Across the insurance industry, claims organizations have made significant progress in modernizing their core processing systems in the last several years. Typically, the objectives of these programs are to increase speed, improve accuracy and reduce risks in all phases of claims handling. Given that claims interactions are “moments of truth” in customer relationships, insurers have good reason to ensure that the experience for policyholders is smooth and satisfying at every step of the process.

No matter where insurers are on this continuum, robotic process automation (RPA) can help them achieve their business objectives while leveraging existing technology and boosting returns on previous and current transformation investments. In seeking the best path forward, claims leaders will want to consider:

Suggested approach and lessons learned: following the leaders

Significant numbers of insurers are already using RPA in their claims organizations. In designing the business case for robotics, claims leaders should seek an incremental approach, adopting more ambitious use cases once they have built momentum and demonstrated results through initial and targeted deployments. With RPA, there’s no need to try do too much too fast, which may be attractive for insurance executives seeking to minimize risk and disruption in their adoption of enabling technologies. Further, an incremental approach can help organizations overcome their natural wariness toward RPA in terms of its workforce impacts.

See also: Robots and AI—It’s Just the Beginning

The following lessons learned come from early adopters:

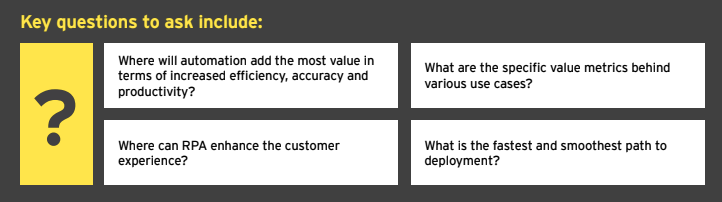

Target the opportunities: In developing a business case and tangible ROI model, specific tactical questions can lead to the right strategy as well as clarify the highest priorities for near-term automation. Finding answers may require a robust assessment of current capabilities and the completion of a cost-benefit analysis, given that the candidates for automation may number into the dozens.

Engage IT early and often: To ensure a smooth implementation and integration with other systems, there are many important infrastructure, governance and security questions to address. IT leaders reluctant to deploy another technology in the claims “stack” should consider how RPA can support strategic platform upgrades and those mandated by regulatory change. Most RPA tools are product- and platform-agnostic and work with existing IT architecture.

Find the right partner: External vendors and suppliers – including insurtechs, consultants and systems integrators – will be part of the solution, so it’s important to choose wisely. Beyond technical expertise, look for those firms with deep technical and operational claims knowledge, including a clear understanding of how it affects the customer experience.

Don’t overlook the organizational factors: As with other “digital” initiatives, claims leaders must invest time and resources in education and, if necessary, evangelization regarding the use of RPA. The delicate matter of robots taking over jobs should be addressed, most likely in the context of the need to reskill claims workers, as the role will evolve to become more analytical and more focused on customer needs and the most complex claims.

The bottom line: RPA is critical to the evolving claims process

The time for adopting robotics in claims has come, due primarily to the compelling business case and imperative for claims leaders to enhance performance and contribute more value to the business. Robotics can serve as a foundation in supporting true, end-to-end automation when integrated with other advanced technologies, such as OCR, chatbots, machine learning and NLP.

Indeed, as multiple early adopters have made clear, RPA is ready to help claims organizations advance and enhance outcomes in the digital era through increased automation, higher productivity and increased capacity and strategic focus for claims professionals.

RPA is among the top enabling technologies insurers should consider adopting in claims, as well as other parts of the organization, due to:

Suggested approach and lessons learned: following the leaders

Significant numbers of insurers are already using RPA in their claims organizations. In designing the business case for robotics, claims leaders should seek an incremental approach, adopting more ambitious use cases once they have built momentum and demonstrated results through initial and targeted deployments. With RPA, there’s no need to try do too much too fast, which may be attractive for insurance executives seeking to minimize risk and disruption in their adoption of enabling technologies. Further, an incremental approach can help organizations overcome their natural wariness toward RPA in terms of its workforce impacts.

See also: Robots and AI—It’s Just the Beginning

The following lessons learned come from early adopters:

Target the opportunities: In developing a business case and tangible ROI model, specific tactical questions can lead to the right strategy as well as clarify the highest priorities for near-term automation. Finding answers may require a robust assessment of current capabilities and the completion of a cost-benefit analysis, given that the candidates for automation may number into the dozens.

Engage IT early and often: To ensure a smooth implementation and integration with other systems, there are many important infrastructure, governance and security questions to address. IT leaders reluctant to deploy another technology in the claims “stack” should consider how RPA can support strategic platform upgrades and those mandated by regulatory change. Most RPA tools are product- and platform-agnostic and work with existing IT architecture.

Find the right partner: External vendors and suppliers – including insurtechs, consultants and systems integrators – will be part of the solution, so it’s important to choose wisely. Beyond technical expertise, look for those firms with deep technical and operational claims knowledge, including a clear understanding of how it affects the customer experience.

Don’t overlook the organizational factors: As with other “digital” initiatives, claims leaders must invest time and resources in education and, if necessary, evangelization regarding the use of RPA. The delicate matter of robots taking over jobs should be addressed, most likely in the context of the need to reskill claims workers, as the role will evolve to become more analytical and more focused on customer needs and the most complex claims.

The bottom line: RPA is critical to the evolving claims process

The time for adopting robotics in claims has come, due primarily to the compelling business case and imperative for claims leaders to enhance performance and contribute more value to the business. Robotics can serve as a foundation in supporting true, end-to-end automation when integrated with other advanced technologies, such as OCR, chatbots, machine learning and NLP.

Indeed, as multiple early adopters have made clear, RPA is ready to help claims organizations advance and enhance outcomes in the digital era through increased automation, higher productivity and increased capacity and strategic focus for claims professionals.

RPA is among the top enabling technologies insurers should consider adopting in claims, as well as other parts of the organization, due to:

- Why robotics is well-suited for use in claims and how it complements other enabling technologies

- Key components of the business case and value proposition

- High-priority opportunities and common use cases for deploying RPA

- Applying the principles and techniques used by successful early adopters as they develop their own implementation approach

- Automate discrete tasks or activities

- Work in concert with other systems on transaction processing, data manipulation, communication and response triggering

- Facilitate straight-through or “no-touch” processing, working alongside analytics tool sets and other cognitive technologies, such as machine learning and natural language processing

-

- Streamlining vendor applications and estimating: Most current estimating processes require adjusters or others to rekey data from one form or system to another. Robotics along with enabling technology such as optical character recognition (OCR) can eliminate that duplicate effort by bridging the gap between claims systems, vendor apps and third-party estimating systems.

- Capturing and managing claimant data: RPA can be on the receiving end of claims submissions, especially those that typically include photos from customers. Robots can ensure the right information ends up in the right systems and attached to the right claims. As such, they ensure human representatives have the information they need to move claims forward and respond to customer inquiries. Customers who prefer self-service also benefit when submitted information is more readily accessible.

- Streamlining, automating and enhancing communications: Claimant communication remains a largely manual undertaking, requiring adjusters or other claims staff to initiate and, in some cases, monitor the process. RPA can help operationalize smart rules so the right letter (e.g., one required to be sent 30 days after a loss is reported) reaches the right claimant at the right time through the right channel. For instance, robots can pull data from claims submission forms and pre-populate letters that are typically housed in other systems and map distribution to customer preferences.

- Scanning, indexing and converting forms and data: RPA has proven especially proficient at pulling data from standard fields on medical bills, from claimant name and address, to provide information to coding details. Standard in name only, these forms are a common source of errors. Similarly, RPA can transfer and convert data across older claims systems that may be used by individual product lines or regions to newer enterprise systems.

- Validating payments: Conventional wisdom holds that 3-5% of claims payments are inaccurate, though no one knows for sure, given the difficulty and expense in auditing all claims. The key is robots’ ability to quickly and cost-effectively run QA on entire populations of forms and payments, rather than just a small sample. For example, rather than auditors discovering a $5,000 payment on a $500 settlement months after a customer has cashed the check, robots can flag the disparity beforehand. Further, they can help deliver the information and intelligence so that human analysts can investigate anomalies proactively.

- Customer-facing enhancements: RPA can alleviate the need for time-consuming and costly adjuster input by supporting customer-friendly apps for capturing photos of fender-bender car accidents and submitting all claims submission forms with just a few taps and swipes. Chatbots, another automation tool easily integrated with RPA, are already handling many routine communications tasks, including notifications of settlements and customer inquiries into claim status.

- Integrating other enabling technologies: RPA will become more prevalent, especially as claims groups adopt other enabling technologies. For instance, AI-powered bots will likely handle the inputs from drones conducting standard property inspections or surveying damage after catastrophic storms. Integrating RPA with machine learning and natural language processing (NLP) can enable the initiation of new claims and issue first notice of loss (FNOL) communications by scanning and analyzing unstructured communications, including emails from agents or even voice interactions. Robots will also be used widely in the real-time review of social media streams to assess claims severity and reduce fraud. RPA will receive and route advanced telematics data (including video imagery) that will be instantaneously captured during automobile accidents and downloaded from the cloud, automatically triggering an FNOL entry.

Suggested approach and lessons learned: following the leaders

Significant numbers of insurers are already using RPA in their claims organizations. In designing the business case for robotics, claims leaders should seek an incremental approach, adopting more ambitious use cases once they have built momentum and demonstrated results through initial and targeted deployments. With RPA, there’s no need to try do too much too fast, which may be attractive for insurance executives seeking to minimize risk and disruption in their adoption of enabling technologies. Further, an incremental approach can help organizations overcome their natural wariness toward RPA in terms of its workforce impacts.

See also: Robots and AI—It’s Just the Beginning

The following lessons learned come from early adopters:

Target the opportunities: In developing a business case and tangible ROI model, specific tactical questions can lead to the right strategy as well as clarify the highest priorities for near-term automation. Finding answers may require a robust assessment of current capabilities and the completion of a cost-benefit analysis, given that the candidates for automation may number into the dozens.

Engage IT early and often: To ensure a smooth implementation and integration with other systems, there are many important infrastructure, governance and security questions to address. IT leaders reluctant to deploy another technology in the claims “stack” should consider how RPA can support strategic platform upgrades and those mandated by regulatory change. Most RPA tools are product- and platform-agnostic and work with existing IT architecture.

Find the right partner: External vendors and suppliers – including insurtechs, consultants and systems integrators – will be part of the solution, so it’s important to choose wisely. Beyond technical expertise, look for those firms with deep technical and operational claims knowledge, including a clear understanding of how it affects the customer experience.

Don’t overlook the organizational factors: As with other “digital” initiatives, claims leaders must invest time and resources in education and, if necessary, evangelization regarding the use of RPA. The delicate matter of robots taking over jobs should be addressed, most likely in the context of the need to reskill claims workers, as the role will evolve to become more analytical and more focused on customer needs and the most complex claims.

The bottom line: RPA is critical to the evolving claims process

The time for adopting robotics in claims has come, due primarily to the compelling business case and imperative for claims leaders to enhance performance and contribute more value to the business. Robotics can serve as a foundation in supporting true, end-to-end automation when integrated with other advanced technologies, such as OCR, chatbots, machine learning and NLP.

Indeed, as multiple early adopters have made clear, RPA is ready to help claims organizations advance and enhance outcomes in the digital era through increased automation, higher productivity and increased capacity and strategic focus for claims professionals.

RPA is among the top enabling technologies insurers should consider adopting in claims, as well as other parts of the organization, due to:

- Low cost

- The path to ROI

- Manageable deployment requirements

- Flexible use cases