The insurance industry —which, in the U.S. alone, accounts for $1.2 trillion—works as the "shock absorber" of the economy, so the industry has a vital role to play in the COVID-19 economic disruption that is hitting the world. The Insurance Information Institute, in its first-quarter “Global macro outlook,” reported that COVID-19’s impact on global growth and the insurance industry is likely deeper and broader than the current consensus and could last well into the third quarter and beyond.

Against such an outlook, here’s a view on the overarching trends in the sector in a post-COVID-19 scenario:

STUDYING THE IMPACT ON FUNCTIONS/PROCESSES & FOCUS AREAS FOR INSURERS TO ADDRESS

Rise in Claim Backlogs/ Rejections

The impact of rising claims can be seen in all the stages of the claims process: registration, adjudication and payment. These may lead to backlogs/rejections. There may also be delays in claim payment due to staff unavailability/limited knowledge, leading to customer dissatisfaction/litigation.

Focus: Insurance firms must now focus on implementing intelligent automation and digitalization for efficient claim processing/adjudication, underwriting, etc. to provide better service levels to customers.

This is where increased adaption of enhanced analytics tools like OCR (optical character recognition), CV (computer vision), NLP (natural language processing) and synthetic data preparation can help insurers scale.

Changes in Underwriting/Sales

The industry will see broad underwriting changes as a result of the pandemic. There will be increased/modified underwriting scrutiny, and insurers have to change their underwriting strategy as a result. A potential shift from traditional channels to digital channels from product recommendations to underwriting is expected.

Focus: Some insurance products may do better with direct sales via digital sales channels. Helping the traditional channels with broker/agent enablement with account/customer intelligence with digital tools and better customer insights will be needed. Customer service will have to look at capacity planning, emerging topics and sentiments and try a digital offload wherever required.

Change to a Remote Working Process

This would mean increased digitalization of processes and workflows. Companies have to figure out strategies to maintain productivity and trust while coping with remote working for the long haul. Robust information security and audit processes will have to be built as a result.

Focus: Insurers have to review existing policies inclusions/exclusions and review coverages to adapt to the changes.

Changes in Policy/Product

During and after the crisis, insurers will have to initiate policy/product changes—including what to cover and how to price it. They may address coverage gaps and introduce pandemic/epidemic pricing on their products.

Focus: Insurers have to focus on repricing, rate calibration and reserving. They will also have to calculate exposure estimation loss prediction (using structured internal data and proxy external signals) by sub-industry, lines of business and regions. They would also need the technology, platform and assistance to usher in digital transformation to enable these products.

Anirban Chaudhury leads the insurance vertical at BRIDGEi2i. He focuses on supporting insurers in their transformation journey using innovations that combine advanced AI applications with technology solutions.

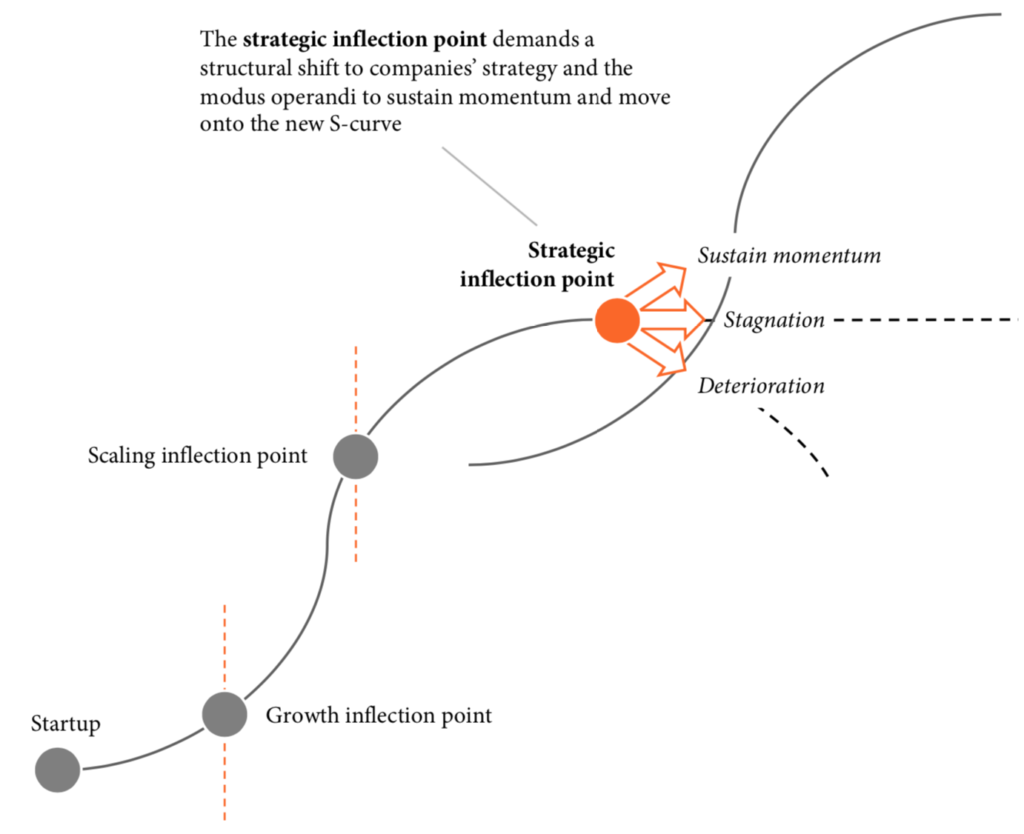

A strategic inflection point, a term first used by then-Intel CEO Andrew Grove, is a period when an organization must respond to disruptive change in the business environment effectively or face deterioration – it’s typically illustrated by the S-curve of business development.

Strategic inflection points are changes that are more than 10 times more significant than typical market changes in the industry; one such clear example is the COVID-19 pandemic that has caused significant disruption to businesses and industries worldwide.

When a strategic inflection point occurs in the market, the companies must act to stay relevant or decline into obsolescence, risking either going completely out of business or ending up as an acquisition target for market players that made the jump onto the new S-curve successfully.

A major reason for companies not being able to make the required shift to the new S-curve is lack of awareness and knowledge in the executive management team; it takes a specific management style and set of competences to actively monitor, understand and act according to market changes.

This whitepaper addresses the management competencies required to successfully lead a company through a strategic inflection point.

The S-curve and why it matters

The S-curve model has proven itself time after time, and it has become clear that all companies, regardless of how successful they are today, at some point will run out of room to grow in their current business areas and trajectory.

There are many reasons for the stalling, from not understanding changes in customer behavior and preferences to sticking to the core competencies of the business (or holding on too long) to not executing and implementing required changes successfully.

In fact, there is less than 10% chance for companies to fully recover, once the company faces a major slowdown in the business (Olson and Bever, “Stall points”).

Faced with this fact, companies must be capable of reinventing themselves over time to stay relevant in the markets, and the S-curve provides an excellent tool to understand this and to help managers identify when it’s time to reinvent the company and jump onto the next S-curve.

Figure 1: The S-curve with key inflection points

Companies rarely go out of business because they’re unable to fix what’s broken, but because they fail to realize (accept) that it actually is broken in due time. When business is "as usual" and management has been accustomed to slow growth – or even stagnating growth – complacency kicks in; “this is our industry, our business, we cannot do anything about it” while indeed management can!

This is where the S-curve becomes an invaluable – and refreshingly simple – tool to help companies understand the market development and enable them to react in time. That is, if the management knows what to do to plan and execute on the response to the changes.

In essence, the S-curve simply depicts the various stages of development of the company and – as history has shown – pretty accurately predicts what will happen next for the company. Analyzed correctly, the S-curve will act as a guide for management on the next strategic move.

Basically, the S-curve has three important inflection points that are necessary to understand:

Starting point

The starting point of the S-curve is where new product and services have just been introduced to the market and are waiting to be picked up. In this phase, the company will typically continue to be innovating the product and service features, testing the market reactions and adjusting the products and services based on the initial experiences with the customers.

During this stage, the company is extremely aware of market changes and focuses on staying agile and flexible enough to respond to these changes as quickly as possible.

Because the organization is fully tuned in on the innovation and development process, and market uptake may be initially slow, there is a risk that the teams become frustrated as growth is not happening fast enough to reward the hard work put into the innovation.

During start-up, management’s focus is on the product development process and how to secure best possible introduction to the market, including adjusting the organization to quickly respond to changes. The need for continuing changes and adjustments often results in less focus on profitability and scalability.

When the new products and services are reaching a stage where they are aligned to market demand, the company will be able to scale and grow the (new) business. This requires scaling of the production and delivery processes and also demands a more structured approach to operating the business as a whole.

It is no longer feasible to sustain the preceding levels of corporate flexibility and agility as the company now has to produce and deliver at scale – often, standard operating procedures are introduced, and management will begin focusing on delivering the products and services while maximizing profits.

The teams will feel excited and inspired by the growth during this stage, and management will have to balance between keeping the motivation high and introducing standard ways of working to secure economies of scale and, through this, profit.

Strategic inflection point

Stagnating — or even declining — growth is a sign the company is approaching the strategic inflection point, the point where the company is forced to respond to disruptive change in the market.

At this point, the company has faced growth decline and management has therefore been focusing on optimization and cost-cutting, focusing on only the key value drivers and costs. This has led to a somewhat frustrated atmosphere in the organization as new initiatives and development typically has been put on hold because of financial constraints.

Unfortunately, many companies fail to realize (or accept) the strategic inflection point in time, allowing the disruption to happen at full scale and speed, further increasing the cost focus and sense of despair in the company.

It’s time to set out a new direction to put the company back on the growth trajectory – and this cannot be done by focusing on costs — there’s a need for a revitalized growth and business development mindset.

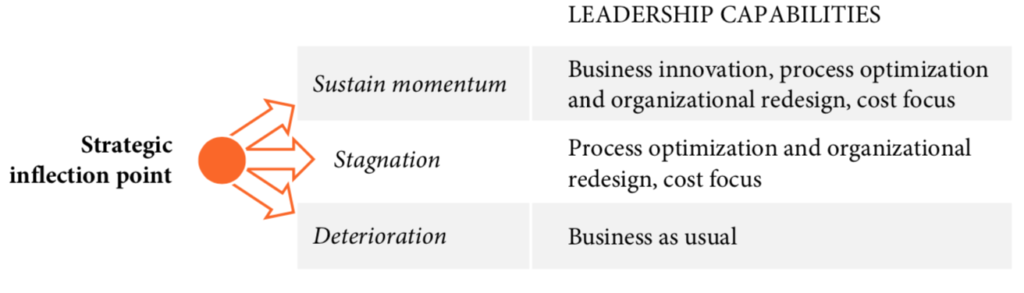

In the New Normal, all capabilities are required at the same time.

However, there’s still a need for focused cost control as the company would need to invest in the future growth and development, and there’s a need to align and optimize the operations to keep the business running during the period of reinvention and redesign of the products and services

Suddenly, all three management capabilities are required; the startup and business building capability, experience and competence in scaling and running operations effectively and cost optimization/restructuring capabilities.

Historically, companies are going through three phases in a cyclical manner, requiring various management capabilities depending on the phase the company is in.

During the growth and innovation/development phase, the primary management capabilities are innovation skills, company start-up experience, market proximity, abilities to see partnerships across industries and think in new value chains and distribution models.

Scaling a company up to cope with increasing demand requires operational experience, optimization capabilities and experience working with processes and process optimization, all connected through solid knowledge on organizational structuring to match the purpose.

Figure 2: Sustaining momentum – moving to the next S-curve – requires leadership capabilities from all stages in the S-curve

Managing a stagnating company takes cost optimization capabilities, including knowledge on outsourcing/offshoring models to secure the company is running with as low a fixed cost base as possible – this frees cash to help the company through the stagnating period.

Sustaining momentum, moving from the current (old) S-curve to the new, requires all capabilities to be present. The leaders must be able to drive business innovation and development in uncharted waters as well as carrying out significant changes to the organization and processes to ensure scalability and effective processes and operations.

Adding to this, the manager must be capable of cutting costs and freeing as much capital as possible to ensure the needed funds for investing in the business innovation.

Focusing on costs, process optimization and organizational redesign will only keep the company on a stagnating route, leaving it as an attractive acquisition target for companies ready to innovate and invest in market and business development.

If leaders leave the company to doing business as usual at a strategic inflection point, the company will deteriorate and become obsolete over time.

Pulling yourself — and the team together.

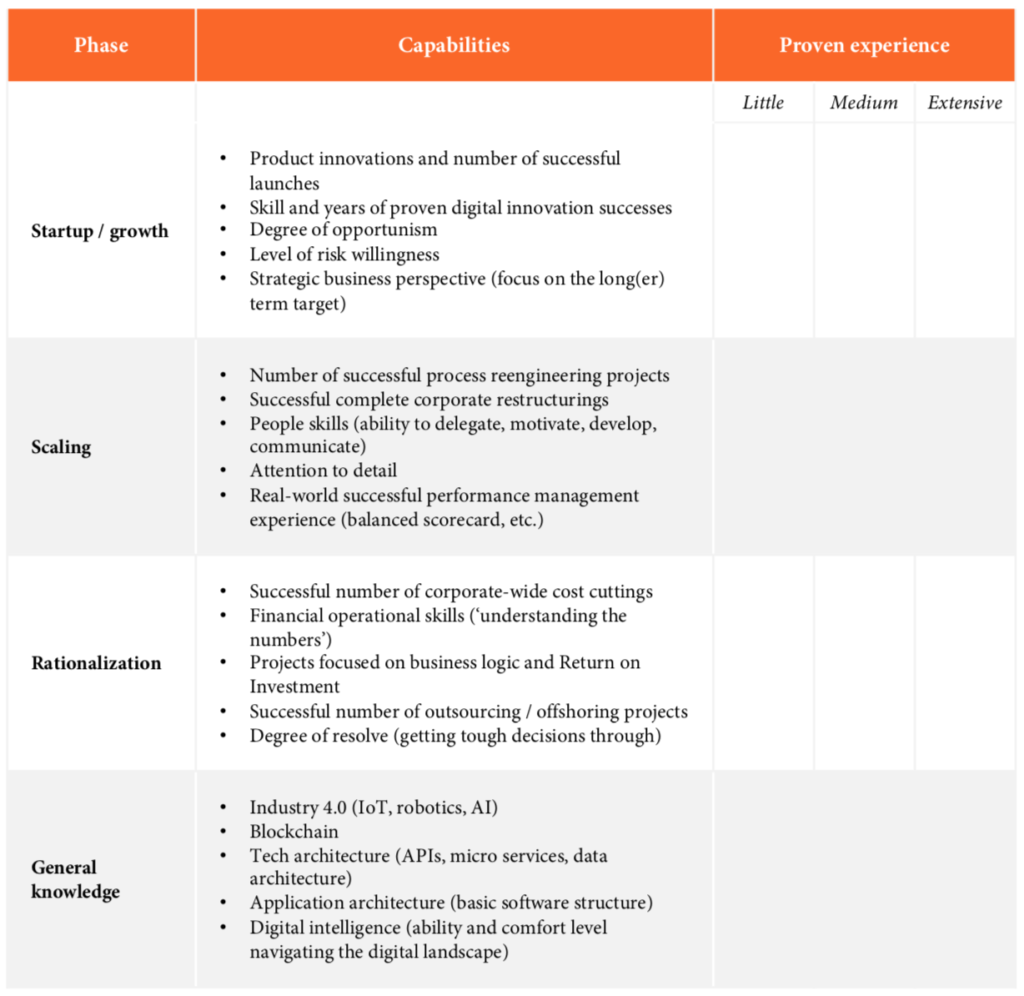

It’s safe to say that most organizations – and insurers specifically – are at a strategic inflection point at this moment, and sustaining business momentum requires leadership that possesses all three capabilities, from growth over scaling to rationalization and optimization.

The fewest – if any – executives have all three capabilities as core competencies, so it is important for managers to understand their own competencies and, based on these, gather a team around them to make sure all required competencies and capabilities are present in the executive management team.

This chapter briefly highlights the leadership capabilities that are specifically required for each of the phases in the S-curve and is meant as a guide to a self-assessment as well as assessing the team members so it’s possible to create a dream team that collectively has all competencies required to secure the momentum of the company going forward.

Use Table 1 as a starting point for evaluating your own key competencies in the light of what’s required for the different S-curve phases and then do the same for the management team – ideally the combined capabilities should all be in the extensive proven experience column.

Table 1: An illustrative method to perform self and team assessment of capabilities to secure momentum at the strategic inflection point

When the team has been identified and established, it is imperative that it is functioning as a cohesive unit, that all major decisions are made in agreement and that the entire leadership team agrees openly and uniformly in front of the employees.

A team that is not fully aligned risks losing the advantage of having all specific capabilities combined, and risks losing the trust of the employees, which will make the organizational change indefinitely more difficult.

Managing another gap — the lack of know-how.

In the New Normal, you cannot do as you did in the old normal, just harder. You need a new way of doing things, a new approach to strategy, to management and to your organizational construct.

The world at present – and according to all predictions in the future, too – will present companies and leaders with a situation of many unknowns and even unknown unknowns. There will be many moving parts that all need attention, and chances are that leaders will not be aware of how many of these will develop over time, let alone how to take action on the developments.

Faced with this, it is easy to become overwhelmed and experience action paralysis, a state where the vast amount of information – or the fact that there is no information – results in a sense of not knowing what to do.

Action paralysis can be extremely dangerous for the company, as managers experiencing this typically will focus on small details in the daily operations instead of grasping the big picture and working on a way forward to secure a future successful position for the company.

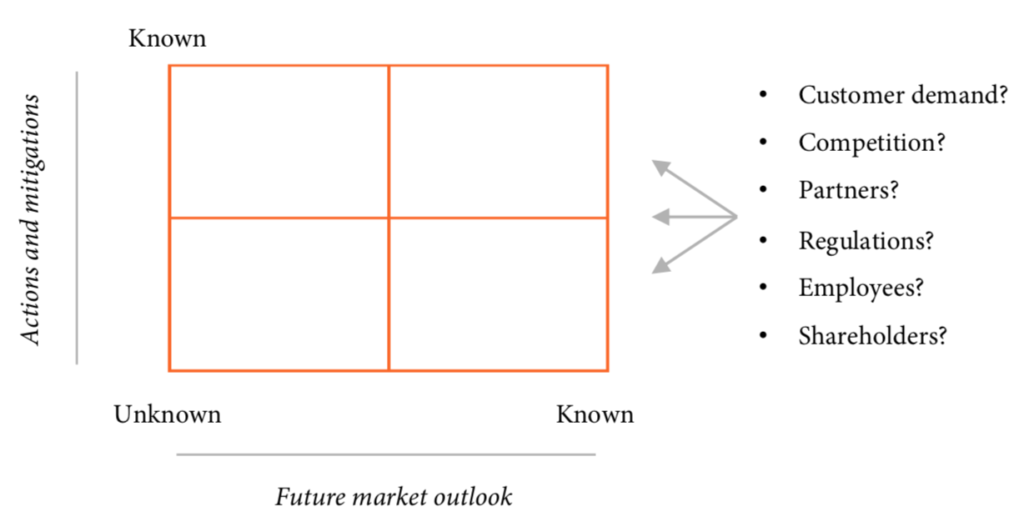

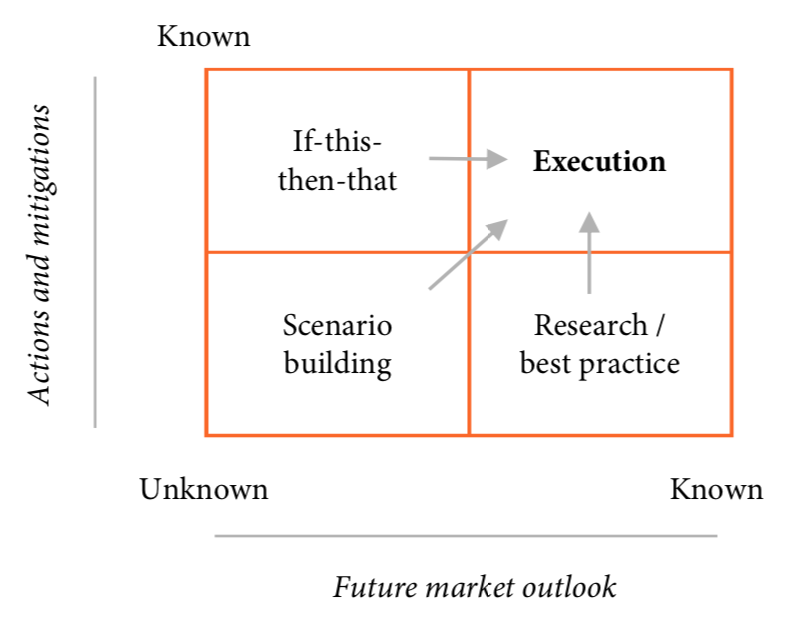

The known-unknown matrix is a valuable tool in creating an overview of the situation compared with what actions are required to be taken – it’s built around an axis of market outlook and development and an axis on actions to be taken as a function of the market development.

Both axes are split into what is currently known and what is unknown, and this mapping helps generate an overview and what’s required to get the sufficient knowledge on how to prepare and execute actions for the company.

Figure 3: The many ‘moving parts’ in an uncertain, volatile business environment; the ‘known-unknown matrix’

All eyes on you.

As executive, and especially during turbulent times, employees will look at you to seek guidance and comfort in the situation – it is an inherited human need to be comforted and feel safe, and employees will seek this from the executive management – and especially the CEO – of the company.

Executives must find ways of eliminating the many unknowns and unknown unknowns and turn the knowledge into specific actions and mitigations – this will be a vital part of becoming confident in setting the direction of the company, provide employees the guidance and comfort they seek and set the company on the course to success.

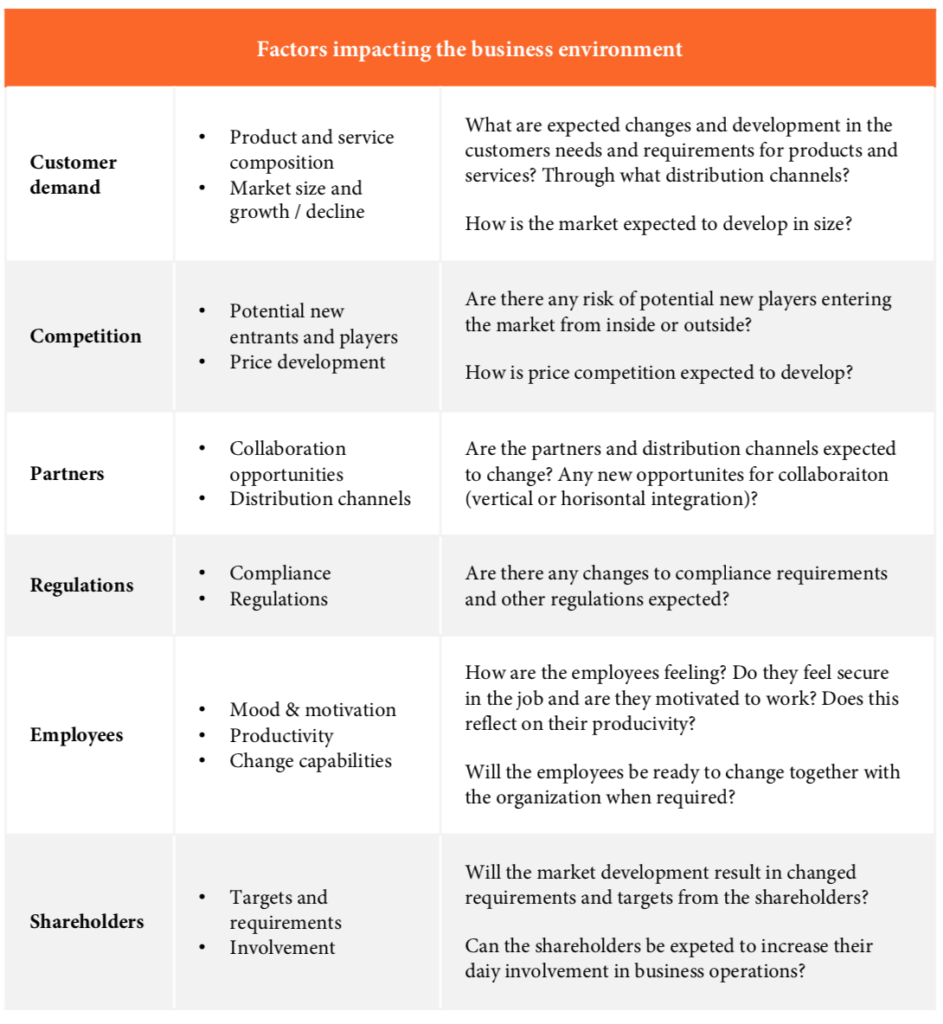

Using the known-unknown matrix will help creating the required overview of the situation and provide a plan for what to do next. As a starting point, areas of the business environment that should be mapped are shown in Table 2.

Table 2: Major elements affecting the market development and the future success of the business

Start out by mapping the factors from Table 2 into the known-unknown matrix with your current levels of knowledge and resulting actions and mitigations.

The purpose of the exercise is to map out what is known and what is unknown so the unknown areas can be uncovered and actions planned – theoretically to move all unknowns into the known-known quadrant.

Don’t think you’re expected to know it all, but you’re expected to know what you don’t know and make decisions based on this, seek advice and guidance wherever and whenever you feel you’re outside your comfort zone.

It is important to seek information from credible sources, which can be anything from industry analysis from partners and via internet, as well as peer discussions within the industry and in near- field industries.

Figure 3: The many ‘moving parts’ in an uncertain, volatile business environment; the ‘known-unknown matrix’

Acting on the known-unknown matrix

One dimension of the known-unknown matrix deals with market intelligence and predictions, and the other dimension is about management reactions, strategy, actions and implementation.

It should be the aim of managers to work on moving all important factors discussed above in Table X into the Execution quadrant of the known-unknown matrix as this will provide the knowledge required to take action.

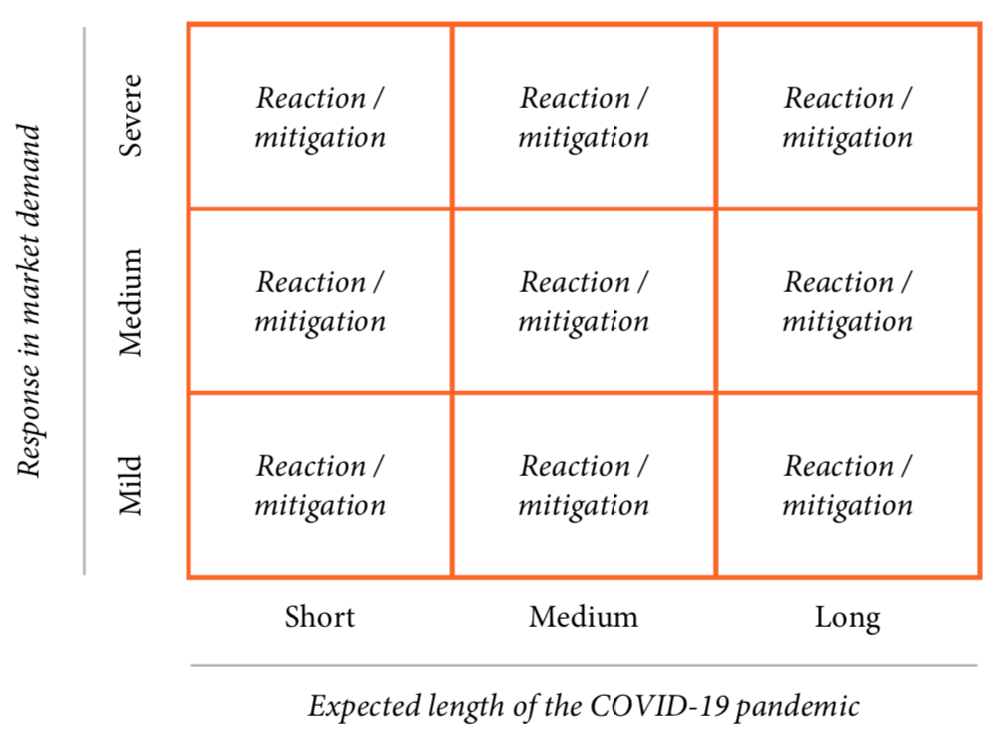

Unknown unknowns – create scenarios

Factors that are in the unknown unknown quadrant are areas where there is not sufficient knowledge about the current and future market development and there is no experience or knowledge on how to take actions on possible outcomes.

Working with uncovering factors in this quadrant can be done through scenario planning where hypothetical developments in the markets are paired with corresponding management actions – there will therefore be created a mitigation from management in the case any of the market developments hypothesized is happening.

Figure 4: Example of a scenario matrix to map actions and mitigations in the ‘unknown unknown’ quadrant

Unknown known

The building of scenarios are closely linked to the quadrant above, the ‘unknown market development, known actions’ as the scenarios are prescribing just that – “if this scenario happens, then we do this” – the difference is here that the leaders already have a set of mitigation actions ready, depending on the market development.

In the cases where the development/future outlook is known for the factors being analyzed, but actions to mitigate the developments are not, research into best practice management responses will go a long way in determining the actions required.

Execution

It is important to understand that when it comes to acting and executing on plans, two dimensions must be considered, knowledge- based and action-based executions.

Knowledge-based – understanding what to do

The knowing what to do is partly covered by the analysis made with the known unknown matrix and covers situation assessment as well as strategy and scenario building.

However, in understanding what to do, it’s crucial that the leaders hone their mental agility – their critical thinking skills and their comfort with complexity. In most cases, the actions required will be taken in unchartered waters, and the leader must appreciate this and be ready to dive into the unknown to execute the plans made.

Action-based – knowing how to do it

One thing is understanding what to do and preparing yourself to do so, another thing is to actually do it. It takes resolve to make the hard decisions and stand firm when (almost) all are against you.

To get things done, it is necessary to cut through the corporate political mess and make sure that the agreed-on actions are actually carried out – there will always be forces trying to work against the change.

Final thoughts

Changing an entire company in unknown times is an incredibly difficult task. However, it is important to remember that the task does not disappear by not responding to it and doing nothing.

This whitepaper covered important areas to be aware of and to understand in the current business environment and in preparing to compete under the New Normal – a new and unseen business environment that is expected to be volatile, uncertain, complex and virtual.

Responsible business leaders should take note of this and prepare themselves to lead their organizations through dramatic changes toward a new operating model and prepare themselves – and their organizations – for a world of constant change.

There will be no new stable business environment for the foreseeable future, and failure to adopt and adjust to this will be fatal for the long-term survival of the firm.

All journeys begin with a first step. I hope reading this was yours.

Good luck.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

A discussion draft of the “Pandemic Risk Insurance Act” has circulated over recent weeks. Based on the Terrorism Risk Insurance Act, the text is an excellent jumping off point to think about what would work and what would not.

The draft quickly forces to the surface an uncomfortable reality that a TRIA-style “make available” requirement would separate policyholders into the haves and the have-nots.

Large corporations with the financial wherewithal and sophistication to establish their own pandemic risk insurance companies may structure multibillion-dollar bailout plans free from government intrusion into executive pay, share buyback plans and layoff strategies. More than 500 such “captives” already participate in the Terrorism Risk Insurance Act and could claim as much as 95% of federal funding under that program.

Small and medium-sized businesses, churches, school districts and other nonprofits and local governments would not fare so well. These regular policyholders cannot afford to set up their own insurance companies. The standard insurance policies available to them only cover business interruption losses caused by “property damage.” PRIA’s "make available" requirement would cancel out a pandemic or virus exclusion – it does nothing to address the necessity of property damage.

A large corporation can simply negotiate with itself to remove the prerequisite of property damage. Regular policyholders would have to file lawsuits seeking a judicial finding of property damage as is happening right now in the context of COVID-19.

The discussion draft should be focusing attention on the needs of regular policyholders. Once we have a solution that works for them, we can worry about what the program can do for insurance companies and large corporations.

Jason Schupp is the founder and managing member of the Centers for Better Insurance. CBI is an independent organization making available unbiased analysis and insights about key regulatory issues facing the industry for use by insurance professionals, regulators and policymakers.

Digital disruption used to be seen by insurance industry watchers as an existential threat to the sector. That argument no longer applies. Today, there’s no argument that the insurance needs digitalization to secure its future.

Across the financial services sector, companies are being re-defined by their clients’ needs.

It’s what happened with banks. They were driven to embrace fintech because of the speed of innovation required, and what their customers were experiencing elsewhere, particularly in the retail sphere. In the same way, insurers (and brokers) are looking to insurtech for answers.

Actually, the insurance industry doesn’t have a choice, with insurance spending as a percentage of GDP declining over the course of the last two decades. The industry’s share of GDP has declined from a high of 7.5% in 2002 to 6.1% in 2017 (source: Swiss Re Sigma Explorer Dataset 2019).

This is happening in part due to an increase in the world’s population and disproportional prosperity growth in emerging markets, creating more consumers who need to protect their property and families. Meanwhile, value is changing in the corporate rankings, where businesses with high-value intangible assets, like Google, Alibaba or Apple, have overtaken companies trading in more tangible products.

It all points to a need for risk management and for the insurance industry to drive innovation and its relevance – especially during a period of great change. Arguably, the incumbent market simply should be innovating at a quicker pace to meet the evolving needs of its client base and its stakeholders.

Many clients today have unmet risk transfer needs, related to intellectual property, the gig worker economy, cyber threats, pandemic or climate, for example. We as an industry need to acknowledge these differences across traditional and emerging markets, tangible and intangible assets, and deliver a differentiated approach in our increasingly connected world.

Meanwhile, the entire sector – brokers and insurers – has been making healthy profits. This combination of an inverted innovation curve and profit pool has proved to be irresistible to entrepreneurs.

Incumbents’ fears around digital disruption are misplaced, however. After all, when the fintech wave hit the banking sector, it didn’t knock out the big players like JPMorgan Chase, Bank of America and Citi. They retained their positions because they took the best of innovation and applied it.

In a similar way, the insurance industry can and will adapt to the direction of change in the use of technology-enabled platforms.

The insurance industry has to incorporate digital distribution and automation in underwriting, the intersection of data science and actuarial science, to design modern underwriting models and create larger pools of insurable risk in ways that insurers remain profitable covering them.

Common ground with clients

Our clients themselves are looking for innovative solutions, so we have common ground. For example, new technology in trucks now allows for user-based analysis of driving behavior. Aon Affinity partnered with CarrierHQ to roll out a new motor insurance program that applies third-party data, real-time driving analytics and a proprietary rating algorithm to score each driver in a fleet of 20 or fewer trucks. Premiums are adjusted monthly for each truck based on the driver scores. To power this behind the scenes, Aon partnered with Instec to enhance the customer experience for small fleet trucking while improving underwriting results for the insurers.

By using our data analytics and insight, we can design technology-enabled platforms for all kinds of business, big and small. It’s why Aon acquired Coverwallet, the leading digital insurance platform for small and medium-sized businesses.

The evolution is unstoppable because innovation benefits both the insurance markets and the underlying consumer.

Even pacesetters like Amazon and Uber continue to be defined by their clients and appreciation of the transparency and convenience these platforms afford them.

To meet the needs of a changing consumer, incumbent businesses – including insurers – need to be client-driven and data-centric to embrace innovation and better network among themselves.

But crucially, everyone needs to stay safe in a dynamic environment heightened by cyber risk, global pandemics and climate change, a problem that insurtech is helping resolve to the benefit of both insurers and insureds.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

John G. Bruno serves as Aon’s chief operating officer as well as chief executive officer of Aon’s data and analytic services solution line, which includes the firm’s technology-enabled affinity and human capital solutions businesses.

In the middle of a pandemic, no one seems to argue that data isn’t essential. What many people don’t realize is that the same attributes that make data vital today won’t go away when the crisis ends. Data, effectively used, will always have ground-breaking, business-changing, mind-enlightening value.

Certainly, one of the benefits from the crisis is that data’s value is selling itself with a clear voice. While insurers were already on a dizzying pace of change, the pandemic has accelerated the need for adaptability.

But there is a hurdle. Without a very strong focus on data as a strategic corporate asset, insurers will struggle to keep up with the necessary changes in the “new normal.” The right philosophy is the foundation needed to design and implement a strong enterprise data strategy.

The Most Vital Data Philosophy — Data as an Enterprise Asset

Every insurance company believes that it knows the importance of data. We say “believes” because if the company truly knew the value of data, there would be an enterprise data governance team that would: (1) treat all data as a true enterprise asset – as opposed to a department asset; (2) look at the data strategy and how the company plans to use data both internally and externally; and (3) have an organizational structure to fully support that strategy.

Most insurance companies have siloed data, owned by various departments, not the enterprise. The attempted solution has been to create a Huber data storage, master data management (MDM) or data lake solution. The company assumes that, once the data is in one of them, everyone would have full access to any type of analytics or reports that they desire from the data. Some insurers spent tens of millions of dollars, only to fail due to the sheer size and complexity of the effort. Too often, it was driven by the IT organization, relegating it to a technology exercise rather than a business-driven strategic project.

Data must be first viewed as a corporate asset, no different from the financial department.

Data Needs an Enterprise Strategy

But most companies do not have an enterprise strategy for data. Many carriers leverage data for predictive analytics by the actuarial department, but these models can take four to six months to develop because, with each data set refresh, the data must be cleansed from scratch. Actuaries report that this cleansing takes 60% to 90% of the total effort depending on the quality of the data. Different departments, such as claims and marketing, have done analysis with their data with varied levels of success. Each instance somewhat resembles the actuarial example — the effort takes too long or the results are suspect due to the quality of the data supplied. In each case, we are still dealing with siloed data instead of integrated enterprise data.

It takes a visionary data leadership team to convince the organization that efficiency and accuracy can co-exist. Enterprises need a full enterprise data ecosystem model to establish and define both internal and external data flows and the business value associated with these efforts. When this happens, an insurer’s capabilities change overnight, but the strategy must come ahead of tactical data efforts.

The enterprise data strategy requires a very strong business focus on the use of data and data quality within the enterprise. Data is not an IT asset, it is a business asset. It is the lifeblood of the insurance business and, indeed, the entire insurance industry. It can no longer be an IT initiative to address the quality of the data and how to integrate it. At the enterprise level, there must be a thoughtful and concerted focus on the business value of data and how both internal and external data can be incorporated into the executive mindset.

This has proved too daunting for most insurers.

Why Is Data an Enterprise Asset and Not a Departmental Asset?

Most corporate assets are clearly considered an enterprise asset. Budgets always start from the top and are broken down into smaller organizations and departments. No company ever tries to start the budget process at the department level and consider it the department’s money that “we’ll share as a good corporate citizen to help the company” as applicable. This would be unthinkable. For each department or organization to decide what assets are theirs and what is worth sharing would never work. Why then is this approach used with respect to data?

You hear statements like, “We need to bring in the claims division’s data or product team’s data or marketing data into a consolidated store.” People are referring to the department’s data as if the department owns it. This kind of thinking adds layers of redundancy and fosters siloed approaches, not to mention losing cross-departmental knowledge and an understanding of synergies.

While an insurer does want to integrate the company’s claims data with the company’s policy data, with the company’s marketing data, it is the enterprise’s data.

The other part of this misaligned mindset is discovered when only the claims team “knows” the claims data, only the product team “knows” the product data and so on.

Carriers must change their mindset about their data. It is the enterprise’s data and must be governed, understood and managed from the very top, no different than any other corporate asset.

Insurance Data Efforts Deserve a Data Management Organization (DMO)

Most insurers have a program management office, or PMO. The PMO’s purpose is to create and maintain a consistent world class project management methodology and process for all project engagements across the company. The PMO establishes policies, processes and best practices, plus standards, training and governance. Project managers are expected to execute against these best practices for each project. The PMO doesn’t get involved in individual projects unless they deviate from planned budgets or delivery timeframes, or fail to adhere to the standards.

A similar approach is required for an insurer’s data strategy. Adding a data management prganization (DMO) and a governance program can be a game changer for providing valuable, holistic data perspectives. Similar to a PMO, a DMO would:

Create and maintain a consistent, world-class data management methodology and process for all data management engagements across the company;

Train, certify (if possible), coach and mentor data stewards in not only data management but also in data delivery, to ensure skill mastery and consistency in planning and execution;

Manage corporate and data priorities, matching business goals with appropriate technology solutions and providing increased resource utilization across the organization — matching skills to data needs;

Provide centralized control, coordination and reporting of scope, change, cost, risk and quality across all data initiatives;

Increase collaboration across data efforts;

Provide increased stakeholder satisfaction with data-related work through increased communications, collaboration, training and awareness;

Reduce time to market by providing better coordination and the right resources with the right skills for the data projects;

Reduce data costs because common tasks and redundant data efforts could be eliminated or managed at the central level; and

While a PMO might be more focused on the internal execution of a project, the DMO must address both internal and external data services and projects. The crucial point of the DMO is that it must be governed and understood at the executive level. It sets the corporate objectives for all data initiatives, and the business value of all data initiatives must be clearly understood at the executive level. The genius of the DMO is in its ability to translate data’s real, enterprise-wide potential, plus its day-to-day value, up to the executive level, where it can promote leadership buy-in. In other words, all of data’s chief users within an insurer gain an internal champion to lobby and lead them in ways they may never have been able to do otherwise. Instead of departments losing control by adding a DMO, they gain an enabler.

Data Needs a Map With Detail

The final step for insurers is to create their data ecosystem strategy and direction. This is more than just documenting the existing data flow. It must take into account where data can be applied to business processes for more effective decisions and business value. For example, one insurer is applying AI to its underwriting process, creating real-time updates to underwriting models. Another example is bringing an insurer’s own historical data on their customer and product experiences into renewal and underwriting decisions. The focus is now on the value of the data being brought into the decisions to improve them, then to make lower-level data corrections at this level.

Data Business Value Must Be Driven by Executives

Many organizations have created CDO (chief data officer) positions or aligned the data group under the CFO. Both of these are great first steps, but they still miss the need for an insurer’s data strategy, direction and projects to all be driven by the executive level and the data asset value understood at the executive level. A CDO should be at the executive table working closely with executives across the organization, eliminating the silos and managing the DMO for the company.

The CDO and DMO should create dashboards to understand the value achieved by data efforts, adherence to the processes and impact. This will ensure that data’s efforts are aligned to business goals and objectives, to help drive better decisions from a business perspective than from a data or IT perspective.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Ben Moreland is VP, data practice and leads the strategy and direction of Majesco’s data and analytics products; he is also responsible for the client delivery of these solutions.

There is still much unknown about how deeply and pervasively the pandemic will affect the U.S. and global economies; however, a deep and long-lasting recession is now a foregone conclusion. The downstream effects of a recession will change the workers' compensation market dramatically for years to come.

Employers should anticipate a hardening workers' compensation marketplace beginning soon.

Rate Increases:

For the past decade, employers enjoyed the advantages of a soft market. Premium rates fell year over year; in 2019, the average workers' compensation rate was at the lowest point in the 46 years since 1973 [California Workers' Compensation Insurance Rating Bureau's 2019 State of the System report].

Businesses in all industries should expect workers' compensation rates to increase dramatically over the next few renewal cycles. Insurance carriers offering both guaranteed-cost and high-deductible policies maintained their market share in a competitive marketplace with enticingly low premiums. Carriers partially offset the cost of insurance with the burgeoning investment returns earned in the booming stock market. With stock market returns evaporated, carriers must now charge the actual full cost of the insurance plus overhead, operating costs and shareholder profits, which will result in dramatically higher premiums.

Reduced Availability of Coverage:

Over the past decade, carriers competed for the employer's business by offering a plethora of competitive options.

Welcome to the new reality of a hard market. In previous hard markets, carriers exited the workers' compensation market altogether to focus on more profitable and predictable lines such as general liability, auto, directors and officers' coverage and the like. With limited competition, the few remaining carriers will become more choosy. Even employers with long-term, loyal relationships to a carrier may be bewildered to be refused a renewal offer. New coverage pricing may be so costly as to require the employer to re-think its entire business and pricing strategy.

This marketplace reversal presents distinct challenges to employers unable to absorb the higher cost of workers' compensation insurance. Higher insurance rates will hammer companies that have long-term, fixed-price contracts or that operate in markets with cutthroat competitive pricing such as service-based businesses, construction and government contracting.

However, all hope is not lost. A few alternatives to traditional workers' compensation insurance have always existed. In California, there is a reliable and robust self-insurance option for employers. A recently conducted actuarial study found that self-insured employers lowered their workers' compensation costs an average of 24% even when insurance rates are favorable. These savings are stable and likely would be even higher in the new hard market. Self-insurance is primarily available to medium-sized and large companies that meet specific financial criteria. Self-insured groups (SIGs) exist in many industries, making self-insurance accessible to smaller employers.

Self-insurance is a stable, predictable and lower-cost option to employers in boom times and recessions.

The employer pays only the direct cost to adjust the claims on an as-incurred basis. There is no carrier involved, so there is no risk of rate increases or lack of available coverage.

In any market, self-insurance offers employers four additional and significant benefits: greater control, increased savings, improved outcomes and peace-of-mind.

Greater Control: Self-insured employers can design their programs, so they exert greater control over how the program works. Employers can determine priorities based on the needs of their company and employees. Priorities may include such objectives as more robust claims processes, faster return-to-work cycles, white-glove treatment of their employees and telemedicine.

Increased Savings: Employers save money because they do not pay carrier overhead, marketing and shareholder profits, as demonstrated in head-to-head studies comparing traditional and high deductible policies with self-insurance.

Better Outcomes: With the potential of greater control over the care and treatment of the employees and processes comes improved outcomes for injured workers. Employees of self-insured companies receive the care and treatment they need in a timely way, delivered by providers chosen by either themselves or their employers. Expedited medical treatment, caring claims administration and return-to-work programs can hasten healing and recovery of the injured workers. Greater control results in employees reclaiming their lives and returning to work sooner, equaling happier employees at a lower cost to the employer.

Peace of Mind: A stable and predictable workers' compensation solution, together with improved outcomes all at a lower cost, contributes to peace of mind for the employer.

Are you interested in looking into self-insurance for your company? First, check with your agent or broker. Some brokers may be knowledgeable and willing to assist you in becoming self-insured, working for a flat fee instead of a commission paid by the carrier. If your agent is not able to assist you, contact the California Self-Insurer's Security Fund or visit the website at www.securityfund.org.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jon Wroten, MBA, CPP is the managing director of California Risk Advisors and the former chief of the California Office of Self-Insurance Plans (OSIP), where he oversaw the nation's largest self-insurance marketplace.

The coronavirus pandemic is already changing the way that American businesses operate, at least temporarily. But look closely, and you can see the potential for long-lasting changes even after life returns to normal.

One of these shifts might just mean the end of the traditional insurance office.

Pandemic-related lockdowns have already forced many major companies to expand work-from-home policies on a short-term basis. Having tried it, some employees and their bosses are considering more permanent changes.

Nationwide Mutual Insurance is going even further. One of the leading life insurance and retirement companies, it moved 98% of its 27,000 employees to working from home in less than a week in early March.

"We keep hearing from members, 'if you hadn't announced you were all working from home, we never would have known,'" he said.

The Fortune 500 company decided to make the change permanent and has already shuttered five offices in Florida, North Carolina, Pennsylvania, Virginia and Wisconsin, and plans to shrink from 20 offices to just four.

As you face similar issues at your business, there are short-term, intermediate and long-term issues to consider.

Short-Term Issues

In the past, employees who worked from home had designed a setup that worked for them. Many workers today are doing so under duress.

Working from home during the coronavirus pandemic is complicated by schools being closed and businesses and workers having no warning.

Taking care of your school-age children, helping with their online learning, sharing home computers and internet bandwidth are all challenging experiences.

Not having the option of going to the office at all is not the best way to make work from home work on a permanent basis.

The coronavirus is going to be with us for a while. Fear of travel and fear of crowds is going to make it hard to convince employees to return to work. Lack of childcare options will continue to be a problem. Even when schools reopen, they may do so under staggered or limited school times.

These issues are going to last for more than the coming 12 months. Now is the time to adjust to the drawbacks of the current forced and hurried experience.

You may need to invest in better laptops and other equipment for your newly remote workers. Your work-from-home staff needs quality video cameras and audio to participate in the increasingly common online meetings.

While your staff may have a home computer their kids use for gaming that has these features, you really do not want to expose your business systems and data to your employees' children’s computers. You would not be pleased if your staff let their kids access the computers in your office. Why would you want your staff working from their kids’ devices?

You may need to provide cell phone or better phone solutions for your home staff. For security reasons, you do not want to have company contacts and emails on your employees' personal phones.

You need to hold regular weekly companywide or department-wide video meetings with your staff. People need to keep the connections with the folks they have been working with in your office.

It is probably a bad idea to have your staff take the computers and printers they currently have in your office home. Most traditional stay-at-home options are combined with remote access to networks and servers used through your current computers at your current physical office.

You need to put in place online methods for your customers to interact with your staff. This means increased use of digital signatures, electronic payments and online video meetings.

Long-Term Decisions

Even in the current situation, working from home provides some positives that you should consider.

Studies over the last several years consistently show benefits to your staff and your company. These include:

13% to 22% increase in productivity

Increased employee retention

Lower cost for everything from rent, to office supplies, to office snacks

Generally happier staff, higher employee morale

Increased productivity and lower costs are two things your business could always benefit from. In the coming economic challenge – whether it turns out to be a recession or even a depression – these may simply be competitive advantages you need.

Take this time to plan how you should restructure your business now. As things settle out you need to have permanent adjustments identified and ready to go.

The future comes gradually, and then all at once. We may be at one of those tipping points, where companies shift from traditional offices in downtown buildings to employees working from home.

Now is the time to start planning for that future.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Having seen more than a little hype in my decades writing about technology, I have for years asked anyone and everyone associated with "smart homes" whether they could make an economic argument for the devices that can protect homes. Would deploying the devices widely cost less than the damage they would prevent?

I finally have an answer. And the answer is... no.

Not, at least, when it comes to a major focus of the "smart home": devices that detect water leaks.

The lack of an economic argument doesn't mean "smart homes" won't eventually happen as detection devices get cheaper. But the economic issues certainly present a hill for advocates to climb, and, with auto telematics, we've seen for more than two decades that a technologically appealing idea doesn't guarantee broad adoption.

My chance to look at a real economic argument finally came courtesy of a LexisNexis analysis of Flo by Moen, which can detect a leak and notify the homeowner or even automatically shut off the water to the house to prevent what can be extensive damage. The analysis reported that installation of the devices in 2,306 homes reduced the number of claims by 96%, in comparison with claims in a control group of 1.3 million homes in similar areas and of similar size and value. The severity of the claims that still occurred fell by 72%.

Sounds impressive, right? But let's take out a proverbial envelope and do some calculations on the back.

Each device is about an $800 proposition — roughly $500 for the device and $300 to have a plumber install it in a home. Multiply that $800 by 2,306 homes, and it costs you $1.85 million to install the devices. Assume even a modest interest cost for that $1.85 million, and you're adding perhaps $50,000 a year to the expense of the installation.

LexisNexis didn't provide the raw data about the number of claims that still occurred, so I made a couple of educated guesses and estimated that those $1.85 million of devices saved the 2,306 homeowners and their insurers about $240,000 a year. That would mean it would take a decade to earn back the cost of installation — $1.85 million plus $50,000 a year for 10 years equals $2.35 million, or almost exactly the $240,000 a year of saving times 10. The payback takes longer, of course, if the devices need any maintenance or, heaven forbid, don't last at least a decade.

(For those of you who, like me, are numbers geeks, I'll explain my reasoning on the savings. The rest of you should just skip to the next paragraph. I began with the 96% number, which meant that 24 out of 25 claims that could have been expected did not, in fact, happen. That meant that either 25 claims was the expected baseline (roughly 1% of the homeowners with Flo installed) or that 50 was the expected baseline (roughly 2%). Our friends at the Insurance Information Institute report that 2% of U.S. homeowners each year file claims related to "water damage and freezing," while the LexisNexis report specified that the claims that were prevented were for "non-weather-related water damage." I don't know exactly how the definitions map to each other, but I assume the LexisNexis definition is a subset of the III figure, so I used the smaller of the two possible baselines. If I'm right, then the devices prevented 24 claims. LexisNexis said those claims average $9,700. Do the math, and you get savings of $232,800. The one claim that still happened was 72% smaller than the $9,700 average, according to the report, so it was reduced by nearly $7,000. Add the two savings, and you're a shade under $240,000.)

Some insurers seem to hope that customers will buy the leak detection devices on their own, but that seems unlikely, at least in any numbers. Perhaps someone will be so scarred by a major loss related to a water leak that he or she will invest in a device. But, if you assume a deductible of $1,000 on a homeowners policy, you're asking people to spend $800 up front to avoid a one-in-100 annual chance of paying $1,000. That math doesn't work for me.

Insurers could subsidize the devices, but who can make a rational argument for an investment with a 10-year return (or even with a five-year return, if I picked an unfairly pessimistic scenario on the number of claims prevented)?

Dan Davis, director of IoT and emerging markets for LexisNexis Risk Solutions, cautioned that the size of the sample for the Flo by Moen study was still pretty small, even though it dwarfed anything I've seen elsewhere. If there was noise in this study, and the actual results turn out to be a 99% reduction in claims, rather than 96%, then you've tripled the savings and brought the economic argument into at least the realm of possibility. (Of course, if that 96% turns out to be 90%, you've got a real problem.)

He said insurers should also be looking at how subsidies for leak-prevention devices might improve customers' feelings about an insurer. How much of a subsidy might a company be willing to offer for a major increase in Net Promoter Score or in the number of years the company can keep a client?

Auto telematics, with their two decades of feeble adoption, have shown the need to think broadly about benefits: Insurers focused on offering discounts to good drivers, only to find that customers often cared more about other, less costly benefits such as free roadside assistance.

The good news for advocates of smart homes is that customers seem genuinely interested, according to other LexisNexis research, and are, despite some privacy concerns, generally willing to share information with insurers in return for some kind of benefit. (My 20-something daughters warn that their generation may be scarred by a 1999 Disney movie, "Smart House," about a smart home that goes berserk and imprisons a family — the story is Disney-ified, but it's still basically HAL from "2001: A Space Odyssey.")

I keep thinking that Roost will build momentum for smart homes based on its intelligent batteries for smoke detectors. The cost of the battery is minuscule, just slightly higher than for a regular nine-volt battery, and there is no cost for installation — you just get on a ladder and swap out your old battery for a Roost battery that alerts your phone any time your smoke alarm goes off. But I have to assume the economic argument doesn't quite work for Roost, either, or someone would have made that argument after years of my asking.

And if a clear case can't be made on preventing fires or water damage, two of the biggest perils for homeowners, then the whole "smart home" movement rests on a shaky economic foundation.

Yes, people will keep buying "smart" devices that help manage energy consumption or that tell you who's at the door (or who's stealing the packages left there), but it seems that the broader revolution will have to wait a bit.

Stay safe.

Paul

P.S. Here are the Six Things I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

COVID-19 and the onset of a deep global recession are reshaping every corner of workers’ compensation, from legal issues surrounding coverage to the delivery of care to injured workers. Some of the changes can be anticipated based on prior recessions. But others are new and highly dynamic and will vary based on the course of the pandemic.

Amid the flux, we see four changes that are critical for carriers to grapple with. How companies respond to these changes may determine their survival in an extremely challenging economic environment. Fitch is expecting a five-year high default rate this month, and economists are expecting even more bankruptcies in the current downturn than in the Great Recession in 2008-2009. Even well-capitalized companies need to quickly adapt.

A Shift in the Types of Claims Filed

Carriers are seeing a sudden shift in the flow of new workers’ comp claims. On the one hand, aggregate claim volume has dropped 40% or more. This is primarily due to the slowdown in activity and hours worked in industries that traditionally drive a high number of claims, especially retail and hospitality. In addition, roads now have 80% less traffic, so there are far fewer accidents and claims from drivers on the job.

At the same time, new types of claims are emerging. Most specifically, COVID-19 claims are rising sharply. As many as 1,500 had been filed in California alone by late April, according to the California Department of Industrial Relations. The share of new COVID-19 related claims flowing into CLARA Analytics’ cross-industry data lake jumped from 1% in March to 4% in April.

The large majority of these claims are from healthcare workers who interact with patients and first responders such as EMTs and firefighters. Many of these cases are likely to be covered under workers’ compensation, pending an array of actions at the state level to cover these workers, such as Kentucky’s state order on April 9.

We should also expect to see a rise in claims from employees who have been recently furloughed. This is driven in part by situations where an employee has an injury that he or she might not normally have filed a claim for in a healthy economy but decides to file the claim given a declining bank account. Experience from prior recessions indicates these situations skew toward cumulative trauma claims, which are complex and costly to manage.

Changes in Healthcare Delivery

Social distancing and crowded hospitals are also leading to treatment delays for non-critical cases, including both recent and long-standing worker injuries. This will create extended periods of disability, more expensive claims and potential litigation. The impact of these delays will depend on the duration of the pandemic. If the impact on hospitals extends deep into the summer or there is a resurgence of the virus in the fall, there could be a new wave of issues for claimants, employers and carriers.

One benefit: The delays are pushing claimants to seek care in new ways, including telemedicine. Services like Righttime and One Call have seen a 2,000% increase in the use of telemedicine in just the past few weeks. Quicker, easier access to physicians may drive better outcomes and enable incapacitated workers to get care they might not otherwise get, which could lead to lower health-related costs.

More Fraud

Experts predict a rise in fraud in the coming months, as COVID-19 opens up opportunities for new scams by the segment of attorneys and providers known to engage in workers’ comp fraud. We will likely also see more claims that are challenging to define as legitimate or fraudulent because they occurred in a distributed work environment where there are no witnesses to corroborate the injury. Even the definition of a workplace injury is strained in a work-from-home situation.

In response, investigation teams are investing in expanding their online detection practices. AI-based data analysis and predictions can open up insights. “Advancements in AI now enable claims teams to see through hidden provider links, complex supply chains and long lag times to identify fraud that previously went unnoticed,” said Dr. Gregory Johnson, a medical cost consultant and former director of medical analytics at the California Workers’ Compensation Insurance Rating Bureau.

A Rise in Litigation

A set of states have recently issued executive orders and directives that shape COVID-19-related workers’ comp coverage, and some states, like California, are on the verge of doing so. As we’ve seen in the past, new legislation drives legal activity, so we can expect to see an increase in COVID-19 litigation over the next few months.

Litigation may also rise from the increase in terminations. An abrupt layoff can leave employees feeling aggrieved. In other cases, workers may simply be anxious to cover an income gap or are uncertain whether to file a workers’ comp or unemployment insurance claim. Unreported or latent injuries can come to the fore and result in a sharp rise in workers’ comp claims.

“Companies that initiate layoffs with little forethought and guidance may see a rise in workers’ compensation claims and experience numerous other unintended consequences,” said Kevin Combes, Aon’s director of U.S. casualty claims, Global Risk Consulting. In the last recession, Aon saw post-termination claims surge at companies that did not manage the event. “Companies that develop thoughtful reduction-in-force strategies are likely to see fewer workers’ comp claims and lower overall expenses,” Combes said.

A Reason for Optimism

Some of the changes we’re seeing, while disruptive, could have major long-term benefits. New healthcare treatments and delivery channels may emerge that improve outcomes and lower costs. Both private and public players in the workers’ comp system are adopting virtual case reviews, settlement discussions and other practices that might also increase efficiency and system access.

In addition, factors that drive cost in the industry may be seeing positive short-term shifts. For example, many claimants and attorneys may be focused on near-term cashflow and are less intent on maximizing claim values by stretching out litigation. As a result, many of CLARA’s customers are seeing cases move to settlement more quickly, at or below reserve estimates. This may be a prime opportunity to resolve stubborn cases or resolve new ones quickly.

Short-Term Disruption, Long-Term Progress

Claims operations at carriers and third-party administrators are not standing still. They are taking steps to respond and prepare for the future. The most aggressive are preparing teams to handle the shift in claims, including new training and handling procedures and updated case reserve guidelines. Many are evaluating new tools and programs to optimize organizational productivity in anticipation of eventual recovery. Principal among the tools available to manage this new world are the AI applications that have recently come to market.

It’s an ideal time to be evaluating AI, which can dynamically update models to account for changes in claims types and trends. By applying AI, claims teams can identify providers to bring into their networks and evaluate and optimize the performance of their attorney panels with evidence from prior outcomes. AI also can aid in making smarter decisions about when to settle a claim and when to litigate.

By investing now in talent and technology, claims teams set themselves up for success when we move into recovery.

Gary has been a leader in the technology industry for over 21 years, with a deep focus on building AI & Machine Learning applications for the Enterprise market. Over the span of his career, he has raised over $1.2B in debt and equity and helped create over $7.5B in enterprise value through 2 IPOs and 4 M&A exits. Gary holds an M.B.A. from the Marshall School of Business at the University of Southern California, where he was named Sheth Fellow at the Center for Communications Management. He also holds a B.A. with honors in Business from Arizona.

As a scientist, I value clarity—in every sense of the word. From the work I do to the conclusions I draw to the products (or policies) I buy, I act based on the clarity of the terms and conditions of the documents I sign; or choose not to sign, if the language is unclear, the provisos too ambiguous, the provisions too abstract.

Were I to act otherwise, unaware of the consequences and unable to bear the costs of my own ignorance, I would betray my commitment to clarity. I would also jeopardize or squander my family’s financial safety.

When in doubt, in other words, have an expert review the words. Have a lawyer explain the words, so the insurance you have is the insurance you need. Simply stated, assurance comes from ensuring you have the right insurance.

According to Reed Aljian of Daily | Aljian, a boutique litigation firm in Orange County, CA:

“Insurance can save a business millions of dollars and can change the landscape of litigation. But if you did not get the right insurance or you did not carefully review the policy to determine whether you have all necessary coverage, your premium payments could be worthless. This is precisely why hiring competent counsel early is important: Get the right insurance, and you could save yourself millions. Get the wrong insurance, or no insurance, and watch your business die.”

I agree with Reed Aljian for reasons both moral and monetary, because I think it is irresponsible to not know—to refuse to know—what insurance you need; while I know how ruinous it can be to dismiss the advice of counsel by trying to defy the odds and anger the oddsmakers, the actuaries who calculate the risks of every policy an insurer issues. I know the outcome from having seen employees lose their jobs and employers close their businesses.

We need sound counsel to help us choose just policies over unsound business practices.

We need to be unafraid to ask for help, too, because many of us are reluctant to admit or embarrassed to say we need help in the first place. But we need only remember a truth as old as the scriptures and as clear as a prelate’s personal constitution: Be not afraid.

In asking for help, we may receive the help we deserve.

When help comes in the form of a lawyer’s advice, when a lawyer clarifies what each form says, when the forms provide the right insurance to protect a business, the rewards belong to the many.

Insurers and lawyers thrive in such a scenario, as do business owners, because clarity is triumphant. So triumphant, in fact, that all parties may pursue their respective interests and champion their individual causes.

Let us work to achieve these goals, knowing that insurers and lawyers have much to offer.

Let us, therefore, resolve to be clear in our intentions, unequivocal in our needs and unwavering in our support of lawyers who can help us.

Get Involved

Our authors are what set Insurance Thought Leadership apart.