Welcome to this special edition that will look at some simple solutions to the myriad of issues facing health insurance, Medicare, Medicaid and long-term care insurance, as well as the high cost of health expenses in retirement. Please note that the concepts that follow do simplify very detailed areas and as such are not complete solutions; rather, this article is to point out some ideas to consider that take what currently exists and improve upon it.

With full repeal of the Affordable Care Act less likely, the big question is the extent of the "repairs" that will happen. Quite a change from earlier in the year. It may be that more people have realized that the Affordable Care Act IS Obamacare and that they have insurance through Obamacare (a nickname for the ACA).

It is clear that there are so many moving parts to how the question of paying a medical (or related) bill is broken down by a wide variety of insurance programs. Finding a solution is challenging because there is a conflict between costs, access to care and quality of care. It is not possible to have it all; trade-offs do need to be made.

The Insurance Bill of Rights provides guidance on setting up a successful road map covering areas of disclosure, clarity and removing complexity. And, in a time of incredible advances, technology can and should be part of the solution.

Complex issues have to be addressed on a step-by-step basis, so let’s start with the desired outcomes, then look at where we are, the simplest solution and what will make this plan work.

To make this happen is going to require compromises, common sense and dealing with reality. There is no perfect plan, but it is entirely feasible to have a plan that addresses the above criteria for almost every American in ways that will not cost significant amounts of money.

What is the current health insurance breakdown?

The Affordable Care Act is an incredible achievement, but it still leaves consumers with a complex mix of health insurance plans including: individual health insurance, small business health options program (SHOP), employer/group health insurance, Medicare, Medicaid, CHIP, VA insurance and other smaller plans.

Any person can obtain health insurance regardless of pre-existing medical conditions. The nonpartisan Kaiser Family Foundation estimates that 27% of adults under age 65 have health conditions that would likely leave them uninsurable under practices that existed before the healthcare overhaul.

The most recent

Health Insurance breakdown by U.S. total population in 2015 was by: employer, 49%; non-group, 7%; Medicaid, 20%; Medicare, 14%; other public, 2%; uninsured, 9%. Sources: Kaiser Family Foundation estimates based on the Census Bureau's March 2014, March 2015 and March 2016 Current Population Survey (CPS: Annual Social and Economic Supplements).

What is required to make this or any other health insurance solution work?

The basic principles of risk management must be applied: In Warren Buffett’s annual letter, he summarized: "At bottom, a sound insurance operation needs to adhere to four disciplines. It must (a) understand all exposures that might cause a policy to incur losses; (b) conservatively assess the likelihood of any exposure actually causing a loss and the probable cost if it does; (c) set a premium that, on average, will deliver a profit after both prospective loss costs and operating expenses are covered; and (d) be willing to walk away if the appropriate premium can’t be obtained."

What is the simplest solution?

We must start with a baseline of easy-to-understand, cohesive and coherent health insurance for all Americans. Then the next step is simplifying and standardizing all of the different types of health insurance out there. This means eliminating all of the varied programs and plans that are redundant both in terms of coverage and oversight while making the rules simple.

If this sounds like Medicare, then we’ve come to the same conclusion. Medicare expansion is the best outcome, as it takes the largest existing U.S. health insurance program and updates it for expanded capacity and today’s reality.

What follows are factors that would affect how this could be done. Why reinvent the wheel. Yes, Medicare is not perfect, but it gets the job done and has a long history.

See also: Key Misconceptions on Health Insurance

Everyone moves to Medicare sooner or later

At some point, all Americans have to move to Medicare from whatever plan they currently have. There are rules about when Medicare has to be applied for that can have a permanent impact on Medicare premiums. Depending on the current health insurance plan, many Americans have to choose new physicians and learn how to use their Medicare plan.

And we already have a plan used by 44 million Americans (15% of the population). Enrollment is expected to rise to 79 million by 2030. And currently only one in 10 beneficiaries rely solely on the Medicare program for healthcare coverage. This shows that there is still an important role for insurance companies and that Medicare is a base rather than a complete solution. Here’s how it could work:

- Medicare Part A Expansion for everyone at no cost. Medicare Part A is free for most Americans already. This would include basic emergency health care services (hospitalization) at no cost to cover all. This includes: hospital care, skilled nursing facility care, nursing home care, hospice and home health services. Medicare Part A is free. Emergency healthcare for all has existed in the U.S. for more than 20 years, through the Emergency Medical Treatment and Labor Act of 1995. Under this act, all hospitals are required to treat individuals in need of emergency care regardless of their insurance. If someone is uninsured, they will go to a hospital, and the hospital will treat them. So, very basic healthcare is already provided to all. What is not provided to all is the means to pay for the healthcare. Research finds that each additional uninsured person costs local hospitals $900 per year. Hospitals are therefore acting as "insurers' of last resort. Hospitals do receive some compensation through Disproportionate Share Hospital (DSH) payments, which are owed under federal law, to any qualified hospital that serves a large number of Medicaid and uninsured patients. However, these payments are not enough to cover hospital costs. It is estimated that hospitals absorb about 2/3 of the cost for this uncompensated care. Therefore, because this minimum level of care is mandated by federal law, then this minimum level of care should be included under a baseline expanded Medicare plan. The care is already being provided, but it's not fully funded.

- Medicare Part B revision: Match the benefits offered by Medicare Part B preventative (outpatient services) with the essential benefits offered by Medicare Part B. This solves the issue of areas where there are minimal or no choices of insurance for consumers. If insurance companies withdraw, consumers could purchase Part B from Medicare to cover essential benefits. Most of Medicare’s preventive services are available to all Part B beneficiaries for free, with no co-pays or deductibles, as long as you meet basic eligibility standards. These are services not covered by Part A: Mammograms; colonoscopies; shots against flu, pneumonia, and hepatitis B; screenings for diabetes, depression, and heart conditions; and counseling to combat obesity, alcohol abuse and smoking are just some of Medicare’s lengthy list of covered services. (to get these services for free, you need to go to a doctor who accepts Medicare “on assignment,” which means he or she has agreed to accept the Medicare-approved rate as full payment. If you have Medicare Advantage, your plans are also required to cover the same free preventive service). The ACA requires plans to provide these essential health benefits: outpatient care, trips to the emergency room, treatment in the hospital for inpatient care, care before and after your baby is born, mental health and substance use disorder services (including behavioral health treatment, counseling and psychotherapy), prescription drugs, services and devices to help you recover if you are injured, or have a disability or chronic condition, lab tests, preventive services including counseling, screenings, and vaccines to keep you healthy and care for managing a chronic disease and pediatric services. This includes dental care and vision care for kids. Therefore, the main substantive changes would be moving emergency room care to Part A, adding pediatric care to part B and adding prescription drugs to Part D.

- Medicare Part C (Medicare Advantage Expansion): This allows consumers the choice of having a private health insurance company for Parts A & B along with the optional Part D. It gives private insurers a chance to use Medicare Part A and Part B subsidies to provide an alternative to traditional Medicare coverage. It may provide additional coverage, such as vision, hearing, dental and even health and wellness programs.

- Medicare Part D expansion: Including current ACA and other health insurance plan participants in Part D would allow them to continue to have prescription medications. It would also allow for coverage of certain over-the-counter medications as currently covered by Medicare. Covering these OTC medications is important as medications oftentimes go from being prescription to being OTC and are still necessary for healthcare consumers.

- Medigap Supplement Expansion: This would allow consumers access to the current range and possibly new versions of coverage to supplement Parts A, B & D (replacing the ACA metal tiers).

- Add Medicare Part LTC: Offer a standard long-term-care insurance policy backed by the federal government.

Additional options and coverages can be provided through insurance companies, as they currently do for Medigap insurance supplements and Medicare Advantage. This provides choice and flexibility to consumers.

Yes, this would grow Medicare significantly. However, this would streamline the administration services provided by the Department of Health and Human Services, which oversees the Center of Medicare Services. Fewer programs to administrate means increased efficiency and lower costs if done properly.

Will there be any underwriting?

Medicare does not require underwriting. Expansion would allow for the continuation of guaranteed access for those with pre-existing conditions with no evidence of insurability.

Wait, isn’t Medicare going bankrupt?

Before, we move on to potential funding for a basic Medicare Type A plan available to all, let's be clear: Medicare is not going to go bankrupt. This is a common fallacy.

The 2016 report of Medicare’s trustees finds that Medicare’s Hospital Insurance (HI) trust fund will remain solvent — that is, able to pay 100% of the costs of the hospital insurance coverage that Medicare provides — through 2028. Even in 2028, when the HI trust fund is projected for exhaustion, incoming payroll taxes and other revenue will still be sufficient to pay 87% of Medicare hospital insurance costs. The share of costs covered by dedicated revenues will decline slowly to 79% in 2040 and then rise gradually to 86% in 2090. This shortfall will need to be closed through raising revenues, slowing the growth in costs or most likely both. But the Medicare hospital insurance program will not run out of all financial resources and cease to operate after 2028, as the “bankruptcy” term may suggest.

The 2028 date does not apply to Medicare coverage for physician and outpatient costs or to the Medicare prescription drug benefit; these parts of Medicare do not face insolvency and cannot run short of funds. These parts of Medicare are financed through the program’s Supplementary Medical Insurance (SMI) trust fund, which consists of two separate accounts — one for Medicare Part B, which pays for physician and other outpatient health services, and one for Part D, which pays for outpatient prescription drugs. Premiums for Part B and Part D are set each year at levels that cover about 25% of costs; general revenues pay the remaining 75% of costs. The trustees’ report does not project that these parts of Medicare will become insolvent at any point — because they can’t. The SMI trust fund always has sufficient financing to cover Part B and Part D costs, because the beneficiary premiums and general revenue contributions are specifically set at levels to ensure this is the case.

Read more about why Medicare is not "bankrupt."

Is the Affordable Care Act really affordable?

The U.S. uses a lot of healthcare. Expenditures were projected to reach $3.2 trillion (yes, trillion) in 2015 - or about $10,000 per person (Centers for Medicare & Medicaid Services, 2015). That’s a lot to pay for and more than most Americans can pay each year. Whether it can be paid for or not, the cost still remains.

Here’s how each dollar is spent: Prescription drugs - 22.1 cents, Physician services - 22.0 cents, Outpatient services - 19.8 cents, Inpatient services - 15.8 cents, Operating costs - 17.8 cents and Net Margin - 2.7 cents.

In a

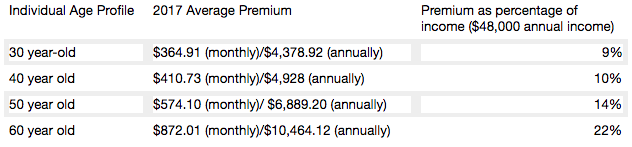

recent study, HealthPocket found that the percentage of monthly income needed to pay the average unsubsidized ACA premium can present considerable financial challenges to older adults. For example, when examining an individual who makes $48,000 annually (just above the $47,520 cut-off for individual premium subsidy eligibility in 2017) 60-year-olds would need to spend 22% of their income to afford the average silver plan premium while 30-year-olds would only need to spend 9%.

Average cost for an average annual worker and employer contributions for single and family (

Kaiser Family Foundation): Single coverage, all firms: total $6,445 (employer share, $5,306; employee share, $1,129). Family Coverage: total $18,142 (employer share: $12,865, employee share: $5,277). In 2017, the maximum allowable cost-sharing (including out-of-pocket costs for deductibles, co-payments and co-insurance) is $7,150 for self-only coverage and $14,300 for families.

Most marketplace consumers have affordable options. More than 7 in 10 (72%) of current enrollees can find a plan for $75 or less in premiums per month, after applicable tax credits in 2017. Nearly 8 in 10 (77%) can find a plan for $100 or less in premiums per month, after applicable tax credits in 2017.

Two recent

Kaiser Health Tracking Polls looked at Americans' current experience with and worries about healthcare costs, including their ability to afford premiums and deductibles. For the most part, the majority of the public does not have difficulty paying for care, but significant minorities do, and even more worry about their ability to afford care in the future. Four in ten (43%) adults with health insurance say they have difficulty affording their deductible, and roughly a third say they have trouble affording their premiums and other cost sharing; all shares have increased since 2015. Among people with health insurance, one in five (20%) working-age Americans report having problems paying medical bills in the past year that often cause serious financial challenges and changes in employment and lifestyle.

Even for those who may not have had difficulty affording care or paying medical bills, there is still a widespread worry about being able to afford needed healthcare services, with half of the public expressing worry about this. Healthcare-related worries and problems paying for care are particularly prevalent among the uninsured, individuals with lower incomes and those in poorer health. Women and members of racial minority groups are also more likely than their peers to report these issues.

Making health insurance affordable again

Medicare Part A is currently available with no premium if you or your spouses paid Medicare taxes. Medicare Part A can continue to be offered for free to those who pay taxes and for those who qualify for Medicaid.

Medicare Part B premiums are subsidized with the government paying a substantial portion (about 75%) of the Part B premium, and the beneficiary paying the remaining 25%. Premiums are subsidized, with the gross total monthly premium being $134. This amount is reduced to $109 on average for those on Social Security. Depending on your income, the premium can increase to $428.60 monthly. View information on Part B premiums

here.

Medicare prescription drug coverage helps pay for your prescription drugs. For most beneficiaries, the government pays a major portion of the total costs for this coverage, and the beneficiary pays the rest. Prescription drug plan costs vary depending on the plan, as does whether you get extra help with your portion of the Medicare prescription drug coverage costs. Higher earners pay more.

Beneficiaries enrolled in Medicare Advantage typically pay monthly premiums for additional benefits covered by their plan, in addition to the Part B premium.

Kaiser Family Foundation figures.

How is Medicare financed?

Medicare Part A is financed primarily through a 2.9% tax on earnings paid by employers and employees (1.45% each) (accounting for 88% of Part A revenue). Higher-income taxpayers (more than $200,000/individual and $250,000/couple) pay a higher payroll tax on earnings (2.35%). To pay for Part A, taxes will need to go up, but the trade-off is that premiums for the supplemental coverage will be less because it covers less - net impact to the consumer is zero.

Medicare Part B is financed through general revenues (73%), beneficiary premiums (25%), and interest and other sources (2%). Beneficiaries with annual incomes over $85,000/individual or $170,000/couple pay a higher, income-related Part B premium, ranging from 35% to 80%. The ACA froze the income thresholds through 2019, and, beginning in 2020, the income thresholds will once again be indexed to inflation, based on their levels in 2019 (a provision in the Medicare Access and CHIP Reauthorization Act of 2015). As a result, the number and share of beneficiaries paying income-related premiums will increase as the number of people on Medicare continues to grow in future years and as their incomes rise. Premiums would be less than under current individual insurance plans because certain essential benefits would be covered by the expanded Medicare Part A.

Medicare Part D is financed by general revenues (77%), beneficiary premiums (14%) and state payments for dually eligible beneficiaries (10%). As with Part B, higher-income enrollees pay a larger share of the cost of Part D coverage.

Medicare Part C (The Medicare Advantage program) is not separately financed. Medicare Advantage plans such as HMOs and PPOs cover all Part A, Part B and (typically) Part D benefits. Beneficiaries enrolled in Medicare Advantage plans typically pay monthly premiums for additional benefits covered by their plan in addition to the Part B premium.

From Kaiser Foundation:

The Facts on Medicare Spending and financing worksheet.

The public need for increased plan choice and market stability

Health insurance exchanges haven’t worked so far. Currently, there are only 12 state-based marketplaces; five state-based marketplace-federal platforms, six state-partnership marketplaces; and 28 federally facilitated marketplaces. A list of State Health Insurance Marketplace types can be be found on the Kaiser Family Foundation

website.

The Congressional Budget Office said that although the ACA’s markets are “stable in most areas,” about 42% of those buying coverage on Obamacare’s exchanges had just one or two insurers to pick from for this year. Currently, one in three

counties has just one insurer in the local market, significantly less choice than the one in 14 counted last year, according to the nonpartisan Kaiser Family Foundation. And five states have a single insurer: Alabama, Alaska, Oklahoma, South Carolina and Wyoming. Moving to a Medicare-based system would mean that, if an insurance company decides to leave a county or state, the residents still have access to health insurance. There are parts of Tennessee where there may not be any exchange insurance options for 2018. And Oklahoma’s insurance regulator warned last week that his state’s lone carrier may quit the market.

With issues facing the Affordable Care Act on subsidies, Medicaid expansion and other potential changes, consumers may end up with few choices as insurance companies decide to not participate in the exchanges in the future. Humana has announced that it will drop out of the 11 states where it offers ACA plans. Other major insurance companies, including Anthem, Aetna and Molina Healthcare, have warned that they can’t commit to participating in the ACA exchanges in 2018.

Medi-gap supplements and Medicare Advantage will boost choice. Medicare Advantage has proven to be popular, and enrollment is expected to increase to all-time high of 18.5 million Medicare beneficiaries. In 2017, this will represent about 32% of Medicare beneficiaries. Typical Medicare Advantage plan providers offer managed care plans.

Access to the Medicare Advantage program remains nearly universal, with 99% of Medicare beneficiaries having access to a health plan in their area. Access to supplemental benefits, such as dental and vision benefits, continues to grow. More than 94% of Medicare beneficiaries have access to a $0 premium Medicare Advantage plan. 100% of Medicare beneficiaries – including Medicare Advantage enrollees – have access to recommended Medicare-covered preventive services at zero cost sharing.

Consumers have access to information to improve plan choice. Medicare beneficiaries are allowed a one-time opportunity to switch to a five-star Medicare Advantage plan or prescription drug plan in their area any time during the year. Medicare has a low-performing icon on

Medicare.gov so beneficiaries know which plans are not performing well. Medicare Advantage plan sponsors are also required spend at least 85% of premiums on quality and care delivery and not on overhead, profit or administrative costs.

According to a recent fact sheet from

CMS.gov,

Moving Medicare Advantage and Part D Forward: Some counties have low Medicare Advantage penetration rates because the number of hospitals and doctors is too low for use of a managed care network to make much sense. This mirrors some of the reasons why there are few marketplace options in certain counties and state and is exactly why there needs to be a plan available through the federal government, as with the current Medicare Parts B & D.

When retirees are unhappy with Medicare Advantage plan provider directories, they typically combine traditional Medicare coverage with Medicare supplement insurance, or Medigap coverage. Retirees using Medigap coverage with traditional Medicare can use any provider that takes Medicare.

Consumers are better able to control their Medicare Advantage Plan (Part C) premiums by choosing a plan without a monthly premium, having a plan that pays part of Medicare Part B, having a deductible, choosing a copayment (coinsurance) amount, choosing the type of health services, setting their limit on annual out-of-pocket expenses and choosing whether they go to a doctor or other medical service supplier who accepts assignment (from Medicare).

Balancing the risk pool

The risk pool must be sufficiently large to take advantage of the law of big numbers. Insurance companies reflect healthcare costs, and their mission is to spread the risk and be balanced. If the risk pool is unbalanced by covering too many sick people and not enough healthy people, the insurance company will have higher claims and will need to collect higher premiums. When this happens, healthier individuals are usually the first to drop coverage, which they feel is not needed, which leaves a growing proportion of “less healthy” individuals. At some point, the imbalance becomes unsustainable, and the carriers exit the market entirely.

The only reason healthy people buy health insurance is that they know that if they wait until they get really sick no insurance company will sell them a policy. The same principle holds true for all insurance products. You can’t buy auto insurance after you get into an accident. You can’t buy life insurance at a reasonable cost after your doctor has given you six months to live. The fact that your car is already wrecked, or your arteries already clogged, are pre-existing conditions that no insurance company would be expected to ignore.

Allowing voters the low-cost option to buy health insurance after they actually need it is very popular. It’s like promising motorists they can stop paying their monthly auto insurance premium and just buy a policy after they have an accident. If the government were to require this, all auto insurance companies would quickly go out of business (unless they were bailed out by the government).

Contrary to belief, younger people (millennials) do want want health insurance and consider it a top life priority, according to a study from research firm Benson Strategy Group. Eighty-six percent of millennials are insured, and 85% said it is "absolutely essential" or "very important" to have coverage, according to the survey. Researchers said most millennials get their insurance through an employer (39%) or Medicaid (20%).

Shifting work force and ending the current group health insurance market

The U.S. work force is shifting, with fewer Americans working at large employers and being covered by group health insurance. Americans are moving more to being “gig” employees, freelancers/consultants, part-time employees, job movement, cash employees and seasonal employees and continuing to start businesses.

For employers, counting employees for purposes of ACA compliance seems to be an expensive nightmare.

The size of your employer is a major factor on if health insurance is offered: 96% of firms with 100 or more employees offered health insurance, 89% of employers between 50 and 99 employees offer health insurance, while 53% of employees with three to 49 workers offered health insurance; the average is 56% of employers offering coverage. So unless you work at a big firm, you can't count on health insurance anyway. And dependent on the size of the firm, there is no guarantee that it will offer coverage to spouses, dependents or domestic partners.

Even those with group health insurance received less value than historically. According to a recent LinkedIn study (2/2017), a total of 63% of respondents indicated that their healthcare benefits were either more expensive or stingier than in the previous year, and 40% saw both an increase in premium costs as well as higher out-of-pocket copays and deductibles when they used their health plans.

In a survey (2/2017), nearly one in five LinkedIn members in the U.S. (or 19%) indicated that health insurance has been their primary reason for taking, leaving or keeping a job.

If health insurance is available as proposed through individual, portable insurance plans, there will no longer be employer health insurance programs. Excluding premiums from taxes was worth about $250 billion in forgone tax revenue in 2013, according to the Congressional Budget Office. Some health economists have argued that the exemption artificially drives up health spending. Employer-provided health benefits, often worth thousands of dollars a year, aren’t taxed as wages are. People who have to buy coverage on their own don’t enjoy the same tax advantage. Currently, employers do offer supplemental benefits to their employees that they often pay at least part of the premium.

See also: Walmart’s Approach to Health Insurance

Eliminate health insurance age bands

Medicare premiums do not increase with age. Medicare premiums do increase based on income. If someone age 85 is not paying more than someone age 65, why should someone age 50 pay more than someone age 35? Why should a basic health insurance plan work any differently?

Yes, healthcare costs increase with age. Per-person healthcare spending for the 65 and older population was $18,988 in 2012, more than five times higher than spending per child ($3,552) and approximately three times the spending per working-age person ($6,632). From NHE

Fact Sheet (Centers for Medicare and Medicaid Spending)

Health insurance is currently priced by age bands starting at age 21. Thirty-year-olds have premiums that are 1.135 times more; 40-year- olds pay 1.3 times more; 50-year-olds pay 1.786 more, and 65-year-olds pay 3 times the cost listed. Based on a

study by Value Penguin on the Average Cost of Health Insurance (2016).

Private insurance companies are required to offer the same benefits for each lettered Medicare supplement plan, and they do have the ability to charge higher premiums for this coverage. Medicare Supplement Pricing does allow for community-based pricing. And they also do have attained-age-rates where premiums increase as you get older. However, the issue-rated plans have premiums that are lower based on the age which you enroll.

Higher premiums for higher earners

Medicare does require higher-income beneficiaries to pay a larger percentage of the total cost of Part B based on the income you report to the Internal Revenue Service (IRS). Monthly Part B premiums are equal to 35, 50, 65, or 80 percent of the total cost, depending on what is reported to the IRS. This in keeping with the current progressive tax system (or at least the planned theory of a progressive tax system).

A big Medicare impact from the ACA came via financial improvements it put in place to help the program. It raised a bunch of taxes, including requiring high-income wage earners to pay higher Medicare payroll taxes and stiff premium surcharges for Medicare Part B and D premiums. Health providers and Medicare Advantage insurance plans were also willing to accept lower payment levels from Medicare in exchange for the law’s provisions that would expand their access to more insurance customers.

The individual mandate is not working

Besides being unpopular, the individual mandate is not working. The economics of the ACA are not sound for the long term as there is no balanced offset between how insurance companies typically operate from charging high-risk consumers more than low-risk consumers and providing coverage to all. A planned offset was the penalties on those who didn’t participate. The Supreme Court recognized this as a flaw and Justice Roberts argued that the relative lightness of the penalties was insufficient to compel anyone to buy insurance and, as a result, he considered them to be a “tax” that could be voluntarily avoided rather than a coercive penalty to force commercial activity.

The individual mandate requires nearly all Americans to have health insurance coverage. The individual mandate is an important as it met the critical issue of insurance companies guarding against anti-selection; having health people wait until they need health insurance to sign up. This was meant to be an incentive, however, it is a penalty.

The full penalty for 2016 was $695 per person, $347.50 for each child, up to a maximum of $2,085 -- or 2.5% of your household income, whichever is higher.

It won’t ever work as it’s currently set up since the IRS isn't allowed to collect this penalty the same way it collects on other tax debts. The IRS can deduct penalties you owe from future tax refunds, however, they cannot garnish wages.

The IRS last month quietly reversed a decision to reject tax returns that fail to indicate whether filers had health insurance, received an exemption or paid the penalty. While this has always been key to enforcing the individual mandate, the IRS had been processing returns without this information under the Obama administration.

The IRS attributed the reversal to Trump's executive order that directed agencies to reduce the potential financial burden on Americans.

There are some who feel that since the IRS will accept a tax return without the penalty, that it can be skipped. The IRS has stated that: "Legislative provisions of the ACA law are still in force until changed by the Congress, and taxpayers remain required to follow the law and pay what they may owe,". The agency added that "taxpayers may receive follow-up questions and correspondence at a future date.”

This uncertainty and lack of uniformity is not positive for anyone. And you catch more flies with honey than vinegar. Therefore boosting the benefits is going to work better than a straight out penalty. For insurers, figuring out how to prod younger, healthier Americans to sign up for coverage is critical. As covered elsewhere in this article, there are other, potentially more effective ways to accomplish this. Having a base plan like Medicare will shift some burden directly onto the U.S. Government.

Increasing the burden on the U.S. government and the NFIP

Yes, it’s going to take a lot of planning and conservative

assumptions and could be set up along similar lines as the National Flood Insurance Plan (NFIP) created in 1968 by Congress to help provide a means for property owners to financially protect themselves. NFIP is administered by the Federal Emergency Management Agency (FEMA), which works closely with more than 80 private insurance companies to offer flood insurance to homeowners, renters, and business owners. In order to qualify for flood insurance, the home or business must be in a community that has joined the NFIP and agreed to enforce sound floodplain management standards. Coverage can be purchased through private property and casualty insurance agents. Rates are set nationally and do not differ from company to company or agent to agent. These rates depend on many factors, which include the date and type of construction of your home, along with your building's level of risk. Check out the National Flood Insurance Plan

overview. Read

answers to common questions about NFIP. There are issues with the NFIP and it is scheduled for reform. The solution to this is to have flexible pricing for private insurance companies such as with Medicare Supplements and Medicare Advantage.

Revise tax credits

Providing tax credits helps low- and moderate-income patients afford health insurance. Premium tax credits protect consumers from rate increases. Marketplace tax credits adjust to match changes in each consumer’s benchmark silver plan premium. Additional consumers are eligible for tax credits. As Marketplace tax credits adjust to match increases in benchmark premiums, some consumers in areas that had low benchmark premiums in 2016 may be newly eligible for tax credits in 2017. Of the nearly 1.3 million HealthCare.gov consumers who did not receive tax credits in 2016, 22 percent have benchmark premiums and incomes in the range that may make them eligible for tax credits in 2017. In addition, an estimated 2.5 million consumers currently paying full price for individual market coverage off-Marketplace have incomes indicating they could be eligible for tax credits.

The Advance Premium Tax Credit is an ACA mechanism for helping some ACA exchange plan users pay for their health coverage. The enrollees estimate when they apply for coverage how much they'll earn in the coming calendar year. The exchange and the IRS use the cost of the coverage and the applicant's income to decide how much the applicant can get. If the applicant qualifies for APTC and buys an exchange plan, the government sends the APTC help to the health coverage issuer while the plan year is still under way. The enrollee does not get to touch the APTC cash.

The ACA currently requires consumers to predict in advance what their incoming will be in the coming year. The majority of consumers apply for individual health insurance during open enrollment for the following year in the preceding end of the year. So they are guessing what their income will be the following year. Then, they even up with the IRS the following year (almost a year and a half later).

Consumers who predict their income be too low and get too much tax credit money are supposed to true up with the IRS when the file their taxes the following spring. The IRS has an easy time getting the money when consumers are supposed to get refunds. It can then deduct the payments from the refunds. When consumers are not getting refunds, or simply fail to file tax returns, the IRS has no easy way to get the cash back.

The exchanges and the IRS also face the problem that some people earn too little to qualify for tax credits but too much to qualify for Medicaid. Those people have an incentive to lie and say their income will be higher than it is likely to be.

And it’s not even close to working, The Treasury Inspector General for Tax Administration, an agency that monitors the Internal Revenue Service, gave that figure in a new report on how the IRS handled ACA premium tax credit claims for 2014 and 2015. The IRS found that, as of June 30, 2016, the IRS had processed about 5.3 million 2015 returns that included claims for $20.3 billion in tax credits, part of which was $18.9 billion in APTC subsidy help. In June 2015, the IRS had processed 3 million 2014 returns that included claims for $9.8 billion in ACA premium tax credits, including $9 billion in APTC help. For the 2015 returns, which were processed in 2016, IRS program errors led to IRS premium tax credit amount calculation errors for 31,493 returns, TIGTA says. The programming errors led to 16,375 filers getting an average of about $300 too much help each, and 15,118 filers getting an average of $440 too little help each. ACA public exchange program managers send their own tax credit data files to the IRS. The IRS investigates when the gap between what the exchange reports and what the taxpayer reports is big, but not when the gap is small. Because of that policy, the IRS failed to investigate exchange-taxpayer data gaps for 903,488 2015 returns. A majority of the unexamined gaps seemed to hurt taxpayers, rather than helping them, TIGTA says. A review of the APTC gap data suggests that 511,384 affected filers may have missed out on an average of about $1,000 in help each, and that 392,104 may have gotten away with receiving an average of about $300 too much help each, according to TIGTA.

Another issue is that currently, eligibility to receive premium tax credits to purchase exchange coverage is determined by income and whether individuals and families have access to affordable employer coverage. However, many families are not eligible for premium and cost-sharing subsidies to purchase coverage on the exchanges because of the “family glitch,” because determinations about the affordability of employer-sponsored coverage are based on the cost of employee-only coverage, ignoring the cost of family coverage. As a result, these lower-income families are ineligible for subsidies to purchase coverage on exchanges. An estimated 10.5 million adults and children may fall within the family glitch, according to the Department of Health and Human Services’ Agency for Healthcare Research and Quality

Credits would be relative to income and would be lower for those in higher brackets to match our current progressive income tax system. These advance able, refundable tax credits would need to reflect income and location of the health insurance plan. Tax credits would be available to more Americans than under current ACA rules.

Increase subsidies

On the insurer side, risk-based subsidies can help ease the financial pressure posed by enrollees with high health care costs.

Subsidies under the ACA are available to help qualifying Americans pay for their health insurance premiums. These subsidies work on a sliding scale, limiting what you are personally required to contribute toward your premiums to a fixed percentage of your annual income.

The dollar value of your subsidies will depend in part on the cost of the benchmark ACA plan in your area. If the benchmark plan costs more than a certain percentage of your estimated annual income, you can get a subsidy in the amount of the difference. You may then use that subsidy when you buy a qualified ACA health insurance plan. The main factor is your income. You can qualify for a subsidy if you make up to four times the Federal Poverty Level. That's about $47,000 for an individual and $97,000 for a family of four. If you're an individual who makes about $29,000 or less, or a family of four that makes about $60,000 or less, you may qualify for both subsidies.

Subsidies would also need to be fair to older enrollees. Current subsidies under the ACA, allow eligible enrollees to obtain a plan for less than 10% of their income. Having the proper type of subsidy will be crucial. According to the Price-linked subsidies and health insurance mark-ups

study from the National Bureau of Economic Research

Senior House Republicans have stated that they expected the federal government to continue paying billions of dollars in subsidies to health insurance companies to keep low-income people covered under the Affordable Care Act for the rest of this year — and perhaps for 2018 as well.The Republican-led House had previously won a lawsuit accusing the Obama administration of unconstitutionally paying the insurance-company subsidies, since no law formally provided the money.Although that decision is on appeal, President Trump could accept the ruling and stop the subsidy payments, which reduce deductibles and co-payments for seven million low-income people. If the payments stopped, insurers — deprived of billions of dollars — would flee the marketplaces, they say. The implosion that Mr. Trump has repeatedly predicted could be hastened. The annual cost of these subsidies is estimated at 7 billion dollars. See

“Health Subsidies for Low Earners Will Continue Through 2017, G.O.P. Says”.

Keep the cost-sharing reductions

People who earn up to $29,000 not only get subsidies to pay for their health insurance premiums, they also receive "cost-sharing reduction," or CSR, funds, to make out-of-pocket costs more affordable. Maintaining the CSR payments, which amount to $9 billion to insurers for 2017 is critical. Currently payment of these CSR funds have been halted by the House.

Wait, isn’t the ACA already costing too much?

It turns out that the ACA has turned out to much more cost effective than originally projected. The Congressional Budget Office now projects its cost to be about a third lower than it originally expected, around 0.7 percent of G.D.P. A report from the nonpartisan Urban Institute argues that the A.C.A. is “essentially underfunded,” and would work much better — in particular, it could offer policies with much lower deductibles — if it provided somewhat more generous subsidies. The report’s recommendations would cost around 0.2 percent of G.D.P.

Use a value-added tax (VAT) or other sales tax

Use the current Medicare Payroll Tax and supplement it with a sales/value added tax, that way everyone pays for the plan who would use it - underground economy, cash economy and those don’t file income tax returns This would encourage more people to file income tax returns to get the proposed (current) credit. This would be a boost to the US economy and the Federal Budget as this missed income tax revenue while reducing resources from the IRS in finding those who don’t file income tax returns.

Trade-offs needs to made and the only way to do so is to ensure that everyone has a baseline of benefits . Adding a value added tax/sales tax to help finance it would ensure that that plan is not solely supported by those who pay income, the plan is supported by anyone who makes a purchase, as let's face it, some people don't report income. Tax credits would still be available to those who qualify based on income. This would also encourage more people to file tax returns to make sure they received the credit if eligible. In fact, give everyone who files a $100 credit for their health insurance if they file, I'll bet the number of income tax returns would rise significantly.

Stop tax evasion

If all tax evasion were stopped, this alone could pay for health care. Following are some

stats on tax evasion from The National Tax Research Committee released by Americans for Fair Taxation: Estimated Future Tax Evasion under the Income Tax and Prospects for Tax Evasion under the FairTax: New Perspectives

To enable the federal government to raise the same level of revenue it would collect if all taxpayers were to report their income and pay their taxes in full, the income tax system, in effect, assesses the average household an annual “surtax” that varies from $4,276 under the most conservative scenario, to $8,526 based on the more likely to occur historical evasion trends. The IRS estimates that almost 40% of the public are out of compliance with the present tax system, mostly unintentionally due to the enormous complexity of the present system. These IRS figures do not include taxes lost on illegal sources of income with a criminal economy estimated at a trillion dollars.

Market stabilization - Risk-sharing modifications

Diversifying the risk pool and keeping the market stable is a critical factor in maintaining viability for insurance companies. The ACA included 3 components to help accomplish this goal:

- Reinsurance provides payment to plans that enroll higher-cost individuals. This protects against premium increases in the individual market by offsetting the expenses of high-cost individual. It was expected that this would be profitable for the Government, however, while it has been able to meet its obligations, it has yet to turn a profit. As this has been a positive, the program should be maintained. Reinsurance must continue to be available for plans selling individual and small group products.

- Risk adjustment redistributes funds from plans with lower-risk enrollees to plans with higher-risk enrollees. This is intended to protect against adverse selection and risk selection in the individual and small-group markets inside and outside the exchanges by spreading financial risk across the markets.

- Risk corridors limit losses and gains outside of an allowable range. This is designed to stabilize premiums and protect against inaccurate premiums.Risk corridors protect plans that accumulate unexpectedly high risks by giving them access to funds collected from insurers that experience unexpectedly low risks. This has not worked so far and the programs owes more than $8 billion for 2014 and 2015. If 2016 losses are about the same ($7 billion in losses on $90 billion in premium revenue) the total ACA risk corridors program shortfall will increase to about $15 billion.

It is important to note reinsurance and risk corridors are used without controversy in the Medicare private drug-insurance market. Risk corridors though have been problematic for Medicare Part D. Several program modifications may be necessary at the same time—that is, a package of changes—to balance concerns about cost control and incentives for selection behavior. See

sharing risk in Medicare Part D.

Maintain a medical loss ratio

Insurance companies profits should be reasonable so the medical loss ratio should be kept in place. The MLR provision “plays an essential role in holding insurance companies accountable for how they spend the premium dollars they collect from consumers. Weakening it could increase costs for consumers by allowing insurance companies to spend more on administrative activities like marketing and profits.

It’s important to remember that for a health insurance company (or any insurance company for that matter) to stay in business, is that must make a profit so that it can be around to pay claims. Premiums must be adequate to cover claims, administrative costs, taxes, and fees, and still provide a margin for profit or contribution to reserves and surplus. At bottom, carriers operate on a cost-plus model. Medical costs—principally hospitals, physicians, imaging and prescription drugs—are “what they are.” Insurance companies merely facilitate their payments. Of course, how payments are determined and made is enormously complex. Prices are negotiated (but only at the margins), incentives applied, and networks built and nurtured, all to gain incremental competitive advantages in the marketplace. Here’s the overall breakdown: Overall: Medical expenses are 80%, Operating Costs are 18%, net margin 3%. Per:

America's Health Insurance Plans (AHIP). Please visit the link for breakdowns on the costs and sources of information. Values exceed 100% due to rounding.

Adding incentives to education and prevention

Carrots always work better than sticks. It is important to emphasize the benefits of having health insurance. This can be stressed through education about preventative care and how it increases overall long term health. When we are young, it is hard to envision the health issues that happen as we age. Incentives to participate in wellness programs can be a consideration and do not have to be monetary. As an example, consider how some health insurance plans are experimenting with giving out “Fitbit's” to plan participants. If someone signs up for a Medicare Advantage or Medicare Supplement plan and meets criteria of monitoring their health, they could receive a fitness tracker at a discount with software to help their health. This would lower costs over the long term. Education and prevention are key.

Cost penalties

For some people carrot’s aren’t enough and in order to ensure fairness, there would need to be a cost penalty. Overall, there is not much written about dissatisfaction with Medicare penalties, so why not apply them across the board? For example, if you don’t purchase Medicare when you are first eligible, your monthly premium may go up 10%. You'll have to pay the higher premium for twice the number of years you could have had Part A, but didn't sign up. For example, if you were eligible for Part A for 2 years but didn't sign up, you'll have to pay the higher premium for 4 years. There are exceptions to this rule. However, this is fair to all and does create a penalty for waiting until you need to use care. Or we could go with the Part B penalty which is more stringent and increases the monthly premium for Part B by up to 10% for each full 12-month period that you could have had Part B, but didn't sign up for it.

Limited open enrollment period

Continue the current Medicare open enrollment period. Limit the exceptions. Shortened enrollment period are necessary to ensure that people apply before they need coverage. Currently many people sign up for the exchanges during the year and then drop their plans during the year, this does not allow insurance companies to have a full year of premiums. Exceptions would have to be verified for reasons such as birth of a child (adoption, etc), marriage or other major life event. Insurers have done studies showing that claims costs are higher for those who’ve enrolled under the ACA special enrollment periods which means that it’s likely that people are gaming the system to just have coverage when they need it.

Continuous coverage requirement/premium penalty

Insurance companies can be more effective in setting reasonable premiums when they have more consistent data such as continued premium payments. When someone signs up for insurance companies project that they will continue the policy for the year. If they drop the coverage mid-year, there is less income to the insurance company. Consumers should be able to drop coverage at any time. However, just like with Medicare Part B, they would have to pay a higher premium of up to 10% for each 12 month period during which they didn’t have coverage (perhaps to a maximum of 40%) unless they had “good cause”. This would provide a disincentive to consumers purchasing coverage only when they need it. Just like it’s okay for homeowners to not be able to purchase coverage while their home is on fire, they should not be able to purchase health insurance only when they need it. Coverage would still be available to all.

Overdue premium payment requirement

Payment of any overdue premiums with shorter grace period for supplemental plans to match Medicare: Enrollees would have to pay overdue premiums before enrolling with the same insurer the following year. If you don’t pay your Medicare premiums, you risk losing coverage. But it won’t happen right away. You’re billed for Part B in 3-month increments, and you will have a grace period of 3 months after the due date. If you have not paid by the end of the grace period, you’ll receive a letter letting you know that your coverage will be terminated at the 4-month mark, unless you can pay in full 30 days after termination notice. Consumers would need to wait until the next open enrollment period, unless they qualified for a special enrollment period or had “good cause”.

Reduce fraud and billing errors

Fight fraud and billing errors. The exact amount lost to fraud, is of course, unknown.

The National Health Care Anti-Fraud Association estimates conservatively that health care fraud costs the nation about $68 billion annually with other estimates ranging as high as 10% of annual health care expenditure, or $320 billion. Visit

The Coalition Against Insurance Fraud for more statistics. Not really pocket change. And while there are are significant resources aimed at fighting fraud, it's still not sufficient. Read

this article to learn more about the challenges of health care fraud and why it is not a victimless crime. Insurance companies and the health care industry pass on the cost to consumers. Medical billing errors further compound the issue. If you suspect that there has been a fraudulent billing issue,

read this FAQ. Each state insurance department would need to beef up their investigator’s department or we would need federal investigators from Medicare.

Increase insurance company oversight

There is a concern about insurance companies “gaming” the Medicare Advantage payment system by making patients look sicker than they are. This allows the insurance companies to increase their Medicare billing.

Overspending tied to inflated risk scores has repeatedly been cited by government auditors, including the Government Accountability Office. A series of articles published in 2014 by the Center for Public Integrity found that these improper payments have cost taxpayers tens of billions of dollars.

The Justice Department recently joined a California whistleblower’s lawsuit that accuses insurance giant UnitedHealth Group of fraud in its popular Medicare Advantage health plans. According to the attorney, William K. Hanagami, the combined cases could prove to be among the “larger frauds” ever against Medicare, with damages that he speculates could top $1 billion.

Healthcare cost containment

Health care costs are rising faster than inflation. It is not realistic to be able to keep up with this. Last year, Americans spent an equivalent of about 18% of Gross Domestic Product (GDP) on health care. Cost pressures will rise with our aging population. Much of the current spending is inefficient. Technology, discussed further on could help with these inefficiencies.

Between November 2015 and November 2016, medical care prices increased 4.0 percent. Health insurance prices and prescription drug prices both increased 6.0 percent during this 12-month period. Medical care commodities and services make up about 8.5 percent of the total Consumer Price Index for All Urban Consumers (CPI-U) market basket. The CPI-U for all items rose 1.7 percent over the year ending November 2016.From November 2010 to November 2016, medical care prices have increased 19.7 percent, driven by increases in the prices of hospital services (+32.5 percent), health insurance (+27.8 percent), and prescription drugs (+24.0 percent). Only the prices of nonprescription drugs have fallen over this 6-year period, declining 2.7 percent. Comparatively, the CPI-U for all items has increased 10.4 percent over the same period. U.S. Bureau of Labor Statistics

See also: Real Reason Health Insurance Is Broken

Legitimate pricing transparency

A strategy of requiring healthcare providers to publish their rates and offer the same discounts to all health plans could result in more competition and options for consumers. Full cost disclosure would include the premium along with the total maximum annual out-of-pocket costs. Regulating the discounts would make it easier for consumers to comparison shop accurately so they could take control of their spending and help bring down the cost of care overall, he adds.

This is part of the ACA, however it has been overlooked. This included holding providers of care accountable for costs and quality of services through value-based payments that reward clinicians and organizations that provide better care at lower costs. The price of a service is determined by the cost of the service rather than the insurance held. This does not meant they cannot set their own rates, however, they cannot charge different rates to different customers.

Congress must compel medical providers to play by the same rules that apply to all other sellers of consumer goods and services. They should remain free to set their own prices.

Legitimate pricing of health services will empower patients to be able to shop for fair value. This would make networks obsolete as there would be no distinction between in-network and out-of-network. Real free market competition by healthcare providers will reduce health expenditures by a minimum of 33% - overnight (and the USA would still have approximately the highest cost per person healthcare on earth).

A “Petition to End Predatory Healthcare Pricing” and to require legitimate pricing has garnered more than 100,000 signatures this year. As the petition states: a simple blood test for cholesterol can range from $10 to $400 or more at the same lab. Hospitalization for chest pain can result in a bill from the same hospital for the same services ranging anywhere from $3,000 to $25,000 or more. Price transparency initiatives are futile when prices may vary by a factor of 100 for the exact same service performed by the same provider.

Improved data sharing

Bloomberg explained in a report that the pooling of data is important, especially for small insurers that do not have extensive databases that larger insurers have. The data is used to determine actuarial rates that reflect the risk attached to coverage offered by insurers, which helps them accurately assess exposures and price premiums.“One of the main benefits of the exemption is that it allows insurers to share information on insurance losses so that the insurance industry can better project future losses and charged actuarially based prices for their products,” the statement also said.

Additionally, the Property Casualty Insurers Association of America said in a February testimony that, “(anticompetitive) price fixing, bid rigging, and market allocations are generally illegal under state anti-trust laws.” This would hold true for health insurance companies as well. The Bloomberg report noted that measures are already in place to preclude anti-competitive practices in the industry in each of the states.

Increase wellness incentives/credits

This can be done by insurance companies, employers and other centers of influence. Using fit bits to encourage physical activity. Surcharge for tobacco cessation. Weight management. Lifestyle changes.

Increase virtual health care options

Increase the use of telemedicine/“skype” medicine - easier for everyone to not have to come in to see a doctor - reduces costs, saves time for consumer and still provides solutions. Implement more urgent care facilities to reduce the amount of emergency room visits. It is estimated that this could save $7 billion annually.

Healthcare savings account expansions

The cost of health care starts with the health insurance premium, however, it also includes deductibles, co-payments, co-insurance and whatever is not covered that are still medical necessities - think aspirin, allergy medicine, etc. In addition there are expenses such as travel to treatment, child care, special equipment or home modifications, or lost income caused by time away from work. Health insurance may really be 50-60% of your total annual health care outlay.

Implementing and allowing health care saving accounts for all would help offset all of these other costs and provide positive economic benefits. Moving from strictly being a reimbursement plan to being a reimbursement plan and a retirement plan would help increase American’s retirement savings and offset the guessing required on reimbursement accounts such as flexible spending accounts and dependent care spending accounts which are currently only available through employers.

Americans need assistance on saving more money and this will work better than FSA’s that can be use it or lose it. HSAs are now available only to people who have high-deductible health insurance plans. These plans should be open to everyone. The tax credit for an HSA would be set to a level sufficient to cover the maximum premiums combined with deductibles, co-pay and maybe an extra 25% for additional expenses outlined above.

This would also help offset the anticipated high cost of healthcare costs in retirement. According to a study by Fidelity in 2016, a couple starting retirement today would have estimated total health care costs $260,000. That’s a lot, so saving in advance for it would be beneficial. Currently health savings accounts have significant tax benefits and can be used an additional retirement account. Withdrawals after age 65 for general retirement purposes have no penalties, you simply withdraw the money and pay ordinary income taxes just like an IRA, 401(k) or other qualified retirement plan.

Allow states to take over rate reviews

Under the Obama administration, the CMS determined that all but four states have adequate rate reviews, and “we don’t see any reason why the federal government should be duplicating that review”. In a market stabilization proposed rule published Feb. 17 in the Federal Register, the CMS proposed allowing states to set standards for network adequacy. Deferring to states to take on more authority in implementing health-care reform has been a major theme of Republicans in Congress.

Under the current regulatory regime, this really should be handled by state insurance departments which currently oversee premiums for auto insurance, homeowners insurance, long term care insurance (lines of coverage differ by state).

Maintain current rules for insurance companies to not sell across state lines

Currently there is a mostly effective State based regulatory system centralized through the National Association of Insurance Commissioner. Overall, the NAIC has enacted some good model regulations. Under the current regulatory set-up, insurance companies can set up headquarters in states with weaker requirements which they already do anyway when they can. In the long run, this is not good for anyone. Currently, each state sets its own consumer protections and demands for what insurance must cover, if an insurance company could sell policies in a state without that state’s approval, then any state specific requirements would not apply resulting in fewer consumer protections, less-comprehensive plans and limit states' ability to regulate insurance companies. Premiums would also not be lower since a key driver of health insurance premiums is local costs of health care. Another challenge is that almost all health care is delivered locally. To succeed, insurance companies need a significant toe-hold with hospitals and other providers in their local market; an out-of-state insurer would lack that and thus struggle in its negotiations to form a delivery network. This is why many new entrants to the health insurance market haven’t succeeded. Read more from the NAIC Center for

Insurance Policy & Research: Interstate Health Insurance Sales: Myth vs. Reality.

Insurance agent value and compensation

Keep professional, trained insurance agents around. For example in Oregon, insurance agents earn about $400 per year for each Medicare supplement or Medicare Advantage policy they write, but only about $144 per year in commissions for selling an individual policy through the ACA public exchange system. This lower compensation level hurts consumers, by reducing their access to licensed professionals who can help them choose and understand coverage. Regulators should set and enforce commission payment standards.Neither the current law nor any reform effort will be successful unless a large number of healthy Americans decide to sign up for coverage. Agents play a critical role in the orderly delivery of health insurance.Traditional agents and brokers “do a much better job’’ of helping people get proper coverage than do the insurance counselors — called “navigators’’ or “assisters’’ — whose positions were created by the ACA.

This would require a shift in the calculation of the Medical Loss Ratio (MLR) Rule. Currently, if an insurance company spends less than 80 percent (or 85 percent in the large-group market) of premiums on medical care and efforts to improve the quality of care, it must refund the portion of the premiums that exceed this limit. Agent’s commissions are included in the administration category which must remain at 20% or below. Commissions should be removed from that category or the percentage increased to allow insurance agent to receive reasonable compensation.

Maintain the health insurance CEO tax cap

The deduction for any health insurance company executive is sharply limited by the ACA, which caps at a maximum of $500,000 the amount of an individual executive's compensation that an insurer could deduct as a business expense. It’s estimated that this generates $400 million in tax revenue (according to recent testimony to the House Ways and Means Committee by Thomas Barthold, chief of staff for the Joint Committee on Taxation).

Technology implementation

Technology will be a long term driver in reducing health care costs by streamlining data, underwriting, dispersing care, reducing fraud, improving wellness and other potential positive outcomes.

This is somewhere that an InsureTech company using Blockchain technology could make a difference. Consumers seem readier to accept digital products than just a few years ago. The field includes mobile apps, telemedicine—health care provided using electronic communications—and predictive analytics (using statistical methods to sift data on outcomes for patients). Other areas are automated diagnoses and wearable sensors to measure things like blood pressure.

58% percent of smartphone users in the U.S. have downloaded a health-related app, and around 41% have more than five health-related apps, generating data that insurance providers could use to fine-tune their individual premium pricing and encourage low-risk customer behavior.

Most of the efforts to integrate technology by insurers are simple and mainly designed as promotions, like awarding credits for a number of steps taken. This is the tip of the iceberg, big data could be used for adaptive premium pricing based on comprehensive health data for each customer. The problem is likely a skepticism toward new technology for which no historical experience is available.

Virtual healthcare

Virtual healthcare includes healthcare services that are technology-enabled and are provided independently of location, such as video encounters with physicians, remote biometric tracking, and mobile apps for health management. According to a study by Accenture, using virtual health care for annual patient visits could save more than $7 billion worth of primary care physician time each year. For more, read:

78% of Americans Support This Revolutionary Healthcare Technology, but Only 21% Have Tried It

Continue Medicaid expansion

Currently 31 states, in addition to the District of Columbia have expanded Medicaid under the ACA. Kansas and North Carolina are in the process of expanding Medicaid while most other states are considering it. Find out

where your State stands on Medicaid expansion.

Medicaid is the

largest insurer with more than 70 million beneficiaries. Medicaid expansion has accounted for over 10 million of those enrollees. It is the main provider of long-term services for seniors and people with disabilities and pays for one-fourth of all mental health and substance abuse treatments. Forty percent of children rely on Medicaid through The Children’s Health Insurance Program (CHIP).

Under the ACA, the program has been opened up to more low-income adults with incomes of up to 138% of the poverty line -- $16,400 for a single person -- in states that opted to expand their Medicaid programs. Under the program, the federal government paid 100% of the costs of the expansion population for the first three years and is slowly lowering the reimbursement rate to 90%.

A July 2015 Government Accountability Office report — which relied on GAO’s past reports, documentation from the Centers for Medicare & Medicaid Services and interviews with CMS officials — also echoed other research: “Medicaid enrollees report access to care that is generally comparable to that of privately insured individuals and better than that of uninsured individuals, but may have greater health care needs and greater difficulty accessing specialty and dental care.” The report mentioned mental health care as a specialty area of concern. However some doctors do not take new Medicaid (or Medicare) patients do to lower reimbursement rates and additional paperwork.

A

study published in JAMA Internal Medicine in 2016, that looked at survey data for three states and found Medicaid expansion “was associated with significantly increased access to primary care,” as well as “fewer skipped medications due to cost,” among other factors.

Adding long-term-care insurance (Medicare Part X):

According to the U.S. Department of Health and Human Services, a person turning 65 today has almost a 70% chance of needing long-term care services at some point in his lifetime. Long term care is a growing need with an aging American population. The individual long term care insurance marketplace has had many struggles with the current marketplace being reduced to just a few insurance companies offering individual long term care insurance policies (this does not include hybrid or combination life/annuity & long term care insurance policies or life insurance with long term care insurance riders).

It is important that long term care insurance be made accessible on a standardized, monitored basis as set forth in the NAIC model regulations. Since the private insurance marketplace has mostly not been successful, this is something that should be considered and made an option under the expanded Balanced Health Insurance Plan.

Medicare does not cover services that include medical and non-medical care provided to people who are unable to perform basis activities of daily living, like dressing or bathing. Long-term supports and services can be provided at home, in the community, in assisted living, or in nursing homes. Individuals may need long-term supports and services at any age. Medicare will pay for skilled nursing services, but it will only cover a maximum of 100 days in a nursing home, and it won't pay at all for home aide services (when a person comes to your house to help you with ADLs and other basic activities). Medicaid will cover such services, but not until you've exhausted all other resources and are essentially broke.

Long term care insurance was included in the original Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010, established a national, voluntary insurance program for purchasing community living services and supports known as the Community Living Assistance Services and Supports program (CLASS Act). The CLASS program was designed to expand options for people who become functionally disabled and require long-term services and supports.

The class plan would have allowed all working adults to enroll directly through voluntary premium contributions or through payroll deductions through their employer or directly. Benefits would have been payable to insured had multiple functional limitations, or cognitive impairments. The plan would have paid a monthly cash benefit that would be used for long term care insurance services (this is an overview).

The goal was to have the plan financed entirely through premiums of participants, however, at that time, the Federal Agency tasked with implementing the CLASS Act was not able to come up with a workable solution that would have had affordable premiums and had a useful benefit structure.

Another goal of the plan was to partially reduce the reliance on Medicaid. CLASS was to be the primary payer for individuals with Medicaid.

Planning and pre-funding long term care insurance needs is now more important than ever. Given the issues with the private long term care insurance market and that the CLASS program was not workable, then it is time for enacting a public-private partnership to make it work. Why can’t a long term care insurance program be set up with a similar public-private partnership as the NFIP (as discussed earlier)?

The Trump administration and Congress must support the ACA as is

House Speaker Paul Ryan stated after the recent defeat of the GOP’s/Trump’s “American Health Care Act” - “Obamacare is the law of the land, it’s going to remain the law of the land until it’s replaced.” Under Article II of the Constitution, the president is responsible for the execution and enforcement of the laws created by Congress. Therefore whether Trump likes or doesn’t like the ACA, which is his prerogative, he has a responsibility to all American citizens to support it.

The Trump administration therefore needs to act in good faith on the ACA. Unfortunately, The Trump administration pulled the plug on all ACA outreach and advertising in the crucial final days of the 2017 enrollment season. Individuals could still sign up for ACA plans, however, the administration stopped advertising that fact. This included halting all emails sent out to individuals who visited HealthCare.gov, the enrollment website, to encourage them to finish signing up. Those emails had proven highly successful in getting stragglers to complete enrollment before the deadline.

By taking these actions and threatening to take other steps to handicap the ACA, Mr. Trump is not fulfilling his constitutional duties to support something that is already law. As people, we’re faced all day in dealing with situations we don’t always like even if that includes eating our vegetables.

Members of Congress and the Senate must participate in the same way as everyone else:

Everyone needs to play fair. Documents obtained under the Freedom of Information Act show that unnamed officials who administer benefits for Congress made clearly false statements when they originally applied to have the House and Senate participate in D.C.’s “SHOP” Exchange for 2014. Notably, they claimed the 435-member House had only 45 members and 45 staffers, while the 100-member Senate had only 45 employees total.

The Federal Employees Health Benefits Program gives federal employees a choice of health plans and pays up to $12,000 of the premium. But the ACA kicked members of Congress and congressional staff out of the FEHBP, and said the only way they can get health benefits is through an Exchange.

The ACA bars businesses with more than 100 employees from participating in SHOP Exchanges. Until this year, D.C. barred businesses with more than 50 employees. By claiming that the House and Senate fit under those limits, they were able to draw money from the federal Treasury—i.e., a subsidy of up to $12,000 for each member and staffer.

In addition besides being another perk for the wealthy (which most members of Congress and the Senate are) is that it potentially violates multiple laws. Read more:

On ObamaCare, is there one set of rules for Congress and another for citizens?

See also: The Basic Problem for Health Insurance

What is the bottom line on the numbers discussed in this article?

Current total health care costs: healthcare expenditures were projected to reach $3.2 trillion (yes, trillion) in 2015 - or about $10,000 per person (Centers for Medicare & Medicaid Services, 2015).

- Legitimate pricing: savings of 33% - $1 trillion

- Terminating employer health insurance: Excluding premiums from taxes was worth about $250 billion in forgone tax revenue in 2013,

- Fraud: health care fraud costs the nation about $68 billion annually with other estimates ranging as high as 10% of annual health care expenditure, or $320 billion

- Virtual Health Care: $7 billion

- Medicare Advantage overspending on inflated risk scores - $10 billion plus annually (Government Accountability Office).

- Maintain the health insurance CEO tax cap: estimated $400 million in tax revenue (according to recent testimony to the House Ways and Means Committee by Thomas Barthold, chief of staff for the Joint Committee on Taxation).

- Reviewing Medicare coding errors: $20 billion per year.

- Cutting Tax Evasion: if all taxpayers were to report their income and pay their taxes in full, the average household would “earn” $4,276 to $8,526 based on the more likely to occur historical evasion trends - which is almost as much as spent per person each year on health care.

By simply adding legitimate pricing alone, there were would be no issue on health care funding. It’s simply a matter of implementing the principles of The Insurance Bill of Rights.

The bottom line

This will work because so much of this is already in place and a lot of the rest would be quick and easy to implement. As in all areas, knowledge is power. Consumers can take control of your insurance portfolio by becoming educated about insurance. Better education and understanding will lead to positive results for consumers and for the insurance industry. If a consumer purchases the right insurance coverage, they will meet their needs and the insurance industry will benefit from satisfied customers. Review

The Insurance Bill of Rights and make sure that you understand how it applies as a consumer and a member of the insurance industry.

I