Usage-based pricing is a fascinating topic for insurers. A technology that allows persistent monitoring of risk exposure during the coverage period could potentially enable insurers to price each risk at the best rate.

The potential, however, is not the reality.

In 2017, 14 million policies sent telematics data to insurers around the world, of which 4.4 million were in the U.S market, based on an estimate by the IoT Insurance Observatory, an insurance think tank that has aggregated almost 50 insurers, reinsurers and tech players between North America and Europe. (In the U.S., there were a further 3.6 million policies that are still active and commonly defined as telematics but that in the past had a dongle only and didn’t send any data to insurers last year.)

However, less than 9% of the global insurance telematics policies were characterized by usage-based pricing, which is a mechanism that charges the policyholders for the current period of coverage based on how they behave (mileage or driving behavior) during this period.

Instead, the vast majority of the telematics policies bought by customers around the world today have a defined up-front price for the current policy term. Moreover, the telematics data registered during the policy period does not affect this price in any way, and is used only for proposing a renewal price at the end of the policy. So, these policies are not usage-based because at the beginning of each policy term the customers are sure about the amount they are going to pay for the policy, regardless of their behavior during the months of coverage.

These existing implementations of telematics-based pricing are somewhat validated from consumer perceptions toward insurance. In a survey of 1,046 U.S. consumers, the Casualty Actuarial Society Insurance On-Demand Working Party has addressed and demystified some of the behavioral economics assumptions on the insurance products. The research showed that only 32% of consumers reviewed their personal lines (auto and home) coverage more than once per year. Furthermore, 89% of consumers said they would rather pay a single, stable price per year compared with paying per usage without a certainty of total price. Usage-based auto insurance, across the entire on-demand category studied by the working group, is attractive to people penalized by traditional insurance products, that is, consumers with low usage who would otherwise have to pay for more coverage than they need.

Potential and Success Stories

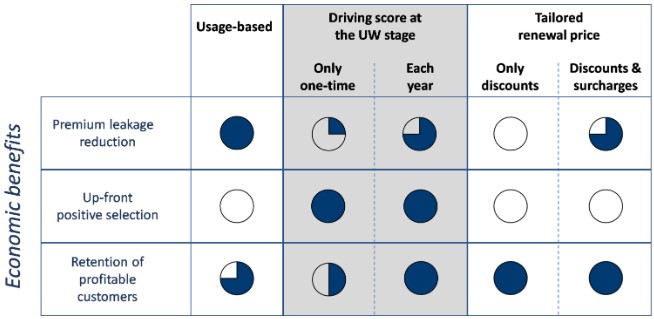

The usage-based approach persistently monitors the policyholders and charges (potentially) each customer a rate commensurate with actual exposure, minimizing the premium leakage in each coverage period. The resulting minimized earning volatility from usage-based pricing allows insurers to increase the leverage and through this to improve investment return and the return on equity of the company. This approach also allows for increased retention of good risks, at any pricing level, which are penalized by competitors with less accurate pricing mechanisms. The quality of the portfolio is improved (with more profitable customers) at each renewal.

The resulting lower volatility from usage-based pricing and better quality of the portfolio over time would also enable insurers to negotiate lower reinsurance costs.

But while usage-based insurance could theoretically be a profitable option for insurers, the problem seems to be the lack of customer demand for an insurance product where there isn’t a defined up-front price for all the entire coverage period..

See also: Rethinking the Case for UBI in Auto

Newcomers to the insurance market are bringing a different perspective to the problem, recognizing that small clusters of drivers who have been heavily penalized by the current insurance rates—such as extremely low-mileage drivers, or extremely safe drivers without a credit score—could be enough to start a niche business. There are a few success stories of insurtech startups, such as Insure The Box and Metromile, which have been able to build portfolios around 100,000 policies and relevant company evaluations within six to seven years.

Driving Scores at the Underwriting Stage

One way to combat the lack of market fit that has affected the usage-based adoption could be to use a driving score at the underwriting stage. This way, insurers will make an up-front quotation by using—together with traditional data—the driving data.

The value created through this approach is clear and similar to experiences the sector has had integrating new risk factors (e.g. credit scoring) in pre-existing risk models. This telematics-enhanced risk model enables more accurate pricing. This, in turn, allows insurers to generate favorable selection by attracting the best risks for each pricing level (leaving the worst to the competitors). Through the creation of smaller and more homogeneous clusters of clients, this approach even reduces premium leakage, reducing the volatility. And, if the driving score is used at each renewal, there is a chance of improving portfolio quality over time (at any pricing level), with insurers using driving scores for underwriting, benefiting from retention of the most profitable customers--those who are penalized by competitors with less accurate pricing mechanisms.

The ROI of this approach is extremely positive, but the current scenario for obtaining the customer driving score seems very different from the scenario we have known for the credit score. The credit score (or the granular data necessary to calculate it) is available on the entire customer base and certified by reliable third parties, so each insurer can gather this data any time a customer requests a quotation via an agent, a broker, a call center or even online. Moreover, anyone who doesn’t have a credit score is considered a nonstandard risk. So, the concretization of the driving score dream requires the availability and reliability of third-party data for the insurers and, most importantly, the creation of frictionless purchasing processes for the clients.

Data exchanges, which bring OEM data to insurers, have been present in the U.S. customer market for a few years, but because there are many points of friction throughout OEM funnels, they still represent only 2% of the U.S. telematics insurance portfolio. This customer fatigue is due to the need to opt in to request a quotation. Eligibility for the opt-in comes in a moment when he is not shopping around for insurance coverage (a few months after the purchase of the new car). The quotations, which are done with anonymized data, are only indicative, so the customer needs to add data later to receive the real proposal.

Try Before You Buy

A different way to concretize the wish to access a driving score any time an insurance price quotation is calculated is by using a try-before-you-buy app. Given the current level of smartphone penetration, such an app likely provides an easier way to address a large part of the market than with the data exchanges and may also reduce customer frictions. As insurtech carrier Root is currently doing, an insurer can ask a prospect to download an app on his smartphone, calculate the driving score through collected data and, after a while, calculate the quotation incorporating the customer’s driving score. Using this approach, this less-than-two-year-old auto carrier startup wrote 1.5 times more premium than the more-talked-about carrier Lemonade. (Both are insurtech carriers, although Lemonade is writing renters insurance, and Root is writing auto). Root even entered in the insurtech unicorn club in August, thanks to a $100 million round of funding raising the valuation to $1 billion.

Tailored renewal price

As mentioned, 90% of the current global telematics policies only use the driving data for tailoring the renewal price to the customers after having monitored them for a few months (rollover approach) or for the entire coverage period (leave-in approach).

Are insurers achieving any economic value through this pricing approach?

They can increase the retention of the most profitable risks at each pricing level by providing a discount at renewal. However, this additional discount reduces the profitability of these policyholders. So the chance to create some value through this “discounted retention” is linked to the presence of a high-level churn rate. If surcharges to the worst risks at each pricing level are added, insurers will have the opportunity at renewal to partially reduce the premium leakage they have identified on these risks, or push some of them toward competitors.

The accompanying chart (right side) summarizes these pricing thoughts: The expected ROI of the “discount at renewal” is definitely lower than the driving score scenario—it structurally misses the ability to have a positive up-front selection by attracting the better risks at each pricing level—but it is positive if surcharges are added.

The IoT Insurance Observatory has found that a large portion of the policies using driving data for tailoring renewal prices have not resulted in any bad driver penalties.

So, are these telematics portfolios destroying value instead of creating it?

The reality is that there is value created on these portfolios, but the value is not tied to pricing. And some of the pricing approaches are even reducing that value.

First, there are many examples of the risk self-selection impact of all the telematics-based products around the world. Even if two customers seem to be equal based on their characteristics, the one who accepts the telematics product has a lower probability of generating a loss. The stronger the monitoring message on the product storytelling, the higher the self-selection effect. The most statistically robust study is on the Italian auto insurance market, where this risk self-selection effect has accounted for 20% of the claim frequency. In this market, telematics products currently represent more than one-fifth of the personal lines auto insurance business, and the storytelling of the product is hugely focused on monitoring and customer support at the moment of a crash.

Other than risk self-selection, three other telematics-based use cases have been exploited by insurers.

Some international insurers have reinvented their claims processes through telematics data: Their new paradigm is fact-based, digital and real-time. Insurers such as UnipolSai have introduced tools for their claim handlers that allow a quicker and more precise crash responsibility identification and have been providing precious insights to support the activity of all the actors involved in the claim supply chain (both loss adjusters and doctors).

See also: Is Usage-Based Insurance a Bubble?

A second well-demonstrated telematics use case is the change of driver behavior. VitalityDrive introduced by the South African insurance company Discovery Insure is the first insurance telematics product entirely focused on promoting safer behavior. All the product features—from gas cash-back (up to 50% of fuel spending per month) to active rewards through the app (including coffee, smoothies and car wash vouchers)—are contributing to the risk reduction of the book of business and to increased retention of the best risks.

Both the Italian and South African experiences have even been characterized by the insurers’ ability of enhancing the insurance value proposition by adding telematics-based services bundled to the auto insurance coverage. The fees paid by customers for these services almost offset all the costs of the telematics services on the insurers’ income statements

Based on the experience of the IoT Insurance Observatory, global insurance telematics best practices have generated more value through these four use cases than through pricing as of today. So, the sum of the self-selection effect, the claim cost reduction and the economic impact of changes of behavior allows an insurer to provide an important up-front discount at the same level for all the new telematics-based policyholders.

This relevant level of up-front discount -- 20% or more -- has been able to drive the adoption (overcoming any eventual customer privacy skepticism) because it fits with the customer desire to save money, contrasting the low adoption rates generated for more than a decade in the U.S. where up-front discount offers are typically only 5%.

The discount should be maintained, on average, at the same level at the renewal stage. Moreover, an additional economic value can be generated—at each pricing level—by providing additional discounts to the best policyholders and reducing the discount to the worst ones.

This is what the international best practices are doing today.

The IoT Insurance Observatory has found that a large portion of the policies using driving data for tailoring renewal prices have not resulted in any bad driver penalties.

So, are these telematics portfolios destroying value instead of creating it?

The reality is that there is value created on these portfolios, but the value is not tied to pricing. And some of the pricing approaches are even reducing that value.

First, there are many examples of the risk self-selection impact of all the telematics-based products around the world. Even if two customers seem to be equal based on their characteristics, the one who accepts the telematics product has a lower probability of generating a loss. The stronger the monitoring message on the product storytelling, the higher the self-selection effect. The most statistically robust study is on the Italian auto insurance market, where this risk self-selection effect has accounted for 20% of the claim frequency. In this market, telematics products currently represent more than one-fifth of the personal lines auto insurance business, and the storytelling of the product is hugely focused on monitoring and customer support at the moment of a crash.

Other than risk self-selection, three other telematics-based use cases have been exploited by insurers.

Some international insurers have reinvented their claims processes through telematics data: Their new paradigm is fact-based, digital and real-time. Insurers such as UnipolSai have introduced tools for their claim handlers that allow a quicker and more precise crash responsibility identification and have been providing precious insights to support the activity of all the actors involved in the claim supply chain (both loss adjusters and doctors).

See also: Is Usage-Based Insurance a Bubble?

A second well-demonstrated telematics use case is the change of driver behavior. VitalityDrive introduced by the South African insurance company Discovery Insure is the first insurance telematics product entirely focused on promoting safer behavior. All the product features—from gas cash-back (up to 50% of fuel spending per month) to active rewards through the app (including coffee, smoothies and car wash vouchers)—are contributing to the risk reduction of the book of business and to increased retention of the best risks.

Both the Italian and South African experiences have even been characterized by the insurers’ ability of enhancing the insurance value proposition by adding telematics-based services bundled to the auto insurance coverage. The fees paid by customers for these services almost offset all the costs of the telematics services on the insurers’ income statements

Based on the experience of the IoT Insurance Observatory, global insurance telematics best practices have generated more value through these four use cases than through pricing as of today. So, the sum of the self-selection effect, the claim cost reduction and the economic impact of changes of behavior allows an insurer to provide an important up-front discount at the same level for all the new telematics-based policyholders.

This relevant level of up-front discount -- 20% or more -- has been able to drive the adoption (overcoming any eventual customer privacy skepticism) because it fits with the customer desire to save money, contrasting the low adoption rates generated for more than a decade in the U.S. where up-front discount offers are typically only 5%.

The discount should be maintained, on average, at the same level at the renewal stage. Moreover, an additional economic value can be generated—at each pricing level—by providing additional discounts to the best policyholders and reducing the discount to the worst ones.

This is what the international best practices are doing today.

The IoT Insurance Observatory has found that a large portion of the policies using driving data for tailoring renewal prices have not resulted in any bad driver penalties.

So, are these telematics portfolios destroying value instead of creating it?

The reality is that there is value created on these portfolios, but the value is not tied to pricing. And some of the pricing approaches are even reducing that value.

First, there are many examples of the risk self-selection impact of all the telematics-based products around the world. Even if two customers seem to be equal based on their characteristics, the one who accepts the telematics product has a lower probability of generating a loss. The stronger the monitoring message on the product storytelling, the higher the self-selection effect. The most statistically robust study is on the Italian auto insurance market, where this risk self-selection effect has accounted for 20% of the claim frequency. In this market, telematics products currently represent more than one-fifth of the personal lines auto insurance business, and the storytelling of the product is hugely focused on monitoring and customer support at the moment of a crash.

Other than risk self-selection, three other telematics-based use cases have been exploited by insurers.

Some international insurers have reinvented their claims processes through telematics data: Their new paradigm is fact-based, digital and real-time. Insurers such as UnipolSai have introduced tools for their claim handlers that allow a quicker and more precise crash responsibility identification and have been providing precious insights to support the activity of all the actors involved in the claim supply chain (both loss adjusters and doctors).

See also: Is Usage-Based Insurance a Bubble?

A second well-demonstrated telematics use case is the change of driver behavior. VitalityDrive introduced by the South African insurance company Discovery Insure is the first insurance telematics product entirely focused on promoting safer behavior. All the product features—from gas cash-back (up to 50% of fuel spending per month) to active rewards through the app (including coffee, smoothies and car wash vouchers)—are contributing to the risk reduction of the book of business and to increased retention of the best risks.

Both the Italian and South African experiences have even been characterized by the insurers’ ability of enhancing the insurance value proposition by adding telematics-based services bundled to the auto insurance coverage. The fees paid by customers for these services almost offset all the costs of the telematics services on the insurers’ income statements

Based on the experience of the IoT Insurance Observatory, global insurance telematics best practices have generated more value through these four use cases than through pricing as of today. So, the sum of the self-selection effect, the claim cost reduction and the economic impact of changes of behavior allows an insurer to provide an important up-front discount at the same level for all the new telematics-based policyholders.

This relevant level of up-front discount -- 20% or more -- has been able to drive the adoption (overcoming any eventual customer privacy skepticism) because it fits with the customer desire to save money, contrasting the low adoption rates generated for more than a decade in the U.S. where up-front discount offers are typically only 5%.

The discount should be maintained, on average, at the same level at the renewal stage. Moreover, an additional economic value can be generated—at each pricing level—by providing additional discounts to the best policyholders and reducing the discount to the worst ones.

This is what the international best practices are doing today.