We are living in a hyperconnected world, and the presence of IoT devices has already been more pervasive than many of us have realized. Mobile phones in our pockets are full of sensors. Their software is updated over the air. And, when we lose them, we can remotely track their position. Meanwhile, restaurants are using simple QR-codes to comply with COVID safety measures, warehouses are employing robots to automate certain manual activities, etc. The spread of the IOT continues.

Although IoT has not yet been systematically addressed by the large majority of insurers, several early adopters have already concretely demonstrated the potential of using this technology. I have had the privilege to directly support many of these players through the activity of the IoT Insurance Observatory, an insurance think tank that has aggregated almost 60 insurers, reinsurers and tech players between North America and Europe.

Today, there are international insurance companies with millions of policies priced with telematics in their auto portfolios, millions of customers using an IoT-enabled wellbeing reward systems in their life insurance portfolios and thousands of workers protected with real-time risk mitigation solutions in their workers’ compensation portfolios. The level of maturity is higher on insurance personal lines; however, a new wave of IoT-based initiatives is occurring in commercial lines.

These successful player journeys show IoT’s extraordinary potential to generate value for insurers, policyholders and even the entire society. Indeed, IoT allows an insurer to connect with its clients and their risks, providing benefits on four axes:

- Improving customer experience by enhancing proximity and frequency of interaction with them, therefore moving beyond the traditional risk transfer. Many players are selling additional services for a monthly fee; others have found new ways to sell insurance coverages thanks to IoT;

- Enhancing core insurance activities (assessing, managing and transferring risks) by using IoT solutions for continuous underwriting, claims management and risk reduction. Using the insight generated by the analysis of the flow of IoT data has promoted less risky behaviors in real time;

- Generating knowledge about policyholders and their risks, to insure them in a different way, to enable up- and cross-selling and to insure new risks;

- Providing positive externalities to society.

Unfortunately, many players in different markets have not understood the strategic nature of this innovation. They have considered IoT adoption as an IT project or the creation of a product. Instead, best practices show that IoT adoption is a strategic choice that requires a multi-year commitment to develop needed, specialized IoT competencies and leadership competencies.

Each of the successful pioneers has designed its vision and strategy for IoT usage within its business processes.

A common mistake is to focus on the “thing,” such as a smart device. However, IoT is about data, not things. Even a focus on data is a mistake. What really matters is the usage of the data. The transformation of the business processes – through data usage – has been the secret sauce of any successful IoT insurance program.

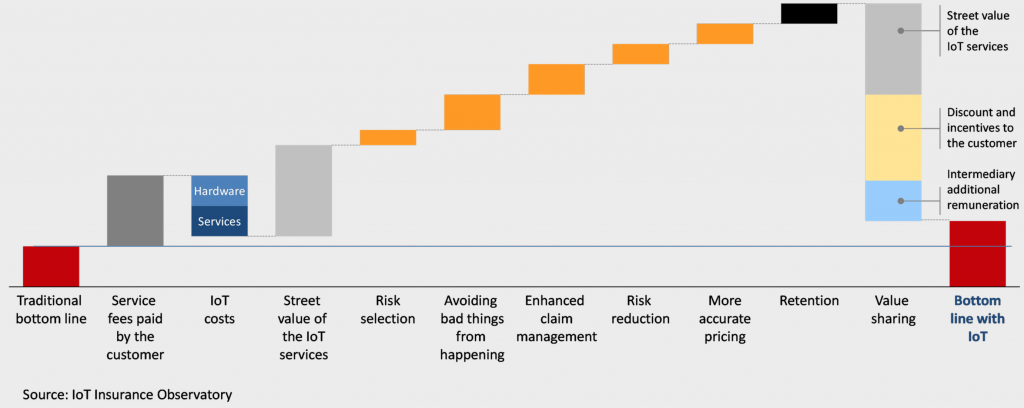

Some international success stories – from auto telematics to property insurance for smart commercial buildings – have already shown robust ROI. However, there is not much low-hanging fruit where a single use case generates enough value to cover all the emerging IoT costs. Typically, IoT insurance programs need deep functional competencies and a multi-functional approach to have multiple use cases that contribute to the return on the technology investment.

The opportunities for using IoT data in the insurance sector are summarized by the following framework, which has been developed within the IoT Insurance Observatory over the last five years.

See also: 4 Connectivity Trends to Watch in 2021

Each of these use cases has been successfully implemented by tens of pioneers in different international markets and in different insurance business lines.

These use cases don’t change the nature of the insurance business, but they allow insurers to do their job better. However, this paradigm requires moving beyond the traditional insurance economics (premiums, claim costs, administrative costs) integrating service fees, partners contributions, benefits generated by the usage of IoT data, IoT costs and value-sharing with policyholders (cashback, discounts, etc.).

Insurance IoT is a new way of thinking about the activity of assessing, managing and transferring risks that fits with a world that is going to be more and more hyperconnected, a trend that insurers can neither stop or ignore.

This article was originally published by Technology Magazine - IoT Edition