The use of accelerated underwriting processes has come a long way in the last five years. Although it was an innovative idea not long ago, most insurers now engage in accelerated underwriting to some degree and are increasingly looking for novel ways to remove inconvenience, delay and cost from the new business process.

However, as impressive as its uptake has been, the industry has yet to begin tapping the true – and transformative – potential of accelerated underwriting. This is because most of the time it has lacked the automation component. Automation has the potential to benefit insurers across their entire business, but this is especially true of accelerated underwriting, which at its heart is about streamlining and speeding policy issuance for simpler, lower-risk cases.

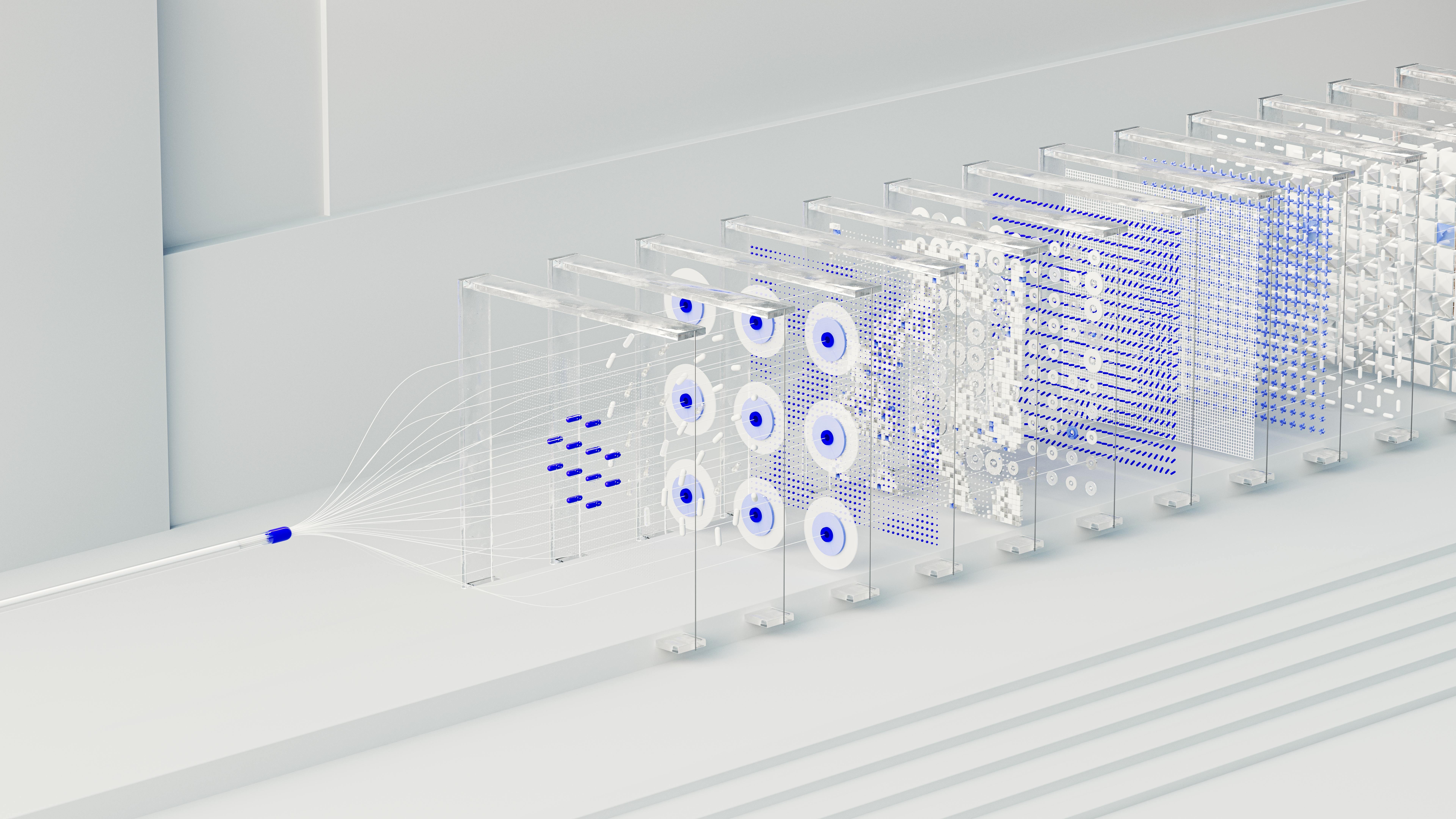

It’s here that automation can really shine. Take for instance a case where an accelerated underwriting process removes the need for an in-person examination. Without automation, that review by an underwriter will still take 24-48 hours to be completed, even though the relevant information is instantly available in seconds. With automation, the entire application and underwriting process can be reduced to a matter of minutes.

This is precisely what new technology platforms are enabling. Advances in AI and machine-learning have come to the point whereby technology can consistently and efficiently underwrite a large proportion of cases. Technology can respond intelligently to input, in real-time, determining what additional information is needed, and then make an underwriting decision and issue insurance coverage. What’s more, when appropriately linked with and integrated into the rest of the business, it can feed information back for better risk modelling in the future.

See also: 3 Ways to Optimize Predictive Analytics

When you add in a layer of predictive analytics to the automation, things start to get really interesting. Predictive analytics can add value to the risk selection process and our understanding of the risk in a number of ways. The first, mentioned above, is a ‘bottom-up’ benefit – i.e. cases where the analytics engine can spot relationships in the underlying data that are then brought to the attention of underwriters, who can then investigate whether and how that pattern relates to real-world factors.

Another way predictive analytics can add value runs in the other direction - top-down. It means business managers and underwriters have access to a vast pool of analyzable data that they can use to help answer questions and test hypotheses or ideas. Having this ability can remove a lot of unnecessary trial-and-error, and can give all levels of the business a better view of information that is vital to long-term success.

A third and very significant value-add from predictive analytics is that it can help with the systemic stratification of ‘grey areas’ within the underwriting process– that is, the cases in the middle that aren’t either extremely healthy, or obviously high-risk. Segmenting this grey area and formulating better approaches to these cases is crucial for any insurer looking to reduce “RTUs” (Refer to Underwriter) and gain a market edge, and a sophisticated analytics engine can make the process a lot more efficient and smarter.

It is these elements – automation combined with predictive analytics – that could turn accelerated underwriting from a useful cost and time saver into something that could truly revolutionize the insurance business model as a whole. So far, insurers have predominantly used accelerated underwriting to target the same customers they’ve historically targeted. What automated underwriting and predictive analytics can unlock is the ability to actually grow the pie – to target new or previously untapped markets, and create a wider variety of more specialized products focused on particular customer niches. The time and cost savings associated with using this technology could enable different business models for distribution and make it more attractive to target markets that were previously viewed as uneconomical. This process is particularly well-suited to digital distribution, and to making headway into the underserved middle market.

Connected to this – and under-utilized at present – is the way in which automated systems are able to integrate new data sets quickly and holistically. Data has always been, in one way or another, the lifeblood of insurance. But in the modern digital age with its corresponding explosion in the amount of data available, a lot of potentially relevant data sets go untapped by the industry. The ability to access this data and integrate it into risk selection processes will be a big determiner of success for insurers in the near future – those that don’t succeed could get left behind.

Of course, opportunity and challenge are two sides of the same coin. The addition of automation and analytics to accelerated underwriting holds tremendous potential, but also poses a big challenge. Insurance isn’t renowned for being a particularly tech-savvy industry. Yet, to make full use of these new capabilities, firms are going to have to embrace technology and data science.

Most companies will need to work with partners to help the transition. Not just a software vendor to access the technology itself, but there will be a need to find the necessary expertise in both the technology and the insurance sector as whole in order to facilitate a business process revamp. Collaboration will be key in supporting the integration effort needed to fully realize new technology’s potential within a business. But automation does not mean a total overhaul of existing business structures and processes – because this too is likely to incur more risk than opportunity. Firms should take a modular and flexible approach, using systems that can sit within a variety of existing infrastructures with minimal disruption.

See also: How Underwriting Is Being Transformed

The shift to automation and analytics is coming fast. And when it does, the implications for insurance business models – what’s possible and what’s not – could be just as profound as e-commerce was for the retail sector. For those that get ahead, the rewards could be just as great.

Power of Accelerated Underwriting

The industry has yet to tap the true potential of accelerated underwriting because the automation component has been missing.