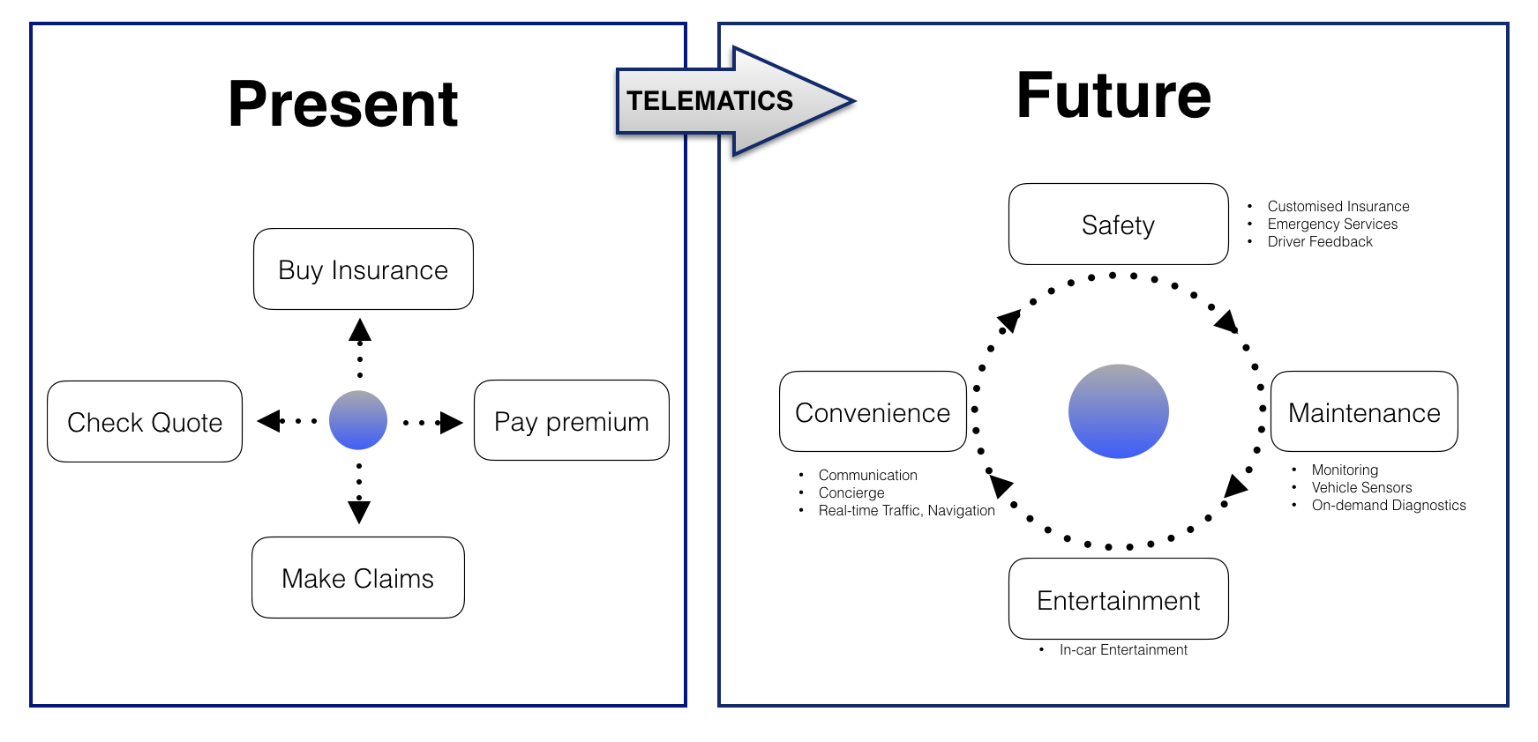

Telematics has the potential to dramatically alter the auto insurance industry, from personalized premiums based on individual driving data to automated emergency services and entertainment-based add-ons to more immediate and active management of claims.

Risk Assessment

Risk Assessment

Value Proposition

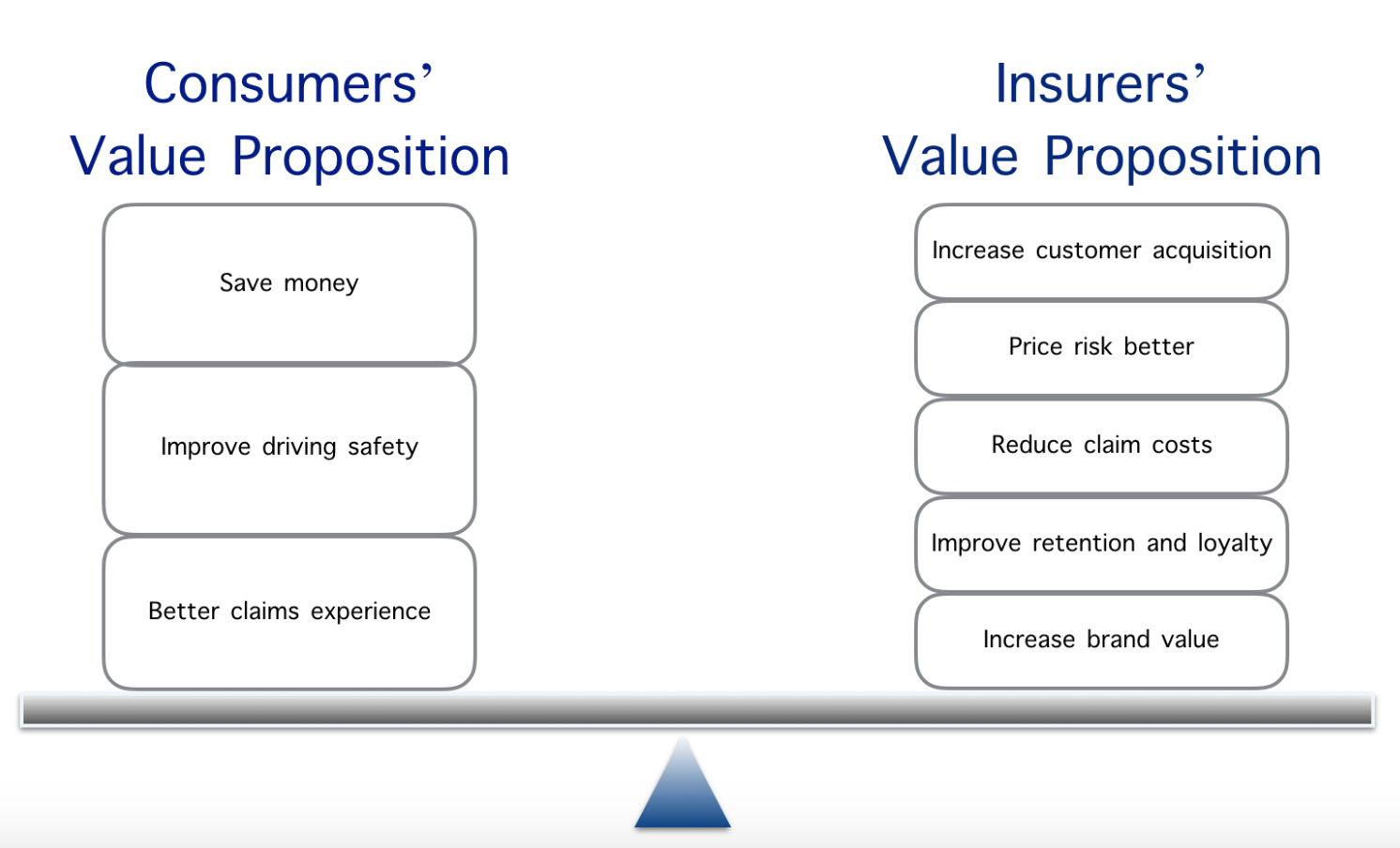

Telematics has much to offer both consumers and insurers.

Value Proposition

Telematics has much to offer both consumers and insurers.

Solution Analysis

Technology solutions available today are similar in terms of what is possible, but there is a difference in the manner that information is collected, delivered and used. When selecting the most appropriate technology solution and provider to partner with, I recommend the following considerations:

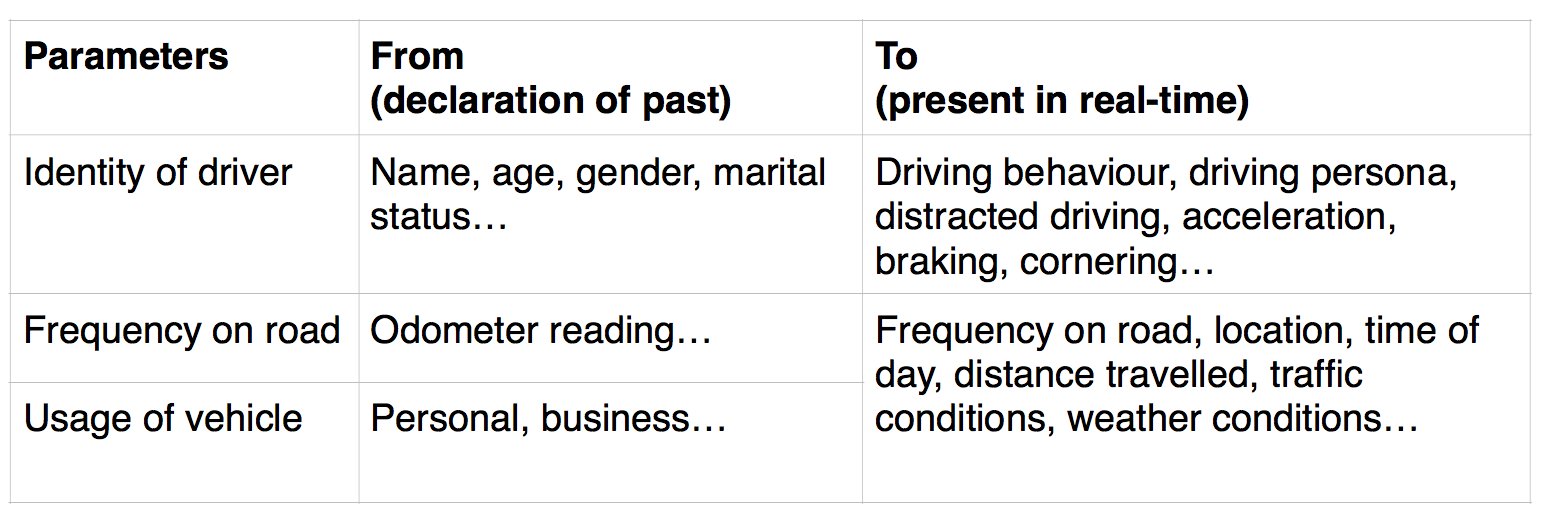

1. Telematics Model (PAYD, PHYD, CYD, Embedded): Several telematics models are emerging with varying levels of consumer interaction and integration.

Pay As You Drive (PAYD) is a mileage-based system that has been around for some time in varying forms. A device is installed in the car to validate when and where a car is driven. More advance systems are available now.

Pay How You Drive (PHYD) considers driving style and behavior in addition to collecting mileage and GPS data. The average driver has one accident every 10 to 12 years, but more common are unsafe driving maneuvers that increase the likelihood of an accident. An accelerometer used in the PHYD models can provide event information such as abrupt acceleration, deceleration, hard braking and sharp turning, which help us understand driving behavior and predict accident claims better.

Control Your Driving (CYD) goes to the next level. While PAYD and PHYD models are about collecting data rather than interacting with consumers, therefore passive in nature, CYD uses the data to provide constructive feedback to drivers through mobile or in-vehicle interfaces and potentially improves driving habits. There is sufficient evidence that driving behavior can be improved with feedback. The teen and elderly markets are niches for early adopters of this model.

Vehicles embedded with telematics devices are the long-term aspirations of both automakers and insurers. These systems provide all-around safety and driving assistance. These systems usually include services such as adaptive cruise control, collision warning, lane assistance and blind-spot detection. This model is growing fast in the auto market, driven by the safety benefits of reduced driving risk. New technology can enable additional services and features like safety controls activated when poor road conditions are detected by the GPS. BMW’s connected drive is the first step in this direction. Mobileye is helping autonomous cars "see" via crowdsourcing; the company has outfitted 4,500 NYC Uber and Lyft cars with anti collision technology. Some analysts project that all major manufacturers will have embedded telematics solutions in their cars within the next five years.

See also: Game Changer for Auto Telematics

2. Data Protection (collection, use, disclosure and storage of personal information): Telematics generates big data. Therefore, the ownership, collection, use, disclosure and storage of data becomes crucial in gaining trust and loyalty.

Privacy: The success of other industries indicates that people are willing to trade some of their privacy in return for the right services, in the right time at the right place. That has proved true in social media, Uber, online credit card use and internet banking. When it comes to telematics, though, the stigma of insurance companies and the fear that data about driving behavior could be misused are causing concern. To overcome this hurdle, we must be as transparent as possible up front, offer the right amount of value-added services and carefully position the offering with the right messages to win over consumers. The telematics solution selected must provide a feasible program that gets appropriate access to driving patterns without seeking access to too much data. Aggregated driving scores, limitations on driving history and GPS use and specialized onboard data analysis functions could mitigate these concerns. As long as we know about driver safety and potential risks, we don’t need to dive deep into consumers' personal data.

Storage: Dynamically generating data within an automobile or mobile phone creates challenges. The sheer amount of data generated makes it difficult, if not impossible, to store it within the automobile or mobile phone itself. Thus, decisions about what to store, and where, become very important. This issue is amplified by the privacy concern of data storage. In cases where certain pieces of data are not stored within the automobile or mobile phone, the retention aspect of privacy policies becomes important. Once the data is destroyed, there is no way to recover it. Moreover, unlike static data, which is collected only once by any interested party, dynamic data is collected repeatedly by a service provider to keep it up to date. Thus, there has to be a continuous transfer of dynamic data from many vehicles through the telematics service provider to application service providers. This requires an efficient and scalable evaluation of constraints in the privacy policies.

Security: The growth of e-commerce on the web has been limited by the reluctance of consumers to release personal information. 94% of web users decline to provide personal information to websites at one time or another when asked, and 40% who provide demographic data have gone to the trouble of fabricating it. If potential auto telematics users share the concerns of web users, then a large segment of the potential telematics market, perhaps as much as 50%, may be lost. There is significant potential for misuse of data collected. Consumers may substitute false data or hack into vehicle applications. Telematics service providers may sell consumer data to third parties without the permission of consumers. Therefore, telematics applications will be successful if providers know that the data they receive is accurate and if consumers know that their privacy is assured. Data protection must provide both privacy and security protection. Telematics solutions that can achieve that protection while enabling the sharing of data are the most viable options.

3. Ease of Installation (solution access): Complex installation processes (like blackbox installation) result in lack of interest and conversions from the traditional insurance model to the telematics model. AXA launched a mobile telematics solution in some of its international markets but was unsuccessful in acquiring a buy-in from consumers as the app had to be switched on before a drive. Such a solution leaves room for anti-selection and requires additional effort in the day-to-day lives of consumers. Even insurers like Progressive have only managed to convert approximately 20% of their book of business to the telematics model despite more than a decade of marketing initiatives and spending.

4. Ease of Use (interaction and feedback): The telematics solution selected must be intuitive and easy to use for both consumers and insurers. It should help us identify the risk (item that is insured), peril (anything that could cause damage — breakdown, weather conditions, fire, water, ice, road conditions, accident, etc.) and hazards (anything that increases the chances of peril — speeding, hard braking, driving behavior, etc.). The solution must be able to answer questions such as who is driving, how well the person is driving and how much is the car being driven. Mobile telematics solutions must be able to distinguish driving from walking, riding a bike or hopping on a train, bus or boat, for instance. The right solution will employ real-time data analytics and feedback to engage consumers, improve driving safety and facilitate better claims experience and meaningful dialogue with insurers.

5. Accuracy (trust): Our business is built on trust. It is imperative that the telematics solution we implement helps build trust and value in the digital age. Data accuracy is crucial in acquiring a buy-in from consumers, assessing driving behavior, pricing and speed and quality of response during a breakdown or accident.

6. Notifications (auto alerts): Most fleet telematics solutions have failed to create value as the focus has been largely on collection of information alone. Such solutions require someone to run reports, analyze them and understand them before taking corrective actions. This results in delayed feedback to drivers and in most instances becomes reduced to just knowing where vehicles in a fleet are (dots on a map). Automatic notification and alerts facilitate information to be reviewed at the right time, in the right place and by the right person for improved service (safety, accident and roadside assistance) and quality of care.

7. Ease of support (cloud): Cloud-based telematics solutions facilitate the delivery of new or upgraded capabilities without stretching IT bandwidth and keep the total cost of data ownership low. This is imperative if we wish to own the data. If not, then partnering with a solution provider that can maintain and support the solution at scale in an economically viable manner is crucial.

Customer Engagement

Engaging customers to improve driving behavior calls for a change in human behavior.

Humans are not inspired to act on reason alone. You don't connect with your audience by using conventional rhetoric, which in the business world usually consists of a PowerPoint presentation in which you say "here is our company’s biggest challenge, and here’s what we need to do to prosper," while building your case through statistics, facts and quotes from authorities. The problem with rhetoric is two-fold. First, the people you are talking to have their own set of authorities, statistics and experiences, so, while you are trying to persuade them, they are arguing with you in their heads instead of being motivated to reach certain goals. Second, if you do succeed in persuading them, you’ve only done so at an intellectual level. That’s not good enough. The theory of rational action that claims human beings are abstract symbol manipulators much like computers that seek to maximize their self-interest has dominated most of the 20th century and is the foundation for major institutions, from stock markets to governments. Research in the last couple of years, though, has led to a profound shift in how we understand human thought and behavior.

Scientists have pieced together enough evidence to know that humans are embodied beings, which means we work the way we do because of the kinds of brains we have, the kinds of bodies we have and the typical experiences that pervade our evolutionary history. We know now how real human nature works (mostly). The big picture is that we are profoundly moral beings, and our behavior is shaped by value judgments, deeply held beliefs and assertions about right and wrong. We are profoundly social, and our behavior is influenced by the behavior of those around us through shared stories, common expectations and need for cooperation (and competition). We make decisions through context-based logic determined by how we understand the situations we find ourselves in and reason with our emotions. Try asking someone on a date without those subtle emotional cues of presence, enthusiasm and appeal.

I believe that something as simple as fun can influence human behavior for the better. In a series of experiments, Volkswagen tested this theory. Check it out…

The speed camera lottery

Can we get people to obey the speed limit by making it fun to do so? The winning idea was so good that Volkswagen, together with the Swedish National Society for road safety, actually made this innovative idea a reality in Stockholm.

Piano Stairs

Can we get more people to take the stairs instead of the escalators by making it fun to do so? Piano stairs created on Odenplan underground station in Stockholm have become a hit in cities worldwide from Milan to Santiago and more.

The way to persuading people and ultimately a much more powerful way is by uniting an idea with an emotion. It comes down to good design in our attempts to change human behaviour and will depend on our understanding of REAL human nature. Knowing where we went wrong in the past and what we know now is right, we can engage and design models to promote socially desirable outcomes like reduction in environmental impact and greater sensitivity to the needs of others.

See also: 5 Value Levers for Auto Telematics

Using the fun theory to improve driving behavior is a tested formula that has worked globally and one that I would recommend as a first step. Create a competition that is built off recognition and rewards good behavior. Huge, safe-driving campaigns could be turned into beautiful marketing messages that people would be proud to be a part of. The intelligence and data we collect could change the way we do business altogether.

Liberty Insurance: Drive Well from Michael Hanson on Vimeo.

Delivery

Inventing a future and testing ideas is not enough. To bring auto telematics solution to life, models need to change from actuarial to actuarial plus big data. Implementation will require collaboration between solution providers, underwriters, actuaries and product and marketing teams to create economically viable customer propositions, storytelling and messaging that connects with your audience and keeps their attention long enough to convert.

Scale

Companies like Uber and Lyft struggle with public perception and regulations globally. Partnering with them and creating compelling value propositions for their drivers presents an opportunity for efforts in auto telematics to scale quickly.

Conclusion

The winners will be early movers that capture the safest drivers, take advantage of pricing power and strengthen customer relationships while easing privacy concerns.

Solution Analysis

Technology solutions available today are similar in terms of what is possible, but there is a difference in the manner that information is collected, delivered and used. When selecting the most appropriate technology solution and provider to partner with, I recommend the following considerations:

1. Telematics Model (PAYD, PHYD, CYD, Embedded): Several telematics models are emerging with varying levels of consumer interaction and integration.

Pay As You Drive (PAYD) is a mileage-based system that has been around for some time in varying forms. A device is installed in the car to validate when and where a car is driven. More advance systems are available now.

Pay How You Drive (PHYD) considers driving style and behavior in addition to collecting mileage and GPS data. The average driver has one accident every 10 to 12 years, but more common are unsafe driving maneuvers that increase the likelihood of an accident. An accelerometer used in the PHYD models can provide event information such as abrupt acceleration, deceleration, hard braking and sharp turning, which help us understand driving behavior and predict accident claims better.

Control Your Driving (CYD) goes to the next level. While PAYD and PHYD models are about collecting data rather than interacting with consumers, therefore passive in nature, CYD uses the data to provide constructive feedback to drivers through mobile or in-vehicle interfaces and potentially improves driving habits. There is sufficient evidence that driving behavior can be improved with feedback. The teen and elderly markets are niches for early adopters of this model.

Vehicles embedded with telematics devices are the long-term aspirations of both automakers and insurers. These systems provide all-around safety and driving assistance. These systems usually include services such as adaptive cruise control, collision warning, lane assistance and blind-spot detection. This model is growing fast in the auto market, driven by the safety benefits of reduced driving risk. New technology can enable additional services and features like safety controls activated when poor road conditions are detected by the GPS. BMW’s connected drive is the first step in this direction. Mobileye is helping autonomous cars "see" via crowdsourcing; the company has outfitted 4,500 NYC Uber and Lyft cars with anti collision technology. Some analysts project that all major manufacturers will have embedded telematics solutions in their cars within the next five years.

See also: Game Changer for Auto Telematics

2. Data Protection (collection, use, disclosure and storage of personal information): Telematics generates big data. Therefore, the ownership, collection, use, disclosure and storage of data becomes crucial in gaining trust and loyalty.

Privacy: The success of other industries indicates that people are willing to trade some of their privacy in return for the right services, in the right time at the right place. That has proved true in social media, Uber, online credit card use and internet banking. When it comes to telematics, though, the stigma of insurance companies and the fear that data about driving behavior could be misused are causing concern. To overcome this hurdle, we must be as transparent as possible up front, offer the right amount of value-added services and carefully position the offering with the right messages to win over consumers. The telematics solution selected must provide a feasible program that gets appropriate access to driving patterns without seeking access to too much data. Aggregated driving scores, limitations on driving history and GPS use and specialized onboard data analysis functions could mitigate these concerns. As long as we know about driver safety and potential risks, we don’t need to dive deep into consumers' personal data.

Storage: Dynamically generating data within an automobile or mobile phone creates challenges. The sheer amount of data generated makes it difficult, if not impossible, to store it within the automobile or mobile phone itself. Thus, decisions about what to store, and where, become very important. This issue is amplified by the privacy concern of data storage. In cases where certain pieces of data are not stored within the automobile or mobile phone, the retention aspect of privacy policies becomes important. Once the data is destroyed, there is no way to recover it. Moreover, unlike static data, which is collected only once by any interested party, dynamic data is collected repeatedly by a service provider to keep it up to date. Thus, there has to be a continuous transfer of dynamic data from many vehicles through the telematics service provider to application service providers. This requires an efficient and scalable evaluation of constraints in the privacy policies.

Security: The growth of e-commerce on the web has been limited by the reluctance of consumers to release personal information. 94% of web users decline to provide personal information to websites at one time or another when asked, and 40% who provide demographic data have gone to the trouble of fabricating it. If potential auto telematics users share the concerns of web users, then a large segment of the potential telematics market, perhaps as much as 50%, may be lost. There is significant potential for misuse of data collected. Consumers may substitute false data or hack into vehicle applications. Telematics service providers may sell consumer data to third parties without the permission of consumers. Therefore, telematics applications will be successful if providers know that the data they receive is accurate and if consumers know that their privacy is assured. Data protection must provide both privacy and security protection. Telematics solutions that can achieve that protection while enabling the sharing of data are the most viable options.

3. Ease of Installation (solution access): Complex installation processes (like blackbox installation) result in lack of interest and conversions from the traditional insurance model to the telematics model. AXA launched a mobile telematics solution in some of its international markets but was unsuccessful in acquiring a buy-in from consumers as the app had to be switched on before a drive. Such a solution leaves room for anti-selection and requires additional effort in the day-to-day lives of consumers. Even insurers like Progressive have only managed to convert approximately 20% of their book of business to the telematics model despite more than a decade of marketing initiatives and spending.

4. Ease of Use (interaction and feedback): The telematics solution selected must be intuitive and easy to use for both consumers and insurers. It should help us identify the risk (item that is insured), peril (anything that could cause damage — breakdown, weather conditions, fire, water, ice, road conditions, accident, etc.) and hazards (anything that increases the chances of peril — speeding, hard braking, driving behavior, etc.). The solution must be able to answer questions such as who is driving, how well the person is driving and how much is the car being driven. Mobile telematics solutions must be able to distinguish driving from walking, riding a bike or hopping on a train, bus or boat, for instance. The right solution will employ real-time data analytics and feedback to engage consumers, improve driving safety and facilitate better claims experience and meaningful dialogue with insurers.

5. Accuracy (trust): Our business is built on trust. It is imperative that the telematics solution we implement helps build trust and value in the digital age. Data accuracy is crucial in acquiring a buy-in from consumers, assessing driving behavior, pricing and speed and quality of response during a breakdown or accident.

6. Notifications (auto alerts): Most fleet telematics solutions have failed to create value as the focus has been largely on collection of information alone. Such solutions require someone to run reports, analyze them and understand them before taking corrective actions. This results in delayed feedback to drivers and in most instances becomes reduced to just knowing where vehicles in a fleet are (dots on a map). Automatic notification and alerts facilitate information to be reviewed at the right time, in the right place and by the right person for improved service (safety, accident and roadside assistance) and quality of care.

7. Ease of support (cloud): Cloud-based telematics solutions facilitate the delivery of new or upgraded capabilities without stretching IT bandwidth and keep the total cost of data ownership low. This is imperative if we wish to own the data. If not, then partnering with a solution provider that can maintain and support the solution at scale in an economically viable manner is crucial.

Customer Engagement

Engaging customers to improve driving behavior calls for a change in human behavior.

Humans are not inspired to act on reason alone. You don't connect with your audience by using conventional rhetoric, which in the business world usually consists of a PowerPoint presentation in which you say "here is our company’s biggest challenge, and here’s what we need to do to prosper," while building your case through statistics, facts and quotes from authorities. The problem with rhetoric is two-fold. First, the people you are talking to have their own set of authorities, statistics and experiences, so, while you are trying to persuade them, they are arguing with you in their heads instead of being motivated to reach certain goals. Second, if you do succeed in persuading them, you’ve only done so at an intellectual level. That’s not good enough. The theory of rational action that claims human beings are abstract symbol manipulators much like computers that seek to maximize their self-interest has dominated most of the 20th century and is the foundation for major institutions, from stock markets to governments. Research in the last couple of years, though, has led to a profound shift in how we understand human thought and behavior.

Scientists have pieced together enough evidence to know that humans are embodied beings, which means we work the way we do because of the kinds of brains we have, the kinds of bodies we have and the typical experiences that pervade our evolutionary history. We know now how real human nature works (mostly). The big picture is that we are profoundly moral beings, and our behavior is shaped by value judgments, deeply held beliefs and assertions about right and wrong. We are profoundly social, and our behavior is influenced by the behavior of those around us through shared stories, common expectations and need for cooperation (and competition). We make decisions through context-based logic determined by how we understand the situations we find ourselves in and reason with our emotions. Try asking someone on a date without those subtle emotional cues of presence, enthusiasm and appeal.

I believe that something as simple as fun can influence human behavior for the better. In a series of experiments, Volkswagen tested this theory. Check it out…

The speed camera lottery

Can we get people to obey the speed limit by making it fun to do so? The winning idea was so good that Volkswagen, together with the Swedish National Society for road safety, actually made this innovative idea a reality in Stockholm.

Piano Stairs

Can we get more people to take the stairs instead of the escalators by making it fun to do so? Piano stairs created on Odenplan underground station in Stockholm have become a hit in cities worldwide from Milan to Santiago and more.

The way to persuading people and ultimately a much more powerful way is by uniting an idea with an emotion. It comes down to good design in our attempts to change human behaviour and will depend on our understanding of REAL human nature. Knowing where we went wrong in the past and what we know now is right, we can engage and design models to promote socially desirable outcomes like reduction in environmental impact and greater sensitivity to the needs of others.

See also: 5 Value Levers for Auto Telematics

Using the fun theory to improve driving behavior is a tested formula that has worked globally and one that I would recommend as a first step. Create a competition that is built off recognition and rewards good behavior. Huge, safe-driving campaigns could be turned into beautiful marketing messages that people would be proud to be a part of. The intelligence and data we collect could change the way we do business altogether.

Liberty Insurance: Drive Well from Michael Hanson on Vimeo.

Delivery

Inventing a future and testing ideas is not enough. To bring auto telematics solution to life, models need to change from actuarial to actuarial plus big data. Implementation will require collaboration between solution providers, underwriters, actuaries and product and marketing teams to create economically viable customer propositions, storytelling and messaging that connects with your audience and keeps their attention long enough to convert.

Scale

Companies like Uber and Lyft struggle with public perception and regulations globally. Partnering with them and creating compelling value propositions for their drivers presents an opportunity for efforts in auto telematics to scale quickly.

Conclusion

The winners will be early movers that capture the safest drivers, take advantage of pricing power and strengthen customer relationships while easing privacy concerns.

Risk Assessment

Value Proposition

Telematics has much to offer both consumers and insurers.

Solution Analysis

Technology solutions available today are similar in terms of what is possible, but there is a difference in the manner that information is collected, delivered and used. When selecting the most appropriate technology solution and provider to partner with, I recommend the following considerations:

1. Telematics Model (PAYD, PHYD, CYD, Embedded): Several telematics models are emerging with varying levels of consumer interaction and integration.

Pay As You Drive (PAYD) is a mileage-based system that has been around for some time in varying forms. A device is installed in the car to validate when and where a car is driven. More advance systems are available now.

Pay How You Drive (PHYD) considers driving style and behavior in addition to collecting mileage and GPS data. The average driver has one accident every 10 to 12 years, but more common are unsafe driving maneuvers that increase the likelihood of an accident. An accelerometer used in the PHYD models can provide event information such as abrupt acceleration, deceleration, hard braking and sharp turning, which help us understand driving behavior and predict accident claims better.

Control Your Driving (CYD) goes to the next level. While PAYD and PHYD models are about collecting data rather than interacting with consumers, therefore passive in nature, CYD uses the data to provide constructive feedback to drivers through mobile or in-vehicle interfaces and potentially improves driving habits. There is sufficient evidence that driving behavior can be improved with feedback. The teen and elderly markets are niches for early adopters of this model.

Vehicles embedded with telematics devices are the long-term aspirations of both automakers and insurers. These systems provide all-around safety and driving assistance. These systems usually include services such as adaptive cruise control, collision warning, lane assistance and blind-spot detection. This model is growing fast in the auto market, driven by the safety benefits of reduced driving risk. New technology can enable additional services and features like safety controls activated when poor road conditions are detected by the GPS. BMW’s connected drive is the first step in this direction. Mobileye is helping autonomous cars "see" via crowdsourcing; the company has outfitted 4,500 NYC Uber and Lyft cars with anti collision technology. Some analysts project that all major manufacturers will have embedded telematics solutions in their cars within the next five years.

See also: Game Changer for Auto Telematics

2. Data Protection (collection, use, disclosure and storage of personal information): Telematics generates big data. Therefore, the ownership, collection, use, disclosure and storage of data becomes crucial in gaining trust and loyalty.

Privacy: The success of other industries indicates that people are willing to trade some of their privacy in return for the right services, in the right time at the right place. That has proved true in social media, Uber, online credit card use and internet banking. When it comes to telematics, though, the stigma of insurance companies and the fear that data about driving behavior could be misused are causing concern. To overcome this hurdle, we must be as transparent as possible up front, offer the right amount of value-added services and carefully position the offering with the right messages to win over consumers. The telematics solution selected must provide a feasible program that gets appropriate access to driving patterns without seeking access to too much data. Aggregated driving scores, limitations on driving history and GPS use and specialized onboard data analysis functions could mitigate these concerns. As long as we know about driver safety and potential risks, we don’t need to dive deep into consumers' personal data.

Storage: Dynamically generating data within an automobile or mobile phone creates challenges. The sheer amount of data generated makes it difficult, if not impossible, to store it within the automobile or mobile phone itself. Thus, decisions about what to store, and where, become very important. This issue is amplified by the privacy concern of data storage. In cases where certain pieces of data are not stored within the automobile or mobile phone, the retention aspect of privacy policies becomes important. Once the data is destroyed, there is no way to recover it. Moreover, unlike static data, which is collected only once by any interested party, dynamic data is collected repeatedly by a service provider to keep it up to date. Thus, there has to be a continuous transfer of dynamic data from many vehicles through the telematics service provider to application service providers. This requires an efficient and scalable evaluation of constraints in the privacy policies.

Security: The growth of e-commerce on the web has been limited by the reluctance of consumers to release personal information. 94% of web users decline to provide personal information to websites at one time or another when asked, and 40% who provide demographic data have gone to the trouble of fabricating it. If potential auto telematics users share the concerns of web users, then a large segment of the potential telematics market, perhaps as much as 50%, may be lost. There is significant potential for misuse of data collected. Consumers may substitute false data or hack into vehicle applications. Telematics service providers may sell consumer data to third parties without the permission of consumers. Therefore, telematics applications will be successful if providers know that the data they receive is accurate and if consumers know that their privacy is assured. Data protection must provide both privacy and security protection. Telematics solutions that can achieve that protection while enabling the sharing of data are the most viable options.

3. Ease of Installation (solution access): Complex installation processes (like blackbox installation) result in lack of interest and conversions from the traditional insurance model to the telematics model. AXA launched a mobile telematics solution in some of its international markets but was unsuccessful in acquiring a buy-in from consumers as the app had to be switched on before a drive. Such a solution leaves room for anti-selection and requires additional effort in the day-to-day lives of consumers. Even insurers like Progressive have only managed to convert approximately 20% of their book of business to the telematics model despite more than a decade of marketing initiatives and spending.

4. Ease of Use (interaction and feedback): The telematics solution selected must be intuitive and easy to use for both consumers and insurers. It should help us identify the risk (item that is insured), peril (anything that could cause damage — breakdown, weather conditions, fire, water, ice, road conditions, accident, etc.) and hazards (anything that increases the chances of peril — speeding, hard braking, driving behavior, etc.). The solution must be able to answer questions such as who is driving, how well the person is driving and how much is the car being driven. Mobile telematics solutions must be able to distinguish driving from walking, riding a bike or hopping on a train, bus or boat, for instance. The right solution will employ real-time data analytics and feedback to engage consumers, improve driving safety and facilitate better claims experience and meaningful dialogue with insurers.

5. Accuracy (trust): Our business is built on trust. It is imperative that the telematics solution we implement helps build trust and value in the digital age. Data accuracy is crucial in acquiring a buy-in from consumers, assessing driving behavior, pricing and speed and quality of response during a breakdown or accident.

6. Notifications (auto alerts): Most fleet telematics solutions have failed to create value as the focus has been largely on collection of information alone. Such solutions require someone to run reports, analyze them and understand them before taking corrective actions. This results in delayed feedback to drivers and in most instances becomes reduced to just knowing where vehicles in a fleet are (dots on a map). Automatic notification and alerts facilitate information to be reviewed at the right time, in the right place and by the right person for improved service (safety, accident and roadside assistance) and quality of care.

7. Ease of support (cloud): Cloud-based telematics solutions facilitate the delivery of new or upgraded capabilities without stretching IT bandwidth and keep the total cost of data ownership low. This is imperative if we wish to own the data. If not, then partnering with a solution provider that can maintain and support the solution at scale in an economically viable manner is crucial.

Customer Engagement

Engaging customers to improve driving behavior calls for a change in human behavior.

Humans are not inspired to act on reason alone. You don't connect with your audience by using conventional rhetoric, which in the business world usually consists of a PowerPoint presentation in which you say "here is our company’s biggest challenge, and here’s what we need to do to prosper," while building your case through statistics, facts and quotes from authorities. The problem with rhetoric is two-fold. First, the people you are talking to have their own set of authorities, statistics and experiences, so, while you are trying to persuade them, they are arguing with you in their heads instead of being motivated to reach certain goals. Second, if you do succeed in persuading them, you’ve only done so at an intellectual level. That’s not good enough. The theory of rational action that claims human beings are abstract symbol manipulators much like computers that seek to maximize their self-interest has dominated most of the 20th century and is the foundation for major institutions, from stock markets to governments. Research in the last couple of years, though, has led to a profound shift in how we understand human thought and behavior.

Scientists have pieced together enough evidence to know that humans are embodied beings, which means we work the way we do because of the kinds of brains we have, the kinds of bodies we have and the typical experiences that pervade our evolutionary history. We know now how real human nature works (mostly). The big picture is that we are profoundly moral beings, and our behavior is shaped by value judgments, deeply held beliefs and assertions about right and wrong. We are profoundly social, and our behavior is influenced by the behavior of those around us through shared stories, common expectations and need for cooperation (and competition). We make decisions through context-based logic determined by how we understand the situations we find ourselves in and reason with our emotions. Try asking someone on a date without those subtle emotional cues of presence, enthusiasm and appeal.

I believe that something as simple as fun can influence human behavior for the better. In a series of experiments, Volkswagen tested this theory. Check it out…

The speed camera lottery

Can we get people to obey the speed limit by making it fun to do so? The winning idea was so good that Volkswagen, together with the Swedish National Society for road safety, actually made this innovative idea a reality in Stockholm.

Piano Stairs

Can we get more people to take the stairs instead of the escalators by making it fun to do so? Piano stairs created on Odenplan underground station in Stockholm have become a hit in cities worldwide from Milan to Santiago and more.

The way to persuading people and ultimately a much more powerful way is by uniting an idea with an emotion. It comes down to good design in our attempts to change human behaviour and will depend on our understanding of REAL human nature. Knowing where we went wrong in the past and what we know now is right, we can engage and design models to promote socially desirable outcomes like reduction in environmental impact and greater sensitivity to the needs of others.

See also: 5 Value Levers for Auto Telematics

Using the fun theory to improve driving behavior is a tested formula that has worked globally and one that I would recommend as a first step. Create a competition that is built off recognition and rewards good behavior. Huge, safe-driving campaigns could be turned into beautiful marketing messages that people would be proud to be a part of. The intelligence and data we collect could change the way we do business altogether.

Liberty Insurance: Drive Well from Michael Hanson on Vimeo.

Delivery

Inventing a future and testing ideas is not enough. To bring auto telematics solution to life, models need to change from actuarial to actuarial plus big data. Implementation will require collaboration between solution providers, underwriters, actuaries and product and marketing teams to create economically viable customer propositions, storytelling and messaging that connects with your audience and keeps their attention long enough to convert.

Scale

Companies like Uber and Lyft struggle with public perception and regulations globally. Partnering with them and creating compelling value propositions for their drivers presents an opportunity for efforts in auto telematics to scale quickly.

Conclusion

The winners will be early movers that capture the safest drivers, take advantage of pricing power and strengthen customer relationships while easing privacy concerns.