When was the last time you sent a fax? For that matter, how many in-person meetings have you had this year? From the first cellphone call in 1973 to the first text message sent in 1992 to the rapid adoption of online meeting platforms in 2020, people are constantly exploring and adapting to new technology quickly, with many embracing the next digital update wholeheartedly. Unfortunately, the same cannot be said about the insurance industry, which is mired in antiquated business activities.

Insurance is an essential safety net for people, but often the industry relies on outdated business models and systems, some based off mortality tables that were developed in 1971 and 1984. At the same time, industry leaders have refused to embrace technology so much so that, in a Center for the Study of Financial Innovation survey about the risks facing insurers, insurance companies ranked outdated technology as the greatest threat to their business.According to a McKinsey report, nine out of 10 insurance companies identified legacy software and infrastructure as barriers to digitization.

Many corporations rely on the mentality of, “It’s worked for 100 years, so why fix it?” This became even more evident during the COVID-19 pandemic when many consumers, quarantined at home, turned to digital channels to find solutions to their insurance needs but found a lack of digital adoption. This doesn’t just prevent companies from gaining new clients but also alienates existing ones. According to a Bain & Co. brief, consumers who encounter problems in their digital interactions tend to give their insurance provider lower loyalty scores.

While there has been a plethora of data to help insurance companies create more responsive products and attract new consumers, most insurance companies analyze only dozens of different variables -- many based on that data from decades ago -- to arrive at their numbers.

By contrast, cloud-based artificial-intelligence (AI) assisted software can process 6 billion records composed of mortality, consumer demographic, health and social trends. The result is more precise, dynamic, insurance-oriented algorithms than can be leveraged throughout the insurance value chain.

In fact, cloud-based AI can compare thousands of variables simultaneously in a few hours. The resulting analytics and algorithms are easy to interpret and integrate into insurance processes that enhance pricing, risk assessments and customer acquisition, resulting in a data-driven competitive edge.

A robust, full-stack, Insurance-as-a-Platform (IaaP) approach can quickly and robustly analyze and process all of this data to help insurance companies more precisely determine risk, create better, more appropriate products for their clients and improve customer experiences. This enhanced data can also help insurance companies price products more accurately, understand the demographics of who is ready to buy and when they are ready and get the right risk on their books — making them and their agents more profitable in the end.

Insurance companies that embrace technology will be the ones that succeed. Insurtech companies can help them succeed by providing data-based recommendations for competitive product pricing, to create products that consumers want and to improve the insurance-buying process, making it easier for both the client and the agent.

In a digital world, data -- and the ability to fully analyze it -- is critical to insurers’ survival. The businesses that will succeed will be the ones that can quickly analyze and adapt to data to make better business decisions and serve their customers better and faster.

Now, agents will never be left out of the equation. They are the ones who develop relationships and build personal networks — an agent serves as a place of trust. But the future of insurance is a hybrid where consumers can choose a digital experience or a traditional one and move between the two.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

EY’s Global Insurance Consumer Survey reveals how insurers can support the needs of those affected by the COVID-19 pandemic.

In brief

Insurers must evolve to meet changing consumer behaviors and priorities caused by the pandemic.

The greatest opportunity for insurers lies with those most financially affected.

Pervasive and contentious social issues call for insurers to engage, collaborate and lead the development of new solutions.

In late 2020, EY Insurance conducted a global survey of 2,700 consumers and 1,200 small business owners to understand how the pandemic has affected their lives. Our survey of consumers focused on their needs for personal lines and life and retirement insurance products.

To better understand the concerns and product preferences of respondents, we grouped these individuals into three segments: most financially affected, moderately affected and least affected. Across all segments, there are clear opportunities based on consumers’ shifting priorities:

Consumers are seeking to restore their financial well-being and security, with more than half of respondents saying they plan to save more as a result of COVID-19.

Those who experienced the greatest financial distress from the pandemic intend to minimize future financial risk and uncertainty.

The most affected consumers are socially active and place a high value on social responsibility in their insurance purchasing decisions.

Our survey confirms what we’ve heard from senior insurance executives across the industry: This is a moment of opportunity for the industry to increase its relevancy and live its purpose by playing a critical role in the recovery of consumers and the wider economy.

To play such a role, insurers will need to develop innovative products that align to consumers’ evolving needs and provide tangible value.

How the pandemic has affected insurance consumers

Our methodology allowed us to identify the extent to which the pandemic has affected the financial state of respondents in each country. As exemplified in the chart below that displays data from our life insurance findings, there is a sizable difference in impact between those most financially affected and those least affected. For instance, 54% of the most affected experienced a loss of a regular work schedule to a great degree, and 56% lost income to a great degree. Among the least affected respondents, those figures were 0%.

While the most affected consumers are typically younger (70% are under the age of 45) and less affluent than overall respondents, they are not exclusively from these sociodemographic groups. For example, in the U.S., 56% of the most affected respondents held at least one college degree, and 40% earned over $100,000 a year.

The survey also explored respondents’ concerns for the future and their appetite for insurance products. The most and least affected reported similar concerns and insurance needs, suggesting a widespread feeling of vulnerability and anxiety in a world already defined by geopolitical tensions, growing inequality and threats from climate change.

How the pandemic is shifting preferences on protection

Finding financial well-being through cost-effective alternatives

Looking at life insurance and retirement, the top concerns can be directly linked to the health and financial impacts of the pandemic: Fear of losing a loved one is by the far the greatest concern, followed by financial well-being. In seeking financial security, consumers are most interested in products that cover loss of income, credit card bills and other existing financial commitments.

Given the heightened financial anxiety and focus on financial well-being, consumers are seeking cost-effective insurance alternatives, such as policies with lower premiums. Consumers also express willingness to provide personal data or wear a fitness tracker in exchange for a discount or customized monthly rates.

From the perspective of personal lines, behavioral change brought about by the pandemic is reflected clearly in the results. For instance, cyber fraud as a result of increased time online was the respondents’ top concern, followed by paying for insurance for a car that’s being driven less. Consumers are also more interested in usage-based insurance and home-protection products.

Given that remote working is expected to continue for many employees, insurers should develop products suited to the “new normal,” such as home-protection and usage-based policies.

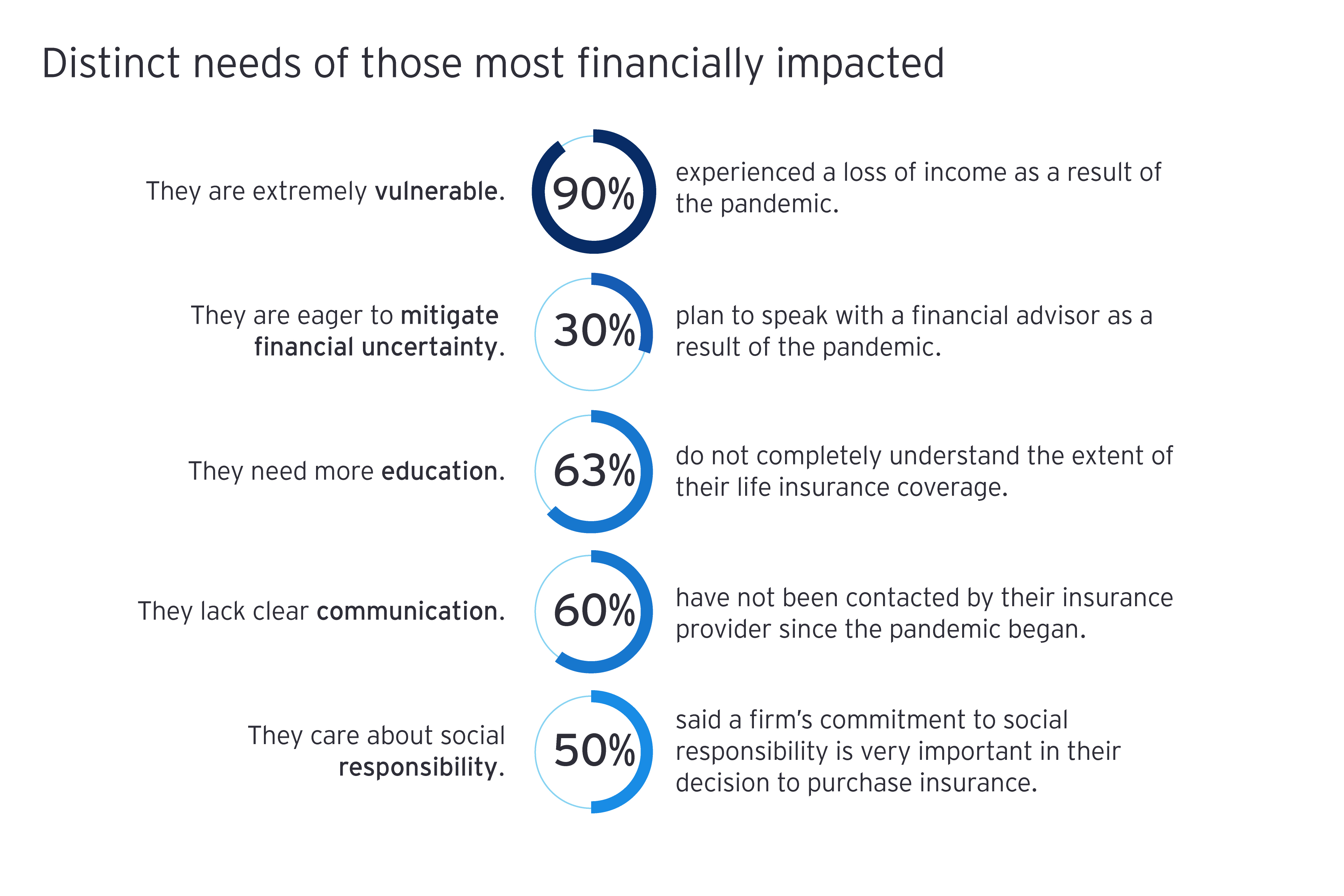

What to know about those most affected

Those who have experienced the greatest financial impact are inclined to plan for future financial uncertainty: They are more likely than respondents overall to develop an emergency plan, speak with a financial adviser, increase contributions to pension and retirement accounts and purchase new forms of insurance.

Despite this group’s heightened focus on financial planning, since the onset of the pandemic, the majority (60%) of this demographic said that they have not been contacted by their insurance provider. A majority (63%) also said they do not completely understand the extent of their life insurance coverage.

Insurers that contact this demographic, communicate the value of insurance and offer protection solutions at a time of need can help this segment recover while forming the foundation for long-term customer relationships.

Why social responsibility and justice matter

The most affected consumers are both highly concerned about social justice causes and place a greater value on an insurance firm’s social responsibility efforts in their purchasing decisions.

More than half of the most affected respondents reported that a firm’s commitment to social responsibility (racial injustice, environmentalism, income equality, police brutality and employee relations) is very important in their decision to purchase insurance. In addition, the most affected were twice as likely (61%) to donate money, time or supplies to a racial justice organization since March 2020 than respondents overall (31%).

Corporate activity around social purpose is becoming increasingly important to brand reputation and customer retention — and insurers need to think differently about what they are doing in this space.

Insurers have an opportunity to engage a socially active, energized audience by amplifying their corporate social responsibility efforts, including policies and investments to promote equality, diversity and inclusion. Within executive ranks, environmental, social and corporate governance (ESG) and sustainability-related initiatives and a focus on long-term value are important to demonstrating the vital purpose of the industry.

Strategic and operational implications for insurers

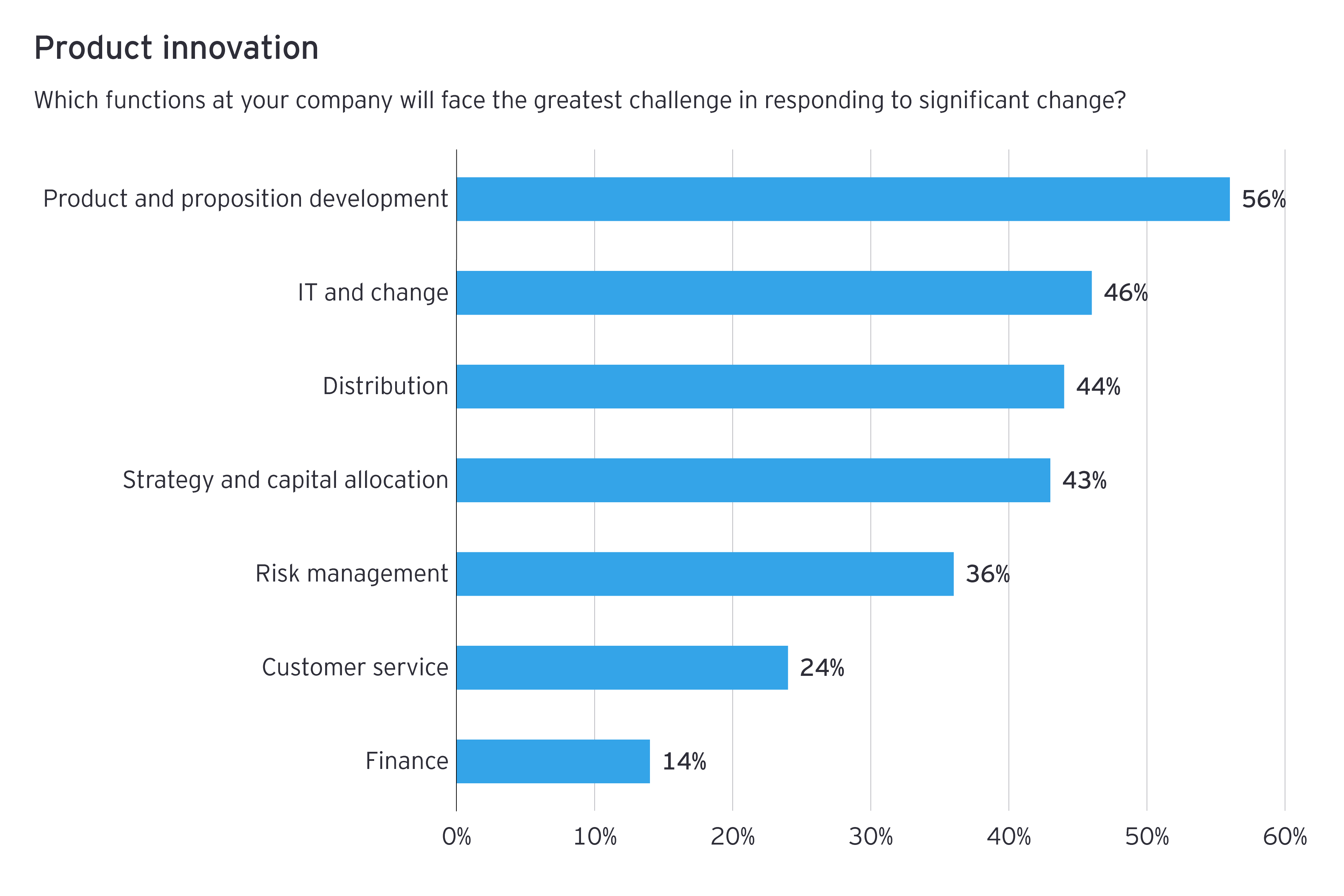

To meet consumers’ evolving concerns and needs, insurers must reimagine their offerings and overall value proposition for both existing and prospective customers. Satisfying this market demand starts with a product innovation strategy built around unique solutions that create differentiation in the market.

However, many executives express concern over the ability to achieve such a strategy. In our December 2020 poll of nearly 100 global C-suite insurance executives conducted during a virtual event, product development was predicted to face the greatest challenge in adapting to change.

Developing leading solutions requires an integrated approach that applies innovation discipline to highly regulated products. It also requires the ability to leverage external ecosystems and collaborate with others outside of the industry. Finally, insurers need an adequate technology architecture and supporting platforms.

But everything relies on first identifying the customer and an unmet need.

While COVID-19 vaccinations may help address our physical health concerns, the financial distress the pandemic has caused many consumers will be felt for years to come. As consumers’ concerns and needs change, insurers have a responsibility to live their purpose of providing protection to all.

Developing products around new customer behaviors and priorities, and reaching new demographics in need, will help the industry maintain its relevance and play the role it needs to in the recovery.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Bernhard Klein Wassink serves as the EY global customer and growth leader for insurance. He assists clients in developing growth strategies, increasing distribution effectiveness, improving customer experience and embedding digital strategies for growth.

U.S. catastrophe losses have leveled off at sub-$350 billion for the past three years, with 2035 marking a seven-year low. The Insurance Institute for Business and Home Safety (IBHS) just certified its 1,000th Fortified Community, meaning 75% of Americans now live in a jurisdiction with a truly holistic, fully risk-aware, climate resilience plan. New housing stock in the red climate zones slid to a 10-year low. New Orleans’ recent Resilient Community Bond put that blended finance/community-based insurance market over the $5 trillion mark. In Washington, Congress has already reauthorized the barely tested Resilient USA Risk Pool, updated information-sharing rules governing the National Risk Modeling Facility and tripled the matching funding for the Mangrove Project, which over the past decade has used mangrove restoration to protect 2.5 billion people from flooding globally.

The insurance industry, rightly credited with driving a generational resurgence in analytics-based resilient thinking, became the top recruiter of young engineers and coders in the country.

All of this is clearly fiction. Or is it? Each alternative reality, if pursued relentlessly, is entirely feasible.

If we’re going to “flatten the curve” of weather losses in 15 years, we need to initiate large-scale community resilience starting . . . now. If we want to help mayors, county commissioners and governors take the brave steps needed to protect their constituents (i.e., our balance sheets) we need to find new ways to arm them with the knowledge and financing to get the job done. If we want a holistic policy framework that aligns incentives around priorities informed by risk, we in insurance need to influence debates we aren’t even part of today. And if we’re serious about winning, we need to understand that the resilience sprint we’re running is the ultimate team sport that will require a relay of impact-oriented partnerships.

In short, between now and then, the insurance industry needs to stop wishing others could see the critical role we can play in preparing the country for climate change and just start playing that role ourselves. Because never before has so much rested on the ability to understand and manage complex risks.

The challenges with our playing that role on climate are real. To start, the primary means by which we send risk signals is no longer enough — or even possible — in some cases. A highly regulated, 12-month, risk-based contract in a hypercompetitive market isn’t going to be terribly effective signaling risks that will emerge five, 10, 15 or 20 years later. We must find novel ways beyond terms and conditions to deliver the stunning bundle of risk knowledge and foresight we package into a “simple quote,” like we did with IBHS, the Insurance Institute for Highway Safety (IIHS) or Underwriters Laboratory.

The deeper challenge we face is overcoming our instinctive reflex to view climate risk as a threat to profitability not an opportunity for impact. When under a multi-variant, long-term threat, the natural tendency is to be defensive, skeptical and insular, and these survival instincts are clearly evident in the initial response to climate we’ve seen from many of our institutional voices in the U.S.

If, instead, we recognized that the world is essentially begging the insurance industry to step into its broader societal role, we would see promising paths open up before us. Paths to reawakening the awesome power of nature to secure resilience. Paths to aligning economic interests for the betterment of social interests. And paths to harnessing a sense of pride that only comes from a workforce that knows its purpose is making a difference.

Now humor me again with another look at March 2036. Cat losses are linear, exceeding $400 billion, with no end in sight. Communities are paralyzed by non-stop recovery efforts, unable to make system-level changes in their risk profiles due to politicized risk projections and limited funding options. Governments are still inconsistent – in some cases contradictory – in setting pre-event incentives. The National Flood Insurance Program (NFIP) has been extended to cover personal auto flood losses to prop up the fastest-growing entitlement on the federal balance sheet. Residual markets have become the top insurer in 20 states. And the average age of an insurance sector employee just passed 54.

This, too, is pure fiction. Or is it? The answer is literally up to us. Because we are the ones who know that absent a fundamental reset the next 15 years will bring hotter weather, wetter storms, more destructive winds, higher water marks and untold human and economic misery.

We are the ones who know how to signal risk, amass risk-based capital and restore people’s lives. And we are the ones – in our actions and our inactions – making generational decisions today.

Which future are you choosing?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Francis Bouchard is an accomplished global public affairs professional who serves an adviser, catalyst and contributor to a series of climate resilience and insurance initiatives.

Six Things Newsletter | March 9, 2021

In this week's Six Things, Paul Carroll tackles the myth of 'sold, not bought.' Plus, does the pandemic signal the end of agents? What's wrong with commercial auto? The false dilemma facing life insurers; and more.

In this week's Six Things, Paul Carroll tackles the myth of 'sold, not bought.' Plus, Does the pandemic signal the end of agents? What's wrong with commercial auto? The false dilemma facing life insurers; and more.

A recent conversation crystallized a thought that has been rattling around in my brain for a while: that, despite the shibboleth, insurance is no longer “sold, not bought.”

The reverse isn’t yet true, either. It isn’t correct to say that insurance is bought, not sold. Instead, we’re in a middle ground, where insurance is both sold and bought. People certainly still rely on advice about insurance, and a good agent can spot a need and fill it with a policy, but a huge percentage of people now begin their searches online. They also do more and more research on their own, out of reach of brochures and PowerPoint presentations. With COVID accelerating the move to digital, customers often won’t even sit down in person with an agent before buying a policy.

Yes, “sold AND bought” is confusing — but the situation also creates opportunities for those who are first to adapt to the new reality... continue reading >

That was the dictum of the late, great Mel Bergstein, who way back in 1994 founded the pioneering digital strategy firm Diamond Management & Technology Consultants. (It became part of PwC in 2010.) I heard Mel’s line a lot, as a partner with Diamond from 1996 through 2003, and I think his are words to live by in the insurance industry these days.

Everyone seems to have gotten the memo about the need to digitize insurance and to explore innovative ideas, but the present typically creates a real drag that slows movement toward the future.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Social media can be a rewarding place for insurance agencies – it provides a platform to build relationships with customers and prospects and, ultimately, grow revenue. The benefits have never been greater. In fact, a recent study from Sprout Social indicates that, after consumers follow a brand on social media, 91% will visit its website or app, 89% will make a purchase from the brand and 85% will recommend the brand to a family member or friend.

But social media can also be an unforgiving place. Over the last year, we’ve seen an uptick in social media fails as businesses tried to join conversations about trending headlines and serious issues – from pandemic developments and racial justice to election validity – sometimes causing irreparable reputation damage and business impact.

As consumers increasingly turn to social media to inform decision-making, it’s critical for agency owners to build their social media skills to navigate the risks and reap the rewards. Here are six tips to get you started:

1. Establish the ground rules.

Creating general social media guidelines for your agency will help you make faster and smarter decisions in any situation. The guidelines can be as simple as a one-page document that outlines:

Your social media objectives

Your target social media audience

Your social media “voice”

Topics you will/will not address on your channels

Frequency of posting

Engagement approach

Who has access to post on your social media accounts

When and when not to respond to conversations

These guidelines can and should evolve along with your agency. Revisit them regularly to ensure they still complement your overall business strategy.

2. Be a good listener.

While you shouldn’t make posting decisions based on what everyone else is doing, you also shouldn’t make decisions in a vacuum. It’s important to truly understand a trending situation as well as the mood on social media and in traditional media before making a decision about whether to post.

As you evaluate the situation, look at the conversation that’s already happening. Are other agencies jumping in? If so, what’s driving that? How are people responding to that content? Are the media stories about agency response positive or negative? Are your customers and prospects joining the conversation? Are they asking you to join? Why? Understanding the landscape can help make a decision that feels right for your business and the moment.

When the racial and social justice movement gained momentum last summer, businesses were eager to show their support on social media. Those with a track record for actively discussing and addressing these issues were greeted with positive feedback. Those that issued hollow statements about support and solidarity without action were savaged. For example, Ben and Jerry’s statements were viewed as appropriate because the brand and its founders have a long history of social activism, while the NFL’s statement that included the phrase “we need urgent action” was blasted.

4. Pause when appropriate.

Sometimes, you just need to hold off on any kind of social media posting – either because everyone’s attention is elsewhere or out of respect for the situation at hand. For example, many insurance agencies we work with paused on posting around the presidential election because that event dominated the social media conversation. And we’ve advised them to pause during moments of national and world crisis because of the gravity of those situations. Continuing to post promotional content at these moments can imply your agency is disconnected from the world around you – or simply doesn’t care. Pay attention to what is happening in the world and pause posting during times of crisis.

5. Engage with care.

Treat the content you like and share with the same care you treat your own social media content. Before you deem something worthy of engagement, review it carefully. Verify the content’s accuracy, check for hot-button language, know your source and review the current comments to avoid an inadvertent issue. For example, a controversial news figure might post something completely neutral on Twitter that you think is relevant to your customers. However, your customers might view a retweet of that post as an endorsement of the controversial figure.

6. Live the brand.

As an agency owner, you are the brand, and anything you post on your social media accounts becomes a reflection of that brand. In a recent New York Times story, journalist and digital communication expert Sree Sreenivasan summed it up well: “The fact is that it’s impossible to separate the personal use of social from the professional, and everything you say online can and will be used against you. There are ways in which you can try to safeguard your privacy and control who sees particular content, but the onus is on you to be vigilant. So, the more seriously you can take your social media activities, the better.” You can mitigate your risks by embracing the same social media guidelines for your business and personal accounts.

Every day on social media, agencies of all sizes are judged by what they say and what they don’t say. Understanding the risks that come with a social media presence – and how to mitigate them – is just as important as understanding how to use these platforms to connect with customers.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

It has been a year since the first cases of COVID became known, beginning an upending of the world as we knew it. As COVID hit, our strategies, priorities and plans all took on a new view, a new focus and in many cases a new urgency – through the eyes of digital engagement, for customers, employees and channels. The good news: Many initiatives were still relevant. The bad news: Many initiatives needed to accelerate because market assumptions and strategies changed substantially overnight.

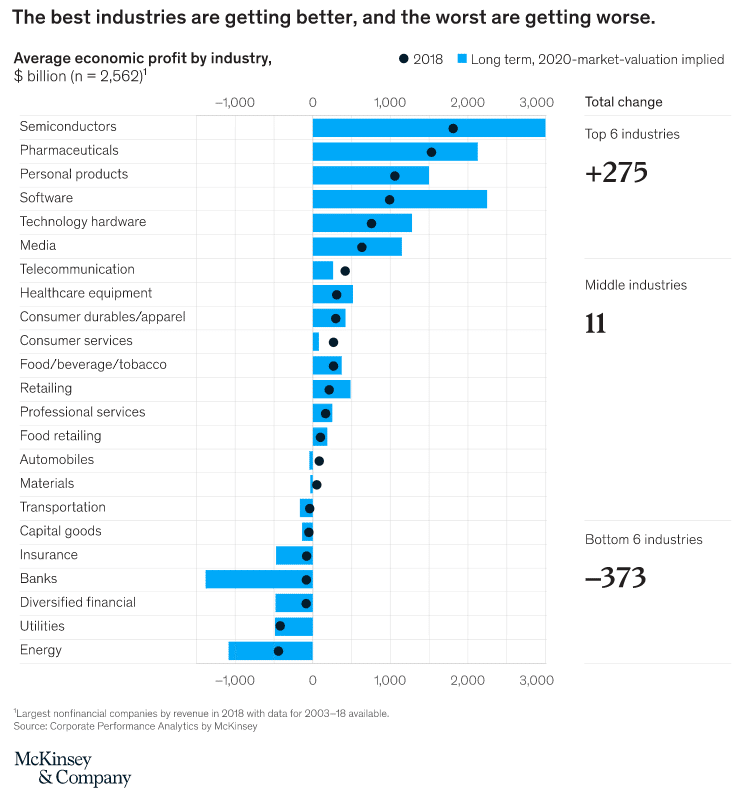

COVID affected all industries, but some were better prepared than others because they were well down the path of digital transformation. McKinsey, in a multi-year, multi-industry research initiative, assessed economic profit by industry and identified what they term an “economic profit gap,” which became evident in 2010 and has been widening ever since. Within the industries tracked, insurance is in the bottom six, showing a gap that was growing even before COVID. This is no surprise, given the influx of capital to insurtech focused on transforming the centuries-old industry.

Figure 1:

A Growing Gap Between Leaders, Follower and Laggards

Today, COVID has widened the gap between the top, the middle and the bottom – aligning to our Strategic Priorities research tracking Leaders, Followers and Laggards the past six years. The COVID crisis has exposed and heightened the power of future-ready, digital business models that proved more resilient, which in many cases accelerated dramatic growth. Consider these examples:

Streaming media vs. traditional cable

At-home cooking vs. eating out

Curbside pickup or delivery vs. eating out

Digital e-commerce vs. in-store buying

Home delivery vs. in-store buying

A recent report by Andreessen Horowitz found that, in the first six months of 2020, e-commerce in North America as a percentage of overall commerce increased more than in the entire previous decade – going from 16% in January 2020 to 27% in July 2020, after starting 2010 at only 6%!

Parts of the insurance industry also experienced this surge. AccuQuote, a national online life insurance agency, saw a 20% to 30% uptick in life insurance applications. This aligns with a Forbes report that said that online life insurance sales increased 30% to 50% for companies with speedy apps that used data/algorithm-driven underwriting, particularly for people 45 and under, the prime growth market of millennials and Gen Z. Another Forbes article reported that P&C usage-based insurance (UBI) accelerated in North America as people reevaluated traditional auto insurance. Prodigy, a provider of software for auto dealers that lets customers compare and buy insurance when they purchase a vehicle, said that online insurance sales grew 300% in 2020 and that millennial buyers tended to gravitate toward UBI.

Redefining the Future Out of a Crisis

History tells a great story of opportunity and innovation for those who embrace disruption. Looking back at other crises and catastrophes, there is a strong relationship between disruption and opportunity – driven by innovation in business and technology.

Think about the Spanish flu. It increased interest in epidemiology and established the national disease reporting system; World War II brought radar and computers; and the 2008 financial crisis gave rise to the sharing and gig economies and insurtech. Out of every one of those catastrophic or major events arose fascinating and world-shifting new businesses and technologies that helped us adapt to a rapidly changing world.

Now, a year after the emergence of COVID, companies – both insurers and those who are insurer customers – realize we will never go back to “normal.” Companies with resilient, future-ready digital business models were better-positioned to ride the trends, embrace disruption and thrive during the crisis, increasing their competitive advantage and establishing them as a next-gen leader.

Leaders Hit Hyper-Acceleration

Our new Strategic Priorities 2021 report, based on post-COVID insurer survey results, shows a dramatically widening gap when looking at insurers focus on key strategic initiatives the last year between Leaders and Laggards of 64% – representing a 20% growth in the gap from last year. Followers were “treading water” to keep even with the previous year – with a 12% gap.

Even more concerning is the widening gap with Leaders in the next three years of 102% for Laggards and 28% for Followers, reflecting a 40% and nearly 10% gap growth for each! These gaps do not bode well for insurers’ ability to grow and remain relevant with the ever-increasing pace of change and disruption.

Insurance companies have a unique opportunity to re-envision their future of insurance today and redefine their strategies and priorities for 2021 and beyond.

The COVID crisis along with other customer, demographic, technology and market boundary shifts are changing risk, customer behaviors and expectations – creating the demand for new risk products, value-added services and customer experiences that the insurance industry must respond and adapt to. These shifts create opportunities to make insurance better and more relevant through the innovative application of technology. Most importantly, we have the opportunity to make the change happen if we break down the silos and long-held business assumptions, embrace next-generation technology and ecosystems, and more!

Look at the accomplishments of Operation Warp Speed in the face of an “impossible” challenge! The approach delivered the first approved vaccine in less than nine months as compared to the “traditional” process, which could take 10 to 15 years!

Think what insurance could deliver – new products, customer experiences, services and much more. Instead of taking years … what can we do in weeks or months? The impossible is possible!

So how do you position yourself as a Leader, climb the economic power curve and become strong innovators?

Know where you are in the Knowing-Doing Gaps from our Strategic Priorities research that define Leaders that are accelerating digital transformation with resilient digital business models. Then rethink and reprioritize your strategies and priorities to take advantage of the shift and opportunities unfolding. Most importantly, execute on these priorities with focus and urgency.

This year’s Strategic Priorities report is more important than ever for insurers to assess where they stand and how they will respond, because “business as usual” is no longer a strategy in this time of dramatic change and pressure.

It is time for bold moves.

Finding the right balance between optimizing today’s business and boldly creating tomorrow’s business is more important than ever. Are you ready to strike that balance and rise as one of the post-crisis leaders?

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

The Myth of 'Sold, not Bought'

It isn't correct yet to say that insurance is bought, not sold. We're in a confusing middle ground, where insurance is both sold and bought.

A recent conversation crystallized a thought that has been rattling around in my brain for a while: that, despite the industry orthodoxy, insurance is no longer "sold, not bought."

The reverse isn't yet true, either. It isn't correct to say that insurance is bought, not sold. Instead, we're in a middle ground, where insurance is both sold and bought. People certainly still rely on advice about insurance, and a good agent can spot a need and fill it with a policy, but a huge percentage of people now begin their searches online. They also do more and more research on their own, out of reach of brochures and PowerPoint presentations. With COVID accelerating the move to digital, customers often won't even sit down in person with an agent before buying a policy.

Yes, "sold AND bought" is confusing -- but this situation also creates opportunities for those who are first to adapt to the new reality.

The conversation that pulled the thought together for me was with Amy Radin, a longtime senior executive at Fortune 500 companies in financial services, including American Express, Citi and, most recently, Axa, where she was chief marketing officer. Amy has added "author" to her resume, publishing a book on how to produce disruptive change in big organizations, and now consults to both big corporations and insurance startups. She spoke with me for a webinar as part of this month's ITL Focus on strategic innovation and brought up agents' "Uncle Joe" issue.

Uncle Joe?

"Even with someone who has bought an extremely high-end policy, they're investigating their options. They're talking to neighbors. They're talking to their Uncle Joe, who is very successful, so they respect his opinion. They're talking to people who lead lives like theirs," Amy said, based on customer journey research she has done or commissioned over the years. "Customers will tell you they went through an investigative process that has nothing to do with anybody who's licensed by the regulators to sell insurance."

She added: "Most policy holders would be offended to hear that the industry views them as being sold to. I doubt any of them will tell you, I just called my agent and said, Tell me what to do."

The "sold, not bought" notion will, I believe, increasingly limit innovation, because it will keep executives focused on the products and on tools for agents rather than on how people's needs are changing in these turbulent times.

Her recommendation: "Go out and listen to your customers. Don't hire a market research firm. Don't rely on surveys. Sit down with a handful of people who are giving you their money and understand what's changed in their lives."

She cite a Harvard Business Review article by Michael Porter that said only 3% of executives actually go out to interview customers -- even as the executives preach the need to be "customer-centric."

"Ask: How am I to do business with? Tell me about that policy you bought? How did you decide what to buy? Who did you consult?

"Don't do this in the context of trying to sell the product. And don't just ask about rational needs. Ask about emotional needs. How are they feeling -- not just what are they doing? Insurance is a product that's pretty fraught with emotions."

She cites an experience she had understanding an emotional need while at Citi, where she was an EVP and chief innovation officer in the U.S. credit card business from 2000 to 2009. During the Great Recession, all sorts of people fell behind on payments, which traditionally would have meant launching a barrage of calls to browbeat delinquent customers. But Amy suspected that many would appreciate a digital experience, so they could negotiate terms and make payments without being shamed by another person.

"It's very emotional to be in collections," she said.

She eventually got to run a test, which found both that customers appreciated the digital option and that Citi profited financially.

"The digital experience is now standard practice in that business globally," Amy said.

Insurance sales are unusually complex because, as Amy put it, "Nobody is getting out of bed in the morning saying, I'm dying to get another insurance policy."

But a challenge creates an opportunity. Some companies are responding by embedding insurance into other sales, to make an offer to people in a time of need -- auto insurance when they buy a car, renters insurance when they sign a lease, etc. Other insurers are trying to fit into the new buying process and make sure that prospects will come across them while doing their research online. Many are trying to clean up their interactions with customers, using chatbots to speed routine inquiries, implementing omni-channel approaches so that someone who begins a conversation with an agent or company via a website can easily pick it up via text message, etc.

Yet those moves feel like just the beginning. Whoever first figures out the new "insurance is sold and bought and sold and bought..." paradigm will create a more collaborative model that will delight customers -- and bring a lot of them into that company's fold.

Stay safe.

Paul

P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

A Conversation on Corporate Strategy, with Amy Radin

With the pace of digitization increasing, people talk a lot about new business models, new products and new technologies that can transform sales and customer service, claims, underwriting and more -- but seldom about how the approach to formulating strategy must evolve.

In this webinar, Amy Radin makes a strong case for starting by reassessing what the customer needs in these changing times, both from a rational and from an emotional standpoint.

In this webinar, we'll cover:

Recognizing opportunity in times of crisis

Embracing digital transformation

Approaching customer experience from a position of empathy

Amy Radin is a Director, Advisor and Author with Fortune 500 experience in consumer financial services and insurance at brands including American Express, Citi and Axa. Her book, The Change Maker’s Playbook: How to Seek, Seed and Scale Innovation In Any Company was awarded the Book Excellence Best Business Book Award 2020. Learn more about Amy and her work at https://www.amyradin.com.

Paul Carroll

Editor-in-Chief, ITL

Paul is the co-author of “The New Killer Apps: How Large Companies Can Out-Innovate Start-Ups” and “Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years” and the author of “Big Blues: The Unmaking of IBM”, a major best-seller published in 1993. Paul spent 17 years at the Wall Street Journal as an editor and reporter. The paper nominated him twice for Pulitzer Prizes. In 1996, he founded Context, a thought-leadership magazine on the strategic importance of information technology that was a finalist for the National Magazine Award for General Excellence. He is a co-founder of the Devil’s Advocate Group consulting firm.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Amy Radin is a strategic advisor, keynote speaker, and Columbia University lecturer focused on why transformation succeeds or stalls in large, complex organizations.

Drawing on senior leadership roles at Citi, American Express, and AXA, including one of the world’s first corporate chief innovation officer roles, she helps leaders build the capabilities required to absorb, scale, and sustain change.

Commercial auto is one of the biggest, most problematic cost centers in the insurance industry. Its loss ratios are incredibly high — and growing — particularly in comparison with other P&C lines. Carriers struggle to make money on the line, and they frequently incur fairly substantial losses.

With fewer claims than most other lines, why is commercial auto such a problem? Because claims are much larger; carriers may be looking at paying out $200,000 vs. $20,000 on different types.

Let’s examine the issues and see how we can turn commercial auto into a revenue generator instead of a black hole.

Commercial Auto by the Numbers

According to the National Association of Insurance Commissioners, commercial auto represents $39 billion in earned premiums. Yet, it pays out approximately $28 billion in losses, which excludes all of the internal administrative costs. Some folks in the industry thought that losses might go down this year due to fewer cars on the road, given COVID-19, but this has not been the case. One large carrier recently shared with me that they’ve seen a similar level of claims (both in terms of frequency and severity) because many commercial trucking organizations are working nonstop to keep the supply chain going.

If even a pandemic won’t lower the loss ratio, are we doomed? Let’s break this down a bit further.

Of the $28 billion in losses, roughly 60% went to medical costs associated with bodily injury. There is not much that can be done here from a carrier standpoint, short of offering slightly lower premiums for companies that incorporate the strictest safety standards and tools like electronic logging devices. Even this technology can be a double-edged sword given that the more advanced vehicles tend to be more expensive to fix in the event of an accident. While measures can sometimes minimize the severity of injury, accidents still happen.

Carriers have seen an uptick in accident rates involving bodily injury or death over the past 10 years, in part because more commercial vehicles are on the road traveling more miles each year. Then there is the role of drivers themselves. The trucking industry has a remarkably high turnover rate. For example, in the third quarter of 2019, large truckload carriers’ turnover rate increased to an annualized rate of 96%, according to Trucker.com. As companies basically overhaul their entire workforce each year, many don’t invest the resources into in-depth training programs, leading to less experienced, more accident-prone commercial drivers on the road.

Driver issues withstanding, the non-medical costs still leave $11.6 billion in losses. Where does it go? Very simple: Legal costs account for 40% of losses; the system is broken.

Losing Battle

Litigation tends to happen when claims are not resolved quickly or when something is perceived as unfair. While such concern is perhaps understandable, in practice it is not so innocent. A growing body of attorneys are ready to sign on to “help” plaintiffs, initiating cases that should never be filed, and they have become quite proficient at securing huge settlements.

The lawyers who specialize in auto claims know exactly what to look for and can be quite convincing in wooing potential clients and later in threatening the carriers with which they are attempting to negotiate. For example, the lawyers might spot something not related to the specific incident but that could be tied to the company. A savvy attorney would tack on additional charges, such as negligence, on top of bodily injury, pain and suffering. Tactics like these drive settlements higher. Complicating matters, states have very different statutes on bad faith suits filed by attorneys. Some states are more prone to settling cases early, and, as a result, lawyers in these areas increase the number of suits they file — which increases the cost for carriers.

One thing that many insurance firms and self-insured enterprises are just realizing is that plaintiff attorneys are rapidly becoming data-aware and using that awareness in a highly sophisticated and strategic way. Once upon a time, plaintiff attorneys were good at qualifying clients that they had a high degree of confidence could return them a large settlement. While that’s still the case, in the last half decade or so, even moderately sophisticated plaintiff firms have compiled significant datasets on enterprises and insurance companies, in many cases down to the general actions taken at an adjuster level. They use this data to plan their litigation strategies, select the most effective partner and manage each step of the process in an intelligent way. The result is that carriers and self-insured enterprises that do not have similar data-savvy practices are essentially being bled dry because they have nothing to counter this advantage.

Attorneys are more than willing to try their hand in court, and juries can be quite sympathetic to plaintiffs they feel were wronged by a big company. As a result, there has been a certain degree of social inflation, as jury awards can rise astronomically if for no other reason than a desire to help the little guy fight back against the “evil” corporation — and winning verdicts keep going up. According to Shaub, Ahmuty, Citrin & Spratt, the median of the top 50 single-plaintiff bodily injury verdicts in the U.S. nearly doubled from 2014 to 2018 (moving from $27.7 million to $54.3 million).

As it stands today, there is tremendous variability in jury awards, just as there is with out-of-court settlements. Looking across claims, there might be very little difference in the facts of the case, yet one plaintiff walks away with millions while another receives a much smaller verdict. Carriers are often unwilling to risk the chance of coming out on the wrong side, hence agreeing to a settlement that may be uncalled for.

It is clear that litigation is the most significant hurdle to better loss ratios across the commercial auto line. If we can reduce, standardize or eliminate costs associated with litigation, the industry would be in a much better position.

A Process Evolved

New technologies, artificial intelligence (AI) and machine learning, in particular, can help. For example, you may want to know the likelihood of attorney involvement based on several claim factors, or you want to know which attorney is involved and what kind of settlements he or she negotiates for similar claims. But most importantly, you want to know what actions to take to prevent attorney involvement. AI and machine learning applications are emerging that can identify claims early in their life cycle that need the most attention.

Imagine how powerful it would be if you had an application that inherently understood the intricacies of commercial claims — one that would warn you of claims that were in danger of slipping to an attorney. Solutions are hitting the market that leverage capabilities like natural language processing and deep learning techniques to analyze hundreds of data points hidden within claims. They now can tap into structured data as well as the really interesting unstructured data, like notes or police reports, as well as decoding the sentiment of claimants. This collection of data provides pretty telling clues as to how a claim might progress.

An adjuster could get an alert about aspects of the claim that are troublesome, access to detailed attorney scores and ratings in case the claim escalates and, if need be, the optimal time to settle for a favorable outcome. With this information, the adjuster could take immediate action to head off the problem.

As applications get smarter, they will be able to determine what a claim settlement should look like and why with a much higher degree of certainty based on similar claims. This can be instrumental in the adjuster’s or defense counsel’s ability to negotiate with the claimant’s counsel. Armed with this kind of hard data, the organization could walk into settlement negotiations in a much stronger position and begin to counter the formattable data advantages that plaintiff attorneys have been amassing.

AI and machine learning systems also help organizations close claims faster, and, in doing so, relieve some of claims management teams’ administrative burdens. Additionally, by closing claims quickly and fairly, claimants receive settlements faster, return to their everyday lives sooner and thus generally wind up in a better financial position without ever involving an attorney.

Considering the high loss ratios of commercial auto insurance today and the propensity for them to increase further, emergent AI-based applications are our best hope for improving profit margins and repairing the commercial auto line.

Gary has been a leader in the technology industry for over 21 years, with a deep focus on building AI & Machine Learning applications for the Enterprise market. Over the span of his career, he has raised over $1.2B in debt and equity and helped create over $7.5B in enterprise value through 2 IPOs and 4 M&A exits. Gary holds an M.B.A. from the Marshall School of Business at the University of Southern California, where he was named Sheth Fellow at the Center for Communications Management. He also holds a B.A. with honors in Business from Arizona.

The “alley-oop” can electrify a basketball game if the passing and timing are precise enough and the dunk thunderous.

The possible disintermediation of incumbent insurers via technology has been a favorite topic of discussion in the industry. But the COVID era has created a distinct advantage for incumbents, has changed customers’ attitudes on privacy and has heightened interest in insurance, while there has been a hiccup for insurtech. For the traditional carriers, that's an alley-oop!

In fact, I believe that the post-COVID era -- 2021 forth -- will let these incumbents Benjamin Button their way to a new look via a technology-based overhaul of products, services, distribution and operating models.

Big Tech, insurtech, managing general agencies and excess and surplus carriers that have been bubbling along for years will now witness a different outlook from their traditional insurance counterparts, which are gearing to strategize and execute at DEFCON 1 level.

This article is the first of three parts analyzing the posture of the incumbents vis-à-vis new-age competition in the face of COVID-induced global economic slowdown and liquidity strains (in addition to the persistent issues of high cost base, complex underwriting practices and opaque pricing). The overarching view encapsulates commercial and personal lines – property/casualty, life and accident and health.

For the longest time, the insurance industry operated on three maxims:

Insurance is purely a risk transfer mechanism

Insurance is sold and not bought

Insurance incumbents’ grasp on massive data cannot be matched

Big Tech, neo insurers and insurtech have been creating a ripple in the $6 trillion insurance market solely by turning the three maxims on their head.

Apple, Google and Amazon have already charted sophisticated territories in fintech (most notably in payments, banking and lending) and have stirred the insurance sector lately, while the likes of Lemonade, Root and Metromile have attempted to erase the incumbents’ raisons d’être.

The appetite is no surprise given the companies' access to customer data, prowess in analytics and ease of distribution via popular platforms, which are elite in customer experience and provide real-time customer care while offering pay-as-you-use models.

Some notable actions:

Amazon: Alexa-focused partnerships (Cigna, Allstate and Geico), Pillpack digital pact (BCBS)

Google: CapitalG’s investment in Applied Systems, a core insurance agency management software provider; Alphabet’s Verily partnership with Swiss Re

Apple: John Hancock's Vitality and UnitedHealthcare’s Motion, a national wearable device program

Lemonade: powered by machine-learning underwriters and settles claims online within minutes

Tesla: zooming in on individualized risk pricing and selling insurance directly to its drivers (underwritten by its partner, Markel)

The concept of asymmetries propelling disruptive market entrants (such as the ones listed above) is based on the notion that disruptors aren’t challenged by motivated-enough incumbents because the two do not see the market opportunity the same way. What if, however, the market opportunity itself goes through a sudden seismic shift demanding both the disruptor and incumbent see the landscape through the same lens?

In this post-apocalyptic year, it is easy to miss the quantum leaps that the large carriers took, such as:

Chubb’s new "digital insurance in a box" -- Chubb Studio gave a new meaning to embedded insurance as it extended its products to retail, travel, telecom and banking

State Farm’s Cape Analytics, which assisted focus on AI-powered geospatial property data

Travelers’ Qualtrics digital experience manager for experience analytics and real-time detection

A record-breaking telematics upswing that needs a full article dedicated just to it: Nationwide (frankly a first mover since 2011, boasting mostly OEM partnerships) USAA’s SafePilot, Berkshire Hathaway's TrackMRI

Operational excellence/[rocess redesign examples such as Prudential’s PruFast Track; AIG’s use of ServicePower; or John Hancock’s ExpressTrack

So what gives? A combination of the "slow incumbent" myth’s bursting, along with a change of pace for customers.

Behind the scenes, large carriers have been preparing for the journey to customer advocacy, going from being primarily a claims payment business to engaging with consumers for reduction or prevention of claims and to becoming the byproduct of the services that customers buy -- telematics for UBI (usage-based insurance) or IoT to prevent machinery failure or aerial surveillance for risk monitoring or health wearables or use of artificial intelligence and machine learning for loss anticipation.

Data was always king for carriers. They are strengthening their prowess via partnerships with social media giants, OEMs and retail and travel companies.

The seemingly stiff carriers were on a path to digital transformation pre-COVID anyway. Powered by “everything as a service,” their move from rigid systems such as agency management system, claims system, etc. to modularized core claims, underwriting, products and pricing are giving them nimbleness now that the world has become ultra-dynamic.

Finally, my personal favorites: the insurtechs! Their potential for turning headwinds into tailwinds when joining hands with carriers is a force to reckon with. Whether as partners or acquisition targets, insurtechs have been a focal point of carriers’ corporate venture capital arms -- both for investment and for ingenuity. The courtship has resulted in several wins, such as turbo-charging customer experience and finding pockets of innovation such as in risk selection and in fraud detection. Zurich’s partnership with Snapsheet to simplify the customer claims experience or Travelers’ InsuraMatch acquisition for real-time quoting are notable collaborations.

Carrier-insurtech collaboration is the fastest and most robust way for carriers to become specialists at scale. On the other hand, carriers foresee a bigger realm serving as insurtech’s right hand (e.g., AXA served as a reinsurer for Lemonade, Oscar and Pure).

I won’t spend time expanding on the historic muscle of incumbents, that of capital, access to distribution access, brand, appreciation of the regulatory landscape, etc.

In the parallel universe, customers’ preferences have changed dramatically. They are now ready to relinquish savings in favor of investing in policies. Health and safety undoubtedly take precedence over personal privacy. Customers' willingness to share data both in personal lines and in commercial space has given a new meaning to the so-far-experimental UBI models.

Of course, the large incumbent carriers should see this new setting as a transient competitive advantage. For the longest time, they have used technology to do more of the same, just faster or cheaper. It's not easy for large organizations to rethink the proverbial question of, “What do we want to be when we grow up?”

They still much spent a lot of time practicing pick-and-rolls and give-and-goes if they want to score on that alley-oop!

Get Involved

Our authors are what set Insurance Thought Leadership apart.