For those of us who have a front row seat to the digital transformation of the customer experience in life insurance, there is a sense that our world is being, or about to be, rocked.

In a way, it is; however, when you understand the customer experience cycle and all its component phases, you realize that the job of attracting new customers is, at its heart, fundamentally the same, but now there are more options for doing so.

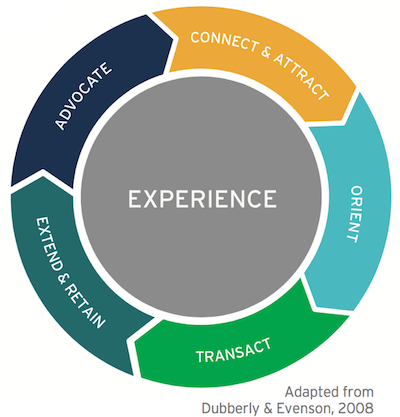

The experience cycle, a model developed by Dubberly & Evenson, 2008, is a great framework for understanding the phases that turn a prospect into a customer and a customer into a raving fan of your brand. While life insurance customers are seldom characterized as raving fans, there’s no reason the industry shouldn’t continue to strive for ways to achieve enthusiasm.

If we are to create raving fans, we must consider all the phases of the customer experience deeply. Then we must do our jobs right at each phase, understanding what drives satisfaction and behavior, what turns people off and what touchpoints are most important or provide missed opportunities.

Prior to the digital age, it was hard to do this in any setting other than in person or face to face with an agent. Now, if we are to recognize omnichannel expectations, we need to ensure we are covering all of these bases in whatever channel we are using. And if we are using multiple channels, we had better be saying and conveying the same thing, because gaps or inconsistencies create mistrust.

For example, if your website offers a needs assessment or a wellness scoring system, your agent channel should be well versed in it, too. Imagine someone engaging with your online tools, getting a result and then switching to your agent channel for advice about it. Then imagine the agent doesn’t know about the tool, doesn’t understand it or, worse, chooses to dismiss it. How would it make that potential customer feel about your company?

Yikes.

See also: Digital Innovation in Life Insurance

So a good starting point to avoiding that nightmare and others is to understand the phases of the customer experience cycle and make sure all channels are aligned similarly around the experience you want to create.

Here are the phases and what we should seek to achieve at each phase:

1) Connect and Attract: We must find the people who are best suited for what we offer and engage them in a way that’s meaningful to them, leading to openness to learning about what we can deliver.

Best suited means many things. With life insurance, in particular, it can mean health classification, financial status, need or even geography, as residents of certain states can’t get access to all products available. To figure out how to sort people, we need the most sophisticated tools at our disposal.

In addition, we must communicate in an authentic way, especially in scenarios where there is no human being talking with customers. If they are engaging in an online environment, the communication needs to “feel” human and real.

2) Orient: Here is where we help people understand what they should expect in the process, how long it takes and why we do things the way we do (e.g., asking personal questions). This helps set the expectation for what comes next so that they feel empowered and not “in the dark.”

3) Transact: Here is where we actually exchange a person’s time, data and money for a product. In life insurance, this is where the application lives and the way in which we take payment. There has been a great deal of industry focus and technology development around this phase to help life carriers improve the customer experience, work smarter (not harder) and attract new business by leveraging data and advanced analytics to use a more streamlined approach to assessing risk.

4) Extend and Retain: This is fancy talk for how we make sure we are delighting our new customers in unexpected ways and keeping them. For the life insurance industry, this phase will be particularly challenging, as it has been focused mostly on the process of how bills are received, preventing lapses and, ultimately, how claims are handled. These, however, are table stakes. Raving fans don’t come from meeting expectations; they come from exceeding them.

5) Advocate: Here is where a raving fan gets to tell others about his/her experience and presumably get others involved. While life insurance is generally a low-involvement product category, and one that is challenged by negativity associated with death, there are indirect ways to find positives within the experience.

We have an opportunity to create positive experiences through services, information exchange and learning and creating awareness of others’ experiences. The Ice Bucket Challenge for ALS is an example of where negative feelings of fear and helplessness were turned into people feeling empowered to help. The challenge went viral, creating much greater awareness and research funding for a disease that many knew little about. In what ways might the life insurance industry take a lesson from that?

The key to all of this is a deep understanding of your customers and potential customers coming from unrelenting curiosity, leading to compassion and empathy. Learning and embodying the tenets of the customer experience cycle is a good first step to understanding.

See also: Making Life Insurance Personal

If you’d like to learn more, click here to register to join us for a complimentary 45-minute webinar with 15-minute Q&A on Thursday, May 24, 2018, at 2:00 p.m. ET in partnership with LexisNexis Risk Solutions. During this first webinar, our speakers will explore the first phase of the customer experience cycle — Connect and Attract — and share key insights and findings that life carriers can use to transform the customer experience in life insurance, starting at the point of marketing.

1) Connect and Attract: We must find the people who are best suited for what we offer and engage them in a way that’s meaningful to them, leading to openness to learning about what we can deliver.

Best suited means many things. With life insurance, in particular, it can mean health classification, financial status, need or even geography, as residents of certain states can’t get access to all products available. To figure out how to sort people, we need the most sophisticated tools at our disposal.

In addition, we must communicate in an authentic way, especially in scenarios where there is no human being talking with customers. If they are engaging in an online environment, the communication needs to “feel” human and real.

2) Orient: Here is where we help people understand what they should expect in the process, how long it takes and why we do things the way we do (e.g., asking personal questions). This helps set the expectation for what comes next so that they feel empowered and not “in the dark.”

3) Transact: Here is where we actually exchange a person’s time, data and money for a product. In life insurance, this is where the application lives and the way in which we take payment. There has been a great deal of industry focus and technology development around this phase to help life carriers improve the customer experience, work smarter (not harder) and attract new business by leveraging data and advanced analytics to use a more streamlined approach to assessing risk.

4) Extend and Retain: This is fancy talk for how we make sure we are delighting our new customers in unexpected ways and keeping them. For the life insurance industry, this phase will be particularly challenging, as it has been focused mostly on the process of how bills are received, preventing lapses and, ultimately, how claims are handled. These, however, are table stakes. Raving fans don’t come from meeting expectations; they come from exceeding them.

5) Advocate: Here is where a raving fan gets to tell others about his/her experience and presumably get others involved. While life insurance is generally a low-involvement product category, and one that is challenged by negativity associated with death, there are indirect ways to find positives within the experience.

We have an opportunity to create positive experiences through services, information exchange and learning and creating awareness of others’ experiences. The Ice Bucket Challenge for ALS is an example of where negative feelings of fear and helplessness were turned into people feeling empowered to help. The challenge went viral, creating much greater awareness and research funding for a disease that many knew little about. In what ways might the life insurance industry take a lesson from that?

The key to all of this is a deep understanding of your customers and potential customers coming from unrelenting curiosity, leading to compassion and empathy. Learning and embodying the tenets of the customer experience cycle is a good first step to understanding.

See also: Making Life Insurance Personal

If you’d like to learn more, click here to register to join us for a complimentary 45-minute webinar with 15-minute Q&A on Thursday, May 24, 2018, at 2:00 p.m. ET in partnership with LexisNexis Risk Solutions. During this first webinar, our speakers will explore the first phase of the customer experience cycle — Connect and Attract — and share key insights and findings that life carriers can use to transform the customer experience in life insurance, starting at the point of marketing.

1) Connect and Attract: We must find the people who are best suited for what we offer and engage them in a way that’s meaningful to them, leading to openness to learning about what we can deliver.

Best suited means many things. With life insurance, in particular, it can mean health classification, financial status, need or even geography, as residents of certain states can’t get access to all products available. To figure out how to sort people, we need the most sophisticated tools at our disposal.

In addition, we must communicate in an authentic way, especially in scenarios where there is no human being talking with customers. If they are engaging in an online environment, the communication needs to “feel” human and real.

2) Orient: Here is where we help people understand what they should expect in the process, how long it takes and why we do things the way we do (e.g., asking personal questions). This helps set the expectation for what comes next so that they feel empowered and not “in the dark.”

3) Transact: Here is where we actually exchange a person’s time, data and money for a product. In life insurance, this is where the application lives and the way in which we take payment. There has been a great deal of industry focus and technology development around this phase to help life carriers improve the customer experience, work smarter (not harder) and attract new business by leveraging data and advanced analytics to use a more streamlined approach to assessing risk.

4) Extend and Retain: This is fancy talk for how we make sure we are delighting our new customers in unexpected ways and keeping them. For the life insurance industry, this phase will be particularly challenging, as it has been focused mostly on the process of how bills are received, preventing lapses and, ultimately, how claims are handled. These, however, are table stakes. Raving fans don’t come from meeting expectations; they come from exceeding them.

5) Advocate: Here is where a raving fan gets to tell others about his/her experience and presumably get others involved. While life insurance is generally a low-involvement product category, and one that is challenged by negativity associated with death, there are indirect ways to find positives within the experience.

We have an opportunity to create positive experiences through services, information exchange and learning and creating awareness of others’ experiences. The Ice Bucket Challenge for ALS is an example of where negative feelings of fear and helplessness were turned into people feeling empowered to help. The challenge went viral, creating much greater awareness and research funding for a disease that many knew little about. In what ways might the life insurance industry take a lesson from that?

The key to all of this is a deep understanding of your customers and potential customers coming from unrelenting curiosity, leading to compassion and empathy. Learning and embodying the tenets of the customer experience cycle is a good first step to understanding.

See also: Making Life Insurance Personal

If you’d like to learn more, click here to register to join us for a complimentary 45-minute webinar with 15-minute Q&A on Thursday, May 24, 2018, at 2:00 p.m. ET in partnership with LexisNexis Risk Solutions. During this first webinar, our speakers will explore the first phase of the customer experience cycle — Connect and Attract — and share key insights and findings that life carriers can use to transform the customer experience in life insurance, starting at the point of marketing.