In April, something significant happened in the auto industry: Tesla confirmed that production had begun on its Cybercab, a fully autonomous vehicle with no steering wheel, no pedals, and no human in the loop. Until now, the conversation has focused on what this means for Uber and Lyft and on whether robotaxis are going mainstream.

But perhaps there's an equally consequential question. What happens to the insurance industry once the driver has gone the way of the Edsel? Unfortunately, the industry has not seriously tried to answer it.

The Model Was Built Around the Human

Commercial auto insurance was designed around a single variable: the person behind the wheel. That is why insurance prices reflect driving behavior; liability follows whoever was driving, and policy language assumes a human making decisions on the road in real time. The full architecture of risk assessment, premium calculation, and claims resolution rests on the assumption that human judgment is what gets priced.

Open almost any commercial auto policy today, and the human driver as the unit of risk appears on nearly every page. But remove the driver, and pricing assumptions, liability triggers, and claims logic all rest on a human variable that no longer exists. So the language built for that world has to be rewritten.

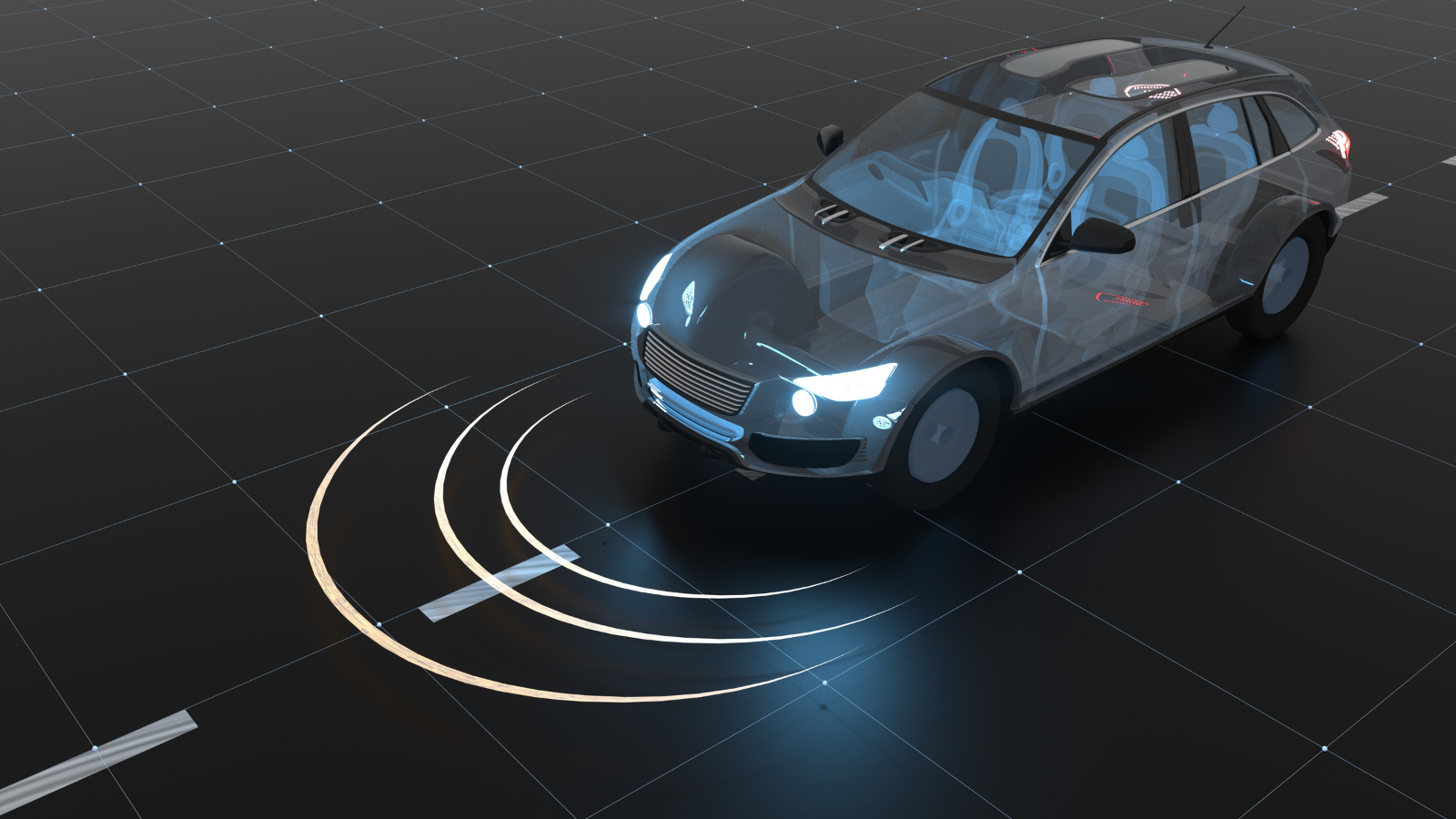

Autonomous vehicles are no longer theoretical. From Level 3 consumer vehicles to more than 700,000 weekly robotaxi rides globally, deployment is moving faster than the regulatory frameworks meant to govern it. With that comes an even deeper anxiety the industry rarely discusses openly - autonomous vehicles are much safer than vehicles with human drivers. Research in Traffic Injury Prevention found Waymo cut injury-causing crashes by 79%, with intersection crashes down 96%. Tesla reports Full Self-Driving (Supervised) improves U.S. road safety by over 80%.

On its face, all of this is nothing but good news. But for an industry where roughly half of all premiums are tied to auto, those numbers describe an existential shift. Fewer claims are indeed good for society, but they also represent a fundamental challenge for a business model never redesigned to reflect it.

The Transition Is the Real Challenge

The most challenging chapter is perhaps underway, in the chaotic middle ground before full autonomy becomes the norm.

Waymo's current operating model shows how messy this can be. In Austin, it has partnered with Uber, while in San Francisco it competes directly against Uber and Lyft. In both markets, it works with maintenance fleets including Hertz, Avis, and new AV service companies. Each raises different insurance questions.

Once a Waymo comes off the road and a human driver takes it in for service, there is no settled answer for what is being insured. These vehicles can be worth hundreds of thousands of dollars due to their embedded sensors and software. If a maintenance technician damages a radar unit and that vehicle later causes an accident, is the resulting liability an auto insurance issue or product liability? Current policies do not offer a clean answer.

Mixed-fleet operations carry that ambiguity: overlapping liability, unclear ownership of risk, and policy language written for a world that no longer exists. The work ahead, therefore, is a fundamental redesign of how liability gets assigned in multi-party autonomous operations. When something goes wrong, the question of responsibility, whether the OEM, the platform, the maintenance fleet, or the software provider, has no clean answer.

Data is the starting point, and fleets like Waymo and Tesla are sitting on enormous amounts of operational data that could reshape how risk is understood and priced. But that means insurers need access to that data, and the frameworks to build products around how these vehicles actually operate.

Regulators have a significant role to play, too, because the state-by-state patchwork that just about worked for rideshare will not scale for autonomous vehicles. Federal coordination on liability standards and minimum insurance requirements for AVs would give the industry a target to build against.

The Window to Get Ahead Is Narrower Than It Looks

The rideshare era offers a partial template. When Uber arrived, insurance took years to catch up, but the industry muddled through. However, the trajectory this time looks faster. Nevertheless, unlike the rideshare era, the industry already knows how to build insurance products for markets without a rulebook.

But the scale is different, the liability questions more complex, and the next major AV incident will create enormous pressure to fix things quickly, in public, under scrutiny. Waiting for that moment is the wrong strategy.

Insurance has to shift from static to dynamic, using real-time data to map how risk is distributed across platforms, fleets, maintenance partners, and technology providers. Liability has to follow that data through every link in the chain.

Adapting will not be enough, because a model that priced human behavior for a century is finished. What replaces it will look almost nothing like today's commercial auto insurance. Carriers treating this as a rebuild will define the next era of mobility risk. Everyone else will be left writing policies for a road that no longer exists.