and annuities that are close to moving into production.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.