In today’s world, technology is making everything easier, more efficient, and less expensive. Unfortunately, one area where technology efficiency has not impacted the insurance industry is in the active use of electronic signatures for applications and other forms. This is unfortunate, as significant productivity gains and expense reductions can be achieved by the widespread use of electronic signatures for most insurance transactions.

While many agents and brokers have heard of electronic signatures, some questions still remain. Is a digital signature truly legal? Will it hold up in court? Are cloud-based digital signatures secure? What choices do I have for e-signing documents?

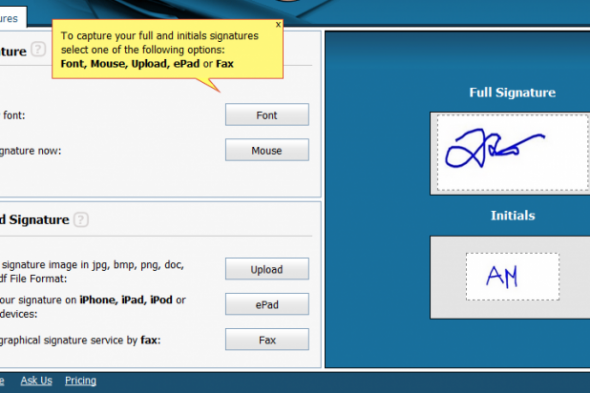

Workflow improvement

Consider how a simple insurance agency workflow—getting an application signed—could be improved with an electronic signature process. The basic workflow steps currently look like this:

- Agency staff inputs application information into the agency management system.

- The ACORD application is generated by the system and is probably printed as an electronic PDF file.

- The electronic application is sent as an email attachment to the client for signature.

- The client physically prints out a copy of the applications and signs with a pen. They then scan the application and email it back to the agency.

- Agency staff receives the signed application, forwards it to the insurance company for processing, and attaches the document to the client file.

- Agency staff inputs application information into the agency management system.

- The ACORD application is generated by the system, attached to an email, and sent to the policyholder for their signature.

- The client receives the email and opens the document. They electronically sign the document and immediately send it back to the agency.

- Agency staff receives the electronically signed application, forwards it to the insurance company for processing, and stores the document in the client file.

- The signature must be logically associated with the document.

- Both parties must have agreed to conduct the transaction via electronic means.

- If the sender inhibits the receiver’s ability to either store or print the record, the document is not enforceable against that recipient.