This article was written with Adrian Jones, a #traditionalindustry guy and insurtech investor who writes in his personal capacity. The authors’ opinions are solely their own, and only public data was used to create this article.

***

“All the insurance players will be insurtech,” as Matteo titled his recent book, but some insurtechs have chosen to be insurers. Real insurers. Which means they file detailed financial statements. These obscure but public regulatory filings are a rare glimpse into the closely guarded workings of startups.

Full-year 2017 filings for U.S.-based insurers were released earlier this month. Here’s what we found:

*The company has gross paid-in surplus of over $31 million so this figure is probably low. **Excludes a write-in for “revenue from parent for administrative costs,” possibly a way of topping up the company’s surplus[/caption]

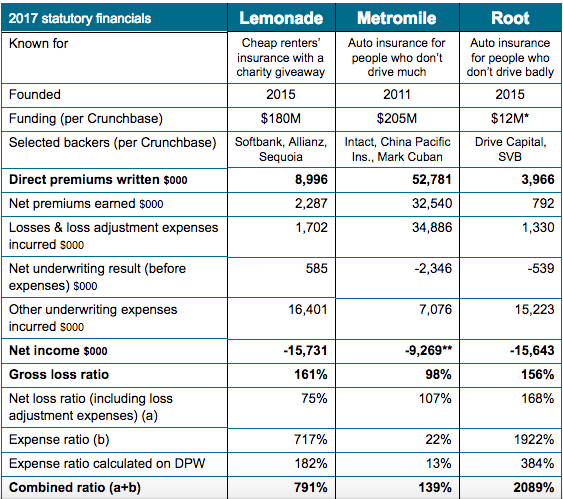

A combined ratio greater than 100% usually means a loss. Combined ratio doesn’t include returns from investing insurance reserves, but the days of double-digit bond yields are long gone. In a low-rate environment, investment income can’t offset poor technical results. The ratios are typically calculated on net earned premiums, but we also show a row where the expense ratio denominator is total direct premiums written, which may be more appropriate for growing books.

Observations:

*The company has gross paid-in surplus of over $31 million so this figure is probably low. **Excludes a write-in for “revenue from parent for administrative costs,” possibly a way of topping up the company’s surplus[/caption]

A combined ratio greater than 100% usually means a loss. Combined ratio doesn’t include returns from investing insurance reserves, but the days of double-digit bond yields are long gone. In a low-rate environment, investment income can’t offset poor technical results. The ratios are typically calculated on net earned premiums, but we also show a row where the expense ratio denominator is total direct premiums written, which may be more appropriate for growing books.

Observations:

1. Underwriting results have been poor

All three companies have a gross loss ratio of near 100% or higher. (For reference, the industry average in 2016 was 72%). That means they have paid $1 as claims for each $1 earned from policyholders in the last 12 months.

An insurance startup has to prove two critical things:

1. Underwriting results have been poor

All three companies have a gross loss ratio of near 100% or higher. (For reference, the industry average in 2016 was 72%). That means they have paid $1 as claims for each $1 earned from policyholders in the last 12 months.

An insurance startup has to prove two critical things:

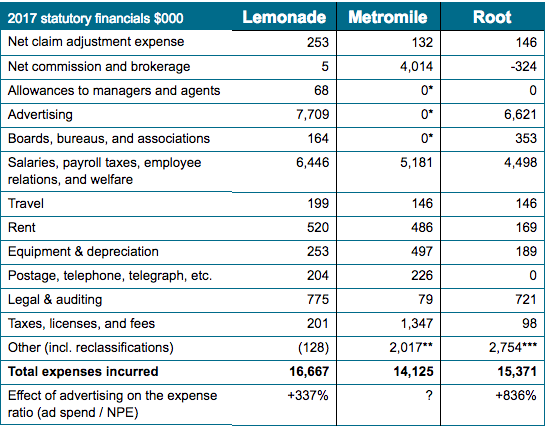

*Likely included in commission and brokerage expense, which is net of $2.1 million ceded to reinsurers **Largest write-in item is “other professional services” at $891,000. ***Includes $1,958 of unpaid current year expenses and write-ins like “other technology” and “contractors”[/caption]

Observations:

*Likely included in commission and brokerage expense, which is net of $2.1 million ceded to reinsurers **Largest write-in item is “other professional services” at $891,000. ***Includes $1,958 of unpaid current year expenses and write-ins like “other technology” and “contractors”[/caption]

Observations:

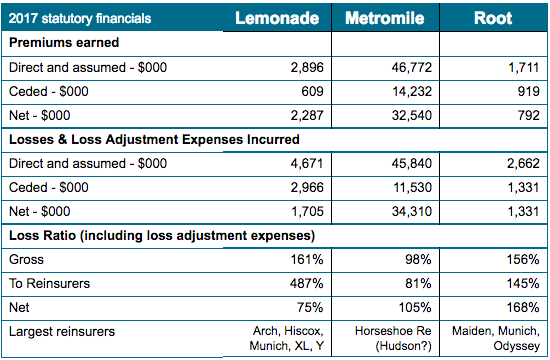

(Source: Schedule P; subject to minor variations compared to prior tables)[/caption]

Observations:

(Source: Schedule P; subject to minor variations compared to prior tables)[/caption]

Observations:

- Underwriting results have been poor

- It costs $15 million a year to run a startup insurtech carrier

- Customer acquisition costs and back-office expenses (so far) matter more than efficiencies from digitization and legacy systems

- Reinsurers are supporting insurtech by losing money, too

- In recent history, the startup insurers that have won were active in markets not targeted by incumbents

*The company has gross paid-in surplus of over $31 million so this figure is probably low. **Excludes a write-in for “revenue from parent for administrative costs,” possibly a way of topping up the company’s surplus[/caption]

A combined ratio greater than 100% usually means a loss. Combined ratio doesn’t include returns from investing insurance reserves, but the days of double-digit bond yields are long gone. In a low-rate environment, investment income can’t offset poor technical results. The ratios are typically calculated on net earned premiums, but we also show a row where the expense ratio denominator is total direct premiums written, which may be more appropriate for growing books.

Observations:

- Lemonade

- Considering the statutory top line before reinsurance of $8,996,000 of gross premium written, it’s unclear how Lemonade calculated that “our total sales for 2017 topped $10 million.” The premiums reported by Lemonade may already have deducted the 20% fee paid to the affiliated agency – the parent company’s only source of income due to the giveaway model. (This would also explain why there is no commission and brokerage expense showing.)

- Lemonade claims to have insured “over 100,000 homes.” If we assume that this figure includes rented apartments, then it implies premium written per policy of $90, or $7.50/month, if premium written is based on an annual policy.

- Lemonade’s giveaway does not appear to be separately disclosed. Nonetheless, one of the brilliant aspects of the business model is the fact that even with a 791% combined ratio, Lemonade still has at least one or two pools doing well and thus enabling the PR of a giveback.

- Metromile

- As the oldest startup in this group, Metromile has by far the highest premium, but the loss ratio is still nearly 100%. The expense ratio appears to have scaled down to a reasonable number, but the company puts $7 million of expense into “loss adjustment expense,” which may flatter the expense ratio.

- Root

- As with Lemonade, the loss ratio around 160% is cause for concern – is this a few volatile claims (bad luck) or a problem with pricing? Time will tell.

- Berkshire Hathaway Direct Insurance sells online via biBERK.com but isn’t a venture-backed startup. They wrote $6.4 million in premium last year, their second year of operations, most of it workers' compensation. Their loss ratio gross of reinsurance was 124%.

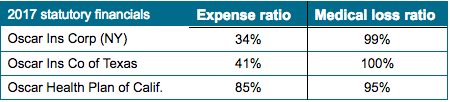

- Oscar is a startup brought to you by Jared Kushner and others who have plowed in $728 million already, with more funds being raised currently. Oscar shows no signs of profitability in its three main states:

1. Underwriting results have been poor

All three companies have a gross loss ratio of near 100% or higher. (For reference, the industry average in 2016 was 72%). That means they have paid $1 as claims for each $1 earned from policyholders in the last 12 months.

An insurance startup has to prove two critical things:

- Does the underwriting model work?

- Does the distribution model work?

*Likely included in commission and brokerage expense, which is net of $2.1 million ceded to reinsurers **Largest write-in item is “other professional services” at $891,000. ***Includes $1,958 of unpaid current year expenses and write-ins like “other technology” and “contractors”[/caption]

Observations:

- Lemonade:

- This startup is spending almost $1 in advertising for every $1 of premium they wrote ($7.7 million of advertising for $9 million of premium written). Again, if we assume Lemonade has insured 100,000 homes and apartments, then the customer acquisition cost (CAC) assuming only advertising expense is around $77. This is probably a measure that encourages the company’s backers, because the CAC of a renewal policy written directly is minimal, and the industry-average churn rate is single digits in U.S.

- The regulatory and overhead costs are considerable – notice lines like legal and auditing; taxes, licenses and fees; and some of the salary expense.

- The volumes have to continue to grow exponentially for some years to get the cost base (also net advertising) lower than the 20% of the premium required to make a profit for the parent company (for reference, the market average expense ratio was 28%). Recall that Lemonade’s parent or affiliates take a 20% flat fee up front for their profits and expenses and gives to charity anything left after paying claims and reinsurance.

- Metromile:

- Has the highest tax expense, perhaps because it is selling the most, with many states charging premium tax as a percentage of the policy value.

- Their “legal and auditing” expense is probably much higher but is put into “other.”

- Note the absence of advertising expense but large commission and brokerage expense, partially ceded to reinsurers. Accounting treatments, as ever, can vary by company.

- Root

- The company’s small volume makes it difficult to run the same absolute expenses as Lemonade and Metromile, but it might not be wise to grow a book running a loss ratio of more than 150%.

- Has no telegraph expense (woo-hoo!).

- Unclear why the company has almost $2 million of unpaid expense.

(Source: Schedule P; subject to minor variations compared to prior tables)[/caption]

Observations:

- Lemonade seems to have a great reinsurance scheme, but they have to hope that reinsurers continue to take $5 in losses for every $1 in premium ceded to them. The amounts ceded are small, and Lemonade has a big panel of reinsurers.

- Metromile and Root do not appear to get much loss ratio benefit from their reinsurance.

- 21 specialized in high-volatility catastrophic risk like hurricanes or earthquakes. Incumbent carriers have largely stopped or greatly limited their new business in certain catastrophe-exposed regions, sometimes because they felt that regulators or competitors (often government-run pools) did not allow them to charge adequate premiums.

- Nine were motor insurers, mostly non-standard motor. Non-standard means bad drivers, exotic cars or other risk factors that “standard” carriers avoid.

- Two don’t have a rating.

- Two remain: Trupanion (a pet insurer) and ReliaMax (which insurers student loans).

- Are urban millennials actually a new market that is being ignored by incumbents?

- Are direct and B2B2C distribution really new markets that incumbents cannot penetrate? Can “platformification” be profitable over the long term?

- How quickly can new/digital systems show cost and pricing benefits over legacy systems that incumbents are retooling aggressively today? How long before the new systems become a legacy for the newcomer that created them?

- Are new underwriting and claims techniques like the use of big data sufficiently disruptive to allow entry to tightly guarded markets?