Most of us have heard the phrase: "Culture eats strategy for breakfast." It could be restated as, "Your actions speak louder than your words." This means that management can dream up any strategy they want, but their behaviors and actions are what create the culture of an organization.

Culture drives how efficient an organization's processes are. Culture drives the success or failure of an organization. Culture is the product of leadership decisions or the lack of decisions.

The best-articulated corporate vision and strategy are of no value if they cannot engage the hearts, minds and work habits of employees at all levels and convey a purpose beyond just profit.

A vision states where an organization wants to go; a strategy defines the path to get there; and the work culture describes how business processes are actually executed along the path toward the vision. The health of a work culture can range from a contagiously high-performance work culture to mediocre or all the way down to a disruptive, confrontational culture that can't get much done on time or done right the first time. A disruptive culture can trump the best vision and strategies every time. On the other hand, if a work culture is nurtured and groomed to align with a carefully crafted vision and strategy, the positive momentum could be unstoppable.

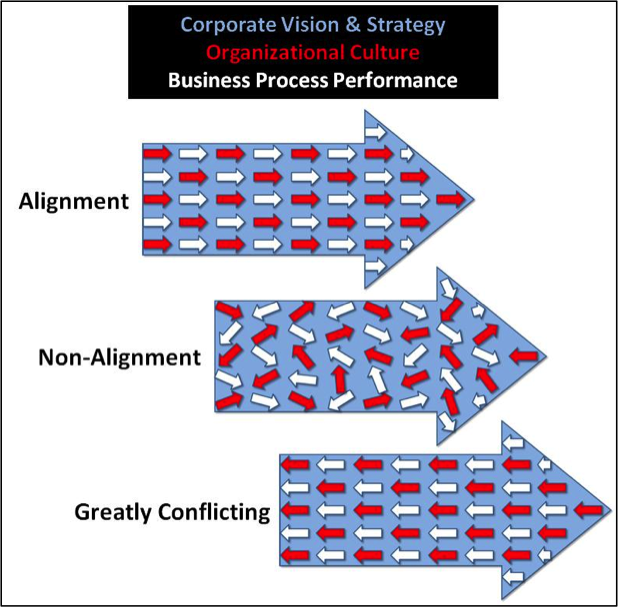

Figure 1 shows possible scenarios of vision, strategy, culture and performance alignment and misalignment. Business process performance (small white arrows) is more correlated with the work culture (small red arrows) than with the vision or strategy (big blue arrow) of an organization. Work culture -- not vision or strategy -- culture drives business performance. The challenge presented by this dilemma is that the work culture is an invisible force that is hard to measure. It shows its good side when you watch it and only displays its bad sides when you look away. The work culture is the product of complex cascade effects inside an organization and is as much affected by leadership actions as it is by the lack of appropriate actions. If left unattended, it will create its own random world of hidden agendas, which will probably not be aligned with the priorities of the organization.

Figure 1 - 3 Possible scenarios of vision, strategy, culture and performance alignment

Figure 1 - 3 Possible scenarios of vision, strategy, culture and performance alignment

Corporate visions and strategies are usually rolled out in formal three- to five-year plans. Work culture management and monitoring is too often not in sync with that plan and referred as an “HR thing," even though it is the gate-keeper of business performance. If you do not understand and actively manage the work culture, it will manage you.

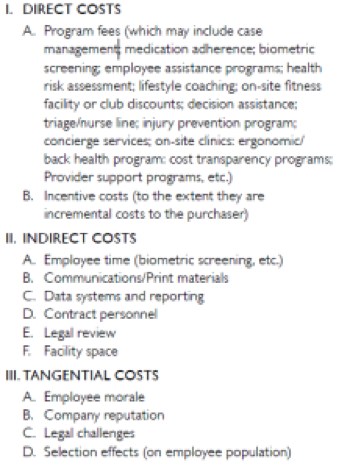

Measuring Cascade Effects Risks

It would be wonderful if we could just plug a measurement device into an organization to check its health and the risks of cascade effects (Figure 2). The work culture defines how employees work with each other through communication, coordination and cooperation. It generates multiple slow-motion and rapid chain reactions, ripple effects and cascade effects that greatly affect the mood and attitude of the organization. It predestines an organization for success or failure.

Figure 2 - The challenge of measuring work culture health and risks

Figure 2 - The challenge of measuring work culture health and risks

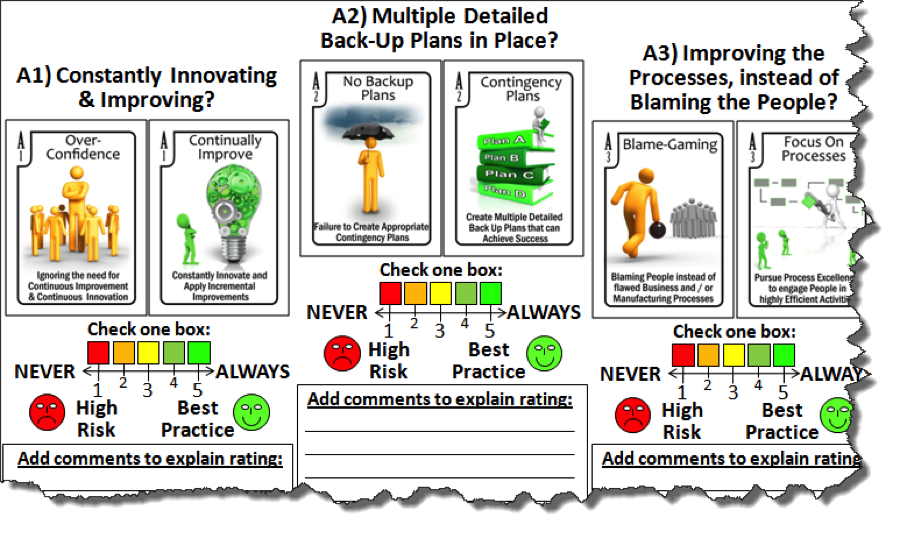

How can we measure the health of invisible cultural chain reactions that can drive the success, mediocrity or failure of an entire corporation? I suggest a series of management and employee surveys and brainstorming assessments to test for the presence of 56 different elements of risk that can be present at any level in an organization. (See Figure 3 for a partial view of the survey.) The culture assessment tool shown in Figure 3 should be used for at least three different levels of management in an organization. These three levels of perception will offer triangulation data points, which will show how common or diverse the perceptions are that describe the organizational culture.

Figure 3 - Partial view of a gamified organizational health survey

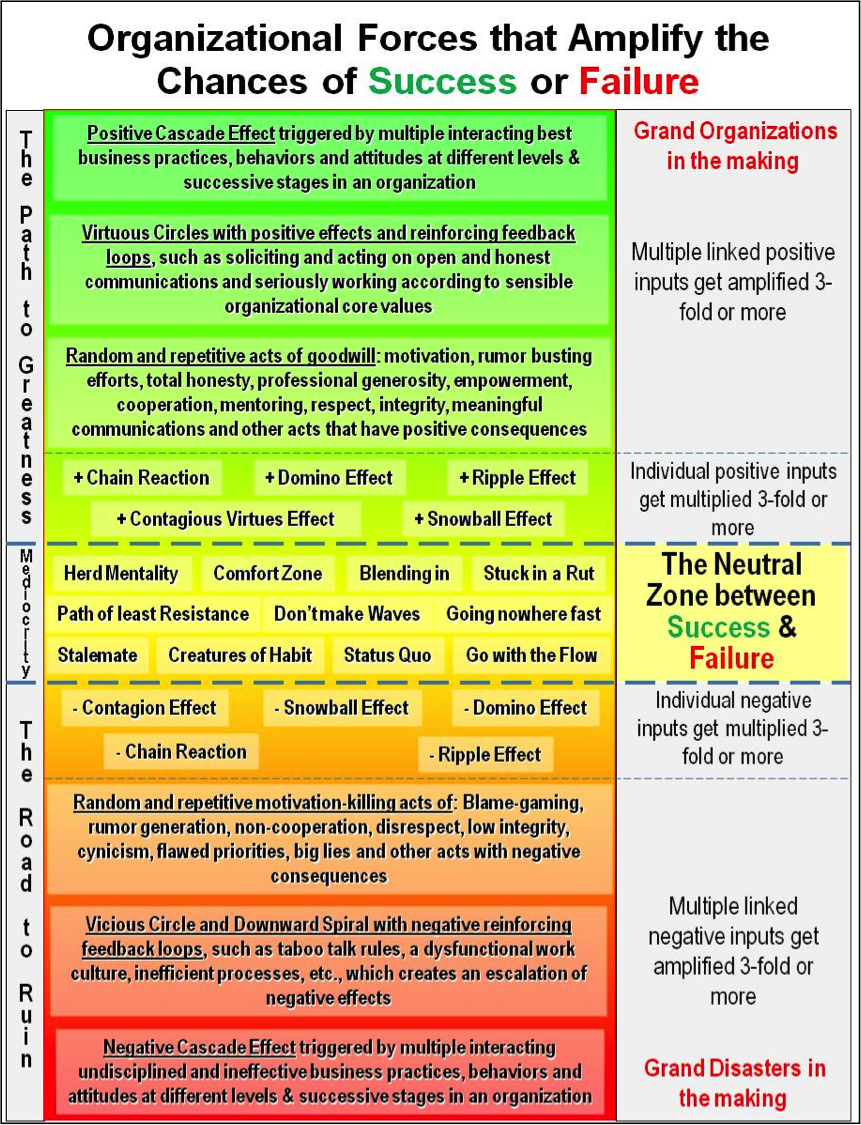

The Organizational Force-Fields That Drive Success or Failure

Chain reactions, domino effects, ripple effects and snowball effects are similar in that they are defined by the single acts that created them. Once triggered, they will play out their effects depending on the amount of resistance the system presents against them. Cascade effects are different. They are fueled by a hierarchy of multiple interacting triggers at different levels in the system. Time delays between cause and effect are common, making the direct correlations between cause and effect more difficult to identify. Each element of the cascade effect can create dramatic outputs involving as many as three degrees of separation, rippling through an organization. There are three types of organizational cascade effects:

- Destructive tsunamis of non-cooperation and negativity

- Expanding groups of status quo herd followers

- Constructive waves of cooperation, empowerment, motivation and positivity

If all of the cascade effects are present in an organization at the same time, the result will be conflict, employee frustration and lack of momentum in the right direction. A random mix containing equal parts of motivated, frustrated, positive and cynical employees co-located for 40 hours a week is not a formula for success; it is a recipe for mediocrity or even disaster.

Positive Organizational Cascades

These are acts of positivity that multiply and can also spread from person to person. In 2010, researchers from the University of California, San Diego and Harvard published the results from their experiments in an article titled: "Cooperative behavior cascades in human social networks." They showed that cooperative behavior can be just as contagious as bad behavior. They showed that positivity can spread from person to person to person by displaying random acts of cooperation, generosity and other positive behaviors. This creates a cascade of cooperation that influences dozens of people who were not involved in the initial trigger event.

Mediocrity and Consensus Cascades

These cascades are the result of contagious personal decisions to blend in with the crowd and not make any waves (also known as "group think"). Many researchers, including those from the computer science department at Carnegie Mellon University, have confirmed this phenomenon. Forces in organizations and society like peer pressure, blending in, the herd mentality and the band-wagon effect can cause an individual to follow the herd, even if that violates personal preferences and value systems of what is right and what is wrong. This is often done to save one’s reputation in a group and gain acceptance. Efforts to achieve team consensus can create the same phenomena, resulting in conclusions that might not always be the best ones. Teams can assign a "devil's advocate" role to a participant to deliberately challenge "herd decisions" to counter this cascade effect.

In 2013, Forbes wrote an article titled: "Brainstorming is Dead…," which summarized recent criticism by many about how creative people can get suppressed by other personalities during brainstorming events when the main priority is to get consensus on all brainstorming conclusions. Forcing consensus is as useful as it is dangerous. To avoid ineffective and dangerous group-think cascade effects, group decisions should build on each other's ideas, when possible, to create innovative hybrid solutions and not pick one idea and totally discount another idea that might have a flicker of genius.

Negative Organizational Cascades

These are acts of negativity that multiply and spread from person to person in an organization. Risky, combative and uncooperative behaviors all have the unfortunate ability to multiply and spread to three degrees of separation from the original act. This can have a negative impact on dozens and even hundreds of downstream people not involved in the initial negative triggering acts. Negative human interactions can break the bonds of humanity and teamwork. These cascades can destroy the work culture, effectiveness and performance of an entire organization.

The Broad Influence of Cascades

Behavioral researchers have demonstrated with team experiments that positive, mediocrity and negative cascades can all have affect three degrees of separation (friends of friends of friends). Other researchers and computer models have determined that only three to four degrees of separation is what separates everyone in the USA, and only six degrees of separation separate everyone in the world. Exceptions to this rule are the secluded tribes in the Amazon jungle and other remote places. Yes, the world is smaller than we think, and actions really do speak much louder than words. Actions and behaviors can reach beyond the horizon and into different time zones.

The Organizational Forces Survey

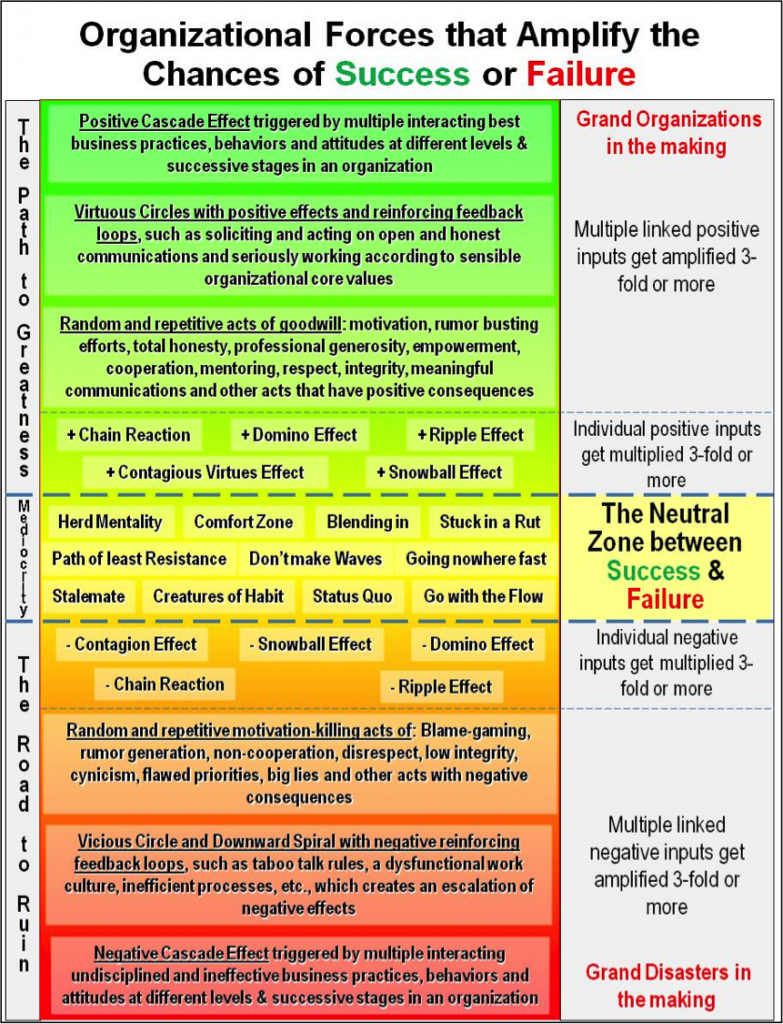

The Organizational Forces Survey tests the health of the individual organizational forces that drive chain reactions, cascades and other behavior propagation phenomena. This survey asks participants to assess the presence of positive and negative organizational forces shown in Figure 4 by identifying the forces they believe to be present. This survey is given to all levels of employees and management.

Figure 4 - The Organizational Forces Survey used to assess the health of the work culture.

Figure 4 - The Organizational Forces Survey used to assess the health of the work culture.

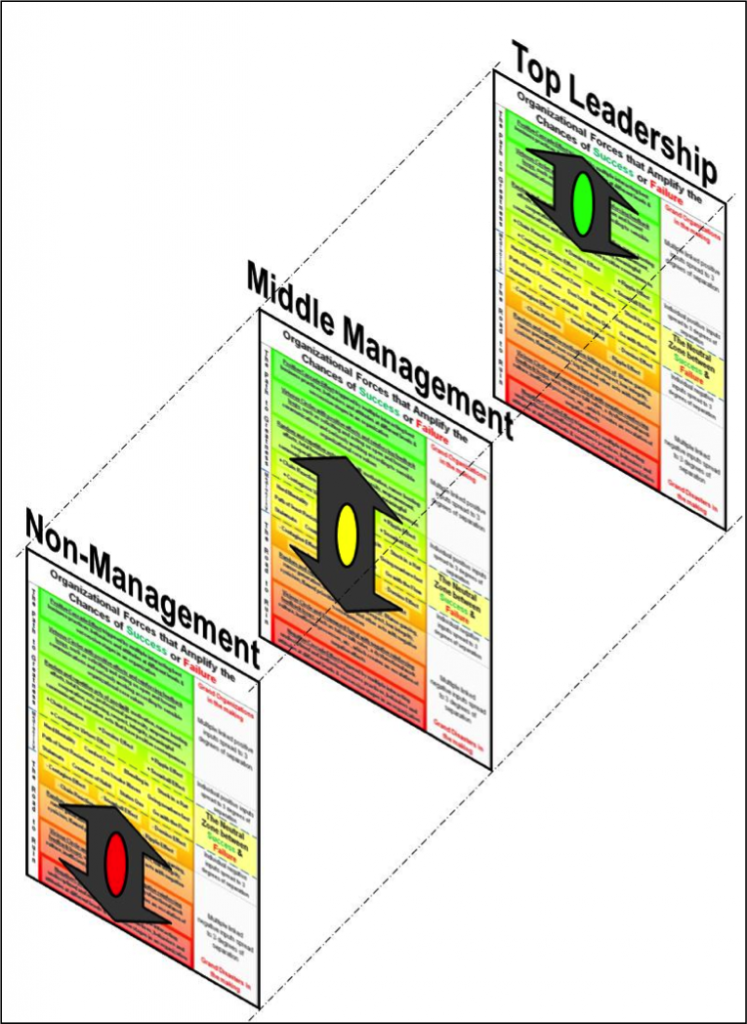

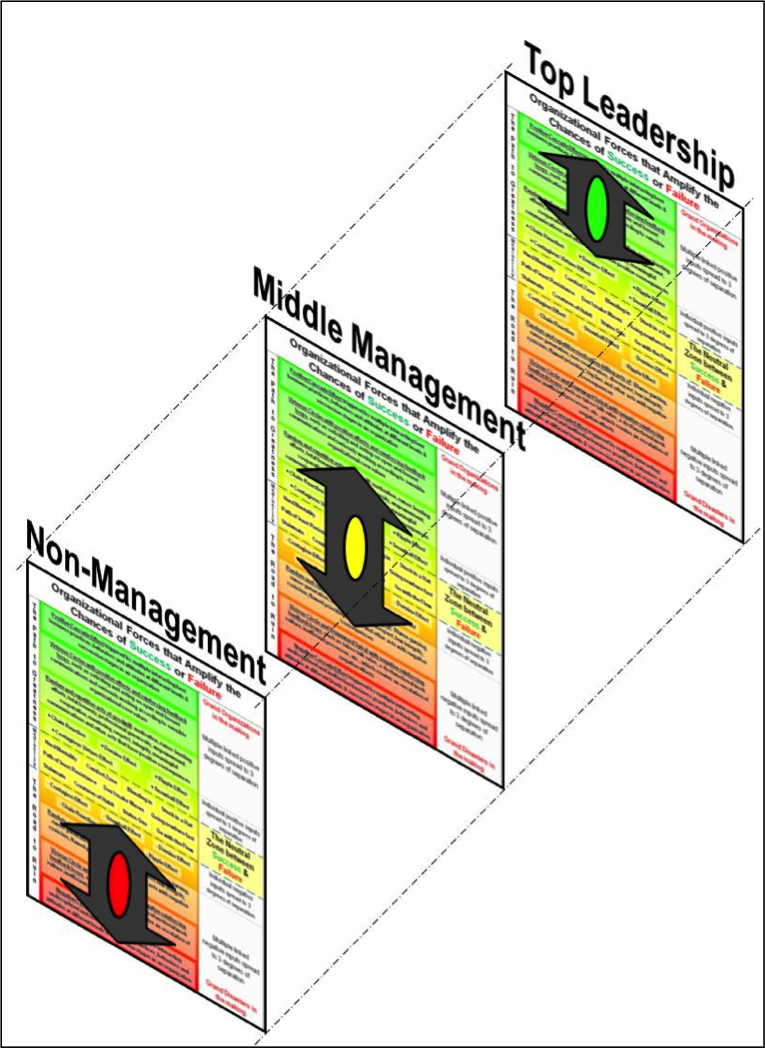

Figure 5 shows an example of survey responses, using the form in Figure 4, that were attained from the survey for three different levels in an organization: top leadership, middle management and non-management. One sign of healthy communications between management and employees is when organizational risk assessments are similar between different levels in the organization. However, that is not the case here.

In this survey response example, top leadership rated the health of the work culture as overwhelmingly positive (green). They perceived their environment to be a Grand Organization in the making. Unfortunately, non-management employee responses to this survey were at the opposite end of the scale (red). They rated the forces in the organization as overwhelmingly negative, filled with high risk and knocking on the door of a Grand Disaster. Middle management rated the work culture as mediocre (yellow), with some responses slightly positive and others slightly negative. This group of employees was apparently influenced by perceptions of top leadership and non-management.

Figure 5 - The range of survey responses from various levels in this organization shows major discrepancies in their perception of the health for the organizational work culture.

Figure 5 - The range of survey responses from various levels in this organization shows major discrepancies in their perception of the health for the organizational work culture.

Conclusion

Grand investigations are often done after a loss of life disaster occurs, such as a NASA space shuttle disaster, a passenger airplane crash or an accidental employee death on the job. However, it is hard to find this level of effort and analysis applied to prevent such disasters. Deep and thorough disaster investigations often find flawed undisciplined leadership practices and organizational cultures at the root of the problems. It is also common to discover a zealous ambition to grow the business without really ensuring that a healthy work culture foundation is put in place to safely support such expansion.

Huge opportunities for organizational productivity improvements still exist today by cultivating a high-performance work culture. Breakthroughs can be made when organizations appreciate the fact that “culture eats strategy for breakfast,” a phrase coined by Peter Drucker, a famous management consultant, educator and author. True organizational greatness can be achieved when organizations look beyond trying to just manage the bottom line and learn how to manage, analyze and monitor the cultural forces and cascade effects that drive success or failure.

A grand vision and strategy can only revolutionize a company when the work culture is healthy, engaged and aligned with those concepts. Taboos on talk must be broken. Open, frequent and candid communications must exist between all levels in the organization. Employee issues and concerns must be addressed in a timely manner as proof that a functioning communication and countermeasure system are in place. Only then can an organization really have a chance to break its barriers to greatness.

{kind=link}