“Social inflation” is considered one of the major emerging risks that the insurance industry must face. While people may misconstrue the term as relating to the rising impact of social media on online behavior of netizens, it has actually to do with increasingly hostile legal environment that insurance carriers are facing today. This manifests in the form of much larger verdicts, liberal treatment of claims by boards, more aggressive plaintiff bars, etc. This article explains the trend and describes measures that carriers can deploy to keep a check on increasing legal expenditure.

Here are some signs of the phenomenon:

- A major P&C insurer anticipates $40 million in quarterly legal costs for property losses alone

- There is a 94% increase in assignment of benefit (AOB) lawsuits in the state of Florida in the last five years

- An increased probability of "nuclear verdicts" (> $10 million) is a real trend. In 2018 alone, the top 100 verdicts ranged from $22 million to $4.6 billion

Here are some factors driving the trend:

- Litigation Funding: Propelled by easy capital availability, a new class of plaintiff attorney funding model has emerged in the last 10 years. Essentially, this model provides funding for legal expenses to plaintiff attorneys in exchange for a portion of the judgment or settlement. The model is good in the sense that it levels the playing field against large, well-funded corporations, but the unintended consequences (for insurance companies) is an exponential increase in attorney representation and pursuit of aggressive legal strategies. Approximately $9 billion has been committed to this "industry."

- Rising anger against big corporations: The very premise of the big corporation versus the individual scenario is driven by anger. The perception among the consumers and the jurors is that a corporation has only one goal: profit. Stagnation of incomes/wages is another contributing factor to this mindset. Big businesses in America like to talk about the good jobs they provide, but median salaries in the U.S. have been flat for decades. This is not because of a failure of workers to become more productive; there were gains in productivity, but they did not go to workers. Gains mostly flowed to the organizations and their shareholders, including executives who received sizable stock-based compensation. Hourly compensation for workers remained practically flat.

- Large verdicts being driven by general social pessimism and jury sentiments: New and interesting patterns are being observed in jury behavior, especially in personal injury and liability claims. Emotion and trust play a big role in how a jury rules. Some of the key reasons behind these large verdicts are: jurors’ distrust in big corporations and their lawyers; jurors paying less attention to lengthy testimonies and complex explanations; impact of social media on how millennial jurors view the court system; impact of emotional stories on how a jury thinks; and the “what if it were me?” attitude influencing how jurors approach justice.

Leaving aside the financial burden from social inflation, which is quite significant on its own, increased litigation also affects carriers in other ways. There can be inaccuracies in reserving, which is based on counsel's estimates of litigation spending. There can be negative press and poor customer engagement/satisfaction. And claims can increase in complexity, delaying settlement. .

Many insurers are either in the early stages of dealing with social inflation or are not moving as fast as they'd like on the problem. The most common reasons include:

- Claim handling practices are often inadequately data-driven

- There is limited ability to foresee litigation

- There is lack of trust in analytical models

- The company takes a semi-reactive approach for claim settlement and negotiations

- Assignments are inefficient, either to claim handlers or attorneys

What can insurers do to manage this growing challenge?

See also: The Data Journey Into the New Normal

Enter machine learning and artificial intelligence

Use of analytics from first notification of loss (FNOL) until the claim is paid is now a norm rather than a competitive edge. All large carriers invest heavily in use cases such as fraud detection, severity-based claim assignment, automatic loss estimation, recovery optimization, etc. However, given the complex nature of how litigated claims are handled, only a few top U.S. carriers are able to weave these capabilities effectively into business processes. Insurance carriers that successfully use analytics to drive business process change in claims litigation will stay ahead of this massive threat.

There are two unmistakable trends that carriers need to leverage:

- Aggressive use of information sitting in claims and policy systems (structured attributes, adjuster notes) to develop signals around plaintiff attorney behavior. These signals then need to be deployed within claims operations to encourage early case assessment and litigation prevention.

- Use of increasingly clean and comprehensive sources of external litigation information (from state courts, where most insurance litigation lies) to inform your litigation strategy. This includes past verdicts information by venues, judges, attorney firms, case types, etc. A thoughtful use of this information can help claims adjusters and defense attorneys devise the litigation strategy to avoid worst outcomes. There are multiple firms providing research tools that are based on these. Our recommendation, however, is for carriers to ingest the information, merge it with internal claims data and develop models and tools providing a comprehensive view

How carriers can leverage this trend

Carriers can use predictive and descriptive analytics solutions in claims management to mitigate the problem. At a high level, such solutions can lower ballooning legal costs by avoiding litigation and optimizing litigation strategy. Both these approaches call for incorporating advanced analytics processes and models at the key steps of the claim settlement process. This includes:

- Advanced analytics and machine learning models to predict and avoid litigation and post-suit strategy formulation

- Natural language processing (NLP) to leverage unstructured data and extract additional insights

- External data ingestion to augment internal data and enhance model accuracy

- Enhanced data management capabilities

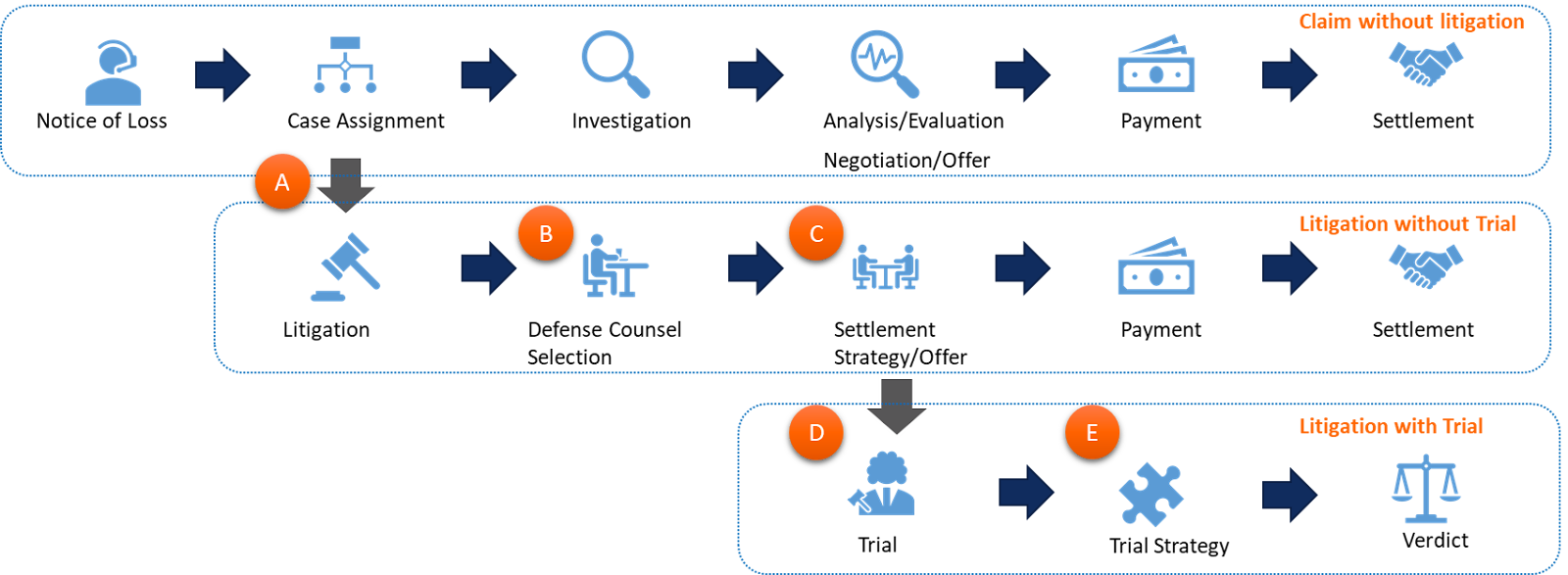

Any insurance claims raised can result into any of the three possible outcomes: claims without litigation, claims that involve litigation without trial and claims that involve litigation with trial. With the help of the aforementioned technologies, carriers can engineer the following mechanisms in the claims management process (Figure 1) to optimize the legal expenditure for a given product:

- A - Prediction of litigation likelihood

- B1 - Defense counsel selection

- B2 - Law firm benchmarking

- C1 - Attorney insights

- C2 – Prediction of settlement failure

- D - Legal activity duration, legal expense prediction

- E - Case-level insights

See also: Growing Risks of Social Inflation

Conclusion

Claims data within insurance companies is being increasingly seen as a key asset, not a byproduct of the claims process. However, the path to using internal and external sources of data to drive business outcomes is long and arduous. It is becoming increasingly important for carriers to incorporate insurance analytics processes geared toward optimizing legal spending. To achieve this, insurers require a combination of capabilities to these engagements, i.e. ability to handle big data, ability to develop advanced analytics solutions and knowledge of "what, why and how to deploy" in claims business processes.