As we've seen with all the recent videos involving police and protesters, cameras are everywhere -- and the spread is just beginning. There will be major implications for insurers.

A truism in Silicon Valley is that you must never confuse a clear view with a short distance -- yet I still do, far too often.

I'm thinking, today, of cameras. I laid out a clear view in a book seven years ago of how the ubiquity of cameras would, among other things, rein in police officers. But the distance certainly hasn't been short. We're just now seeing, based on footage from officers' body cams and from bystanders, the beginnings of the sort of effects I thought would come quickly.

Therein lies a lesson, I think, not just for how slow technology adoption can be but also for the sorts of implications that having cameras everywhere will cause for insurers.

When Chunka Mui and I published "The New Killer Apps: How Large Companies Can Out-Innovate Start-Ups," in 2013, we said cameras were among six technologies that created the potential for a "perfect storm of innovation." (The others were mobile devices, social media, sensors, the cloud and what is generally referred to as big data, though we call it "emergent knowledge.") We said that, while it was surprising that someone had a camera available to film the Los Angeles police beating Rodney King in 1991, cameras would soon be wildly abundant as they shrank from the size of a brick to a dot on the back of a smartphone or other device and as the cost disappeared along with the bulk. So, filming of any abuses should become the rule, not the exception.

We assumed that police would become more careful. But many police departments moved slowly on outfitting officers with body cams and dashboard cams. Then some officers didn't turn their cameras on. Even when there was footage, some police departments tried to hide it (as Chicago did for more than a year following the 2014 death of teenager Laquon McDonald, shot 16 times after walking away from a police officer). Some acted as though there wasn't ample video from bystanders (the approach the Minneapolis police department took in its initial report on George Floyd, even though he was killed in broad daylight in the middle of a crowd). Only now, after a rash of killings of blacks by white officers, on camera, does there seem to be a recognition that cameras are everywhere, that footage will quickly become public and that officers and departments will be held to account for any abuses. And it remains to be seen how much the proliferation of cameras will change police behavior in the long run.

Based on how cameras have played out in police work, I have a clear view of what will happen with insurance as they shrink, decline in cost even further and show up everywhere -- but also a little more humility about claiming to know how short the distance will be.

We're already seeing cameras show up in security systems through doorbells such as Ring, and that opportunity should continue to develop. In addition, I see two major trends developing for insurers from tiny, ubiquitous cameras: 1) There can be a permanent record of just about anything (not merely interactions involving police), and 2) almost all inspections can have a do-it-yourself component -- with the client walking around, using his or her cameraphone at the direction of an insurance professional on the other end of the call.

I'd love to say that I came up with the idea about a permanent record, but it actually traces back to a project that the great Gordon Bell did for a book, "Total Recall," that he published in 2009. Gordon, who developed the first minicomputer and has numbered among computing's visionaries for six decades, had begun digitizing his life in 1998. He scanned all his letters, photos and memorabilia and captured everything he did on his computer. He layered on other capabilities, including an armband that tracked his vital signs and a camera recorder that took regular snapshots of what was in front of him and recorded everything he said.

While his sort of approach raises enormous issues related to the privacy of those he interacted with, the fact is that the technological capability will be there, and everyone, including insurers, will increasingly need to be prepared. Lots of good could come. Disputes about who said or did what when could mostly go away -- you just consult the video. Questions about the maintenance of a building or whether a floor was wet before someone fell might likewise just be a couple of clicks away from being settled. All sorts of fraudulent schemes would be easier to catch. But those privacy issues will be nasty, and loads of other complexities will surely arise.

Cameras will also speed inspection processes and take out a chunk of cost. A homeowner won't have to schedule an inspection with an insurer, wait a week for the inspector to arrive and arrange to stay home for a morning to show the inspector around. The homeowner will just walk around the house and video everything, guided by some combination of an AI and a person -- asking, perhaps, for the homeowner to zoom in on potential damage or on belongings that might be especially valuable. (I'm assuming a drone has already flown around the house to get the exact dimensions and inspect the yard.) The insurer would wind up with an exact record of what was in the house and could thus price more precisely, rather than just assuming that belongings amounted to some percentage of the total value of the house. The insurer could also easily request occasional mini-inspections, to stay current on the home's condition and on belongings.

The possibilities of improved security, permanent records and DIY inspections are just the beginning. Cameras cost next to nothing and don't even have to be connected to anything to be able to transmit pictures to you -- just include a Wi-Fi or cellular antenna in the chip that controls the camera and attach a tiny solar cell and battery, and you can put a camera anywhere. (Again, within privacy constraints. I am most decidedly against anything devious; I'm just sketching the technical possibilities.)

You don't need to stay earthbound, either. Toaster-sized satellites are now blanketing the Earth, creating ways to capture just about any image from above that you might like. Want to see how the roof on a house is faring? Done. Want to check on the financial health of a business you're considering insuring? Just use satellite images to count the cars in the parking lot at various times of the day. Want to keep an eye out for erosion that might put a property at risk? No sweat.

Again, with cameras, cameras and cameras come privacy, privacy and privacy issues. But the view is clear: The world will be blanketed with cameras, and they'll change the dynamics for many aspects of insurance. It's not at all clear, at least to me, how short the distance to those changes will be, but it never hurts to start thinking about the possibilities now.

Stay safe.

Paul

P.S. A personal note that makes me wonder how long we will be dealing with the health issues caused by the coronavirus:

A longtime colleague from the Wall Street Journal, Rich Regis, died this past week at age 67 of complications from illnesses he contracted when the World Trade Center towers collapsed on 9/11. Yes, going on 19 years ago.

It was clear quickly that Rich had been stricken by the toxic cloud that enveloped the WSJ offices, which were diagonally across the street from the South Tower. As his wife testified before a Senate committee in 2007, "Within 3 weeks... [Rich] succumbed to an autoimmune attack, which... led to kidney failure, shock liver, bowel perforations, sepsis and life support.... Doctors opened him up twice, vacuumed him out, replaced his blood, dialyzed his kidneys and re-sectioned his intestines three times."

Rich not only made it back to the WSJ but, before retiring four years ago after 35 years at the paper, cemented his status as a behind-the-scenes legend -- erudite and a pro's pro as an editor but capable of a remarkable variety of profanity, kind but commanding, easy-going but get the hell out of his way as deadline approached. "A gruff mensch," one colleague called him. The WSJ editor-in-chief lionized Rich in a memo Monday that described him as "the sort of character that many of us went into journalism to meet." RIP, Rich.

As a longtime observer of technology, I'm familiar with the concept of the "long tail" -- those Earthlink customers who still have dial-up internet connections decades after the rest of us moved on. As a devotee of the Civil War, I know that Joshua Chamberlain (hero of Little Round Top in the Battle of Gettysburg) became the last casualty of the war when he died in 1914 -- of a wound he suffered 50 years earlier. As a student of insurance, I'm well aware of the tens of billions of dollars that were paid in claims related to asbestos installed decades earlier. But I really thought we were about done with 9/11 deaths.

Now I wonder how long COVID-19 will be with us, given that so many of those who have officially recovered and been discharged from the hospital suffer from myriad, mysterious, debilitating problems.

P.P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

None of us knows what the future holds. But at least prior to March, we had logical bases from which to de-risk decisions.

In the space of a few months, the logic behind our assumptions no longer feels solid. We’ve ripped up our plans. What will happen, when things will happen and how long things will take to happen are all less certain. We are recreating our what to do’s, how to do’s and when to do’s one day at a time.

Back on March 17, NY Times columnist Thomas Friedman referred in an OpEd piece to BC and AC – Before COVID and After COVID – as “our new historical divide.”

Before COVID, the pace of technological change drove everything else

Tech-driven change, as complex as it has been, now feels simple compared with the many dimensions of change triggered by COVID. Who knows what After COVID will look like or, more disconcerting, when we will get there?

What is certain:

Tomorrow is going to look dramatically different than today.

Some habits and practices may return, but we are not going back to the BC world.

No matter how much we may want to revert, things we counted on and cannot control will be gone, other things will change and there will be many new things that we cannot yet even imagine. We will let go of things that used to seem vital, behaviors will change (they already are changing!), business models will die and emerge and globally society will reshape around different norms.

The AC world will be an even greater departure than what we experienced post 9/11

I think back to how much the world changed in 2001. Then, out of extreme fear, I had avoided getting on a plane for months. I remember what a rude awakening that first trip from curbside to the gate at Newark Airport was — my water bottle confiscated, my manicure scissors (a very special set from my mom given to me as a teenager) disposed of because I had mistakenly packed them in my carry-on, the “wand exam” in security because I was the ‘nth’ person in line, so subjected to an extra special check.

How can we prepare when we don’t know what we are preparing for?

There is one foolproof control mechanism we can all deploy at the front end of our future plans. Even before implementing return-to-office plans that ensure employee safety, redesigned customer experiences that meet new needs and tactics that stabilize disrupted supply chains, get clear on your brand’s purpose. Why you exist. Why you matter to the world.

Affirming your purpose will give focus to how you navigate the BC to AC change – it’s a step that won’t clarify everything for which you need to be prepared, but it will make clear to everyone where you are going. That counts for a lot.

Purpose-driven brands achieve 12X the returns in the long run over other brands. In the AC era, as we face unknowns that will force us to make decisions under uncertainty, purpose will be an absolute must-have. Yet, only 27% of customers can name a purpose-driven brand.

Why besides massive ROI leverage is purpose essential? According to a study published in Harvard Business Review, only 28% of employees report that they know their company’s brand values. Getting people back to the office creates a long list of issues. Aligning people to a new direction will be a taller order, where you can succeed if everyone knows why they are there, why the brand exists and where they are heading.

At a refreshingly fast-paced interactive be radical workshop I attended recently, breakout groups developed and shared purpose statements in just two minutes each. This assignment will surely take longer in the real world, but the exercise proved that it can be accomplished with speed.

Right now, we could all use greater clarity. A good purpose statement provides utter clarity around what you are doing. It sets a North Star, telling your team, vendors, partners, other collaborators toward what destination to head, what they are doing and why they are doing it. The statement beats command-and-control operating because it is far more practical, agile and empowering.

Best of all, a good purpose statement allows you to say “NO” – it helps you be clear about your choices.

Crystallizing your purpose now, or pulling yours out and making sure it still works, will help with all of the decisions you are making daily even in the face of tremendous ambiguity about what even the next few months may bring.

Amy Radin is a strategic advisor, keynote speaker, and Columbia University lecturer focused on why transformation succeeds or stalls in large, complex organizations.

Drawing on senior leadership roles at Citi, American Express, and AXA, including one of the world’s first corporate chief innovation officer roles, she helps leaders build the capabilities required to absorb, scale, and sustain change.

The insurance industry is experiencing seismic shifts in day-to-day operations stemming from this invisible yet intensely disruptive contagion COVID-19, but early signs of longer-term trends are also starting to emerge. A few short weeks ago, who would have thought that human health/safety and operational resilience would become the top two drivers of digital transformation? This pandemic has redirected our focus right at the base of Maslow’s hierarchy of needs overnight.

Organizations are overhauling operations to ensure the safety of employees and customers while business continuity and contingency plans are being put in place to ensure acceptable service for customers in this new normal. Insurers are focusing on retaining cash reserves while balancing customer retention with rebates, due to sheer uncertainty of the recovery timeline. Eventually, the obstacles presented by COVID-19 are giving way to new growth opportunities.

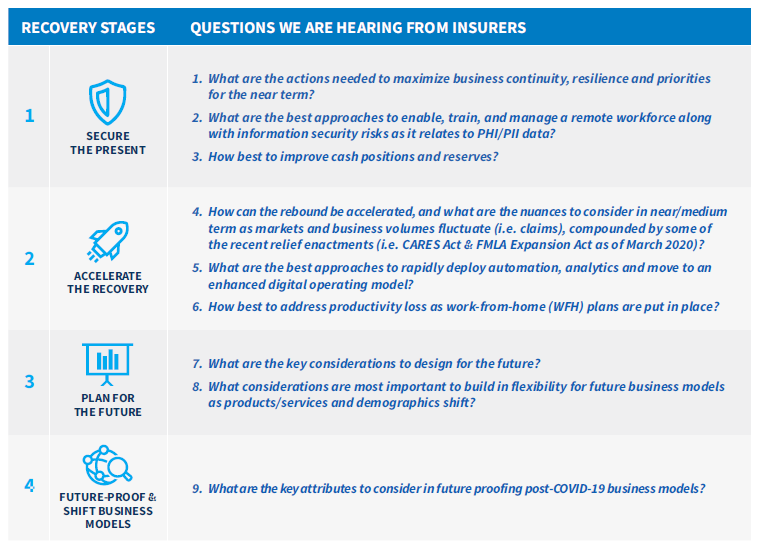

Based on our conversations with our insurance clients, some of the categorical questions being asked are represented in the table below. This paper addresses these key questions with a view to the “Future of Work” and key elements to consider in each of these stages.

Improving Resilience by Accelerating Digital With a Virtual Workforce

Moving not only in response to the present situation but also in preparation for the “Future of Work” will be the key differentiating factor between the leaders and laggards as the industry arrives at its new normal. The key areas that insurers are examining for current challenges and tomorrow’s opportunities fall into the following categories:

Resilience for Near-Term Business Continuity: Insurers are embracing digital channels and have moved to makeshift, pseudo-digital business models essentially overnight to ensure business continuity. In the medium to long term, this will accelerate the digital transformation agenda as it offers intrinsically contactless business, reducing health risk and improved resilience -- in addition to typical transformation targets in growth, delivering customer experience cost-effectively and deploying/testing new products and services at lower costs. As reserves deplete and loss ratios are affected, insurers will soon prioritize these efforts to lower the cost of operations while improving resilience and addressing customer and employee health/safety.

“Distance-Independent” and “Zero Paper” Business Models: In the near term, face-to-face meetings with agents and brokers to discuss policies or with adjusters to file a claim are extremely challenging. Customer journeys need to be modified to enable every step and interaction to happen anywhere and at any time. Paperless claims, data-driven underwriting and fully digital policy maintenance will be critical for longer-term growth and viability.

Resilience in Workforce | Location Independence: We have witnessed a global shutdown in travel, businesses and borders to combat COVID-19. Some experts predict that, while many of these areas may relax these restrictions within a few months, the bans may need to go back in place if there is a resurgence in infections. Consequently underscoring the need to have a workforce – no matter whether these employees are nearshore, offshore or onshore – enabled and equipped to operate from anywhere.

Building Resilience in Operations and Business Models

Organizations are under stress, and so are employees and customers, due to the uncertainty of the recovery timeline. Some are saying the overall economic impact may be far greater than the recession in 2008. Insurers are beginning to realize the importance of digital as a way to enable resilience and are designing it into core operations, technology and the digital workforce while removing reliance on physical locations.

The illustration below depicts how to build resilience into every level of the business, including core operations and technology, the digital workforce and the physical workforce as new business models emerge. Agile, design thinking, cloud enablement and DevOps will also drive quicker iterations to target states; by definition, these will need to be short-run, multi-week/multi-month, not multi-year, initiatives.

Figure 1 - Three rings of resilience as post COVID-19 operating models evolve

Physical Workforce

Remove paper and physical contact points internally and externally to deliver services. Deploy chat/digital channels for customer self-service.

Achieve location-independence through WFH capabilities and reduce workloads by automating away low- and medium-complexity transactions.

Enable better employee experience through rapidly deployable attended/unattended automation to boost employee productivity, offsetting any short-term, WFH-related productivity loss.

Redeploy physical workforce to drive customer experience on high-complexity product innovation or high-impact planning and growth work.

Encapsulate operations with digital capabilities for continuity and offset loss in productivity.

Reduce people-dependent physical interactions and expensive voice and paper interactions while improving CX.

Redeploy moderate- and high-complexity customer interactions for human agents.

Accelerate self-service through chat and voice for low-touch flow transactions.

Core Technology and Operations Capabilities

Resilience in core operations across essential customer touchpoint functions: claims, policy maintenance, underwriting and new business/onboarding (for new offerings post-recovery).

Capacity to deal with spikes in volumes as markets head to a new equilibrium.

Rapidly enabled remote employee hiring, onboarding, training capabilities and WFH operations monitoring.

Moving Forward

For the next three to six months, most companies will be operating to “keep the lights on,” with the focus on delivering essential services and maintaining operations. While this period will be fraught with tactical challenges, it will eventually end; when it does, businesses can look ahead to the future and the opportunities it presents.

We have phased the coming months into stages to prioritize the recovery path and a way forward to the longer-term business model.

Figure 2 - Working through the stages of COVID-19 recovery

Stage 1 | Secure the present: This first phase will be spent protecting core operations and ensuring customer experiences aren’t disrupted across processes as volatility recedes and we head to the new equilibrium.

Question 1: What are the actions needed to maximize business continuity, resilience and priorities for the near term?

Digital and analytics will help address scale and volume variability while lowering operating costs, providing overall cost-per-claim improvement and enabling straight-through processing for low-complexity claims. Additionally, rapidly deployable attended automation can take care of many routine, repetitive tasks and drive efficiencies for underwriters and adjusters on their present-day desktops. For instance, this would include policy lookup, claim filing and data aggregation for underwriting and, consequently, free capacity to focus on complex cases requiring human intelligence and understanding.

These digital interventions lead to improved resilience and enable improved customer service, the most important aspect right now for insurers. Companies that fail to retain their current customer base will create post-COVID-19 drain on margins and cash reserves, especially if the recovery period is protracted. The good news is that, with relatively low-cost yet focused investments and interventions, the simpler transactions can rapidly be ramped onto digital channels, with the added benefit of making employees more productive in the WFH environment.

Question 2: What are the best approaches to enable, train and manage a remote workforce along with information security risk?

Remote hiring, onboarding and training with capabilities to coordinate and monitor WFH workforces are fast becoming new capabilities organizations are building out of necessity to react to near-term operational needs.

Clearly, information security is of critical importance. InfoSec controls span three areas across technical (e.g., encryption, multi-factor authentication), administrative (e.g., role-based security and credentials, data minimization/masking, read-only rights) and physical controls (e.g., supervisory and location-centric monitoring). Risk control self-assessments (RCSA) initiatives will need to be modified to ensure effectiveness of technical and administrative controls, while computer vision and initiatives emerge to augment physical controls.

Operational controls, key performance indicators (KPIs) and metrics are rapidly being updated to look at leading indicators to improve reaction time, exercise operational control on WFH workforces and ensure service continuity. Updated run-books, procedure guides and laptop-camera-enabled monitoring are all making their way into the WFH ecosystem.

Question 3: How best to improve cash positions and reserves?

Building a cash reserve and identifying opportunities for freeing cash flow to drive innovation will also become a parallel priority, as the timeline for recovery is unknown today.

L&A providers are preparing for larger claim payouts and potentially longer-duration disabilities, due to flexibility in parameters stemming from the COVID-19 stimulus package. In P&C, auto insurers have already declared refunds on the premium to control the cancellations due to non-payments. The industry anticipates a higher delinquency quotient, which will require ramping up billing and collections function to recapture potentially lost revenue. This will also create an opportunity for machine learning, analytics and automation-enabled tools to drive efficiencies in the collection function.

Apart from traditional approaches, high-impact, near-term digital interventions and no-code rapid deployments will also help free cash flow with relatively short paybacks. Success factors, however, will depend on focusing on multiple benefit areas and the ability to deploy robust solutions quickly where volume volatility exists. Additionally, service and capabilities are going to be more important than ever, particularly those that are low-effort yet data-driven and can accurately and quickly identify the right opportunities for digitization or automation.

Stage 2 | Accelerate the recovery: Once infections slow and countries begin lifting their stay-at-home orders, insurers can move from focusing on basic operational continuity to building more resilient business models. The focus will quickly move to getting back to normalcy.

Question 4: How can the rebound be accelerated, and what are the nuances to consider in near/medium-term business volumes that will fluctuate (i.e. claims), compounded by some of the relief enactments (e.g., CARES Act & FMLA Expansion Act as of March 2020)?

Digital tools previously seen as ways for cutting costs or increasing efficiency are now essential. They offer protection against similar events or regional COVID-19 outbreaks that could disrupt operations by reducing reliance on human labor through automation, analytics and machine learning. Initially, these efforts will focus on new business/onboarding, then underwriting when the time arrives for new policies to be written. Subsequently, they will help free capacity and mitigate operational, compliance and audit risks as regulatory parameters evolve and changes are made to COVID-19 relief acts throughout the recovery cycle.

Control room functions and tight controls on projected volumes will be essential to ensure scale up/down of digital and human labor to meet changing volume. As a result, digital and human workforces will need to be tightly integrated to enable stable operations and deal with volatility as the relief acts and market dynamics cycle through periods of volatility.

Question 5: What are the best approaches to deploy automation and move to a digital operating model?

The global nature of this crisis demonstrates the need for insurers to take a second look at their location strategy, re-tooling and re-engineering their workforce for maximum resilience. It’s not so much about whether employees are onshore or offshore – it’s about being able to sustain operations regardless of external circumstances. Enabling the remote workforce to be augmented through digital capabilities, whether attended or unattended automation, becomes a key consideration, as this will not only ensure consistently higher service quality but also reduce training needs as staff are hired.

Question 6: How best to address productivity loss?

A primary focus is on achieving location independence through WFH capabilities and reducing workloads by automating away low- and medium-complexity transactions. This includes enabling better employee experience through rapidly deployable attended/unattended automation to boost employee productivity and offset any short-term, WFH-related productivity loss.

Stage 3 | Plan for the future:Shifting from human-centered to digital processes can help companies be prepared for future surprises like the COVID-19 crisis. The key lesson learned is how we think about future models with resilience and flexibility designed in for future sudden shifts in the market.

Question 7: What are the key considerations to design for the future?

Machine learning and intelligent automation will be more important than ever in a post-coronavirus world for both employees and customers; these capabilities will provide customized experiences for a segment of one, tailored to that worker's or consumer’s preferences.

As the next normal settles in and is run for a sustained period, new challenges will emerge and will need to be addressed, especially for workforces in developing countries. One way to address this is to organize work into micro-teams (or pods) and ensure a hub-and-spoke model exists from function leaders through to individual staff. The intention is to drive collaboration and self-directed work reallocation at the micro-team level, when unforeseen circumstances affect a team member.

Question 8: What considerations are most important to build in flexibility for future business models as products/services and demographics shift?

The best way to explain this is to reimagine the future model the same way the larger internet natives have to build their platform business; essentially, to build a layered, or “iPhone,” view to redesigning for the future with:

(a) Foundational capabilities (i.e., physical hardware) across operations, paper/document ingestion, operational capabilities and supporting functions with staffing/WFH.

(b) Functional layer (i.e., operating system or iOS) to include digital capabilities and flexibility for new products/volumes across new business/underwriting, claims, policy maintenance and finance/compliance/audit functions, which are common and reusable to different products and lines of business (LOB).

(c) Product- and LOB-specific capabilities (i.e., apps on the iPhone) across core and specific new products enabled end to end through digital channels and automation capabilities. The goal is to flexibly and inexpensively add, delete and modify new products, such as credit insurance products, short-run coverage for specific regional risks products, parameter changes to categories of policies etc.

Stage 4 | Future-proof and shift business models:The problems insurers faced before COVID-19 may exist once the virus is no longer a pressing concern, but interventions of today should be thought through with the longer-term transformation in mind.

Question 9: Key attributes to consider in future proofing post-COVID-19 business models.

Organizations will look to redesign their business models to be more resilient against competitors now as well as pandemics or emerging regional risks.

This will give rise to “death of distance” or “physical contactless” business models, with ways of operating that can be done from any location. This includes offering products, services and delivery through fully digital channels. This will include providing straight-through underwriting for simple policies, and enabling customers to video conference with an agent for more complex or high-touch services.

Insurtechs, fintechs and other digital natives will exert competitive pressure on legacy insurance companies. Conversely, post-pandemic liquidity and access to private equity and venture capital will create interesting acquisition opportunities for insurers. Focused acquisitions may help leapfrog innovation in customer interaction and operational and distribution areas, but the key will be in the appropriate integration of these acquired capabilities at scale.

Conclusion: Digital as Key Enabler of Contactless, Distance-Independent and Resilient Business Models

COVID-19 has shown how situations can radically disrupt operations overnight. However, it’s also shown that people are equipped to adapt quickly and overcome global business challenges.

Insurers have a significant opportunity to thrive by building in resilience, rapidly deploying contactless business models, lowering reliance on physical locations and leveraging WFH capabilities. All of this needs to be executed with speed, agility and decisive action to assess, align and adapt quickly to the new reality.

Digital, automation, machine learning and analytics will enable future business models and have now become essential ingredients to long-term success, with a renewed focus on health/safety and resilience as well as customer experience and efficiency. However, the right digital capabilities must be applied to produce well-defined and achievable outcomes and are as important in “accelerating the recovery” as they are to designing the “business models of the future.”

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Imagine that you wake up one day in the future and you read this headline:

“Auto insurance is no longer being sold.”

The article says accidents are rare or no longer possible due to autonomous technologies, hundreds of new safety features, an entirely new methodology for handling vehicular risk and a dramatic reduction in the personal ownership of vehicles. When claims events do happen, they are covered by the manufacturer or simply paid for out of a reserve created by a globally pervasive mobility corporation.

If this seems far-fetched, you will want to read Majesco’s latest report, “Rethinking Auto Insurance: From a Transactional Relationship to a Mobility Customer Experience.” Though auto insurance is unlikely to go away any time soon, premiums are beginning to decline and will likely continue to decline in the coming two decades at a rate much faster than many would like to admit is possible. This decline will force auto insurers to reinvent themselves in ways that are both challenging and exciting. It will be the end of auto insurance as we currently know it, but it will be the beginning of mobility experience and ecosystems that could improve insurers’ profits with new revenue sources.

Four years ago, we published our first Future Trends report (with an update to the report in December 2019) that examined a major shift unfolding due to the converging “tectonic plates” of people, technology and market boundary changes disrupting and redefining the world, industries and businesses — including insurance. In particular, these trends are changing traditional auto insurance. Majesco’s new report goes one step further to answer two highly pertinent questions:

What trends are pushing auto insurers to adapt their business models?

Why should auto insurers begin creating mobility experiences and ecosystems that will transform their purpose and their profits?

In today’s blog, we examine the high-level trends that are affecting auto insurers and take a peek into how insurers are likely to adapt and respond. We’ll cover:

Customer, Technology and Market Boundary Changes

The Generational Shift in How Transportation Is Perceived and Used

The Auto Insurance Transaction vs. a Mobility Customer Experience

Customer, Technology and Market Boundary Changes

In February, Uber said that 10% of U.S. millennials who ride with Uber have changed their car ownership behavior. Due to increased costs of vehicle ownership, environmental consciousness, technological innovation and the availability of mobility through Uber, millennials are choosing to get rid of a personal vehicle or choosing not to buy a car.

Because of the customer, technology and market boundary changes, traditional auto insurance is under growing pressure and threat from many fronts, including:

The growing use of non-owned vehicles and mobility options like rideshare, rentals (traditional and shared economy) and other local rental options like scooters and bicycles, reducing the market size for individual auto insurance purchases.

Non-insurance providers that offer/embed insurance for vehicles and other mobility options, potentially cutting off traditional carriers from these opportunities.

Increased effectiveness of safety technology, putting more emphasis on prevention and less on traditional indemnification, potentially depressing auto insurance premiums. It is estimated that advanced driving assistance systems (ADAS) features and enabling technologies increasingly included in new vehicles can reduce losses 20% to 30%.

Connected devices that enable improved data, beyond telematics, such as mileage, location, weather-related and driving behavior. This is allowing for real-time, data-based underwriting and pricing, which could lower premium volume or make it less predictable.

Auto manufacturers that are leveraging their customer relationships and data to offer insurance, repairs and services (Porsche, Volvo, Tesla, Ford, GM, etc.). They are recasting themselves as “mobility companies.”

The rise of on-demand insurance, expected to increase 30% by 2026.

The rise in testing and use of self-driving vehicles and robots due to the COVID-19 pandemic for contactless deliveries, which could accelerate a shift to a future of autonomous/semi-autonomous mobility marked by fewer accidents.

The Generational Shift in How Transportation Is Perceived and Used

Adding to the pressure on auto insurers is the shift in generational views on transportation, mobility and product expectations for auto insurance. Within the report, we discuss the shift between millennials and Gen Z versus Gen X and Boomers, including:

28% of the younger generation currently use a device or app to record mileage and driving behavior — compared with 15% for the older generation – nearly a 100% difference.

11% rented someone else’s car through a sharing service, and 9% rented out their car, versus 2% and 1% for the older generation.

30% of the younger generation are using or would use an all-inclusive vehicle subscription service – nearly four times higher than the older generation, indicating interest in different mobility options as opposed to owning a vehicle.

40% of the younger generational segment would pay $10 per month for a mobility solution with access to a wide array of services. Only 20% of the older generation is interested in this — a 100% difference.

The younger generation is two times more likely to:

buy auto insurance from a car shopping website or a vehicle manufacturer website,

have insurance included in the purchase or lease of a vehicle,

buy insurance from Amazon or Google.

Auto insurers must reimagine the scope of what they will offer to customers – an experience with a risk product, value-added services that are part of a broader mobility ecosystem and a compelling customer experience. This is where exciting new business opportunities await. And where new competitors are emerging, including automotive companies, ride share companies and others.

The industry status quo for auto insurance is rapidly eroding. Insurance is being re-defined with a growing number of influences, upending decades of business assumptions. In this new decade, a fresh auto insurance opportunity exists for those who will participate in a broader mobility ecosystem and the growing number of insurable situations.

The Auto Insurance Transaction vs. a Mobility Customer Experience

As a result of all of these changes, the greater threat may be auto insurers’ continued 100-plus-year-old view of auto insurance as a policy transaction.

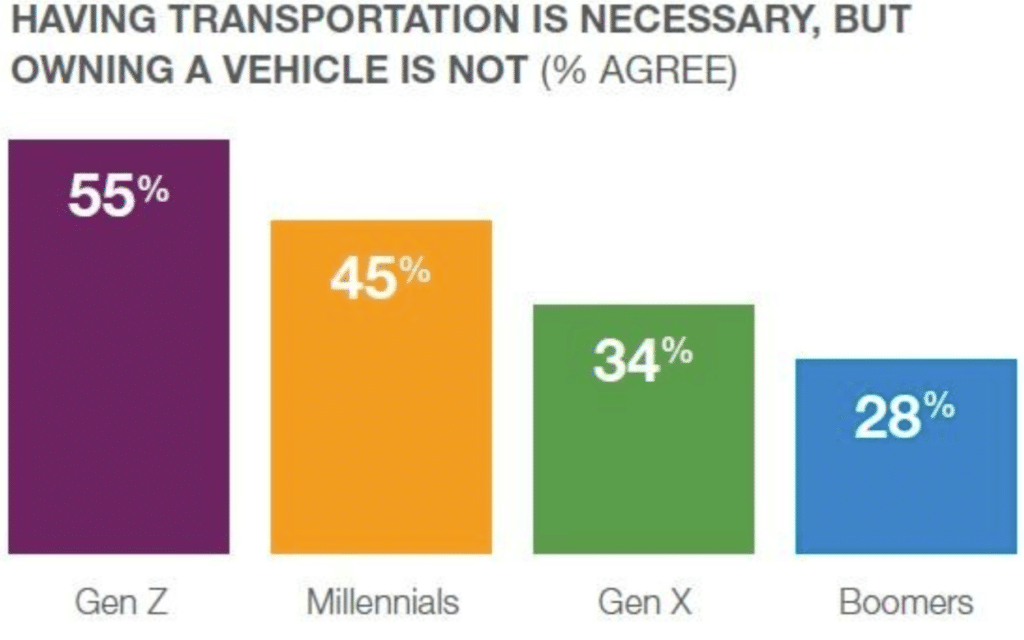

With so much change around transportation options and automotive, companies outside insurance are coalescing around a shift to “mobility.” From the decline in car ownership for the first time since 1960, with 9.1% of households in 2015 having no cars, to the rise of ride-hailing and car-sharing services, a plethora of transportation options continue to expand.

According to a survey from Cox Automotive, nearly 40% agree that having transportation is necessary, but owning a vehicle is not. Most interestingly, among millennials, the rate jumps to 45%, and for Gen Z it jumps to 55%, as reflected in Figure 1. This implies that mobility options are important but can be fulfilled by many means beyond traditional vehicle ownership … a significant shift affecting business models from automotive companies to insurance companies alike.

Figure 1: Importance of vehicle ownership as a mode of transportation

These shifting customer, market boundary and technology trends are creating a new market segment called “mobility” that brings together different elements of other markets or industries, including insurance. Unfortunately, for customers the current experience is fragmented, inconsistent and difficult at best, as they interact with disparate entities to complete necessary tasks across the mobility journey. These would include everything from financing a vehicle, to using and maintaining that vehicle, to selling that vehicle. You could also include transactions such as renting a car, parking a car, purchasing tickets for public transit, using public scooters and bicycles and, of course, maintaining insurance for any of those tasks.

Customers currently have to work with the different parties individually, requiring time and inducing frustration, meaning that customers may reduce, reallocate or eliminate a substantial portion of today’s auto insurance premiums. Insurers must rethink their scope away from an auto insurance transaction to a broader mobility experience that redefines and includes:

Insurance Product: Product (risk, services, experience) redefined but requiring insurance to participate and play within ecosystems, rather than simply existing as an ecosystem unto itself.

Mobility Policy:One unified policy to cover whatever mode of transportation a customer chooses, instead of separate policies for each.

Value Added Services:Risk protection services as a component of an ecosystem that provides a single place for all of the “jobs” a customer needs to get done across the mobility customer journey – providing a powerful, single engagement and eliminating points of friction between the different participants of the ecosystem.

Continuous Underwriting:Constantly updating the risk profile of an individual or thing that changes the terms and pricing, influenced by the continuous flow of data from autos, telematics and IoT devices.

Highly networked, data-driven, value-added mobility business models are rapidly emerging, primarily outside of insurance. Automotive companies like Tesla, Ford and GM are leading this shift along with platform companies like Uber. They are redefining the customer journey, and the entire customer relationship, across a broader set of transportation options.

These shifts will push auto insurers into new realms of business, expanding their definitions of product and service and making them much more relevant to the daily life and experience of each customer.

In our next blog, we’ll look at real evidence from a recent Majesco survey that confirms the trends we have highlighted above. We’ll look at the specifics of two major demographic groups and what they are looking for in their mobility experiences. We will also look at what they are currently doing regarding mobility and technology versus what changes they are considering for the future.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

I’ve seen many insurance trade press articles or social media posts asking why insurers aren’t using either an Amazon or Netflix business model. The articles or posts mention that Amazon and Netflix are massively successful, are driven by a strong customer focus, have operations throughout the globe and, equally importantly, conduct commerce using web-based mobile apps.

So, should insurers use an Amazon or Netflix business model?

No.

I'll explain why, and also cover the functional areas within the insurance value web that can be strengthened using aspects of or principles driving the Amazon and Netflix business models, but let's start at a very high level. Let's look at: business models, the Amazon business model, the Netflix business model and the insurance industry business model.

I always keep in mind that the insurance industry is not homogeneous. However, for the purpose of this post, I will illustrate an insurance business model that has applicability – at a high level – to all of the non-health-insurance lines of business. Please excuse my broad brushstrokes of the insurance business model that I visualize.

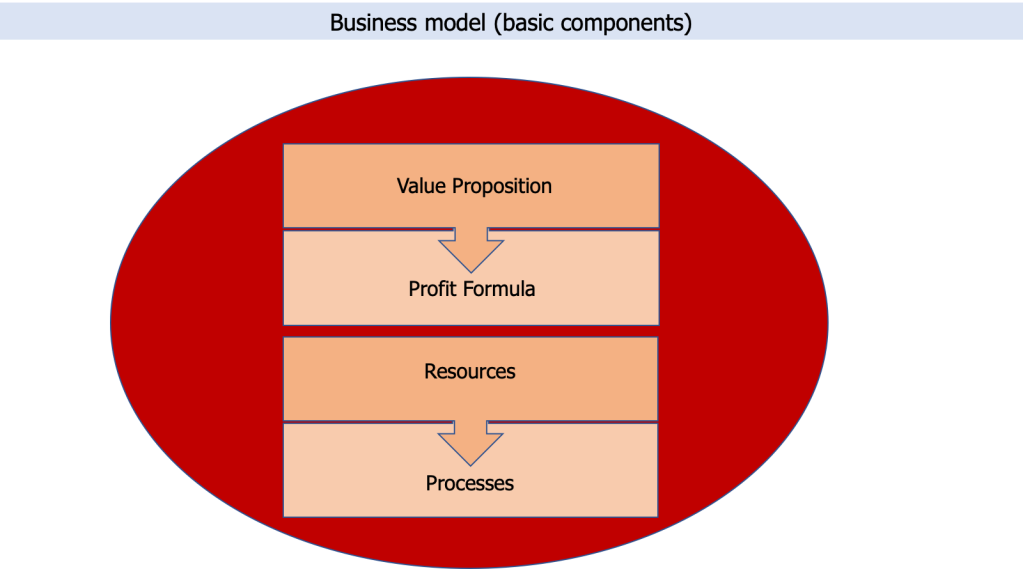

There are many descriptions of business models available from a multitude of sources. I’ve created an illustration from an interview that Harvard Business Publishing had in late 2008 with Professor Clayton Christensen discussing “reinventing your business model.”

To paraphrase Professor Christensen’s description:

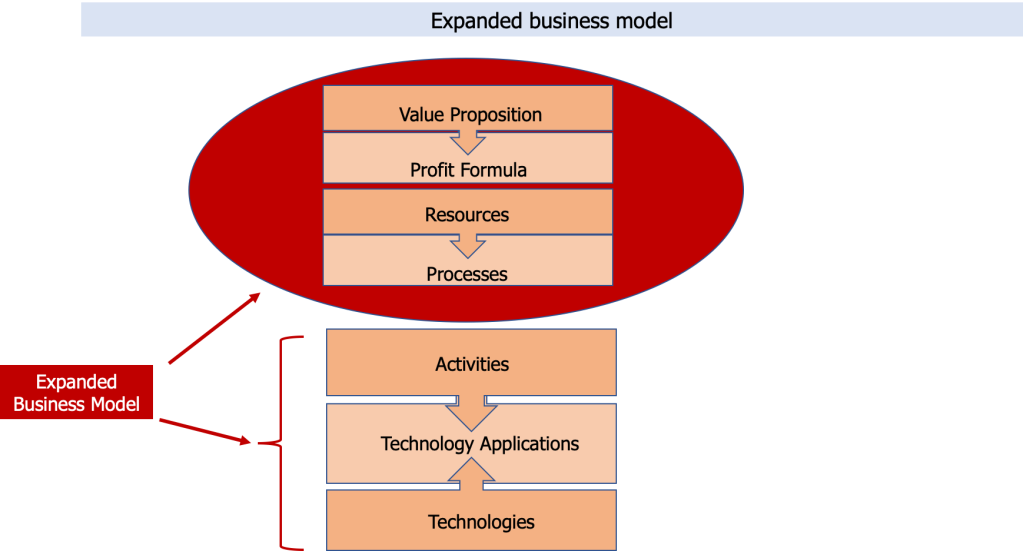

First, a firm creates a value proposition. The value proposition is defined in a manner to help someone accomplish a "job" (i.e., fulfill a need) affordably, conveniently and effectively. Next, the firm establishes a formula to deliver the value proposition in a profitable manner. Then, the firm identifies the resources it needs (i.e., buildings, equipment, people, products and technology) to support the value proposition (and deliver it profitably). Finally, processes coalesce that are required to support the firm’s value proposition and resources simply and affordably.

Expanded Business Model

For me, this is a reasonable, logical description of a business model before factoring in the forces within a specific industry that will alter the components to align with them.

However, I want to expand on Professor Christensen’s business model components. My expansion (see visual below) encompasses three other major components: activities, technology applications and technologies.

These three additional components resemble Russian nesting dolls in that processes are composed of several activities. Each activity can be – and usually is – supported by several technology applications, and, in turn, each technology application can be – and usually is – supported by several technologies.

I think of my three additions to Professor Christensen’s description of a business model as an "expanded business model."

Firms regardless of industry, whether startups or incumbents, need to consider how the set of additional components enable the company to profitably deliver the value proposition (i.e., help a customer fulfill a need) affordably and simply to the company’s target markets -- again, “with regard to the realities of the industry in question.”

For this post, I will not use all of the aspects of the expanded business model to discuss the Amazon, Netflix and insurance industry business models. However, to maintain your sanity and mine, I will discuss the same three elements of the expanded business model (value proposition, profit formula and technology applications) throughout this post.

(I believe that a more extensive discussion encompassing all the components of the expanded model would make sense to write at some point. I’m not sure when I would get to do that.)

Amazon: Industry, Markets and Business Model

In the 2017 letter to shareholders, Jeff Bezos wrote: “One thing I love about customers is that they are divinely discontent. Their expectations are never static: They go up. We didn’t ascend from our hunter-gatherer days by being satisfied. People have a voracious appetite for a better way. And yesterday’s ‘wow’ quickly becomes today’s ‘ordinary.'”

I submit that his company strives to continually provide contentment for his clients in both the consumer and corporate markets that Amazon targets. Whether he succeeds with every initiative, Bezos – based on recorded interviews with him, his letters to shareholders and the stream of new capabilities offered to clients – is driven to continually satisfy people’s voracious appetite by finding a better way for clients to conduct commerce with Amazon.

Amazon Industry and Markets

Industry Description – NAICS

The U.S. government has categorized Amazon as belonging to:

NAICS code 518210: data processing, hosting and related services

NAICS code 454110: electronic shopping and mail-order houses.

Note that on a NAICS two-digit level, code 51 encompasses “information” industries, and code 45 encompasses “retail trade” industries.

During my desk research for this post, at first glance it seems that Amazon employs its products, solutions and services from both industries. However, it is more applicable to state that Amazon learns from and leverages its capabilities in each of its NAICS-coded set of industries to satisfy its clients' “voracious appetites” in both of its target markets.

Target Markets

The company began its operations in the consumer markets (selling hard-copy books) in 1994, and in 2004 the firm decided to offer AWS’ Simple Queue Service (and in-depth knowledge of maintaining, enhancing and managing that infrastructure) to clients in corporate markets. A Wikipedia entry about AWS states that: “Amazon Web Services was officially re-launched on March 14, 2006, combining the three initial service offerings of Amazon S3 cloud storage, SQS and EC2.”

Again from Wikipedia: “In 2020, AWS comprised more than 212 services spanning a wide range including computing, storage, networking, database, analytics, application services, deployment, management, mobile, developer tools and tools for the Internet of Things.”

Four principles guide consumer and corporate markets

Bezos stated in the firm’s 10-K for the fiscal year ended Dec. 31, 2019, that the company seeks “to be Earth’s most customer-centric company.” He wrote that the firm is guided by four principles:

customer obsession rather than competitor focus

passion for invention

commitment to operational excellence

long-term thinking.

At the 2012 re:invent Day 2 conference, Bezos said that the firm’s obsession with retail customers was the same as with corporate AWS customers. He said it was necessary to continually:

improve the reliability of AWS

lower prices for AWS clients

innovate faster APIs for AWS clients.

Constantly lowering costs for customers is part and parcel of the firm’s customer obsession. One major theme that weaves through interviews with Bezos and articles about Amazon is the firm’s drive to answer the question: “How can we generate more revenue from our own infrastructure to lower costs for our (consumer and corporate) customers?”

Summing up Amazon’s consumer market

I think of Amazon as a firm that offers a fusion of physical and digital artifacts, specifically:

purchased physical and digital artifacts, supported by

a supply chain (encompassing digital and physical artifacts supported by servers, distribution centers and delivery vehicles), which are in turn supported by

Amazon’s technology solutions (including AI applications used to quicken and improve customers’ navigation, search and selection of known and predicted consumer product goods (CPG) and media and entertainment products that they might want to consider for future purchase.

I assume that a description of Amazon’s corporate markets, beyond stating that AWS offers scale-as-a-service, could be crafted in a manner that is similar (and more than likely much tighter) to my summary about Amazon’s consumer markets.

However, whether thinking of Amazon’s offerings to its consumer markets or corporate markets, I consider Amazon.com to be an optimization engine that is continually refined to provide retail and corporate customers with an excellent experience conducting commerce with the firm.

Now, let’s discuss the three selected components of the expanded business model (value proposition, profit formula and technology applications).

Value Proposition

I believe that Amazon has two value propositions: one for consumer markets and one for corporate markets. Both are based on the same foundation of customer obsessiveness.

Value proposition for consumer markets: Provide consumers a panoply of digital and physical distribution channels to purchase products from a growing selection of retail and information goods and services at low prices and deliver quickly.

Value proposition for corporate markets: Provide corporations a secure, scalable cloud services platform offering storage, compute, analytics and other capabilities-as-a-service at low prices.

Amazon generates revenue from a wide and expanding selection of sources, including:

retail (CPG)

media and entertainment (including Amazon Prime, a subscription service for consumers)

corporate markets (AWS)

digital advertising services.

Some of the relatively newer sources of revenue include Amazon’s entry into prescription drugs and groceries (Whole Foods).

Amazon continually strives to find ways to make it easy for its retail consumers to conduct commerce with the firm, not only using mobile apps and the firm’s web site, but also using its voice-responsive Alexa devices and, more lately, shopping at the Amazon Go stores. Amazon is offering its Amazon Go store functionality to other retailers.

Amazon’s net income in 2019 was $11.59 billion, which was up from $10.07 billion in 2018.

Amazon Flywheels: Consumer and Corporate Markets

The firm accomplishes its mission through its stellar implementation of the flywheel, which Jim Collins described in his 2001 book, “Good to Great.” The flywheel strengthens the retail and corporate client experience while simultaneously lowering the firm’s expenses.

One of the best discussions of the Amazon flywheel is given by Simon Torrance (dated April 9, 2018, on YouTube and titled: "New Growth Playbook – Amazon’s Growth Flywheel"). I am using his visual below (with his permission) with some minor alterations.

Amazon continually expands the selection of goods and services for customers to choose (which is why it is number 1 in the visual: It drives the flywheel). Doing that increases traffic to Amazon.com. That traffic both drives expanding selection of goods and services and lowers Amazon’s cost structure, which leads to lower prices. And around the flywheel goes.

But wait a second: Amazon allowed third parties to use Amazon’s infrastructure to offer their own goods and services. Doing this accelerates the speed of the flywheel: increased selection leading to even stronger customer experience and …

Amazon’s implementation of the flywheel also illustrates the firm’s realization that it could leverage knowledge of its own infrastructure by offering that infrastructure (i.e., AWS) to corporations for their use to serve their own clients. Moreover, the visual captures how Amazon bridged the consumer and corporate markets to help their corporate clients, their consumer customers, their Amazon Marketplace participants, IoT developers (in this instance) and, of course, Amazon itself. By introducing its own branded connected IoT physical devices (Alexa, Fire TV Stick), Amazon introduced and accelerated purchases (and the corporate flywheel) that corporations could create and deliver to Amazon’s customers, which strengthens, yet again, Amazon’s experience for consumers.

Technology Applications

(I distinguish between technology and technology applications. For me, AI is a collection of technologies and is not itself a technology application. In this section, I discuss a small selection of technology applications that Amazon uses to strengthen customer experience.)

Amazon constantly strives: to make it easier for consumers to conduct commerce with the firm, to drive down the firm’s costs and to expand the number of retail (CPG) and media and entertainment goods and services that customers might want to purchase. Add all of that to one of the firm’s four principles – its passion for invention – and it is no surprise that Amazon is essentially a CX-driven laboratory that continues to create applications from current and emerging technologies to support the firm’s objectives.

Amazon’s technology applications include:

Recommendation engines to suggest products that consumers might want to consider purchasing. The recommendation engines are a quick solution to a customer’s need to navigate Amazon’s vast selection and choose a purchase.

Warehouse robots working with humans to quicken the responsibilities of pickers, packagers and stowers.

Alexa, the cloud-based, voice-controlled virtual assistant that provides information and, of course, an easy way to purchase goods and services.

Amazon mobile apps available on iOS, Android and Windows devices.

eReader (e.g., Kindle – offered as a physical device and as an app available on mobile devices) that enables customers to read purchased books (and magazines) and to purchase more books.

Amazon Prime Video – a streaming app for movies (licensed and original Amazon content) and television shows available on mobile devices.

Amazon continually leverages what the firm learns using its own capabilities and then refines its operations involving either consumer markets or corporate markets.

AWS and Fulfillment by Amazon (FBA) are two examples of Amazon’s expanding its capabilities and profit footprint. A third example is Amazon’s Ground Station-as-a-Service. This is an offering to satellite/Earth observation/NewSpace operators firms that don’t want to build their own ground stations, want to expand the number and location of ground stations they already have built or want to expand the number and location of ground stations they are getting from their current partners.

Netflix: Industry, Markets and Business Model

Industry Description – NAICS

The U.S. government has categorized Netflix as belonging to NAICS code 515210: cable and other subscription programming and NAICS code 532230: video tape and disc rental:

NAICS 515210 includes: establishments primarily engaged in operating studios and facilities for the broadcasting of programs on a subscription or fee basis.

NAICS 532230 includes: establishments primarily engaged in renting prerecorded video tapes and discs for home electronic equipment.

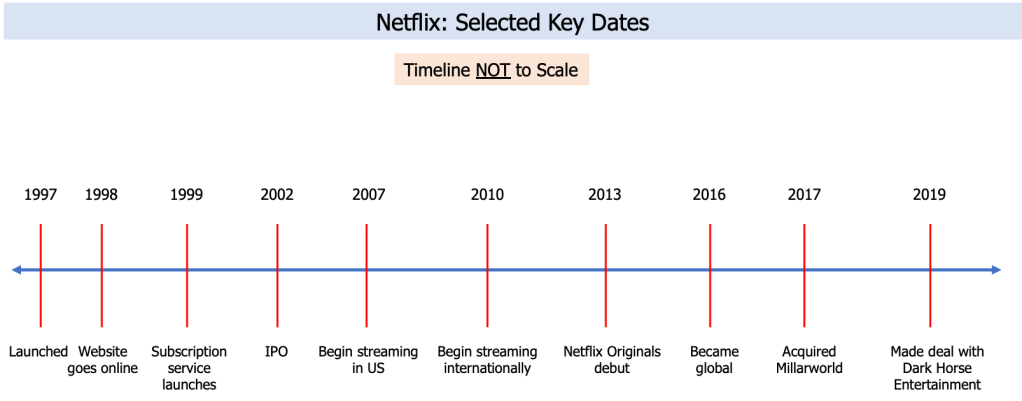

When Netflix began operations in 1997 by offering DVD rental by mail, the appropriate NAICS code would have been 532230. Netflix’ shift from renting DVDs by mail to becoming a subscription-based media firm obscures the reality of constant reinvention that is the firm’s hallmark to support its vision of offering a high-quality customer entertainment experience.

Target Markets

Netflix targets the global consumer market with its offerings of on-demand, subscription-based streaming content.

Netflix has become (according to the firm’s 10-K for 2019) “the world’s leading subscription streaming entertainment service with over 167 million paid streaming memberships in over 190 countries enjoying TV series, documentaries and feature films across a wide variety of genres and languages.” Netflix also has approximately two million customers who still rent and return DVDs by mail.

Netflix creates content in different countries around the world and distributes that content worldwide. Below, the chart shows the average paying memberships growing in the four major regions Netflix operates: U.S. and Canada, EMEA, LATAM and APAC. (Note: APAC excludes China and North Korea.)

Creating compelling content

Founder Reed Hastings says, “Our North Star is how do we do the absolute best content we can to please our customers.” Netflix is all about offering compelling stories to become a destination site for customers’ viewing.

Compelling story-telling is an integral component of who we are as humans (see visual). Our distant ancestors drew pictures on walls letting others know where food was located. At almost the end of the 19th century, Thomas Edison built the first movie studio called The Black Maria. Silent movies ruled the era, including Charlie Chaplin’s “Modern Times.” Much more recently, Netflix created the first Netflix Original web television series, which won seven Primetime Emmy awards, two Golden Globe awards, two Screen Actors Guild award and one Satellite award. Through six seasons, House of Cards won 27 awards.

Selected Key Dates in Netflix’ History

Obviously, the dates of incorporation and IPO are very important for Netflix (see visual). However, if I had to pick some other major dates on the Netflix timeline, my choices would be the dates:

Netflix began streaming (because this initiative redefined the consumer entertainment marketplace to an on-demand (or binging) marketplace)

of all the acquisitions and partnerships, of which I show only two in the visual. The acquisitions and partnerships provide Netflix with intellectual property (IP) that the firm can use to create series and movies.

Value Proposition

To attract customers from other activities that take place in what Hastings called the consumer’s "moments of truth," Netflix created a value proposition to provide on-demand, personalized, streaming entertainment available for viewing on any internet-connected screen for an affordable, no-commitment monthly fee. Did you catch the "no-commitment monthly fee?" Customers can cancel at any time (and come back when they want).

One of Hastings' guiding principles that drives his company to strengthen and reinvent Netflix is that “time is the real competition.” Not Disney+, not Amazon Prime Video, not Apple TV Plus, not Hulu and not other visual entertainment content but time itself. Time that customers could enjoy by reading a book, taking a walk, going to Starbucks or doing anything in their free time other than watching entertainment on Netflix.

Netflix bolsters the value proposition by allowing members to watch as much as they want, any time, anywhere, on any internet-connected screen. Members can play, pause and resume watching, all without commercials.

Moreover, Netflix puts the member (or customer) center stage by creating metrics based primarily on each customer rather than on the content. From the Product Habits blog: “Cable TV channels typically calculate their audiences based on viewership or how many viewers a TV show has. Netflix comes at this from the opposite direction by focusing on how many movies (or shows) a viewer has watched. Rather than optimizing individual shows to maximize the number of viewers, Netflix instead leverages its vast media catalog to optimize for movies watched per individual user.“

Strength of vision

Netflix intends to stay true to its value proposition by stating (and often restating in articles and interviews) that it has no intention of introducing advertisements into content, adding sports or going into gaming.

Story-telling – whether series, films or unscripted content – makes up the entertainment that Netflix currently offers and plans to offer.

But that laser focus on story-telling – and not on other content – does not mean that Netflix has not reinvented and will not reinvent itself. Far from it. Reinvention has been the foundation of Netflix’ success for more than two decades.

The firm has moved from DVD rentals by mail to streaming licensed content (and by introducing streaming – or bingeing – the firm redefined what it meant to watch content on the web) to creating and streaming original content.

Refining the amount of content available on Netflix

The phrase used to be, "What’s on [television] tonight?” Since Netflix and other multichannel video programming distributors (MVPD) redefined the "what" (and the "where" and "when") of content to view, people want to know the availability of streaming content.

From an article on Vox dated Jan. 27, 2020, titled “How Netflix is winning more with less content” written by Rani Molla (@ranimolla): “Ten years ago, Netflix had a total of 7,285 TV and movie titles in the U.S., according to streaming service search engine Reelgood. Now it has 5,838. That’s down nearly 50 percent from a peak of about 11,000 titles in 2012, according to Reelgood’s database, but up from 2018, when it had a low of 5,158.

The decline is part of a long-anticipated move by Netflix away from relying on other studios’ content and toward making its own. Netflix is making that transition as other content makers — namely Apple, Disney, NBC and WarnerMedia — launch and grow their own streaming services. This influx of new services also coincides with Netflix paying higher and higher prices to license content, especially if the content belongs to one of its new streaming competitors. Netflix could also be intentionally winnowing its selection as its vast troves of viewer data show it what people actually watch and what it can afford not to license.

Still, Netflix now spends more than half its cash on originals, Chief Financial Officer Spencer Adam Neumann said on the latest earnings call. That’s up from nothing, less than a decade ago. “The future of our business is mostly originals,” Neumann said.

Implications of Netflix creating original content

Netflix is not only talking the talk but walking the talk” about original content. An article dated Jan. 16, 2020, titled, “Netflix Projected to Spend More Than $17 Billion on Content in 2020,” by Todd Spangler, discusses a BMO Capital Markets forecast: “The streamer will invest around $17.3 billion this year in content on a cash basis … up from around $15.3 billion in 2019. Netflix is not expected to ease up any time soon: Its content spending will top $26 billion by 2028, per BMO’s report.”

The spending on original content will have implications on Netflix’ financials. Moreover, creating and distributing original content has many other implications, including:

decreased licensing cost of other studios' content

increased costs (for original content)

increased need, and cost, for people skilled in creating high-quality, desirable content

tactical hope that original content keeps existing customers and attracts new customers

significantly more control of how long the (original) content can remain on the Netflix media system for viewing by customers.

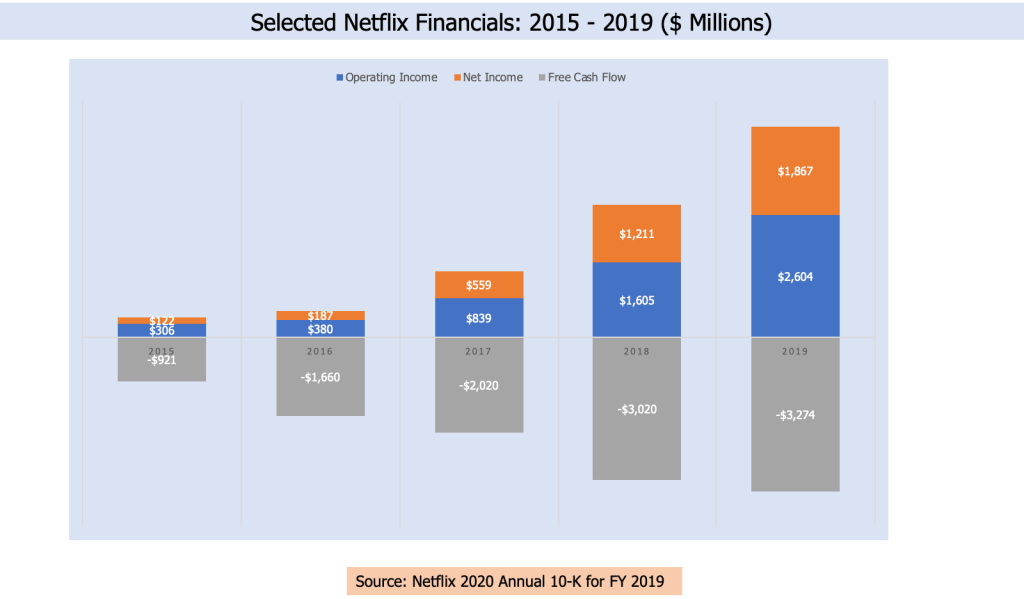

Profit Formula

Netflix’ operating income and net income have been steadily increasing from 2015 through 2019. However, Netflix’ free cash flow has steadily declined from -$921 million in 2015 to -$3.3 million in 2019.

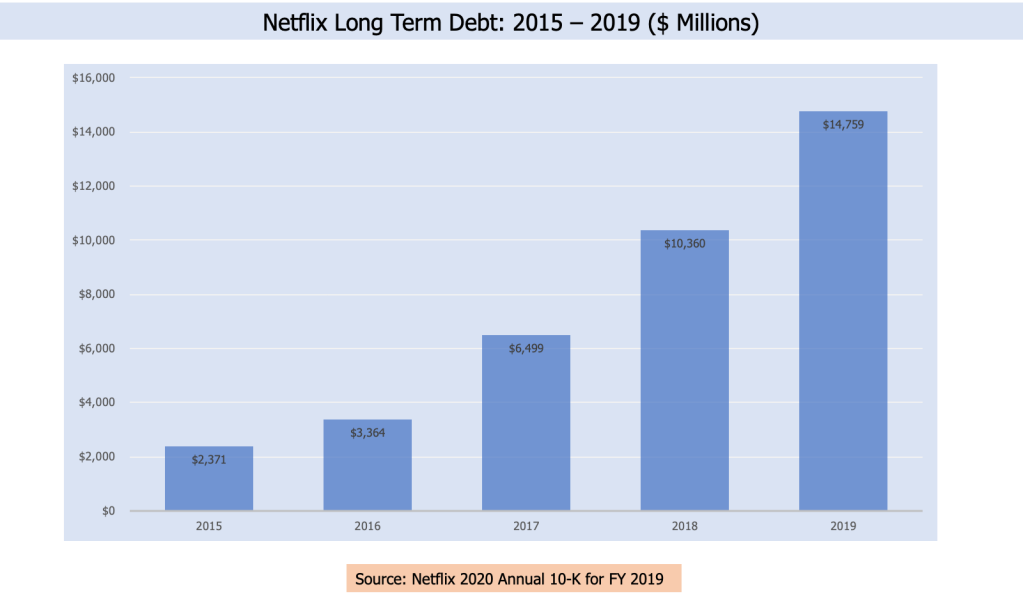

Netflix has also seen a steady increase in long-term debt from $2.4 million in 2015 to $14.8 million in 2019.

I think these financials point to the sustainability of the firm: using long-term debt to create a repository of more original content. How many years can Netflix operate in this manner? Keep in mind that I realize that I may very well be wrong on this matter, as I am not a financial analyst — please let me know.

Technology Applications

Netflix strives to keep its members entertained by offering personalized content. Netflix may no longer have the 11,000 titles for viewing it had some years ago, but 5,800-plus titles remains a large content repository. Moreover, the repository is not static: Netflix continues to license content and will continue to create Netflix Originals.

The volume of current and future planned content creates a challenge for Netflix: determining how to steer the appropriate content to each member. Put another way, the continual challenge for Netflix is how to identify and tell each member about the specific content the member would enjoy that is residing in a particular place (at any point in time).

The answer rests with Netflix’ applications of machine learning to improve each member’s experience. Netflix uses machine learning (which is a technology and not a technology application) to optimize the Netflix service end-to-end, including to (this is directly from the Netflix Research web site):

create and improve the firm’s recommendation engine

optimize the production of original movies and TV shows

optimize video and audio encoding

optimize the in-house Content Delivery Network

power the firm’s advertising spending

power the firm’s channel mix

power the firm’s advertising.

Insurance: Industry, Markets and Business Model

Industry Description – NAICS

The insurance industry has many sub-industries, including the following (using information from the U.S. Census Bureau about the 2017 NAICS codes):

NAICS code 524113 – Direct life insurance carriers: includes establishments primarily engaged in initially underwriting (i.e., assuming the risk and assigning premiums) annuities and life insurance policies, disability income policies and accidental death and dismemberment insurance policies.

NAICS code 524126 – Direct property and casualty insurance carriers: includes establishments primarily engaged in initially underwriting insurance policies that protect policyholders against losses that may occur as a result of property damage or liability. Illustrative examples include automobile insurance carriers, direct; malpractice insurance carriers, direct; fidelity insurance carriers, direct; mortgage guaranty insurance carriers, direct; homeowners’ insurance carriers, direct; surety insurance carriers, direct; liability insurance carriers, direct.

NAICS code 524130 – Reinsurance carriers: includes establishments primarily engaged in assuming all or part of the risk associated with existing insurance policies originally underwritten by other insurance carriers.

NAICS code 524210 – Agencies and brokerages: includes establishments primarily engaged in acting as agents (i.e., brokers) in selling annuities and insurance policies.

NAICS code 524291 – Claims adjusting: includes establishments primarily engaged in investigating, appraising and settling insurance claims.

NAICS code 524292 – Third party administration of insurance and pension funds: includes establishments primarily engaged in proving third party administration services of insurance and pension funds, such as claims processing and other administrative services to insurance claims, employee benefit plans and self-insurance funds.

NAICS code 524298 – All other insurance-related activities: includes establishments primarily engaged in providing insurance services on a contract or fee basis (except insurance agencies and brokerages, claims adjusting and third party administration). Insurance advisory services, insurance actuarial services and insurance rate-making services are included in this industry.

NAICS code 525110 – Pension funds: includes legal entities (i.e., funds, plans and programs) organized to provide retirement income benefits exclusively for the sponsor’s employees or members.

NAICS code 525190 – Other insurance funds: includes legal entities (i.e., funds (except pension, and health – and welfare-related employee benefit funds)) organized to provide insurance exclusively for the sponsor, firm or its employees or members. Self-insurance funds (except employee benefit funds) and workers’ compensation insurance funds are included in this industry.

Keep in mind that not every sub-industry participates in getting and keeping each insurance customer. The role of each sub-industry participant heavily depends on which insurance lines of business the potential client wants (needs?) to purchase, the financial and staff resources of the insurance carriers underwriting the risks and the sub-industry participants involved with customer and claim services.

Two iron-clad rules of insurance commerce

There are two facts that absolutely rule insurance commerce:

Insurance can only be underwritten in any one or more jurisdictions by an entity regulated and licensed to conduct insurance commerce there.

Insurance can only be sold by a regulated salesperson who is trained, certified and licensed to sell specific insurance line(s) of business in specific jurisdictions.

Insurers that use algorithms to sell the insurance policy within seconds (or nanoseconds) must ensure that the algorithms comply with the regulatory requirements of carriers and agents to underwrite and sell the policy in the jurisdiction of the sale.

The importance of insurance regulation

Regulation is critically important to underwriting, sale and service. Why the emphasis? Because insurance mitigates or manages the risks to:

people’s lives, property, income/assets, health, actions and behaviors

The insurance industry targets consumers, corporations, non-profit organizations and, in actuality, any entity that could be hurt financially by any type of risk, whether the risk is caused by natural events or human actions or behaviors.

The insurance industry offers its products and services to every person and every company in every industry subject to the risk appetite of each carrier. The insurance firm’s risk appetite is subject to a variety of attributes of the firm and the potential client, including the various exposures the potential client faces.

Exposures – of individual people, groups of people or companies – to a variety of risks (and in turn exposure to financial losses) where various insurance lines of business provide risk mitigation/management include:

living too long

dying too soon

planning for college education of children

retirement planning

having a swimming pool in a homeowner’s property

getting into an automobile accident

manufacturing products

managing a restaurant

holding sporting events

holding company picnics/outings

using entertainment venues

managing nursing/assisted living homes

launching satellites.

In summary, insurance offers products and services to exposures of life, living, health, working, entertaining and conducting commerce (in any industry).

Skeleton Framework of the Insurance Industry

The insurance industry offers products (i.e., insurance policies) for the exposures articulated above and more within a specific industry structure: life and annuity (L&A), property and casualty (P&C), health (which I do not cover) and reinsurance (which I rarely if ever cover). [I realize this is a simplistic structure that omits other lines of insurance.]

I’ve included the visual below only to give a taste of the industry structure.

Value Proposition

The value proposition of the insurance industry, regardless of major line of business, is to mitigate or manage risks.

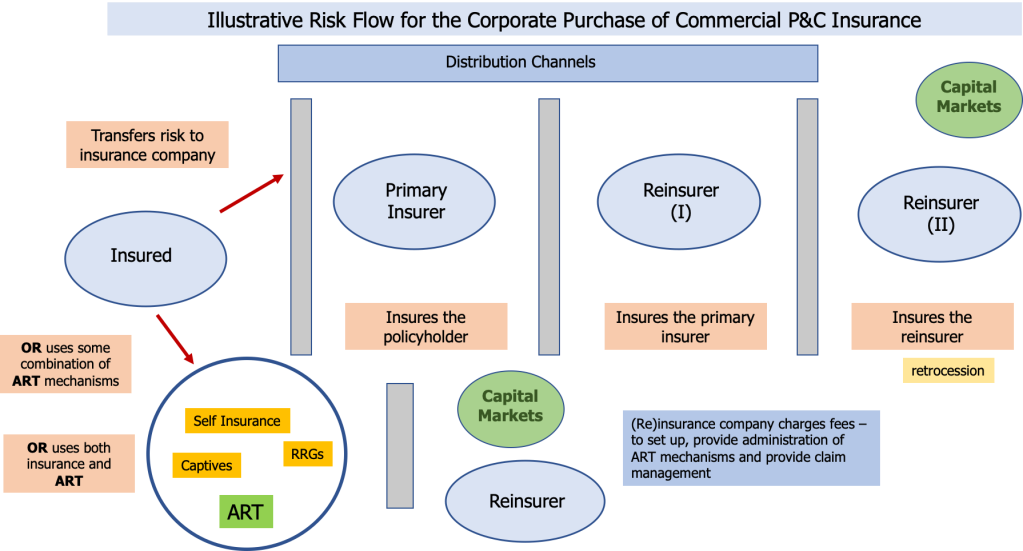

Let’s consider two value chains encompassing the flow of risk of the consumer purchase of insurance and of the corporate purchase of commercial P&C insurance.

My intention below is to show not just a flow of the acceptance of risk by some of the key participants in the insurance transaction but also to reinforce the complexity of the insurance transaction. I agree that consumers (i.e., individuals) don’t need to know the machinations behind their transactions but that ignorance doesn’t negate the complexities.

Illustrative Risk Flow for the Consumer Purchase of Insurance

Illustrative Risk Flow for the Corporate Purchase of Commercial P&C Insurance

Insurers generate their income from two main sources: premiums and investment income. To generate profitable premiums, insurers must strive for quality underwriting (i.e., to truly know the current and future exposures the prospective client faces through the intended length of the insurance policy).

To generate targeted investment income, insurers must strive for excellence in investing within the boundaries required by insurance regulators and must understand the current and future economy, political situation and insurance regulatory philosophies regarding all aspects of getting and keeping customers, whether retail or corporate.

Investment income

The acceptable investment areas are conservative in nature. For the U.S. life and accident and health insurance industry, for instance, the investment portfolio includes: bonds, preferred stock, common stock, mortgages, real estate, BA assets and cash. BA assets refers to the long-term invested assets as would be required to be reflected on Schedule BA of the NAIC Annual Statement Blank or the successor. For 2Q19, bonds represented 78% of the asset concentration.

Premiums

Premiums are the second major component of insurance company profitability. But insurers must strive for quality underwriting, and scale may not be an insurance company’s friend,.

Let’s discuss the concept of scale.

Scale

The mobile app that underwrites and binds an insurance policy within seconds (or nano-seconds) is the equivalent of a modern-day Frankenstein monster that runs amok through an insurance company’s financials, delivering rivers of blood red ink.

Why?

When a L&A or P&C insurance company underwrites and sells an insurance policy, it is simultaneously purchasing a future claim.

To ask two questions that every insurance (underwriting, actuarial, claims, marketing, sales and distribution) executive should consider with the sale of every insurance policy: What is the loss cost associated with the insured (i.e., policyholder), and when will that loss cost emerge for the insurer to adjudicate (and at what costs to adjudicate the claim, including any required investigations into possible fraud)?

The more insurers focus on scale, the more likely that they will incur underwriting losses.

L&A Insurers

The negative impact of scale is minimal for life insurance policies and annuities because L&A insurance companies have the Law of Large Numbers to use in addition to each L&A insurers’ own mortality and morbidity statistics and trends. L&A insurers, using these capabilities, can create models that have a high level of confidence predicting how many people (and more specifically their clients) will live during the year and also predict when death claims will occur. Still, L&A insurers need to to take care of the situations that are not candidates for simplified/accelerated underwriting (i.e., for those prospective insureds who don’t need a medical exam because of age, face amount of policy or other factors).

The negative impact of scale is more apparent for life insurers selling short-term disability (STD), long-term disability (LTD) and long-term care (LTC) insurance policies: These need to develop strong models to create predictions regarding occurrence – and cost – of claims. Mortality and morbidity statistics and trends obviously are in play in these markets. But so are a panoply of costs associated with delivering healthcare and physical rehabilitation. Scale is definitely not a desired attribute of STD, LTD or LTC sales.

P&C Insurers

The P&C market, whether personal or commercial, is where the Frankenstein monster of scale can truly run amok. I believe this holds true in the:

personal lines P&C insurance market

small commercial P&C insurance market

mid-size commercial P&C insurance market of corporate clients that do not have risk managers or only have CFOs who are not experienced in purchasing commercial P&C insurance.