#The Affordable Care Act requires every health plan to offer benefits free from most annual and all lifetime dollar limits. If you have a self-insured plan, you may feel the direct impact of this a little more immediately (although many employers still do not recognize it). Even employers that are fully insured should realize they are the insurance company anyway. The only benefit those employers get is delaying the impact of employees' healthcare spending until their next renewal date. But employers pay dearly in the form of a complete lack of information on exactly how that money is being spent. As a result, companies should start to look at the health plan ID card as an unlimited corporate credit card. Which then raises the question: Who is monitoring that spending?

That unlimited credit card rings up charges like a $444 box of Kleenex (described on the hospital bill as a mucus collection device) and $1,000 toothbrushes, and those are the trivial problems, the ones that can draw a chuckle. Those trivial things need to draw attention to a much broader problem, such as $10,000 surgeries that employers blindly pay $180,000 for.

With the majority of the workforce having a high-deductible plan, every day that goes by it's less and less "other people's money" and more of the employee's, so we're starting to see legal activity -- even before a formal declaration from the Department of Labor that health benefits must be managed by employers with the same level of scrutiny as retirement benefits. [For more detail, you can download “ERISA Fiduciary Risk Is the Largest Undisclosed Risk I’ve Seen In My Career” -- a chapter that was added to the recently released new edition of the CEO's Guide book.]

Most employers use networks as their primary strategy to control that spending. Carrier networks love to tout their average discounts. “We save plans 60% on average off billed charges!” Well, there are two major problems with networks.

First, what is that discount off of? Generally it is off the “ChargeMaster” rate. What is the ChargeMaster, you ask? The ChargeMaster, also known as charge description master (CDM), is a comprehensive listing of items billable to a hospital patient or a patient’s health insurance provider, with highly inflated prices -- several times that of actual costs to the hospital.

The ChargeMaster typically serves as the starting point for negotiations with patients and health insurance providers of what amount of money will actually be paid to the hospital. It is described as “the central mechanism of the revenue cycle” of a hospital. We have seen a billed charge of $1,000 from a hospital for a manual toothbrush. 60% off that is still one expensive toothbrush. We found a $444 charge for a “mucous collection device” later found to be a box of tissues. Not to mention, the billed charges vary so dramatically, even within the same facility that a finite percent off an infinite number has zero credibility. While one ex-hospital CEO describes the ChargeMaster as archaic fiction, it does play into the general obfuscation designed to keep healthcare costs growing.

[Please add your comments below if you have other real-world examples like the $1,000 toothbrush, $444 box of tissues, etc. Or share on social media articles and examples with the hashtag #PPOGate, which people are using to highlight how blind faith in PPO networks has inflicted pain on the working and middle class.]

You might think that all hospitals have similar Chargemaster prices. Nothing could be further from the truth. The Huffington Post did a story when treatment costs were first made publicly available from a federal database in 2013, in which they found the cost to treat COPD (chronic obstructive pulmonary disorder) in the New York City area can range from $7,044 to $99,690. Herein lies the fundamental problem: Back when we had richer health plans, patients didn’t care about the cost, as long as insurance covered it. Now that we are being left with these crazy-high deductibles, we are blaming the insurance company for the plan design (and the cost thereof) that leaves us with this exposure.

See also: Medicare Set Asides: 10 Mistakes to Avoid

Every facility that participates in Medicare and Medicaid is required to file their actual cost, all in, with the Centers for Medicare and Medicaid Services (CMS), and anyone can access this data for a subscription fee. In Charlotte, N.C., the two largest hospitals systems file their cost for a CT scan as being between $75 and $90. Their average billed charge to a health plan? Between $1,800 and $2,700! The hospitals claim they have to charge higher prices to private insurance plans because of the below-cost care they provide to Medicare and Medicaid patients and the “free” care they provide to the uninsureds through the emergency room. Well, uninsured ER rates have dropped significantly under the ACA (and actual ER usage has gone up), and ER rooms are highly profitable to the hospitals for those who have insurance, so shouldn’t there be a positive overall impact on the private insurance pricing? Also, if I go a buy a car, and get a super deal from the dealership, will you be OK being the next customer in the door and being told you have to overpay because the dealer gave some stranger before you a really good price? I think not.

The second problem with PPO networks is that nearly every network contract prohibits the plan (and the employer, by extension) from auditing a bill. The contract actually prohibits the plan from even requesting an itemized bill! All they can get is what’s called a UB, or a universal bill. You can see the form here. Other than the information on who the patient is and whom to pay, the UB only shows total charges and diagnosis. As long as the diagnosis is a covered condition under the plan, the discount gets applied, and the bill gets paid. Bills on this form can easily be hundreds of thousands of dollars. When we have asked for an itemized bill (that the insurance company can’t ask for), we have found pregnancy tests on men and charges for 16 surgical screws when only four were used, just to name a few “errors.”

We have heard firsthand stories where an insurance executive sat down with hospital executives and said, “We need a bigger discount from you guys,” and the execs said no way. So the insurance exec said, “I don’t think you understand…you can bill us more, and it can even net out to more than we pay you now, we just need to say we have a bigger percent off.”

Another perverse incentive to be aware of that came as a result of the ACA is called the medical loss ratio. Under this provision, insurance companies must spend between 80% and 85% of the premiums they receive for medical care for the insureds. If they spend less than that, they must provide a refund. Prior to this law, carriers could keep the difference for profit, so they had stronger encouragement to keep costs down. Now, the only way they can charge their customers more, and thereby boost profits, is if the underlying cost of care also goes up.

We're not blaming the insurance companies. They had to bow to the pressure of their customers (employers) because, if that big local hospital system left their network, they thought customers would leave in droves. (Pittsburgh schools are proving that assumption wrong with a good plan design and collaboration with their teacher union -- details are in the CEO's Guide book that you can download free.) The insurance companies are in a tough spot. If they try to “manage” the care -- i.e. pre-certification, tiered drug formularies and narrow networks -- their customer base gets ornery. And employers are loath to be seen as getting involved in their employees’ healthcare.

I bet most employers don’t want to tell employees where to sleep or what car to drive, either, but I imagine they nonetheless have parameters around how much can be spent for rental cars and hotels when traveling on the company dime.

Fortunately, there are employers all over the country that have wised up and tamed the out-of-control healthcare cost beast. They are spending 20% to 55% less than a typical employer on a per capita basis. Paradoxically, they are finding the best way to slash healthcare costs is to improve health benefits. There are several examples in the CEO's Guide book that range from school districts in the Rust Belt to a municipality in the Midwest to a small manufacturer in the heart of oil country to a hotelier in Florida.

Another statistic carriers love to tout is their auto-adjudication rates (in other words, automatic and prompt payment of claims as they come in). After all, higher auto-adjudication means the providers get paid quicker. And that means fewer headaches for providers and employees. But that also suggests that a 94% auto-adjudication rate means that 94% of the time no one is looking at the bill even to the limited level the contract permits. The same company will reject an expense report submitted by an employee missing a $62 restaurant receipt and then blindly pay a $100,000 medical bill without any detailed review.

So let’s review:

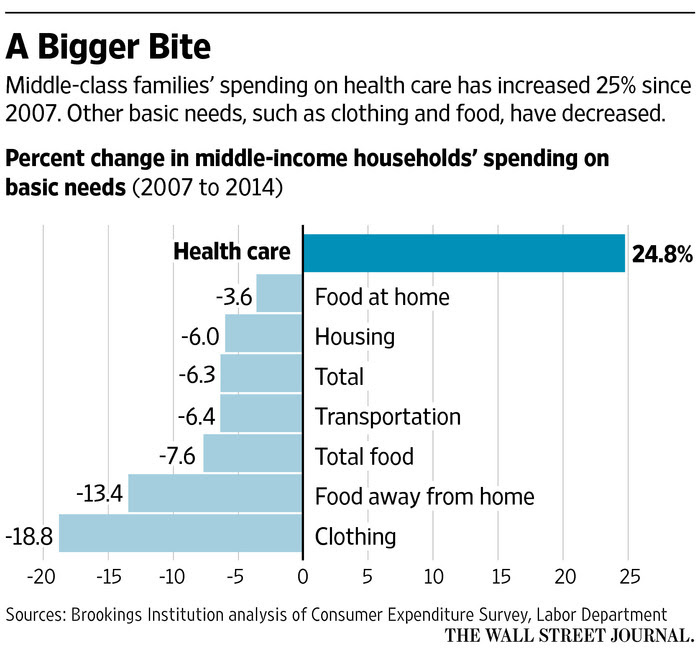

Under ERISA, plan sponsors (the employer) have a fiduciary responsibility to protect plan assets. Because many network contracts prohibit the plan from auditing the bill, and the few that do require 100% of the allowed charges to be paid before an audit can begin, how can a plan sponsor meet its fiduciary requirement under ERISA to be good stewards of plan assets? Old-line benefits brokers continue to advise their clients to sign such egregiously one-sided contracts -- those benefits consultants are going the way of the dodo bird but leave their clients exposed in the meantime. I can say with 100% certainty that plaintiffs' attorneys are gathering their ammunition for these ERISA cases. When you combine the fact that healthcare's hyperinflation has been the overwhelming driver of 20-plus years of wage stagnation and decline and look at the impact on household spending in the graph, the pain inflicted on the working and middle class is palpable.

Smart employers and their benefits consultants are avoiding having a target on their back by taking action now. By applying the best practices captured in the Health Rosetta and various other tools that will be highlighted in the forthcoming book CEO's Guide to Restoring the American Dream - How to deliver world class healthcare to your employees at half the cost, there are many tools to provide employees a world-class health benefits package without giving a blank check to the healthcare industry.

Written with David Contorno, President, Lake Norman Benefits

Under ERISA, plan sponsors (the employer) have a fiduciary responsibility to protect plan assets. Because many network contracts prohibit the plan from auditing the bill, and the few that do require 100% of the allowed charges to be paid before an audit can begin, how can a plan sponsor meet its fiduciary requirement under ERISA to be good stewards of plan assets? Old-line benefits brokers continue to advise their clients to sign such egregiously one-sided contracts -- those benefits consultants are going the way of the dodo bird but leave their clients exposed in the meantime. I can say with 100% certainty that plaintiffs' attorneys are gathering their ammunition for these ERISA cases. When you combine the fact that healthcare's hyperinflation has been the overwhelming driver of 20-plus years of wage stagnation and decline and look at the impact on household spending in the graph, the pain inflicted on the working and middle class is palpable.

Smart employers and their benefits consultants are avoiding having a target on their back by taking action now. By applying the best practices captured in the Health Rosetta and various other tools that will be highlighted in the forthcoming book CEO's Guide to Restoring the American Dream - How to deliver world class healthcare to your employees at half the cost, there are many tools to provide employees a world-class health benefits package without giving a blank check to the healthcare industry.

Written with David Contorno, President, Lake Norman Benefits

- Although carrier networks have some influence over the discount, they have little over the starting price.

- Hospital charges are filed on a UB (universal bill), and the plans are contractually prohibited from asking for an itemized bill.

- If the plan requests any audit at all, they are required to pre-pay the claim, often at 100%, and are then subject to the hospital’s own audit procedures.

- Networks are forced to accept these terms, or their customers will leave because they do not have a broad network.

Under ERISA, plan sponsors (the employer) have a fiduciary responsibility to protect plan assets. Because many network contracts prohibit the plan from auditing the bill, and the few that do require 100% of the allowed charges to be paid before an audit can begin, how can a plan sponsor meet its fiduciary requirement under ERISA to be good stewards of plan assets? Old-line benefits brokers continue to advise their clients to sign such egregiously one-sided contracts -- those benefits consultants are going the way of the dodo bird but leave their clients exposed in the meantime. I can say with 100% certainty that plaintiffs' attorneys are gathering their ammunition for these ERISA cases. When you combine the fact that healthcare's hyperinflation has been the overwhelming driver of 20-plus years of wage stagnation and decline and look at the impact on household spending in the graph, the pain inflicted on the working and middle class is palpable.

Smart employers and their benefits consultants are avoiding having a target on their back by taking action now. By applying the best practices captured in the Health Rosetta and various other tools that will be highlighted in the forthcoming book CEO's Guide to Restoring the American Dream - How to deliver world class healthcare to your employees at half the cost, there are many tools to provide employees a world-class health benefits package without giving a blank check to the healthcare industry.

Written with David Contorno, President, Lake Norman Benefits