Some 25 years after the publication of Nicholas Negroponte’s seminal "Being Digital," it feels trite to write about how digital capabilities and the expectations they create among customers have transformed even traditionally sleepy industries like insurance. Yet, the digital transformation of insurance is not a narrative of progressive evolution but rather a story of successive and disruptive waves. And we are on the cusp of a third one.

The first wave saw insurers learn to exploit digital tools to sell directly to customers. Established players as well as a plethora of tech-first startups proved it was possible to sell insurance online to customers without the benefit of an agent.

The second wave, still in flight, focuses on customer experience, bringing better and easier ways for insurers to process applications, serve customers and pay claims. These efforts have brought new efficiencies to an industry hyper-focused on cost while at the same time addressing the needs of consumers who expect immersive and contextualized digital interactions with all the businesses they patronize.

The third wave, in its infancy, focuses on ecosystems, that is the embedding of insurance within the value chains of other industries. An online world, dedicated to selling us cars, homes, travel experiences and financial services is now discovering the opportunity to bundle insurance with the goods and services they provide. Such bundling addresses customers at the moment of need, at the life event – a new home or car purchase, for example – which triggers the need for insurance protection. Insurance in such a model is, as the title and summary of this article suggest, like French fries, a digital side dish suggested as an add-on to the main course. In the years ahead, we will increasingly see more and more businesses ask the question, “Do you want insurance with that?”

Whose brand is it anyway?

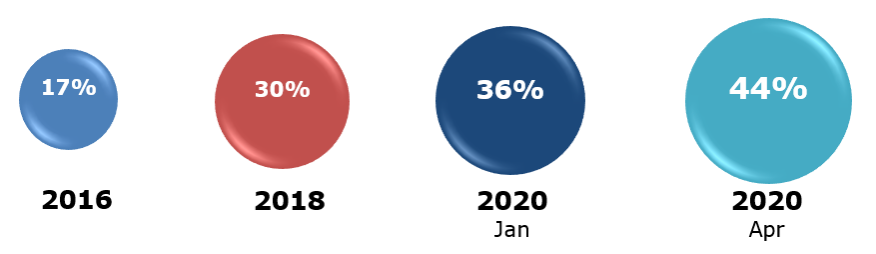

Big Tech has done the spade work for this third wave of transformation. Well before COVID-19, customers were becoming increasingly receptive to the idea of buying insurance from Big Tech firms. And around 44% of the consumers we interviewed as part of Capgemini’s World Insurtech Report 2020 said they would consider coverage offered by Big Tech.

Policyholder willingness to purchase Big Tech coverage is on the rise

The fact that Big Tech has earned and retained customers' trust during various lifestyle interactions is the catalyst behind their increasing willingness to buy insurance, too. Customers say they can count on tech giants for stellar digital experience, intuitive services and real-time response.

So far, Big Tech has been making slow, yet deliberate, inroads into the insurance space. Google subsidiary Verily announced plans in August 2020 for its own insurance company (backed by the commercial insurance unit of Swiss Re Group) to provide tech-driven employer health insurance plans. Verily has also made a health-tracking smartwatch for research use. Amazon invested in Acko Insurance to offer auto coverage via the India-based startup’s platform. Big Tech firms are also integrating existing products (Apple Watch or Amazon Alexa) into the insurance value chain or developing convenient and time- and money-saving offerings that appeal to a broad range of policyholders.

These findings with respect to Big Tech are consistent, of course, across industries. The erosion of traditional brands in favor of new digital ones has occurred in every sector.

See also: Pioneering Use Cases for IoT in Insurance

Equally important is the extent to which the willingness to buy from Big Tech extends to a broader ecosystem of digital-first businesses. Disruptive industry-specific players, most notably in automotive, are as big a change agent as Big Tech. Buying car insurance from Carvana, home insurance from Zillow or small business insurance from Quickbooks makes all the sense in the world, particularly when these digital behemoths demonstrate the power to use data to make the right offer at the right time at the right price.

The challenge to the industry to adapt is profound.

What’s an insurer to do?

As Big Tech and other online powerhouses look to turn insurance into the new French fry, insurers must consider the implications of this digital third wave and choose strategies through which they both embrace and differentiate in the new world of embedded insurance.

Most obvious and relevant is the ability to embrace the new channels. Insurers have always relied on third parties for distribution. A shift in mindset to see e-businesses as the agents of the future requires cultural change and paradigm realignment but is not revolutionary from a business model perspective.

The bigger challenge in many respects is on the technology-side. The constraints of legacy systems and brittle enterprise architectures, which shockingly persist 25 years after Negroponte, limit the ability of insurers to plug and play seamlessly in the new ecosystem. Developing an API framework that enables insurers to connect safely and securely with a broad array of distribution partners – what we at Capgemini call Open Insurance – is a prerequisite to being part of the coming disruption and not a victim of it.

Along with the API-ification of insurance technology comes significant requirements to up the game with respect to data. Succeeding in the new ecosystem, as noted above, requires being there at the right time with the right product at the right price. Doing so requires real-time customer insight, which comes from data mastery. We have been slow to get there. Less than 40% of insurers say they have access to IoT devices and natural language processing (NLP) support systems to enable real-time insights. Producing and leveraging analytics at scale will be the battlefield for this third wave of digital.

Not all French fries are created equal

It will, of course, take more to succeed in the new ecosystem than technological advances.

Competitive differentiation among insurers will need to come from the insurance product itself. In a world where traditional brands have ever-diminishing salience, product and price are the only bases for competition. The standardized products the industry currently offers will force an inexorable race to the bottom, where the cheapest wins. Look for product innovation to be the true benefit of the third digital wave.

See also: o You Know What You Don’t Know?D

The demand is already there. Only some insurers see it.

Incumbent insurance executives interviewed as part of the World Insurance Report 2020 were behind customer expectations regarding new products. Only half of the executives we talked with said they had rolled out usage-based insurance (UBI), such as pay-as-you-drive (PAYD) offerings. Conversely, customers’ year-over-year interest in UBI climbed from 35% in 2019 to more than 50% in 2020. Less than half of the insurers we interviewed said they effectively target promotions at critical life-phase moments, and fewer than 25% said they use artificial intelligence systems to track external data.

The challenges to insurance product innovation are not trivial. Complex regulatory regimes create significant hurdles, making almost impossible the “fail fast” mindset that drives innovation in other sectors. But the challenge for insurers is indeed existential. As the aficionados of one or another fast-food empire will attest, the fries may be a side dish, but they are often the best part of the meal. Insurance should learn from this example.