The insurance industry is in the midst of a crisis as bad as the Great Recession and possibly worse than the Great Depression.

The crisis worsens each day because of the COVID-19 pandemic.

We do not know when the worst will end.

We cannot predict when the pandemic itself will end.

But we can choose what we say and do; what we must say and do for the good of the insurance industry and the economy as a whole.

We must choose to lead.

The choice is just that: a choice to fight fear with facts, because the insurance industry must not let fear be the face of the pandemic. Not when the faces of the heroes among us cover their faces, but show us their eyes.

Their eyes say many things.

Their eyes speak to feelings of loss, depression, doubt and frustration. Their eyes also speak of the resolve to continue.

“The insurance industry must be a voice of clarity and wisdom. People need to hear from experts and executives they trust. Communication is essential to success.”

Albanese is right about trust. Insurers need it, customers demand it and the public deserves it. Which means the insurance industry must work to preserve and protect it.

The industry must convey what it believes and be true to its most fundamental belief, that trust is the basis for everything a business does.

Acts strengthens trust. Put another way, good works are more effective than good words. The works speak for themselves—up to a point.

The moment comes when insurers must speak about their works. The moment is right—now is the moment—for insurers to lead by speaking to the public, about the needs of the public, for the safety of the public.

Each day is a new moment for insurers to offer news, answer questions and address the public. Whether insurers use traditional media or social media to communicate is less important than what they deem to be of importance.

The medium is not the message; the message is the message, regardless if it is a post, a comment, a column or a tweet. Substance comes before style, especially during a pandemic.

The substance of what insurers say should be direct, just as the information they provide—the directions they give—should be correct.

Does this mean insurers must be perfect, that they cannot afford to make mistakes?

On the contrary, mistakes are inevitable, and misstatements are unavoidable. Admitting one’s mistakes is, however, critical to maintaining what too many companies do not enjoy in the first place: trust.

The insurance industry has a chance to personalize its mission and humanize its spirit.

Potential business disruptions are part of a company’s regular continuity plan. Still, few were prepared for the impact of a global pandemic that has shut down businesses around the world. Many companies have faced challenging decisions like laying off or furloughing employees for an extended period, while others have had to shift to a fully remote workforce quickly.

Four leading CEOs in our industry joined us for our special edition Out Front Ideas COVID-19 Briefing Webinar Series to discuss the challenges their businesses are facing and how they are adapting:

Keith Newton – CEO of Concentra

Dave North – CEO of Sedgwick

Tom Warsop – CEO of One Call

Mark Wilhelm – CEO of Safety National

The Carrier Perspective

The insurance companies are facing an onslaught of regulators seeking a myriad of information. Carriers are inundated with data requests, receiving hundreds of bulletins and directives covering most territories, states and Canada. Some states have issued moratoriums on cancellations for non-payments of premiums, while others have requested that carriers make it clear to the public how they will treat premium leniency. Carriers are being asked to provide a COVID-19 readiness plan, including the impact on the business, both operationally and the impact on investment income. The National Association of Insurance Commissioners (NAIC) has stepped in, asking states to pause on data requests, so carriers can focus on servicing their insureds.

Regulators and legislators are seeking to expand the compensability of claims beyond what was planned during the underwriting and pricing phases. Many legistlators are passing laws stating that COVID-19 claims are presumptions, especially for healthcare workers and first responders, meaning it is presumed they contracted the virus while on the job and it should be covered accordingly. Some states are even looking to expand this to all essential workers.

As far as the financial impact on carriers, there are a few items to consider. Carriers could see a decrease in premiums due to employer payrolls decreasing. There are also credit risks due to non-payments on premiums, and there may be portfolio devaluations in the future due to lowered interest rates. However, with specific industries, like healthcare, seeing more claims, many sectors will see a decrease in claims because of shelter-in-place enforcements.

The Third-Party Administrator (TPA) Perspective

Initially, TPAs saw a surge in paid leaves in the U.S., but that has now shifted to unpaid leaves because of the programs that employers have in place. With federal programs, like paid leave extensions, being evaluated, we do not yet know the direct impact they will have on injured workers. It may mean shifting an injured worker off workers’ compensation and on to one of those programs in the future if it is more beneficial.

Many employers are reaching out for planning for a future catastrophe. For example, if a natural disaster like a hurricane or tornado occurred during this time (a “cat” within a “cat”), employers want to know that their business would have a continuity plan in place. Everyone is considering the “what-if” scenarios right now, so many are overly preparing for the next big event.

In the workers’ compensation industry, there has been a drastic decrease in the number of new claims due to some businesses shutting down completely. However, some industries are growing significantly in the current state of the economy, which is noticeable with a more-diversified customer base. Pending claims in workers’ compensation have not seen the same drastic decrease, meaning the injured workers who received our attention before COVID-19 still need assistance, but now are less likely to obtain the care they need. Some patients have no idea how the change will affect their recovery or return to work.

Due to the pent-up demand for healthcare during the COVID-19 crisis, there will be a backlog of post-pandemic patient needs. This demand may put injured workers at a disadvantage because elective surgeries will not be prioritized above other significant needs like trauma surgeries. Actuaries will have to learn how to adjust to this uncontrollable shift. For example, will a lack of litigation be considered a trend, or will litigation rebound based on the high consumption of healthcare upon a return to normalcy?

There is a balance right now of taking care of the injured workers’ needs and also maintaining communication with them. As a workforce, all partners should be ready to embrace the injured workers when the industry returns to normal, readying resources and preparing to handle the increase of needs.

The Ancillary Program Provider Perspective

The most considerable impact has been an unwillingness for injured workers to get the treatment they need because of COVID-19 risks. Because patients do not want to come into contact with others, the frequency of demand is affected and delays their care. Provider access has also seen an impact. While most are still accessible, industries like dentistry have been advised not to continue treatment. The extension of telehealth has also made accessibility to care much better.

Referrals for ancillary services have decreased significantly. Specifically, transportation service requests are suffering, but well-established services like home health do not see the same drop in requests. Some ancillary program providers are seeing furloughs of their workforce due to a decline in demand. Some companies are providing advanced paid time off and healthcare coverage for furloughed employees.

Expect new operating models to emerge from this crisis. There will most likely be a significant increase in remote work employees, now that work from home opportunities have proven to be an adaptable method. The issues surrounding telemedicine use will likely not disappear after this crisis, now that there is a sustained demand for it. Rescheduling technology will also change due to the current number of requests. Shifting to a text-based rescheduling program has seen a much higher response rate from injured employees due to its ease of use, potentially guaranteeing future care for those who cannot currently access it.

The Occupational Health Provider Perspective

Because the occupational health workforce is patient-facing, at occupational medicine centers, employer worksites and primary care facilities, the industry is facing many challenges. These challenges include regulatory directives, limited personal protective equipment (PPE) for front-line healthcare providers and a significant drop in patient volume. However, the industry has dealt with a substantial reduction in patient volume before. During the 2008 recession, there was a significant decrease, but demand rebounded over the months following.

Opportunities have developed from the crisis, including testing assistance and telehealth expansion. While limitations on PPE do not allow for occupational health employees to run testing for COVID-19, they are instead managing fit tests for the frontline providers, like those working the drive-through testing sites, to make sure their gear fits properly. Telehealth has provided an incredible opportunity for occupational health providers to expand their services for injured workers. Many providers that were not interested before have now been working quickly through an approval process, so their patients can receive the care they need. However, most occupational health practices are still open for business, but, to reduce exposure, they have reduced hours and staff in facilities.

While most of the industries within workers’ compensation had the ability to move to a fully remote workforce, declines in patient volume and referrals have forced some to furlough employees until there is a rebound. This crisis has forced all our CEOs to use disaster task forces within their organizations and learn how to readily adapt to changes in their businesses, both financially and operationally. COVID-19 will certainly breed many advances in patient care and opportunities for growth in the workers’ compensation industry, as all of our CEOs are continuously learning from the experiences this has created.

To listen to the full Out Front Ideas with Kimberly and Mark webinar on this topic, click here. Stay tuned for more from the Out Front Ideas COVID-19 Briefing Webinar Series, every Tuesday in April. View the full list of coming topics here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.

Kimberly George is a senior vice president, senior healthcare adviser at Sedgwick. She will explore and work to improve Sedgwick’s understanding of how healthcare reform affects its business models and product and service offerings.

No longer exclusive to healthcare, regularly disinfecting surfaces has become a way of doing business during COVID-19. For essential services, it represents a commitment to both workforce and customers alike. It is important to note that, much like any chemical, disinfectants come with risks, and those risks compound with increased use. Here are some important safety tips to follow while using disinfectants.

1. Choose a disinfectant from the EPA’s List N: Disinfectants for use against SARS-CoV-2.

The EPA has tested List N disinfectants to meet two criteria. First, disinfectants must show efficacy against harder-to-kill pathogens and coronaviruses similar to SARs-CoV-2 (the cause of COVID-19). Second, they must qualify for the emerging viral pathogens claim. The EPA can certify select disinfectants for use against novel pathogens after having cleared a two-stage review. View the EPA’s full List N here.

Mixing disinfectants does not improve their performance or make them intrinsically safer. In fact, these mixtures can often result in conditions that are immediately dangerous to life and health for both workforce and customers. For instance, mixing bleach with other common disinfectants, such as quaternary ammonium (quat) or cleaning acids (citric or peroxyacetic), can generate toxic chlorine or chloramine gases. Hydrogen peroxide and bleach mixtures can result in explosion, if near an ignition source. Allow a bleach-cleaned surface time to completely dry before using another disinfectant or cleaning agent.

3. Disinfect electronics using 70% isopropyl alcohol (IPA) wipes.

Regularly disinfect high-touch electronics surfaces such as touch screens, phones, ATMs, keyboards and remotes. IPA safely disinfects these devices without compromising oleophobic coatings or damaging circuitry.

4. Barring allergies, use disposable nitrile gloves over latex or vinyl when disinfecting.

Nitrile gloves tend to be more chemically resistant and tend to result in fewer allergic sensitivities.

5. Discourage workers from “watering down” or “topping off” disinfectant bottles to stretch supply.

These practices can drastically reduce the efficacy of disinfectants and introduce the risk of mixing incompatible chemicals.

There is no end in sight for this increased disinfectant use, so it is important to communicate these safety tips clearly to your entire workforce. Create an integrated approach with all unit managers to help incorporate these safety measures and enforce them throughout the organization. Risk management is, ultimately, everybody’s job.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Vikrum Ramaswamy is a senior risk control manager at Safety National. He is responsible for managing risk control services for policyholders written out of the Pacific Northwest, Northern California and Southeast territories.

Of late, cloud computing adoption has gained such traction enterprise-wise that it is rightly called the new normal. The 2019 State of the Cloud report by RightScale shows that 94% of organizations use cloud, shifting their corporate workload there. High costs are for now the greatest concern for cloud adopters, but organizations work on tackling it, either on their own or with the help of Google, Microsoft or AWS consulting specialists.

Despite being welcomed by most, cloud computing is still associated with plenty of complications and threats that haunt adopters and skeptics alike. As a result of persisting misconceptions, some enterprises adapt ill-suited cloud policies and practices, while others abandon cloud migration at early stages or steer clear of it altogether.

This article will take a closer look at the top five cloud software risks and examine the ways enterprise decision-makers can contain and manage them.

Data security loopholes

Security concerns are the main reason why cloud computing becomes a no-go option for some companies. This consideration particularly inhibits industries handling sensitive customer data: Banks, medical facilities and such can’t afford a single data breach and therefore by default opt for on-premises software.

But these fears are exaggerated. The strength of security boils down to the measure introduced into a corporate environment. Cloud security provisions indeed differ from on-premises ones, but, when enforced correctly, they render the system impregnable.

At the same time, the cloud beats on-premises systems when it comes to compliance with data privacy and security regulations. Since cloud solutions must adhere to every legislative change, the vendors make the effort to update their software timely. On-premises security measures, on the other hand, are taken by each enterprise individually and may be insufficient or timed poorly. Therefore, cloud software can facilitate full compliance for businesses required to follow the GDPR, HIPAA and other regulations.

The prohibitive cost of ownership

Enterprises tend to adopt cloud computing to optimize costs but do not necessarily achieve the desired results. Cloud software is commonly known as a cheaper option because the adopter does not incur implementation, maintenance and security costs. In reality, hidden incremental costs do pile up.

So, how to estimate whether a cloud solution will indeed be cost-effective?

First off, the responsible parties should factor in the enterprise expansion in the foreseeable future. Because SaaS, PaaS and IaaS licenses directly depend on the number of users, the workforce growth will force subscription prices upward.

Availability of IT resources is another significant part of the equation. When the company employs a full-time development and support team, then the maintenance of on-premises software should not become a large cost component. If this is not the case, cloud software is a more reasonable option. An outsourced cloud-savvy team can easily cover the demands of initial customization and occasional support, while the updates and patches will be the cloud vendor’s responsibility entirely.

The final consideration is the time gap between the project kickoff and the moment the software starts bringing value. For companies looking for quick ROI, cloud solutions offer a much shorter time to market compared with traditional on-premises setups.

Software discontinuation

Another of cloud adopters’ fears is that a vendor may all of a sudden go out of business, taking along the product. The possibility of software discontinuation indeed exists, but this is not as common an occurrence as one may think. Oftentimes, companies abandon the software, either cloud-based or on-premises, that grew outdated in the modern technological context and therefore ceased to be valuable to its users. In this case, the customers are alerted well in advance and given enough time to find a substitute.

To mitigate the risks of possible cloud platform shutdown, companies need to take precautions against vendor lock-in and associated disruptions:

Map out an exit strategy before subscribing to a cloud-based product.

Study the contract carefully to clearly understand vendor obligations.

Maintain data in easily exportable formats.

Management complexity

Hybrid and multi-cloud environments are notorious for bringing confusion into the enterprise setting. As companies take more and more of their workload to the cloud, they sooner or later find themselves unable to fully govern the spiraling infrastructure and ensure its security. This can result in the failure to realize the full potential of the infrastructure, as well as in performance botches, security lags and above-budget spending.

However, proper planning undertaken way ahead of multi-cloud adoption can greatly mitigate such downsides. Starting from the solution architecture and network topology to interoperability mechanics, the environment should be laid out by experts.

Apart from this, a cloud management platform can provide better visibility across multiple accounts, along with cost and security control.

Weak connection and network failure

Ironically, the very thing that makes the cloud possible — internet connection — causes most problems in a cloud environment. Cloud outages strike enterprises large and small and cause data and money losses — in 15% of cases, over $5 million per hour of server downtime. These connectivity issues have a particularly damaging impact on hybrid cloud adopters, which rely on unhindered connectivity for unlimited data transmission between different cloud platforms and enterprise data centers.

Despite being such a thorny aspect, internet connection still has the status of a no-man’s land. On decision-makers’ side, connection tends to be overshadowed by other seemingly more pressing matters such as security, compliance or interoperability. What is more, there is still no consensus about who should take full responsibility for cloud outages—the owner or the service provider. While 65% of businesses rely on cloud software providers for recovery and continuity, according to the Forbes Insights and IBM survey, less than half of them have confidence that vendors would meet their SLAs in case of emergency.

In reality, both the business and the vendor should be accountable for network connection and data recovery. While the latter has its side of the bargain to deliver on, enterprises might well take a more aggressive stance on cloud uptime provision and immediate network recovery. Thus, employing a single network manager to provide for connectivity now can spare you from hiring a whole emergency support team later.

Challenges, not risks

Cloud computing is a very young technology that is as attractive to potential adopters as it is intimidating. However, when examined closely, cloud-related risks are reduced to surmountable challenges.

For each of the “risky” aspects — security, cost of ownership, vendor lock-in, management difficulties and connectivity maintenance — the maturing industry is coming up with appropriate solutions. Cloud service providers also recognize the imperatives and fears of today’s enterprises and work to bridge the existing gaps, be it GDPR-compliant data processing or direct connectivity in hybrid clouds. Therefore, one may expect cloud software to become a more sustainable and safer option for enterprises in all verticals.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Andrey Koptelov is an innovation analyst at Itransition, a custom software development company. With profound experience in IT, he writes about new disruptive technologies and innovations in artificial intelligence and machine learning.

The insurance industry relies heavily on catastrophe modeling to set capital adequacy, adhere and respond to evolving regulatory requirements and stress test portfolios. The same is now increasingly true of the cyber catastrophe sphere, in which key areas of focus include how models can help with capital allocation, stress testing and informing development of underwriting guidelines and insurance products. Parallels can be drawn from the cyber catastrophe and natural catastrophe risk management sectors when modeling these risks.

The introduction of models provided critical insight into the potential for catastrophic claims for all risk policies or policies without clear exclusionary language. Historical events such as the April 1906 San Francisco earthquake (leading to unanticipated claims for fire policies), 2005 Hurricane Katrina flooding (resulting in unanticipated claims for homeowners wind policies) or the 9/11 U.S. terrorist attacks (experiencing unanticipated war exclusion interpretation and definition of a single event), and the current unfolding of the coronavirus pandemic crisis highlight the criticality of understanding the triggers and correlation of potential loss due to a single event.

In many cases, insurers paid losses to avert “reputational risk” and have since used models to provide insight into realistic structuring of policy, reinsurance and other risk transfer vehicles. Clear exclusionary language, endorsements and coverage-specific terms evolved over the decades in concert with evolving scientific knowledge of the risks and modeled loss potential.

Today, we are seeing the same evolution with respect to insuring cyber risk, but over a highly compressed period, without the decades of experience of systemic insured loss events. Many cyber catastrophe risk managers attempt to apply the same lens of current natural catastrophe model availability of data resolution, data quality, catastrophic event knowledge and model validation expectations. But by embracing the commonality of lessons learned from the evolution of the property catastrophe insurance market, we can prepare for an event considered to be a case of not “if” but “when.”

The role of data in models

A first common theme is to recognize that the understanding and availability of information for a rapidly evolving risk means that there is value in aggregate data in the absence of detailed data. This has been and is still the case for property catastrophes and is also the case for cyber catastrophe risk models. Confidentiality obligations in portfolio data as well as the lack of high-quality data is an issue for all models. However, new sources of data as well as sophisticated data science and artificial intelligence analytics are being incorporated into models that provide an increased confidence in assessing the potential risk to an individual company or entity.

A second related common theme is the ability of catastrophe risk models to augment lack of risk-specific data capture at the time of underwriting. This is where all catastrophe risk models add significant value, where context for what should be captured as well as what can be captured is provided. In the case of cyber, this can include access to both inside-out (behind the firewall) and outside-in (outside the firewall) data. Inside-out data refers to aggregate data for segments of the economy, measuring the anonymized trends of security behaviors (such as frequency of software patching). Outside-in data is made up of specific signals that can be identified from outside an organization and that give indications of overall cybersecurity maturity (such as the use of unsupported end-of-life products).

A third commonality is the value in extrapolating the impact of past events into the future given evolving available data on the changing causes of frequency and severity of cyber events. The property catastrophe arena is grappling with very similar issues relative to the rapid and uncertain evolution of climate models. For cyber risks, history is not a predictor of the future in terms of modeling threat actors, the methods they deploy and the vulnerabilities they exploit. However, it is possible to examine historic data and the types of cyber incidents that have occurred while addressing the challenges in the way that information is collected, curated and used. This historic data is used against the backdrop of a near-term threat actor and technological trends to understand future potential systemic losses due to large-scale attacks on bigger and more interconnected entities.

The role of probabilistic models

At the enterprise level, the market is struggling with how to assess potential aggregations within and across business lines. Event clash due to a single event causing multiple loss triggers to policies and reinsurance treaties is a key concern across all lines of business. Use of common cyber and other catastrophe risk loss metrics that can be combined across perils and lines of business are being explored. In addition, regulatory groups are considering requirements similar to property catastrophe risk to address solvency requirements relative to cyber risk.

In this environment, consistent and structured definitions of risk measures are critical for assessing and communicating potential systemic catastrophic loss. Both deterministic cyber scenario event analyses as well as probabilistic stochastic cyber event analyses are required. Given this context, cyber catastrophe risk models that can withstand validation scrutiny similar to property catastrophe risk models require the same level of rigorous attention to transparency in communication of model methodology.

Similarities… but some differences

There are some key differences between the systemic risks of natural disasters and cyber events. One material contrast is that cyber perils manifest with active adversaries seeking to cause malicious damage to individuals and companies globally. The factors affecting modeling include the changing nature of geopolitical threats, the dramatic increase in the use of digital means for criminal enterprises, the hyperconnectivity of developed economies and an ever-increasing reliance on networked technologies. Cyber event scenarios are developed to represent a range of potential systemic events in which technological dependencies affect individual insured companies, due to a common vulnerability or a “single point of failure.” Examples include common cloud service providers, payment systems, mobile phone networks, operating systems and other connected technologies.

There are limitations in any model relating to cyber risk, given the inherent uncertainties. Nevertheless, these models provide valuable insights to better decision-making relating to capital planning, reinsurance and addressing regulatory issues. By learning from previous insurance shocks, we can support a more stable and resilient cyber risk insurance market.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Laurel Di Silvestro is principal client services manager at CyberCube. She is responsible for managing successful client adoption of a suite of CyberCube probabilistic cyber catastrophe risk management models and data products.

The last several months have shown the fragile and connected nature of our global economy. If four months ago you would have told someone that we would be in a situation with record global unemployment, historic government economic stimulus, people sheltering in place, all occurring in less than six weeks, you would have been met with disbelief and disdain. Our bitter reality, however, is that the changes that we have experienced in the last 60 days will continue and will accelerate the impact and consequences for the future.

In many ways, we have been contemplating our current situation for years, as evidenced by the numerous models, books and films that have all described a “post-apocalyptic” world that fundamentally changes society. The previous contemplations were like an amusement park roller coaster experience, fun to momentarily experience the fear and uncertainty, but then easy to return to solid ground when the ride was over. The primary issue is that the entire world is now on the roller coaster and desperately wants to get off but has to wait for the ride to end.

Several authors who focused on historical crises and their long-term impact see common patterns. The crises create fundamental shifts in society, business and culture. The Covid-19 situation will inevitably lead to some of the greatest changes we have seen in the last 100 years.

One of the primary factors underlying our future “new normal” is the steady march to more detailed and prevalent public information about people and their physical state. We have been moving down this path for many years through the ubiquitous sharing of data in both social and business settings. Facebook, Twitter, Instagram and a slew of other software is primarily designed to be a data sharing platform. The virtual sharing of data is done literally by everyone, regardless of age, gender, race or socioeconomic status. In our post-pandemic world, data that describes our health and physical state will become more valuable than currency.

Narrowing this data focus on the worker, the new normal will be greatly different than what we left behind just 90 days ago. First, and most importantly, worker health and safety will be monitored and evaluated more than ever from a strategic, operational and financial perspective.

Strategically, companies will need to rethink worker roles, locations, supply chain and output models. The work from home shift for a majority of historically white collar industries occurred in a matter of hours. Our networking infrastructure, software and excess home working space were quickly converted into a new working model. Moving forward, this more fluid work model will continue with an inevitable reduction in physical office space and the ability to work within different environments. Company campuses will become virtual; physical location will be secondary; interaction will be through a digital camera and microphone. The consequences of this shift are still developing and will change the office working model.

For those blue collar workers where the worker’s body is the means of production, there will also be fundamental shifts. Tracking of worker-specific data and location will become commonplace. Prior to the “new normal,” we saw regulation and case law about the use of biometric data and limitations based on privacy concerns. The new normal, however, will require that people expose specific biometric data (temperature, antibodies) to ensure that workers are not creating or accepting undue risk. Access to locations will be based on a physical and biometric review of workers and will inevitably extend to clients, customers, vendors and any others within company locations. A driver's license and other forms of ID will now include your health card and current physical state.

On the foundation of this additional information, the speed of risk identification will become a primary metric, and the ability to respond will become a determination of operational and management efficacy. The experience with cyber-attacks provide a good parallel. An organizational leader’s responsibility is to take reasonable and rapid efforts to protect the organization and its assets from cyberattacks. We have seen large D&O cases brought for the failure to meet these reasonable standards. A similar effect will occur with infectious diseases, related to how to mitigate and avoid the risk across an organization. The organization's need for identification and response will be measured in minutes.

In 12 months, the only accurate statement is that the world will be a much different place than today. The “new normal” will include the use of people’s personal health and biometric scanning. Temperature scanners will be implemented for access to locations including work, school and entertainment. Our personal data tracking and sharing will take on greater importance, to show the employers, public entities, schools and others our current state of health and ability to safely interact with others.

Technology and data are, and will continue to be, the primary driver of this awareness for our health and safety. As more people are willing or required to share data for the collective safety in the connected world, our privacy standards will evolve.

The direction is clear. Data creates insight, insight creates action and action avoids risk.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Doug Turk is a recognized innovator and leader with extensive experience in starting, growing and managing organizations. His career spans over 20 years in both technology and insurance.

Not that long ago, people didn’t have information at their fingertips, and businesses were successful in using outbound sales and marketing methods such as cold calling and email blasts to close sales.

Today, the buyer’s journey has changed thanks to the Internet of Things (IoT) and other advancements in technology. Now, 57% of the purchase journey is completed before a customer has contacted a business (according to CEB), and 67% of the buyer’s journey is done digitally (SiriusDecisions).

The rise of social media has encouraged organizations to look into ways that they can use the technology, which has led to the development of social selling.

What are the benefits that social selling offers?

1. It appeals to the modern buyer

B2B buyers have 12 to 18 non-human and human interactions along their buyer’s journey (Sirius Decisions), and 68% of buyers prefer to research products and services online (Forrester). It’s essential that you develop and push information and content on social channels that resonate with your target audience and provide the solution to their problems.

This will enable you to influence their choices and position your business as front of mind.

2. It allows you to build “real” relationships

How many cold calls do you actually answer, listen to and respond to?

It’s time for businesses to break down the barriers around selling and get on the same page as their customers. Social selling supports this as, through social media listening tools, you’re able to listen to topics and conversations that are relevant to the insurance and risk management industry.

Added to this, a survey from IBM revealed that only 43% of consumers trust the insurance industry, and the lack of trust in insurance providers has remained above 50% since 2007. Social selling helps you build trust among your audiences by giving you insight into what’s important to your prospects and presenting new opportunities and leads.

3. Your competitors are already using social selling

71% of all sales professionals are already using social selling tools, so if you aren’t you may be putting yourself at a disadvantage (LinkedIn). A report by ITDS revealed that 100% of insurance firms are active on LinkedIn.

According to a study by Capgemini, 22% of insurance policyholders cite social media conversations and interactions as having the highest impact on their purchasing processes. This ranks above the influence of the advice of friends and family, which only 17% of policyholders indicated as most important.

4. The Mere Exposure Effect

The Mere Exposure Effect was first spoken about in 1968 by social psychologist Robert Zajonc. This social phenomenon states that the more a person is exposed to something, the more the person will develop a preference toward that thing over time.

Social media lets businesses tap into this theory through regular and consistent posting and updates. When you’ve created and put into action a dedicated strategy, you can begin to use social media channels to your advantage and ensure that you have messages trickling through all the channels that your audiences use, creating multiple touch points with them.

If you fail to prepare, you are preparing to fail…

To successfully leverage social selling, you need to optimize your social channels to showcase your expertise. For example, research from LinkedIn revealed that members with a photo receive 21X more profile views and nine times more connection requests compared with those that don’t.

So, what do you need to do to give a positive first impression on your social channels?

Here are my top tips:

Post a professional head and shoulders image of yourself

Write your bio/summary to highlight your expertise and what you do on a professional level

Include links to your website and other social channels to encourage visits

Use hashtags that your prospects follow

Create lists on Twitter to monitor content from specific accounts

On LinkedIn, include your job title and keywords in your headline, ask for recommendations to boost your credibility and join LinkedIn groups that are relevant to your industry and begin networking in them

Social selling best practices

Once your profiles are ready to be rolled out, it’s time to kick off your social selling strategy.

Dedicate yourself

Start by creating a plan and setting aside time to dedicate yourself to building your social presence. Being present on multiple social channels can be time-consuming, but if you spend 30 minutes every day monitoring your channels, engaging with others and posting content it’ll help ease the pressures and ensure your feeds are always up to date.

Create and stick to a content plan

The purpose of a content plan is to create meaningful, cohesive, engaging and sustainable content that engages, resonates and attracts your target audience. In today’s social web environment, getting the right message to the right customer at the right time is crucial. To stay front of mind, build rapport and trust and position yourself as an expert, you’ll need to have a solid content plan in place.

Take advantage of social listening

Create and use social lists and monitoring streams to collate what people are saying about you, your company, your industry and competitors, and identify what questions they’re asking and topics they are talking about.

Maintain relationships once you’ve created them

Once you’ve made connections, it’s important to stay engaged with them. So, comment on and like the content that is posted by your prospects.

Be sure to offer advice and guidance to them and contribute to their conversations in a meaningful way if they ask questions.

Share testimonials

Success stories from other customers have a lot of weight, and research from Pretty Links suggests 92% of buyers trust recommendations from peers, and 70% trust recommendations from strangers.

By gaining and sharing third-party testimonials, you’ll start to build your credibility with prospects, and it’s more likely that they’ll begin to trust your business.

Tracking metrics such as likes, comments and shares will allow you to identify the types of content that resonates the most with your audience. And, it’ll enable you to determine if your social selling activities are paying off.

Understand when to take your connections offline

To land a sale, you’ll need to escalate the connection with a prospect by offering a call to continue the conversation offline and on a deeper level. It’s important not to push a call before prospects are ready.

Research revealed that the dollar value of the opportunities for insurance companies to drive results through social media is over $15 million a month (Marketing Tech).

Get Involved

Our authors are what set Insurance Thought Leadership apart.

There has been a radical change taking place in insurance over the past few years. It revolves around the race to zero – or, the concept of streamlining the end user experience to ask less and less information when it comes time to file and process claims.

Regardless of what stage of the digital transformation journey the industry has been in, meeting and exceeding customer expectations has always been a priority – as has been the journey to find smarter ways to do business. Without either of these things, not many organizations would be successful.

Asking less and less from consumers is not necessarily a new concept – but that doesn’t mean that it isn’t more important than ever in 2020.

In 2020, not only is the race to zero more possible than ever (thanks to improvements in software-as-a-service (SaaS), digital technologies and data ecosystems), it’s becoming an expectation.

This is largely being driven by two things: new generations of digitally native consumers who are used to seamless data integrations and information access across every aspect of their lives; and organizations looking for ways to evolve their processes to work smarter and more efficiently to meet these expectations while also remaining profitable.

Whether every line of insurance or business type can get to these hypothetical zero inputs is irrelevant. What’s important is that the new world of SaaS-based solutions, and a transformation to data-driven ecosystems living in the cloud, are changing the insurance game at speeds we’ve not experienced before.

Whatever that limit is, here are a few ways that any organization can realize its potential:

Enable Continuing Improvements With SaaS

It was really only five years ago that we started seeing early adopters embrace SaaS – and only in the last year or so that there’s been a drastic change wherein the majority are heading toward that model. One of the chief reasons for this is the configurability and malleability of new SaaS systems compared with legacy systems.

Insurance is driven by data; however, in the past, as insurers would get new data feeds, it was difficult to take advantage of them in a timely fashion – because existing systems and processes were so locked in. Now, with modern SaaS systems, it’s much easier to make changes to processes, workflows and rules, so that as new types of data and analytics tools become available you can use them to your advantage – and to the advantage of insureds.

Data is golden – but pouring new data into an old process often doesn’t get you where you need to go or get your processes any closer to the hypothetical zero. Instead, we must be thinking about new data sets in new ways and imagining how they can actually affect or drive a new process.

This is no easy feat, and what we’ve seen some carriers do (innovate while understanding the legacy processes within existing organizations) is start companies or build new insurance products. This freedom to innovate, while keeping data outside existing core systems, means the data’s value isn’t limited in a legacy environment where it’s easy to get bogged down.

This sort of innovation remains one of the more interesting recent developments – and will continue to evolve as insurers look to create data-driven products that change the way insureds engage with insurers. The market has reacted to enable this evolution with highly customizable, out-of-the-box SaaS solutions built around configurability and speed.

Think Agility

When it comes to meeting this hypothetical zero in a new data-driven world, we must also consider IT processes – and the agility that’s required to move to market at speed. Things used to take a long time (new products released on an annual or multi-year basis, for example). However, with new, low-code core systems, insurers can be very agile about when and how products are released – and the types of data sources or third-party integrations that can be leveraged in a way that makes a competitive difference in the market.

This can be a challenge for IT departments that aren’t used to working in this fashion, so the mindset truly needs to shift toward “agility.” This goes for updates too. If there are opportunities to prefill through partnerships and integrations, or feed in new data sets, insurers leveraging new systems and processes can easily modify an app or existing product.

Use Data to Make Better Decisions

We’ve talked a lot about how to be agile and think about new ways to access data and information – and reimagine your processes around it. But, once you have that information, there’s another half of the equation you must consider – can I make better decisions and use the right information and tools, such as analytics or scores, to route things appropriately and for easy cases?

From the front end, if I’m using data prefill and getting better data that I might have from older forms, for example, how can this contribute to making better, more informed and faster decisions in the insurance process? Taking this a step further, during times of strain or circumstances where losses pile up, can my organization find opportunities to use data and prefill to offer straight-through processing and enable our workforce to focus its efforts on the more difficult and nuanced cases that require a very hands-on, tailored approach?

If the outcome isn’t better decisions, the value of more data often isn’t realized.

A final point worth noting is the transition to a more open, API-based ecosystem in insurance. Traditionally, the industry has been highly closed off, but we’re seeing more and more negotiations around how to access and build around APIs. With this transition to “openness” (along with a shift in mindset for the entire industry), innovation can take strides, and the race to zero for both insureds and insurers becomes more of a reality.

The core value of insurance will still be worth its weight in gold, but imagine the types of solutions we can develop with an abundance of new information, new processes and new technologies in place.

For anyone in the insurance industry reading this, how do you not get excited about the possibilities in front of us? A new world of opportunity awaits in the race to zero – both in terms of how we reimagine products and policies for consumers and how we operate and process internally.

For those of you not involved in this data-driven insurance technology ecosystem – what are you waiting for?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jeff Wargin leads development of Duck Creek’s industry-leading solutions, responsible for strategy, direction, planning and road mapping. Wargin has spent 20-plus years in the P&C insurance software market.

Why to Prepare to 'Reverse Innovate'

As the pandemic accelerates the insurance industry's digitization, peeks into the future are available--but not where most of us usually look.

The best car-buying experience that I--or pretty much anyone--ever had came 20 years ago. With two young daughters and, thus, soccer car pools looming, my wife and I decided we needed a big, old SUV, and we just happened to have a good friend and neighbor who owned a car dealership that sold them. Mark steered us toward the Yukon XL and, a few nights later, dropped a demo version off in our driveway. We liked it. We picked a color and a few features, and he ordered our car. A few weeks later, he drove that to us, too. We opened a bottle of wine and, in leisurely fashion, signed all the documents, wrote a check and took possession.

Fast forward to today, and, as Consumer Reports writes, many people are headed toward our sort of experience. They likely don't receive a deep, friends-and-family discount and may skip the bottle of wine at signing, but, because of social distancing, people are increasingly ordering cars online and taking delivery at home -- a situation that offers lessons for the insurance world and recommends an approach known as reverse innovation.

Ordering cars online has for 25 years struck me as the right way to do things, and not just because Mark is such a nice guy. You get exactly the car you want, rather than haggling as the dealer tries to convince you to take the heavily loaded car he has on site that is his closest facsimile. Prices drop because dealers don't have to finance the billions of dollars of cars that currently sit on lots or to pay so many salespeople.

The old system has persisted partly because most people, unlike me, want a car right away, not three weeks later. In addition, dealers capture far more of the industry's profits if they, not the manufacturers, handle the sales, and dealers have been able to use state laws to protect their franchises against any centralized, online approach to sales.

But dealers are now having to adapt, and many are struggling. They don't understand the online behavior of customers well enough to know how to guide them through the buying process if a hail-fellow-well-met type can't sidle up to a couple as they walk through the front door of a dealership.

Insurers and their agents/brokers are going through something similar. The shift is less severe--it's easier to walk customers through the details of an insurance policy online or on the phone than it is to try to take a customer on a virtual test drive of a car--but the industry is shifting toward digital during the crisis and will likely never return to the level of in-person interaction that existed just a couple of months ago.

So, how best to prepare for this long-term change?

I wrote four weeks ago about using the restrictions caused by the pandemic as a natural experiment to track how much value you really got out of travel, conferences, face-to-face meetings and other activities that you've never been able to question because they're how business has always been done. Many of us have also long argued in favor of using a "clean sheet of paper" as an occasional exercise to stretch your thinking: You set aside near-term considerations, take out a proverbial blank sheet of paper and imagine what the perfect form of your business could look like in, say, five years. Then you start planning to see if you can't get there from here.

But I wanted to add an idea that will be especially appealing to companies with access to international markets, either on their own or through partners, but that is available even to those of us who just read or watch what happens there. The ideas is reverse innovation.

The innovation is "reverse" because, while those of us in the developed world tend to think that we come up with the new ideas and then eventually export them to the developing world, many ideas can actually flow in the opposite direction. That's especially true when it comes to cost-cutting: An "inexpensive" piece of medical equipment in the U.S. doesn't look so inexpensive in, say, Sri Lanka.

I first came across the idea when I helped two McKinsey partners write a book that, come to think of it, was published seven years ago this week. We described a refrigerator that was designed in India, that cost less than $100 and that was making inroads against "inexpensive" models in the developed world that cost several times as much. I've since become a fan of Vijay Govindarajan, who published a piece with us back in 2013 on how reverse innovation could cut U.S. healthcare costs in half and who has written a very smart book on the topic. The notion has even surfaced as a possible solution to the shortage of ventilators for those who become seriously ill from the coronavirus: A machine designed for rural areas in developing countries would cost roughly $100 each, as opposed to more like $15,000 for those in use across the U.S., and attempts are being made to rush it into production.

In insurance terms, the best example I can think of for reverse innovation is microinsurance. It almost has to be sold in a hands-off fashion, so there must be lessons already available on what works and what doesn't that could be applied to online selling in the developed world. Joan Lamm-Tennant, who is CEO of Blue Marble Microinsurance and who spoke on the keynote panel at the recent (fully online) Future of Risk conference, surely has some advice to offer the rest of us.

There must also be other lessons from other companies doing business in the developing world, where the economics have never supported the kind of person-to-person advice available elsewhere -- and where we may start to see the digital models of the future forming.

Let's go find those lessons.

Cheers,

Paul Carroll

Editor-in-Chief

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

The world has entered recession and is witnessing a paradigm shift in how we interact with each other and how businesses operate with the massive #stayhome and social isolation campaigns.

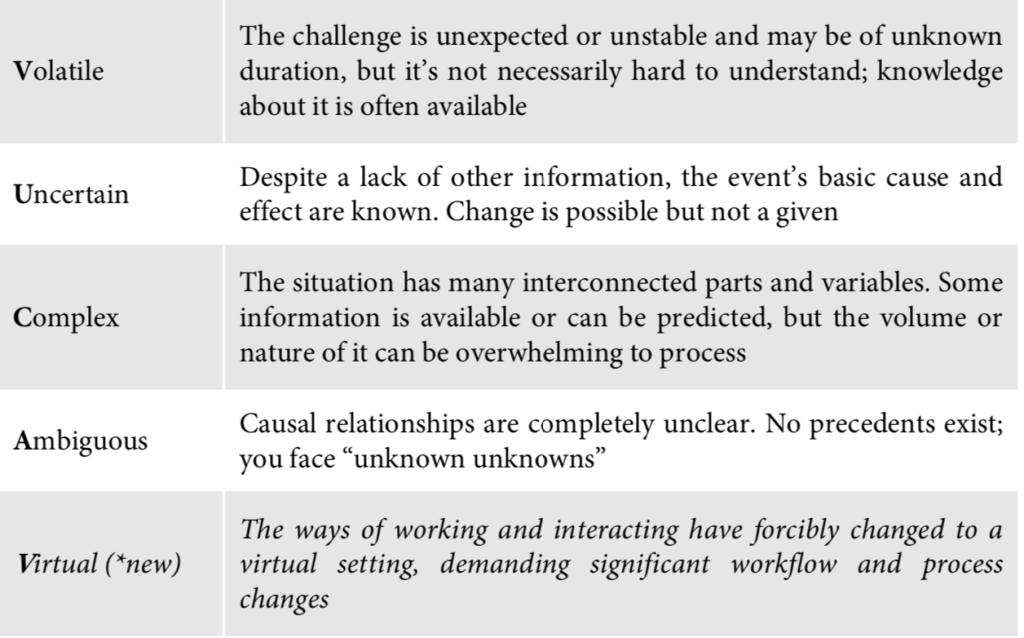

We are looking into a New Normal – a VUCAV world (VUCA+Virtual), where companies and people must interact virtually and in an environment with high rates of unemployment and financial crisis.

Insurers need to prepare for this. They need to radically change the ways they think of interacting with the customers and how they manage their processes internally. If not, they won't stay relevant in the New Normal.

This whitepaper explores how insurers can reinvent themselves as virtual and create an insurer ready for success in the New Normal

COVID-19 has left the world in uncharted waters and in many areas forced a digital acceleration of companies’ product and service delivery processes and distribution channels.

The massive #stayhome efforts have fueled this further with virtual meetings and digital ways of collaborating – the methods and tools used are not new, the massive scale of which they’re used is.

We’re witnessing what can be best described as a paradigm shift – our old ways of working, our beliefs of what’s possible to do digitally and the conviction of some meetings require physical presence are no longer the way we work. We are all virtual.

This has massive implications for almost all industries, and one of the more exposed industries is the insurance industry. Famously known as rigid and lacking behind digital development, a whole industry is now forced to face digital – immediately.

Facing digital right now is one thing; preparing for what’s post-COVID is another. When the virus has been contained, the world will slowly gravitate back to a new equilibrium, a New Normal.

It’s extremely important to realize that we will not be returning to a state like what was before the outbreak – too many things have changed permanently for us and the world to return to what was before. We must prepare for the New Normal.

The New Normal's effects, broad and wide

We’ve already entered a world-wide recession; this is not a new situation, and usually governments have financial instruments to minimize the impact of the falling economic growth, typically stimulants for organizations making it easier to run and grow businesses – but as long as there is no one to run the business, as we’re all staying home, these instruments will have less effect than normal.

At the time of writing, the world is yet to see the full effect of layoffs across all industries and sectors, which will only add to the extent of the recession – the massive layoffs will most likely result in wide-spread depression among people, as there will be extreme competition for the jobs available, and many will see their ability to support their families seriously challenged.

Staying home, doing business, has forced us all to go digital. This has developed our virtual meeting skills and our online shopping savvy and forced us to be used to handle our daily tasks and administration work online – we’re looking at a seismic shift of everyone’s readiness for digital products, services and ways of doing business.

The virtualization of the way we live, work, shop and interact directly affects the future demand for products and services, and people skills and competencies – we will see jobs, products and competencies becoming obsolete as the virtual ways no longer require them. As a result, both companies and people will need to redefine who they are and what they offer.

Just think of 3D printing; when physical distribution is cumbersome, why don’t we just download the specifications for what we need and print it ourselves? That’s how they get spare parts to the International Space Station, so it’s here already.

The insurance customer is no longer the customer the industry has been used to. Customers have been forced to manage their transactions from home by themselves, or with minimal support from virtual agents (brokers, call centers, etc.) – and because they’ve also been forced to meet their friends and families online, as well as doing all their shopping virtually, they have become used to it.

Their – and our – virtual habits have changed profoundly, so companies must adapt to serving customers virtually. Now and post-crisis.

This obviously has significant implications for most insurers, as they have to rethink their digital products, services and distribution channels. The majority of insurers are working on these elements, but few are ready to deliver a complete virtual customer product and service offering. Even fewer are ready to do so in the current environment.

Responding to a VUCAV world

Insurers must find a path forward if they wish to stay (become?) relevant in a New Normal post COVID-19. The path must deliver products and services in a virtual setting and be capable of running large parts of their operations virtual as well – all this at lower costs than today.

Navigating a company in the "old" VUCA world was complex enough, with new business models emerging, constantly shifting consumer trends and unstable economies and political environments around the world.

Adding the virtual element to the VUCA world, VUCAV, complicates the matter, but this is the New Normal so insurers – and all other firms for that matter – must accept it and act on it.

Failure to do so will put the company at risk of going out of business.

Table 1: The new VUCAV world

Source: Own development and Harvard Business Review January-February 2014

The virtual insurer – Phoenix rising

The basic foundation for building a virtual insurer – or transforming an incumbent to a resilient and competitive company – builds on a set of guiding principles. Key principles – the foundation:

Minimize fixed costs

A vital part of creating a resilient company is to reduce the fixed costs to an absolute minimum, as this will provide the firm with greater flexibility to adjust and adapt to sudden changes in the market conditions.

Fixed costs such as long-term rent agreements, permanent employees and capital investments will stay in the balance sheets for a long time and reduce the financial flexibility of the insurer.

Future investments should therefore be seen in the above light, keeping long-term obligations at an absolute minimum, and the current fixed assets as well as permanent staff should be analyzed to gain a better understanding of how to increase financial flexibility.

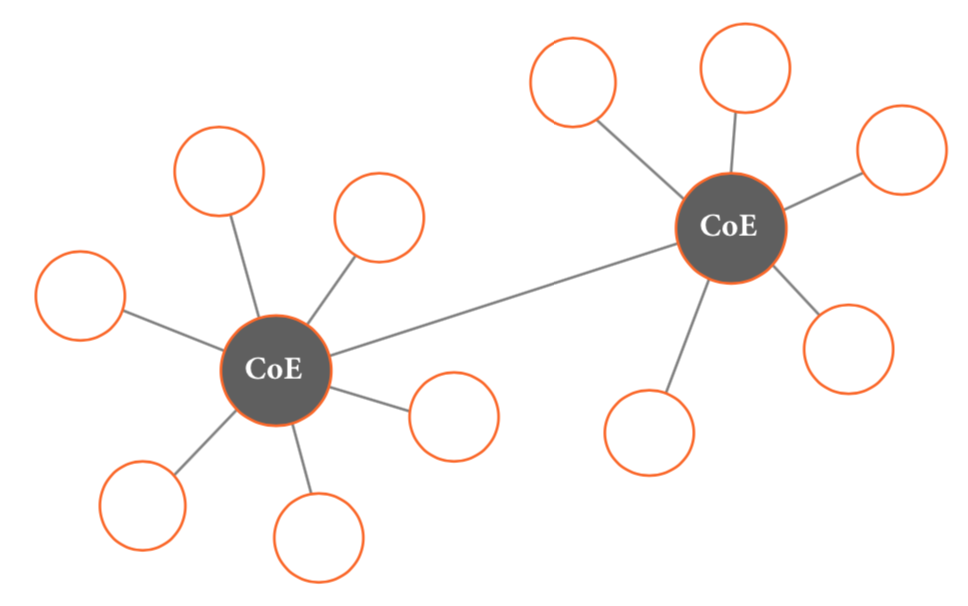

A way of increasing flexibility in the workforce is to create centers of excellence within the company, all leading external teams of experts within specific fields, but outside the core competences of the insurer.

Figure 1: Creating Centers of Excellence (CoE) to minimize fixed costs

This will ensure that key intellectual property is kept at the insurer while specific, more generic tasks and work is outsourced on flexible engagement contracts, allowing the company to scale up or down as required.

Think of permanent staff as the organization’s nerve centers, coordinating all vital functions with external teams.

Maximize virtual

Following the reduction of fixed assets and permanent employees is an increased need for remote work and business development, which is also a consequence of the COVID-19 crisis and a part of the New Normal, where the world has been forced to manage most of their daily tasks virtually.

A key principle for the virtual insurer is therefore to ensure that virtual is permeating all units, processes and systems of the company, including the more difficult tasks of establishing new business between new partners remotely – apart from being a necessity at the moment, this also drastically improves the insurers’ responsiveness in the New Normal.

It does require a continued reskilling of the workforce (and partners) to better deal with being virtual and having more difficult meetings virtually, too – it used to be common practice that tough negotiations and difficult employee talks required physical meetings.

The virtual organization will increase overall speed, as meetings can be held instantly with no transportation required – it’s a more effective way of working and meeting.

Eliminate resource trapping

Resource trapping is what happens when resources are assigned to specific projects in an organization and stay within the unit even after the project has finished. They stay as there are still tasks related to the project, so there’s still a job for the resource to work on, maybe not full time, but there is no real value-add anymore.

As business unit leaders typically are reluctant to give up resources within their organization, there’s little incentive for the unit to free the resource, so the resource is trapped within the unit.

This drains resources, or adds resources unnecessarily, and slows the overall performance and flexibility of the organization. It must be avoided when creating a resilient, virtual insurer prepared to tackle a VUCAV world.

It is therefore vital that being aware of, and eliminating, resource trapping is a key principle to follow when creating a virtual insurer to avoid inflexible costs that are difficult to adjust to market changes.

While the key principles should be the building blocks of the virtual insurer, following these only will not create the agile and fast-moving virtual entity required for successful navigation in a VUCAV world. Creating a responsive organization requires alignment and digitization of the processes and workstreams in the company.

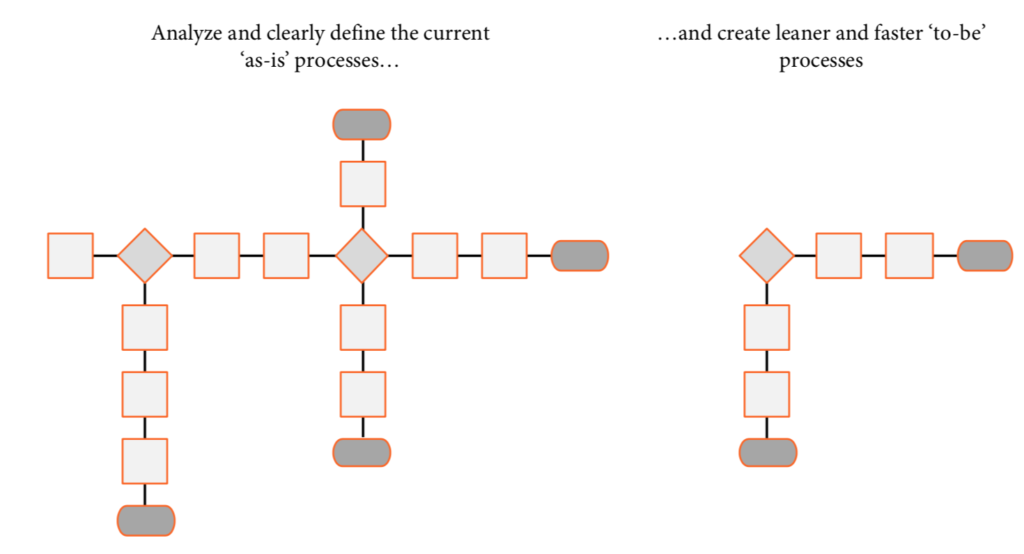

As-is versus to-be

There’s a clear need for introducing new ways of working, heavily supported by technology. This is most often done by mapping out all the current (critical) processes in the organization, bearing in mind that a critical process can be anything from a customer support process to a small, internal process that significantly impedes the daily workflow.

Figure 2: Designing new and optimized processes for faster turn-around times and improved responsiveness

Based on this mapping, the teams will work together to draw out the new, "to-be" processes focusing on how to make this adjusted process as fast and smooth as possible, both for the users of the process and for the customers (which can be internal or external customers).

When implementing the to-be processes, it’s imperative that the processes are digitized to the maximum extent possible. Use digital workflow tools and electronic signatures to ensure a virtual workflow – do not let connection issues to legacy database systems stop this process. Move fast and efficiently.

Think robots, think artificial intelligence

The process optimization work will identify tasks or work streams that for all practical purposes can only be done manually. However, it’s important to analyze to what extent these manual processes are repetitive as repetitive work streams can be outsourced to robots and hence completed faster and much more cheaply as part of the new to-be process.

Deploying robots to handle manual workstreams makes the processes more effective and faster, but the nature of implementing robot process automation will require a clearly defined and documented process, that further improves the overall process sturdiness.

Processes requiring specific knowledge, for example underwriting, should also be looked at, as even underwriting can be automated to a certain extent. Underwriters are already setting the premiums based on formulas, and it’s worth analyzing to what extent it’s possible to automate this process, as well.

If artificial intelligence (AI) – or machine learning – is made part of the (new) underwriting processes, the systems will learn underwriting criteria by themselves and over time become capable of automating more and more increasingly advanced underwriting processes.

Aside from underwriting and process optimization, artificial intelligence can be used to predict changes in consumer behavior early, enabling the virtual insurer to react fast and be ready for the changes even before they are happening.

Working extensively with external partners can further be improved by AI with respect to resource allocation – this would typically be assigning resources in call centers and shared services such as finance, administration and claims management.

In short, adding artificial intelligence greatly improves the insurer’s innovation capabilities, helps optimize operations and greatly support the company in becoming truly virtual.

New ways of working

It should follow from the discussion so far that a virtual insurer requires new ways of working; employees have to get used to working virtually, and performance management systems have to be rewritten too.

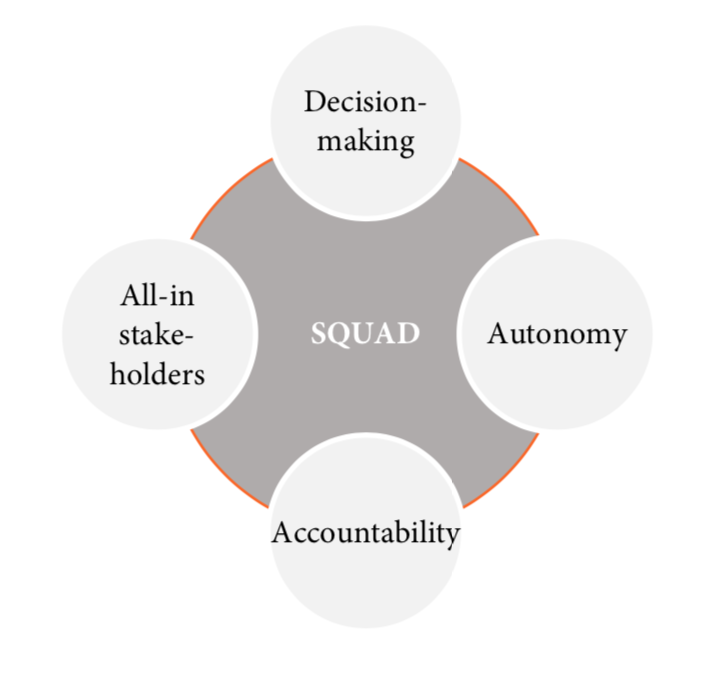

Implementing the agile methodology in managing the workstreams and projects significantly increases the flexibility of the company, as the working squads will work independently and autonomously toward their set targets, reducing the need for daily alignment and control.

Figure 3: Building the virtual insurer around agile squads

A project squad can be likened with a holistic, autonomous project team in the sense that the squad represents everything that is required to secure proper project progress.

The squad is created as a competent unit, capable of making the required decisions to move forward. This significantly reduces outside dependencies and speeds up the administration parts of the project.

Of course, some decisions like major purchases or changes that involve other parts of the organization or customers/partners, cannot be expected to be taken within the squad – in these cases, the squad completes all necessary preparations for approvals to move ahead, so, once the changes are submitted for approval, there should be no iterations.

The squads work best when they are assigned ownership and not tasks – empower the teams to take full ownership and control of the project.

The right tech architecture

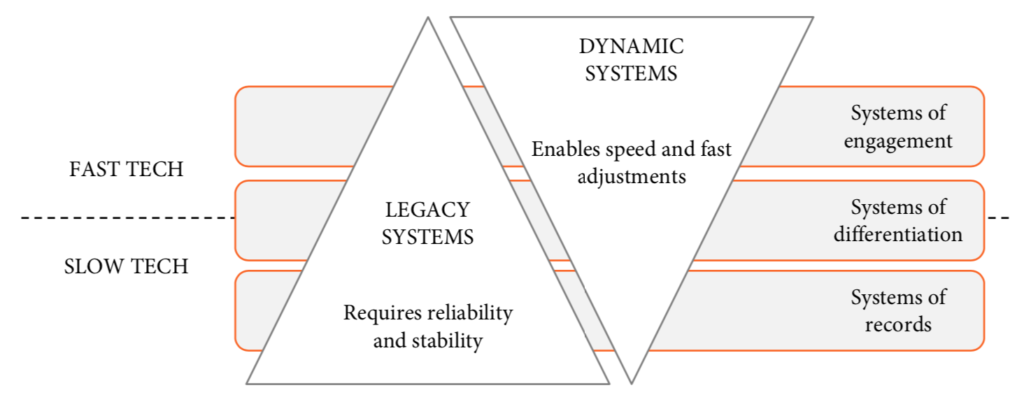

Very few, if any, incumbent companies have the luxury of being able to start all over building their tech architecture – most are to some extent still dependent on legacy IT systems that are very complex to adapt and adjust to changing internal and external requirements. This has historically been the single-most influencing factor stopping insurers – and others – developing digital products and services.

In the New Normal, it is necessary to have a tech architecture that can cope with rapid deployments of changes to both internal and external systems – changes in consumer behavior must be dealt with quickly, and new and smarter processes should be implemented immediately.

Replacing the existing systems will for almost everyone be impossible – it would be too expensive and too time-consuming, and the company risks operating at significantly lower efficiency while the changes are going on.

Gartner introduced the notion of pace-layered architecture that was later dubbed "two-speed IT," illustrating how legacy IT systems can work with new, fast-paced development without losing what is core to the business; the transactional data.

It is possible to expand an existing tech architecture to support two-speed IT, which will greatly improve the virtual insurer’s ability to act fast on market changes.

Figure 4: A two-speed tech architecture enables the virtual insurer to improve time-to-market for digital development Source: Gartner Group

Build vs. buy

When expanding the tech architecture, the important questions of build vs. buy comes up, aiming at whether the company should build the applications in-house or buy ready-made software solutions. The discussion typically revolves around application customization vs. price vs. implementation time.

For a virtual, flexible and agile insurer, there should be no doubt that standard solutions, ready to implement, are the right way forward in almost all instances. However, it is necessary to define the market positioning of the virtual insurer first, so the tech architecture can be designed to create a competitive advantage in the selected market and customer segment.

The buy vs. build depends on where the layer of differentiation is chosen to be, and most practices would suggest that the core differentiation should be built to keep the intellectual property in-house.

But differentiation can also be in the way standard software applications are connected. No matter what, it’s important that the areas of differentiation are decided so the new tech architecture can be built to accommodate that. Examples of differentiation can be within:

Underwriting, bundling of products, special covers or terms and conditions, segment-based pricing, etc.

Customer experience, ease of buying, embedded in other products (part of a TV price, travel tickets, etc.) or simple claims processes, etc.

Products/services

And much more. Bear in mind that even areas of differentiation aren’t guaranteed to last long in the New Normal, so the tech architecture must be structured in a way that makes it possible to rearrange the technical building blocks very easily.

Thoughts on virtual organization

Carrying on the discussion on building the virtual insurer with agile teams and avoiding resource trapping, an organization operating in the New Normal, VUCAV world should avoid the traditional silo structure, as this traditionally hinders fast decision making and reduces the organization’s overall readiness and preparedness for change.

Instead, the virtual company should structure itself around teams, all (most) created for specific priorities, as this will ensure a constant focus on what’s important right now and avoid the building of siloes and internal kingdoms. These teams mostly will be staffed with permanent employees and will also be responsible for managing the outsourced and shared services discussed earlier.

The teams – and the organization – should embrace the principles from Peter Senge’s Learning Organization with a specific focus on a shared vision and personal mastery.

The shared vision supports the agile teams by setting a North Star for the company as a whole, that all agile squads should calibrate their individual goals toward – this creates consistency and unison in the virtual company’s ways of working.

The New Normal and the need for navigating in a VUCAV world requires a new skill set and competencies for employees to perform optimally – it is therefore vital that the organization provides tool and support for the employees to reskill themselves and build the competencies and knowledge required for personal mastery of their tasks.

Key areas of personal reskilling worth highlighting include:

Ability to work effectively virtually – including staying mentally and physically fit

Extreme adaptational skills – ready to adjust and adapt to changing job tasks and environments

Tech savvy – a virtual company requires virtual and digital competent employees

Skilled in digital conflict management – virtual meetings are a common part of the New Normal, so even tough talks must be mastered virtually

From a management perspective, it’s imperative that all teams are working as autonomously as possible with a maximum amount if authority. This will ensure employee commitment and process ownership, which will greatly improve the overall team – and hence organizational – flexibility.

There’s no doubt that insurers – and most other companies, for that matter – are facing a series of very difficult and tough choices around cost optimization, reorganization and how to design the company of the future. And there are no shortcuts. It’s difficult and hard work all the way.

Nevertheless, it is hard work that has to be done. Now. The consequences of not acting now will be fatal.

Stay safe, and good luck.

Get Involved

Our authors are what set Insurance Thought Leadership apart.