|

December ITL Focus: Workers' Comp

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

This month's focus, sponsored by ICW Group, is Workers' Comp.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

This month's focus, sponsored by ICW Group, is Workers' Comp.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

At a time when insurers are pursuing a Predict & Prevent model, workers' comp carriers are leading the way: making workers safer and lowering premiums.

|

|

Paul Zamora joined ICW Group in 2006 to assume the business leadership role of ICW Group’s workers’ compensation product line. Under his leadership, the company’s work comp business has far exceeded industry and competitive benchmarks for growth, profitability and efficiency. Prior to joining ICW Group, Paul served as an assistant vice president at Zenith Insurance, one of the top workers’ compensation carriers in the U.S., where he played a key underwriting role. |

I find it really interesting that, while insurers in so many lines are having to raise rates like crazy, workers’ comp rates keep going down. That seems to mean that carriers, employees and employers are collaborating to reduce workplace injuries. At ITL, what we call “Predict & Prevent” has become a major emphasis for where we think the industry should go, and workers’ comp seems to be a great example of the potential to prevent problems rather than simply helping people recover once something goes wrong.

Maybe you could start us off by talking about how workers’ comp has made such great progress and how it can continue to reduce injuries.

I have a couple of thoughts as to why the industry has done so well.

A few states have been working to reform their workers’ compensation systems. California is an example, having passed a reform bill back in 2012. Prior to 2012, that state was having horrific results. Carriers were dramatically increasing rates, and a bunch of large businesses began to realize that they don't have to have their warehouses in California. They could move them across the border to Arizona or Nevada and save a ton of money. So there was a huge push for reform, and there were enough savings in the system to let carriers reduce rates but still obtain profitability without having a real negative effect on benefits for injured workers. That was a huge win.

Other bills throughout the various states where ICW Group does business haven't quite achieved that result but still have made progress.

The other thing I think we have going for us is the huge financial incentive for policyholders to improve safety and reduce premiums. There's a lot of synergy with us, our agents and our policyholders to try to improve safety.

At ICW Group, we have what we call the Power of Three. We're monitoring how we're helping customers have lower frequency of claims, controlling those costs when they do have claims, so we have the best outcome possible, ultimately having a positive impact on their Experience Modification factor [which compares a company’s actual losses with those that are expected for a company in their industry and plays a major role in determining workers’ comp premiums].

And we're pleased. We’re lowering ex mods for our customers and seeing fewer claims, so companies can pay less premium.

We are working on using technology to track the near misses. Most of the time, when we get a really serious claim, such as when somebody puts a hand in a machine and maybe loses their hand or arm, well, there were a lot of situations where that almost happened but, luckily, the person was able to move their hand or arm out of the way. Tracking those near misses will help us make safety improvements so we protect the worker and greatly reduce those severe claims.

One thing we're doing right now is a pilot with a wearable. It tracks unsafe behaviors that could lead to a repetitive motion claim, or maybe someone is bending the wrong way.

We think there's even better safety technology coming. We are experimenting with smart cameras that can track both unsafe behavior and unsafe conditions. For example, it could see water on the floor and quickly buzz somebody at the employer's facility to go clean it up, and not wait for somebody to actually slip on it and get injured.

The challenge right now is that some of the technology is expensive. The smart cameras are quite expensive. So, it isn’t easy to deploy them to a lot of policyholders. But we believe, no different than a laptop or a cell phone, eventually that technology will become less expensive.

What we're trying to do right now is run pilots to see if the technology works. Does it really drive different behaviors? Does it really help us find and fix the problem before an injury can occur?

We're bullish that the safety technology will be much more affordable, so we can deploy it to more policyholders, and we are also bullish that it will change behavior and mitigate claims.

That all sounds super smart. What are some other big trends you see in workers’ comp leading into 2024?

I believe we're going to continue to see rates decrease. January is the time when most states update their pure premium rates, and just about every state other than Hawaii is recommending decreases. Most are double-digit decreases.

Some of the bigger states, such as California, may have hit bottom in terms of rates. We're starting to see accident year combined ratios climb. Carriers have a massive reserve redundancy from prior years, and they'll use those reserve redundancies to make their calendar year numbers look good. But you eventually will run out of that reserve redundancy, and you will have to start charging the proper rate. We're already seeing some of that in California. We're seeing some of that in other states, as well, such as in New Jersey. But we're also seeing a lot of competition in some of our bigger states, such as Illinois and Florida, where rates have not yet hit rock bottom.

The final thing I'd say is you're going to see the smart carriers go down the path of digitization. Carriers need to understand that, today, we're competing with traditional insurance carriers but that in the future our competition might look different. Amazon could decide they want to get further into the insurance space for one reason or another. And your buyers will be expecting the Amazon-type experience, where they go online and it's really easy to do what they want to do. Carriers need to pay attention.

Amazon is already dabbling. They've started to offer some insurance to small businesses, and it will be interesting to see how that evolves.

I think it's an important point you're getting into about long-term customer relationships. Beyond what you've already said, what is ICW Group doing, and what do you think others need to do, to foster those really long-term, profitable, mutually beneficial relationships?

The number one thing is making sure we're helping our customers have positive long-term results. So how do we make sure of that? How do we make sure they're safer and they’re paying the lowest amount of premium possible because they have safe operations. That they're not losing employees because they're injured? If we're not able to deliver on our Power of Three value proposition, customers are going to find another home.

Providing other value-added services is important, as well. We have a product called HR OnDemand, which was a huge benefit during COVID. There were a lot of HR questions around being in compliance with all of the new COVID regulations, and HR OnDemand allowed customers to talk to an HR expert and get free advice. We also have something called Safety OnDemand. We provide risk management services in-house, meaning we can go out and sit down with you and work with you. There are folks who want that advice at 2:00 am, so a self-help capability through online tools is critical.

Nurse triage is popular now, too. Maybe I don't know if I need to send an employee to the doctor or if they only need first aid. With nurse triage, I can call and speak with a registered nurse who can provide me guidance.

The final one is telemedicine, where you can see a doctor in your own workplace and not have to get in a car and drive to the clinic and maybe sit in the waiting room before you're seen.

Beyond the value-added services, you have to focus on the customer experience. And, as I said, we’re not going to just compete with the traditional insurance carriers in the future. We will probably be competing with companies like Amazon or Google.

Beyond what you just talked about, are there other ways for carriers to support their independent agent networks?

For us, it's extremely important to make sure we listen to our agents and figure out what they need. We are not a direct writer. We have zero direct business, and we don't have any plans to be a direct writer. So 100% of our business is from the independent agent force. Without them, we don't exist. So we try to make our interactions with them as efficient as possible for both of us.

This means focusing on how they submit accounts to us, how we go through the whole quoting process, the binding process, the mid-term servicing of the account and more. How do we make sure they don't have to add staff to try to be more effective in working with us? We've implemented some programs based on feedback from them, such as LeadGen OnDemand, which is a tool that allows them to market themselves to potential insureds in a very efficient manner. We pay for the platform, the mailers and the marketing collateral to help them grow their business. And that has paid huge dividends for us.

We introduced an Agent Portal so they can be more efficient in managing their business and keeping track of what's going on with their customers 24/7. Finally, we make sure we provide a quality product that they're proud to sell. They do not want to get that call at 11:00 pm asking, why'd you put me with that insurance company?

We take a franchise approach, which I think is important for carriers to do. I mean, you can appoint every agent that's got a license to do business, but then your agent community has nothing to differentiate themselves. If you take a franchise approach, you're giving your agents something valuable to have in their toolkit.

Are you expecting any particular changes in regulation?

We kind of wish the states would all be more similar and less nuanced on certain things. When they all have their little nuances, it creates a lot of extra work for everybody. Most of what we write, and I'm sure this is true for most carriers, is for risk that has multi-state exposure. It's a challenge, from a technology standpoint, to make sure your systems recognize all the nuances in, for example, California, Nevada and Arizona. And we need to make sure customers understand them, as well. If the customer is predominantly in one state, they think the insurance rules of that state apply to their business in all states, and that’s not true.

But we understand that change isn’t coming any time soon, if ever. So we just have to stay on top of the issues.

I wonder about some macro trends. It seems like the return-to-the-office movement has stabilized, but there could still be some adjustment, and some offices will be redesigned or repurposed, which could change the dynamics for workers’ comp. I also wonder what will happen with all this “onshoring” of manufacturing that seems to be in the works. Are there any other trends we should be tracking?

Onshoring would mean more jobs and more workers here to insure. At the same time, companies are automating a lot more. I saw a company the other day that has self-driving trucks on a dedicated route. No human being needs to be in the cab. If that level of automation spreads, there's no employee, there's no payroll and there's no workers’ comp premium associated with that job. We have started to see restaurants where wait staff kind of goes away. There's an iPad on your table for you to place your order, and then there's just a person who brings you out the food.

We probably won't see fully automated factories in my lifetime, but we’re paying attention to the trends.

Thanks, Paul. This has been a great conversation.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

The answer is a strategy that blends technology, talent development and alignment with the values of the younger generation.

In a world driven by technological advancements and a changing workforce, the insurance industry faces the critical challenge of attracting and retaining the next generation of underwriters. The answer is a strategy that blends technology, talent development and alignment with the values of the younger generation.

Embracing Technology

The younger generation expects technology to be integrated into the workforce. Technology is not a nice-to-have for insurance carriers; it's table stakes. From implementing advanced underwriting software to incorporating AI-driven risk assessment tools, companies can create a competitive advantage by showcasing a commitment to a tech-centric future, which gives them a leg up on recruiting and retaining talent.

See also: How to Address the Talent Shortage in Insurance

Automation for Efficiency

Automating routine tasks lets underwriters focus on more meaningful work, flexing their underwriting muscles and contributing more effectively. This approach not only increases job satisfaction but also plays a crucial role in preventing turnover.

Automation, far from replacing crucial skills, serves as a complement to the human underwriter. Nobody wants to get into an industry if they feel like tech can do their job tomorrow, so it's important to communicate a commitment to the long-term viability of human underwriters, while simultaneously leveraging technology for increased efficiency.

Upskilling and Continuous Learning

As Gen Z prioritizes jobs that facilitate skill expansion and continuous learning through technology, it's important to provide avenues for upskilling. Investing in training on, for instance, how to use AI to reduce manual steps not only aligns with the preferences of the younger workforce but also benefits the company by ensuring a highly engaged and adaptable talent pool.

See also: What to Understand About Gen Z

The Untold Stories of Stability

Insurers must bridge the narrative gap to attract young recruits. Insurance is not just a job; it's a resilient sector that withstands economic fluctuations, continually evolves and offers a stable career path even in uncertain times.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Adam Cherubini is the chief revenue officer at Send.

His immediate focus is on expansion into the North American market. He has had a diverse portfolio of leadership roles at notable organizations such as QuinStreet, Insweb and Willis Corroon (now WTW). Over the past eight years, Cherubini has led consulting projects focusing on sales, marketing and partnerships at Voom Insurance, Kelly Klee, Notion, HYLA Mobile and Pie Insurance. A former underwriter, he was a co-founder and CRO of Honeycomb, an innovative digital MGA disrupting traditional real estate insurance.

Technology can transform traditional practices, elevating efficiency and enhancing overall policyholder experiences.

In today's digitally driven landscape, insurance companies must implement efficient processes to enhance the claims process, both internally with insurance professionals and externally with policyholders. Technology serves as the catalyst for transforming traditional practices, elevating efficiency and enhancing overall policyholder experiences. The integration of technology not only addresses longstanding inefficiencies but also opens doors to opportunities, positioning the industry at the forefront of innovation.

See also: Enhancing Claims Via Digital Payouts

Navigating the Challenges of Technology Adoption in Insurance

While there are many benefits to technology adoption, it is important to consider the challenges faced by professionals and policyholders. Key challenges include:

Efficiency drives the success and sustainability of insurance operations, making it crucial to overcome the challenges listed above.

See also: 5 Ways Generative AI Will Transform Claims

Embracing Digital Transformation and Insurtech Solutions in the Claims Process

Digital transformation in the claims process and throughout the insurance industry involves a strategic and comprehensive approach to technology implementation.

With an average claims frequency of 8%, policyholders don't understand the claims process. Insurance professionals must ensure that the claims process is efficiently communicated and that transparency is present in every stage of the process, from first notice of loss through to claims completion. Claims professionals also must be educated on new technologies that are implemented throughout the process, especially if it affects their daily operations.

There are many ways that companies in the insurance industry can take steps toward digital transformation, including:

Insurtech solutions offer accelerated processing times, improved accuracy, enhanced policyholder experiences and adaptability to industry trends.

This strategic shift not only optimizes internal workflows but also creates enriching experiences for today's policyholders. Automation facilitates complex coverage decisions while efficiently communicating with policyholders. Real-time updates accessible through a customer portal empower policyholders, offering transparency to keep them informed throughout the process.

Companies in the insurance industry can revolutionize their operations and remain competitive in an ever-evolving landscape, delivering unparalleled efficiency and value to internal processes and the overall policyholder experience.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Clay Rising is the chief claims officer at Brush Claims.

Rising grew up in the insurance industry, working for his father in an independently owned agency throughout high school. He used that experience to gain degrees in risk management and insurance and corporate finance.

After quickly deciding that office life was not ideal, he left the corporate world to build houses for Habitat for Humanity full time. When the housing market turned, he relied on his past and education, coupled with his construction knowledge, and joined The Travelers as an adjuster. He later spent nine years at ASI (which became Progressive Home), where he held numerous leadership roles. He joined start-up Kin as their first VP of claims, where the team grew from one in 2020 to more than 135 today.

While life insurers' initiatives have been underway for years, projects are rife with misalignment, unmet expectations and dissatisfaction.

KEY TAKEAWAYS:

--Rather than implement new projects in isolation, insurers should envision and build an overarching strategic plan for digital transformation across the enterprise.

--Digital transformation requires that legacy systems be retired and policies consolidated onto modern solutions.

--Companies must take a holistic view of the entire insurance value chain, prioritizing data as a central component of transformation efforts and investing in its management, quality and effective use.

----------

Most life insurers are mid-journey when it comes to total organizational digital transformation. While initiatives have been underway for the better part of the past decade, completed project segments are rife with misalignment, unmet expectations and dissatisfaction with the outcome. Insurers are finding that realizing the maximum value from these initiatives is harder than it seems.

In many cases, these projects were touted as low-hanging fruit, designed to be implemented quickly and to deliver value in the short term. Unfortunately, this approach often falls short because the initiatives were not conceived and planned with an enterprise view in mind.

To realize the planned-for value of all digital transformation projects, insurers need to adopt three bedrock principles.

See also: Revolutionizing Life Insurance Uptake in Younger Markets

Principle #1: Begin taking a holistic approach to digital transformation

Projects that have been executed in silos and are not inclusive of the entire organization tend to run into more challenges in quality assurance cycles, resulting in delays, overruns and fewer results. Thus, they don’t produce the expected value.

Rather than implement new projects in isolation, insurers should envision and build an overarching strategic plan for digital transformation across the enterprise. The plan would include solutions for major pain points from all stakeholders. It would consider core systems, digital sales, service solutions and adviser and distributor solutions.

It’s critical for executives to engage all stakeholders and ensure everybody communicates their unique needs and understands how they contribute to the plan’s success. One sometimes unintended, but positive, outcome of this exercise is a strong sense of the organizational benefit and cross-over benefits that each phase of the transformation brings to the company.

The key to organizational buy-in? Starting with a well-conceived and well-communicated plan. Within that overall plan, the enterprise can prioritize coming projects and allocate resources accordingly with energized teams ready to lay the foundation for success.

Principle #2: Reduce reliance on and complexity of legacy systems

Over time, most insurers build increasingly complex policy administration environments. These legacy ecosystems — the result of new product initiatives or M&A activity — create a disconnected landscape of data islands unable to communicate with each other.

With these isolated pockets of data, it’s difficult to provide customers with the same type of smooth digital experiences they enjoy in most other industries. Yet many insurers kick the modernization can down the road year after year, or paper over the cracks with patches and upgrades.

Every year modernization is delayed, the gap grows bigger between the fully digital and mainly manual. It also becomes harder to get the most from any new digital initiative when it’s delivered into an IT environment where connections are difficult, interactions don’t happen in real time and most data is inaccessible.

Digital transformation requires that legacy systems be retired and policies consolidated onto modern solutions.

Principle #3: Focus on data as the foundation for digital transformation by addressing data quality and efficacy challenges

Rather than focusing on isolated digital initiatives, insurers must take a holistic view of the entire insurance value chain. As part of this panoramic view, it’s important to prioritize data as a central component of your transformation efforts and invest in its management, quality and effective use.

Historically, the insurance industry has treated data as a byproduct rather than a strategic asset. For the sake of efficiency in applications, insurance made many decisions that were “data minimalistic.” If you enter only what you need, you can move the application or process along quicker. But this mindset creates challenges when attempting to make better risk decisions.

For example, many organizations are having to rework their data strategies when implementing artificial intelligence (AI) and machine learning (ML) initiatives because the outputs from those applications are only as good as the data being fed into them.

Insurance companies must find ways to bridge the gap between their siloed legacy systems and the broader digital ecosystem, ensuring seamless integration and alignment of data assets.

When an organization implements foundational data principles like adopting robust data management practices, retiring old core systems, connecting systems with application programming interfaces (APIs) and using new, event-driven interaction techniques, they are poised to leverage new digital solutions. These solutions are much better-positioned to provide maximum value and are implemented leveraging new tech and old data that is effective and operationally meaningful.

Creating this level of comprehensive data framework benefits all digital transformation initiatives. It increases the value generated by each one by producing actionable insights, optimizing processes, enhancing customer experiences and accelerating the development of innovative products and services.

See also: Genomics Revolution in Life Insurance

Wrap up

When digital transformation projects are approached as isolated events, they are far less effective than when they are conceived and executed as part of an overarching transformation plan. Maximizing the value of each initiative requires a strategic approach that recognizes the importance of building a foundation for all future development and growth by modernizing core systems and focusing on data.

Successful organizations understand that digital transformation isn’t just about implementing technology, but gaining organizational buy-in, emphasizing the importance of reducing complexity and reaping the benefits of quality data to better align with transformative efforts. These companies are on a holistic digital journey that empowers them to make informed decisions, drive innovation and deliver superior customer experiences.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Brian Carey is senior director, insurance industry principal, Equisoft.

He holds a master's degree in information systems with honors from Drexel University and bachelor's degrees in computer science and mathematics from Widener University.

Combining external data streams with internal analytics creates a comprehensive view of properties that legacy methods can't match.

Inadequate data continues to plague the insurance industry, as exemplified by Hurricane Ian victims in Florida still battling underpayments more than a year later. With claimants left with no option but to sue, the Insurance Information Institute estimated that insurance companies are facing $10 billion to $20 billion in litigation costs.

This situation underscores the critical need for fresh underwriting data in the digital age. Reliance on legacy valuations and records has left insurers struggling to accurately assess claims and risks, while eroding customer trust. The exponential growth of digital data provides immense potential here, if harnessed correctly. Combining external data streams with internal analytics creates a comprehensive 360-degree view of properties that legacy methods cannot match. The streams also provide the opportunity to adopt innovations that enhance inspections, streamline processes and improve customer experiences.

Indeed, forward-thinking insurers are already embracing external data and applying emerging technologies like AI and digital twins to extract richer data insights and enable faster, more efficient services.

While tier one insurers might be able to address all these challenges within their own resources and capabilities, that leaves a swath of the industry looking for answers. These insurers must tap innovative technologies like AI while leveraging new data sources outside their walls. The solution lies in embracing external data partnerships.

The potential of the data explosion in insurance

Data is ubiquitous today. Weather data improves climate risk models. IoT sensor data provides real-time building occupancy and condition details previously unattainable. Even social media and online reviews give insights into property usage unthinkable just years ago. This data explosion has massive implications for insurers.

The use of external digital data streams is advanced. FinTech Futures put the size of the global alternative data market at $17.4 billion by 2027, growing at 40% annually.

See also: 5 Ways Generative AI Will Transform Claims

Profound benefits are already emerging for insurance companies ahead of the curve. A study has identified:

Insurers are already leveraging the trove of external data, alongside conventional analytics, to gain comprehensive insights with which to improve product competitiveness and workflow efficiency and experience.

Satellite data: a revolution in property intelligence

One especially powerful external data source set to disrupt underwriting is satellite imagery.

Accessing accurate property data is still a huge problem for insurers. This data is often compiled from multiple sources (ranging from brokers and property managers to public records) and can be inconsistent or incomplete. As a result, customers often have claims rejected or only partially paid out, as the claimants in Southwest Florida have discovered. And insurers can be held liable for the difference in costs.

When combined with AI analysis, satellite data provides contemporary information that can be verified against visual evidence, rather than paper records. It can include property details like facade materials, construction types, occupancy details and roof geometry at mass scale. In fact, this data can provide detailed coverage for 99% of properties in developed countries.

For underwriters, satellite intelligence reduces in-person inspection costs by 50% on average and takes minutes rather than days to process. For claims teams, it enables real-time damage assessment and accelerated claims processing. And for brokers and their customers, it enables instant, automated quoting and more customized policies.

This data also mitigates premium leakage, enhances loss ratios, reduces under- and over-insurance and generally removes guesswork from the equation.

See also: AI and the Future of Independent Agents

The future belongs to data-driven insurers

Yet many insurers still depend on decades-old surveys and records for property data, potentially leading to underwriting and risk assessment mistakes. In the U.K. alone, 40% of commercial properties and 80% of households are underinsured due to poor property insights -- leading to denied or limited claims.

There is no longer any reason for these gaps. Through innovative data partnerships, insurers of all sizes can now access external data sources and AI capabilities that were previously only available to major carriers. These collaborations accelerate implementation and democratize access to advanced analytics, empowering insurers to leverage leading-edge data intelligence regardless of their scale.

External data and AI are no longer the sole province of tier one insurers -- strategic partnerships provide cutting-edge solutions to insurers across the market, fueling digital transformation through data. Data is the undisputed currency of modern insurance. Only insurers embracing partnerships and innovation will thrive. The time to unlock the black box of external data is now.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Jacob Grob is chief revenue officer and data innovation lead at Tensorflight.

Grob has over 15 years' experience in the data, geospatial and insurance industries working with property and casualty insurance software and data analytics providers, including Maprisk and Corelogic.

Grob holds bachelor degrees in liberal studies and geography from the University of Wisconsin-Whitewater.

Only teams who play together and adhere to their positions can win in polo.

Polo, the “game of kings,” is among the oldest, fastest, roughest and most dangerous team sports. Also known as hockey on horseback, the game is played with two teams of four players each. Polo combines physical skill, mental agility and quick strategic thinking. Players use a mallet to hit a small ball between the opposing team's goalposts, galloping on a horse at 30 mph.

Polo and business both require leadership, teamwork and strategy.

Leadership - No Two People Are the Same

Each player has a specific role and responsibility on the field. There are two players: the horse and the rider. However, horses aren't machines. To be a great polo player, you must be an excellent horseman or horsewoman and develop a relationship with your steed.

In my first polo season, I acquired my first pony, "JJ," an old racehorse, from a friend. Initially I "stick and ball" and fell off a lot. Then I played a couple of chukkas a game and got frustrated playing part-time, and soon more ponies followed. It kept my daughters and their friends busy exercising and grooming and was a great bonding experience.

Looking after different horses taught us that each horse has a distinct personality and unique strengths and weaknesses -- like in business, where no two people are the same and can't be led the same way. Some employees need encouragement and confidence to take risks and chances, while you might need to let others run free or even rein them in occasionally.

Employees and horses have unique motivators, skills and attributes that they bring to the table. Understanding who your people are and their skill sets will help to get the most out of the team, which is critical for strong business leadership and success.

See also: Leadership Lessons From Sports

Try, Try Again, or Get Back on Your Horse and Try Again!

Polo can be a way of life for many players and enthusiasts. Polo fosters a sense of camaraderie, respect and fair play among the players and the spectators.

It is also an extreme sport. Whether galloping 30 mph with your opponent right beside you, getting a very hard ball shot into your back or being checked by your opponent on a 900-pound horse, danger exists everywhere.

Fear can also be part of the game. Whether falling off your horse and suffering an injury, letting your teammates down or starting a new role at work, fear can shrink our confidence, make us hesitate and affect you and your team's performance.

Every polo player will fall off their horse sometime. In fact, in 2015, 58% of polo players in the U.K. reported falls. What matters is how you respond, persevere and conquer your fears. You could give up and say this sport isn't for you. Alternatively, you could embrace a growth mindset and understand that great athletes and successful people get back on their horses and focus on progression and continuous improvement rather than perfection.

After all, every expert was once a beginner.

Teamwork - Play as a Team

Only teams who play together and adhere to their positions can win in polo. For example, the number one player in polo is responsible for scoring goals. The number two player helps both in defense and offense. The number three player is often the captain and leads plays, and the number four is in charge of defending the goal. Without verbal and nonverbal communication, teams won't be able to coordinate plays effectively and ensure that everyone is playing their positions.

In business, everyone on your team has a role and position that suits their specific skills and traits. For instance, while an insurance technology company might have talented software engineers, data scientists, etc., to develop products, they need advertisers, marketers and salespeople with different perspectives and niches to sell their technology and capture market share.

Building a functional team requires leadership. Leaders must ensure that each team member, whether on the field or in the office, feels like they're a part of something meaningful and more substantial than themselves to be successful.

Play together and win together!

See also: 7 Things Sailing Taught Me on Leadership

Strategy and Time

A polo game is divided into six periods called chukkas, each lasting seven and a half minutes. Your team can lose by being two seconds too slow off the mark, letting the opposition get ahead with the ball. The split-second decisions and small room for error have taught me never to second-guess myself or delay in chasing my goals.

In business as well as polo, it is essential to keep communication open with all team members and, when you can, continue to evaluate and improve on;

Both polo and business leaders must have good communication, coordination and motivation skills to lead their teams effectively.

My first polo game was on a farmer's field. Since then, the sport has taken me to places I likely wouldn’t have seen otherwise, including Argentina, the U.K. and all over North America.

Business has also provided quite the journey. In 2000, I founded Global IQX, an employee benefits insurtech. During the COVID pandemic, our company saw remarkable growth, and recently we were acquired by Majesco, a global leader in cloud insurance software solutions.

Whether you are playing a short or the long game, trust yourself and your team and continue to improve so you can knock that ball between the goalposts!

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Mike de Waal is senior vice president of sales at Majesco.

Clients' questions on group benefits, which have typically been about rates or coverage, are increasingly about technology issues.

Traditionally, employer clients have looked to their insurance brokers and brokers have looked to general agents (GAs) or carrier sales representatives for information on the best rates and products.

But client questions are increasingly shifting to technology matters.

Employers offering group benefits to their employees are now as curious about the features and capabilities of the technology used by carriers and ben-admin systems as they are about their rates. And according to a recent study by Ease, 50% of employers sourced their benefits technology from a broker. That new emphasis puts brokers -- and GAs -- in the unfamiliar position of tech advisers, intermediaries between clients and vendors.

That’s what we learned from a recent webinar with representatives from a leading brokerage and general agencies. Technology is transforming insurance, an industry that has traditionally lagged behind others in its adoption. It appears that this new prioritization is driven by clients demanding the same modern experiences, interoperability and ease of use from their insurance carriers that they have in other business functions and personal consumer experiences – also known as the “Amazon Effect.”

For clients, easy data exchange is everything; in fact, 66% of employers prefer carriers that connect to their software over those offering the best-value insurance products.

At our recent convening event, which included experts from United Producers Group and Hub International, we posed question across three areas:

What’s going on with benefits technology today?

The role and versatility of technology is quickly advancing, due in part to the changes brought on by the pandemic and its new work models, as well as by clients and their employees’ expectations. Employees want to better understand their insurance benefits and have benefits experiences that help them use these valued assets in easier ways, which are essential pieces of their total compensation.

Employers are eager to provide modern, differentiated benefit experiences to retain and attract workers, and improved technology is necessary. According to a recent report by Guardian, 79% of employers expect to increase their spending on benefits technology in the next three years.

To get the desired result, clients need a digital benefits strategy, one that will not only please workers but help employers become more efficient and control costs by lessening administrative burdens, reducing manual transactions and addressing compliance. The optimal technology should reduce administrative costs by automating functions now done by people.

The demand for this new technology isn’t only from large clients; small employers also want tech that will allow their various systems -- such as payroll, ben-admin, COBRA and cafeteria plans -- to interact seamlessly.

See also: Why Brokers Should Embrace AI

Where should benefits technology go next?

The panelists want the industry to emphasize investments in speed and accuracy, with a focus on getting insurance cards in new members’ hands as quickly as possible with no glitches or delays. That requires automating the process to minimize or eliminate the manual tasks that slow things down and introduce the possibility of errors.

In addition, brokers must be sure they’re up to speed on the latest industry technology, who offers what, and how different systems interact. If brokers don’t know how to deliver the tech experience their clients want, their clients will find other brokers.

Another point of emphasis was the importance of adopting technology that could help produce clean, accurate data right off the bat -- from the beginning of the process. Too often, insurance enrollment data is unavailable, incomplete or inaccurate. Incorrect data must be fixed at some point, which comes with a high cost in time, labor and strained relationships among sales teams, brokers, groups and more.

See also: AI and the Future of Independent Agents

What do brokers want from ben-admins and carriers?

At the top of their wish list for carriers is application programming interface (API) integration for every policy to allow a single point of entry and an easy bi-directional flow of data so manual intervention is no longer required. There has been progress in this area, but fewer than 15% of carriers now offer it. The need is particularly great for medical insurers.

From ben-admin platforms, the request is to add technology to make their systems flexible enough to accommodate and merge data from multiple sources and handle employers’ increasingly complex benefit structures.

The brokers also requested that carriers and ben-admins focus on speed-to-market for products, simplicity, improved communication and easy data flow among all parties. This, they noted, would allow brokers and GAs time to have the strategic conversations that bring the most value to their clients.

As thought leaders and change agents in our industry, we regularly convene experts to get at the important nuggets in our industry. Talking with leaders like our panelists is a great way to assess where the industry stands and where it needs to be.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Gary Davis is national practice leader at Noyo.

He leads digital transformation efforts – built on a foundation of clean, accurate and secure data – for employee benefits partners. He has nearly 30 years of experience driving innovation through the employee benefits ecosystem, including a previous position as AVP national small business practice leader at Humana.

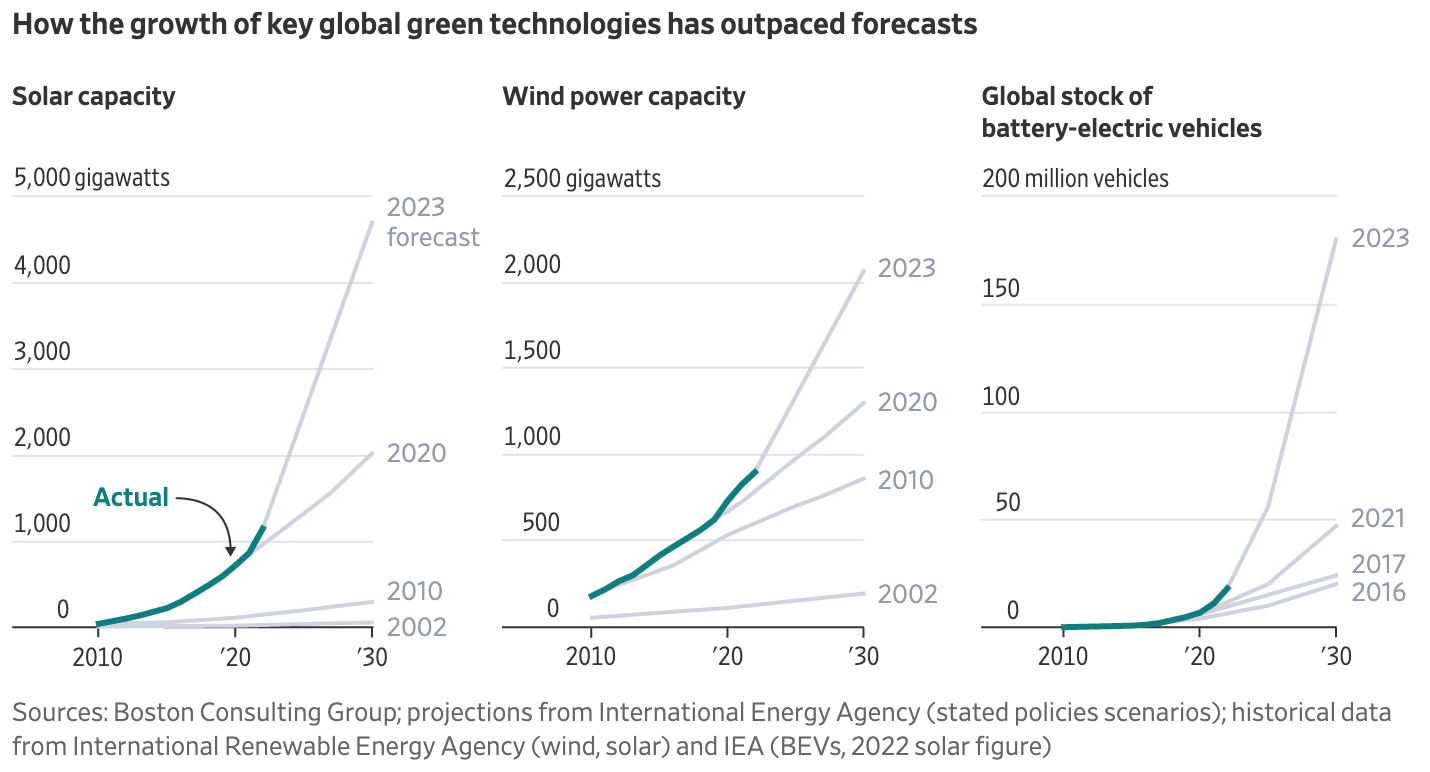

Stunning declines in the cost of solar and wind power are rapidly adding renewables to the world's energy mix.

The recent cancellation of a major wind energy project off New Jersey's shore has cast a pall over efforts to limit climate change. But there are important signs of hope, too -- in particular, stunning declines in the cost of solar and wind power.

With the U.N.'s annual summit on climate set to start later this week, let's focus for a few minutes on the hope.

This chart from a recent article in the Wall Street Journal pretty much says it all:

You can see, in particular, how installations of solar power have consistently exceeded expectations -- by a lot. The 2002 projection the WSJ cites showed almost no adoption of solar by now in the grid because costs were expected to be higher than for alternative sources. Even in 2010, projections were for almost no use of solar in the grid by now. By 2020, the picture had totally changed -- but even that projection was far less optimistic than the current one. The 2023 prediction shows a full-on hockey stick of the sort that makes investors salivate.

The reason? Technology has cut costs far faster than expected.

I have a personal point of reference here. I was part of a SWAT team at the Department of Energy in 2010 (led by Matt Rogers) that was investing $37.5 billion of Stimulus Act money to nurture innovation in a whole range of energy technologies, including solar, wind, batteries and electric vehicles. We took what seemed like a very aggressive view at the time about what technology could do and projected roughly a 60% decline in the cost of solar by 2020 -- while the WSJ article says costs fell fully 90% between 2009 and today.

The cost of onshore wind power has declined by two-thirds over the same period, the article says, and there's every reason to think costs will continue to decline for both it and for solar. Not only will the technology keep improving, but costs steadily fall as manufacturing scales up.

In fact, the New York Times ran a story yesterday about concerns that solar prices are falling TOO fast. The main concern addressed in the article is political: Falling prices might undercut profitability and lead to job cuts in Georgia, where production has boomed because of the clean energy push by President Biden and where any disruption might cost him in the 2024 presidential election. However the politics play out, a plunge in prices will only accelerate adoption.

Solar and wind already have reached a tipping point: The WSJ article says four-fifths of global power capacity added last year uses renewables.

There has been some concern recently about the adoption rate for electric vehicles. While Tesla has had to cut prices on its EVs to maintain momentum, Toyota, which has resisted the move to EVs, has been taking a victory lap because its sales of hybrids have soared this year. The CEO of Mazda, Masahiro Moro, told Fortune the other day that, “we have not put a goal on [the move to EVs]. We will move as fast as the customer. We never want to surprise them with new technology.”

Still, the "disappointing" numbers for EV sales showed a 51% increase for the first three quarters of this year in the U.S. And the chart from the WSJ shows that expectations for growth remain stratospheric, as charging infrastructure will be built out and "range anxiety" will diminish.

The WSJ article says total cost of ownership for small and midsized EVs has dropped below that of cars with internal combustion engines in China and Europe and may cross that dividing line in the U.S. next year. (While EVs cost more up-front, they require far less maintenance, and electricity typically costs much less per mile than gasoline.)

As with solar and wind, costs for EVs will continue to drop as production scales up, and the technology will continue to improve. In fact, battery costs are projected to reach territory by 2025 that we would have considered the Holy Grail during my stint at the Department of Energy: Goldman Sachs predicts that the average cost for an EV battery will fall below $100 per kilowatt hour. That would be down more than 93% since 2008 and a 40% decline just since 2022. Goldman Sachs projects that prices will keep falling 11% a year through 2030.

Of course, the context for all this improvement is a climate that is continuing to heat up. At this point, we're just trying to slow the rate of deterioration and minimize the increase in storms and wildfires that are devastating so many people and, in the process, generating massive insurance claims.

But we have to start somewhere.

Cheers,

Paul

P.S. As I said last week, I encourage you to attend the Town Hall being held on Thursday in Washington, DC, by my colleagues at the Insurance Information Institute. It will bring insurance executives and policy makers together to focus on how to attack the climate crisis. There are more details here, including a discount code. I hope to see you there.

A strong medical stop-loss program must be at the core, and there must be strong communication among the many stakeholders.

In the ever-evolving landscape of employee benefits, self-funding of healthcare offers the potential for greater cost control, flexibility and customization and has become the choice for many employers. At the heart of a successful self-funded approach is a strong medical stop loss insurance (MSL). And employers must understand the pivotal role that different stakeholders hold in designing an optimized MSL strategy.

Collaboration for Success: The Crucial Stakeholders

An effective MSL strategy goes beyond a mere insurance purchase. It's a comprehensive approach that requires collaboration among various stakeholders, so employers need to have clear lines of communication with, and input from, those accountable to the execution of their strategy. These range from captive insurers, reinsurers, clinical teams, underwriters and claims professionals to captive managers and participating companies – all essential for the thriving of the self-funded healthcare model.

Captive Insurer and Reinsurer: Building a Solid Foundation

The foundation of many strong MSL strategies lies in a well-structured captive insurance arrangement. The captive insurer, serving as the company's personal insurance segment, brings a degree of control and flexibility in managing risks. It facilitates a partnership with organizations to fine-tune insurance policies, ensuring they meet specific employee health demands and the participants' unique benefit needs. This customization can encompass coverage extents, terms, premium pricing and claim procedures.

Reinsurers, or excess risk protection through a fronting carrier, complement this structure by providing financial safeguarding, absorbing the shock of unusually high and unforeseen medical costs that could otherwise destabilize an organization’s financial health. These collaborative efforts between captive insurers and reinsurers provide a tailored, risk-mitigated coverage essential for the adaptability and durability of self-funded healthcare, addressing limitations often encountered in conventional insurance models.

See also: A Milestone in Healthcare

Clinical Team: Data-Driven Decision Making

The clinical team’s significance in formulating an effective MSL strategy is paramount. By scrutinizing data, evaluating risks and spotting health trends, these experts furnish employers with the necessary analytics to make informed decisions. Group programs like QBE North America's Agora stand out by embracing comprehensive health management, facilitated by a clinical risk management team analyzing claims utilization and costs to influence adoption of the most significant risk management strategies.

Underwriting and Claims Professionals: Balancing Risk and Cost

The expertise of underwriters and claims professionals is central to maintaining stable operations of any captive strategy. Their expertise ensures that the MSL strategy strikes a balance between managing financial exposure and controlling costs. They navigate the complex realm of past claims data and the current and potentially continuing health conditions of the plan’s membership. This deep dive analysis provides critical insight into the particular health risks specific to each employer’s situation.

For example, QBE North America's underwriting team leverages data analytics to tailor solutions that not only meet employers' financial objectives but also provide a buffer against unexpected medical expenses. Customizing MSL plans ensures alignment with a company’s distinctive needs, taking into account the specific health demands and risk profile of its employees.

Captive Managers and Participating Companies: Seamless Administration

Captive managers play a crucial role in overseeing the day-to-day operations of the self-funded healthcare strategy, as well. They ensure compliance, handle administrative tasks and facilitate communication among all stakeholders. However, the insurer or reinsurer is often called on to provide specialized support in adjudication of MSL claims, as complications may disrupt the health plan, third party administrator and member’s medical provider. This streamlined approach through a partnership allows participating companies to focus on their core operations while reaping the benefits of self-funded healthcare.

Monthly Stakeholder Meetings: Continuing Innovation

A standout feature of successful MSL captives is consistent and diligent engagement of the stakeholders in the partnership. Regularly scheduled meetings or discussions reviewing historical and emerging claim trends and loss ratio performance meetings are engines of innovation, promoting transparent communication, collaborative learning and perpetual refinement of strategies. They allow for targeted discussions to draw wisdom from various experts, encouraging informed, forward-thinking decisions in managing healthcare costs.

See also: How Digital Health, Insurtech Are Adapting

Transparency and Control: The Guiding Principles of MSL Captives

In an era where healthcare costs loom as a formidable challenge, MSL captives are guided by the principles of transparency and control. They represent the forefront of innovation in healthcare cost management, offering the industry a path toward sustainable solutions.

Conclusion

In the realm of self-funded healthcare, the significance of top-tier medical stop loss insurance partnerships cannot be overstated. A successful MSL strategy thrives on collaboration among diverse stakeholders, each playing a pivotal role in ensuring its effectiveness. Further, the importance of aligning with a fronting carrier with the financial class size and rating strength that demonstrates a track record and longevity cannot be overlooked.

As the landscape of employee benefits continues to evolve, the synergy among stakeholders will remain the cornerstone of a prosperous self-funded healthcare journey

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Tara Krauss is the head of accident & health for QBE North America.

She has been with QBE since 2009, including as SVP, underwriting operations. Prior to joining QBE, she held various underwriting and management positions with HCC Insurance (formerly LDG) and SLG Benefits & Insurance.

Tara holds a bachelor of science degree in finance from Merrimack College, where she graduated magna cum laude.