Insurance telematics has been out there for more than 20 years. Many insurers have tried to play with the technology, but few have succeeded in using the data available from connected telematics devices. The potential of this technology was misunderstood, and best practices have remained almost unknown, as it was not common in the insurance sector to look for innovation in other geographies, such as Italy, where progress has been made.

But the insurance sector is being overtaken by a desire to change, and it’s becoming more common to see innovation scouting taking place on an international level. In the last two years, billions of dollars have been invested in insurance startups; innovation labs and accelerators have popped up; and many insurance carriers have created internal innovation units.

On the other hand, I’m starting to hear a new wave of disillusion about the lack of traction of insurtech initiatives, the failure of some of them, or insurtech startups radically changing from their original business models.

In a world that tends toward hyperconnectivity and the infiltration of technology into all aspects of society, I’m firmly convinced all insurance players will be insurtech—meaning they all will be organizations where technology will prevail as the key enabler for the achievement of strategic goals.

See also: Telematics Has 2 Key Lessons for Insurtechs

Starting from this premise, I’d like to focus on two main points:

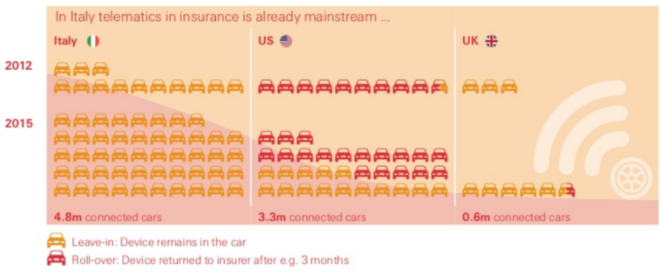

In contrast, another market used telematics in a completely different way—and it succeeded. Almost 20% of auto insurance policies sold and renewed in the last quarter of 2016 in Italy had a telematics device provided by an insurer based on the IVASS data. The European Connected Insurance Observatory—the European chapter of the insurance think tank I created, consisting of more than 30 European insurers, reinsurers and tech players with an active presence in the discussion from their Italian branches—estimated that 6.3 million Italian customers had a telematics policy at the end of 2016.

Some insurers in this market were able to use the telematics data to create value and share it with customers. The most successful product with the largest traction is based on three elements:

In contrast, another market used telematics in a completely different way—and it succeeded. Almost 20% of auto insurance policies sold and renewed in the last quarter of 2016 in Italy had a telematics device provided by an insurer based on the IVASS data. The European Connected Insurance Observatory—the European chapter of the insurance think tank I created, consisting of more than 30 European insurers, reinsurers and tech players with an active presence in the discussion from their Italian branches—estimated that 6.3 million Italian customers had a telematics policy at the end of 2016.

Some insurers in this market were able to use the telematics data to create value and share it with customers. The most successful product with the largest traction is based on three elements:

- The ability of the insurance sector to innovate is incredibly higher than the image commonly perceived.

- While not all insurtech innovations will work, a few of them will change the sector.

- Productivity (generate more sales).

- Profitability (improve loss or cost ratios).

- Proximity (improve customer relationships through numerous customer touchpoints).

- Persistency (account retention, renewal rate increase).

In contrast, another market used telematics in a completely different way—and it succeeded. Almost 20% of auto insurance policies sold and renewed in the last quarter of 2016 in Italy had a telematics device provided by an insurer based on the IVASS data. The European Connected Insurance Observatory—the European chapter of the insurance think tank I created, consisting of more than 30 European insurers, reinsurers and tech players with an active presence in the discussion from their Italian branches—estimated that 6.3 million Italian customers had a telematics policy at the end of 2016.

Some insurers in this market were able to use the telematics data to create value and share it with customers. The most successful product with the largest traction is based on three elements:

- A hardware device provided by the insurer with auto liability coverage, self-installed by the customer on the battery under the car’s hood.

- A 20% upfront flat discount on annual auto liability premium.

- A suite of services that goes beyond support in the case of a crash to many other different use cases—stolen vehicle recovery, car finder, weather alerts—with a service fee around €50 charged to the customer.

- Saving money on a compulsory product. Research shows that pricing is relevant in customer choice.

- Receiving support and convenience at the moment of truth—the claims moment. Insurers are providing a better customer experience after a crash using the telematics data. Just think of how much information can be gathered directly from telematics data without having to question the client.

- Receiving services other than insurance. That’s something roughly 60% of insurance customers look forward to and value, according to Bain’s research on net promoter scores published last year.

- The fee to the customer is close to the annual technology cost for the hardware and services. The €50 mentioned above represents more than 5% of the insurance premium for the risky clients paying an annual premium higher than €1,000. This cluster represents less than 5% of the Italian telematics market. The fee is more than 10% of the premium for the customers paying less than €400. This cluster represents more than 40% of the Italian telematics market.

- The product is a constant, daily presence in the car, with the driver, with no possibility of turning it off. While the product ensures support in case of a crash, it is also a tremendous deterrent for anyone tempted to make a fraudulent claim, as well as for drivers engaging in risky behavior otherwise hidden from the insurer.

- The telematics portfolio has shown on average 20% lower claims frequency on a risk-adjusted basis than the non-telematics portfolio, based on the analysis done by the Italian Association of Insurers.

- Insurer best practices have achieved additional savings on the average cost of claims by introducing a claims management approach as soon as a crash happens and by using the objective reconstruction of the crash dynamic to support the claim handler’s decisions.

- A suite of telematics services is delivered to the customer, along with a 25% upfront discount on the auto liability premium.