DISRUPTION IN THE AUTOMOTIVE ECOSYSTEM: What to Expect, and How to Survive and Win

For the purposes of this paper, and to explain the codependencies and inter-industry impacts, we’ve chosen to define the auto ecosystem as including all business segments affected by the automobile, including: auto manufacturing, auto buyers and drivers; collision repairers; aftermarket suppliers, including parts providers; auto insurance companies and their policyholders; and the deep and extensive claims and services supply chain that supports them, such as the technology and information provider segments. Given the broad scope and complexity of the component topics, we have identified and provided a degree of depth on each one, but by no means should this information be considered exhaustive. The entire auto ecosystem is in the midst of significant disruption, and the dizzying pace of change will only continue to accelerate. This disruption is the result of the convergence of upstream upheaval in these sub-segments of the auto ecosystem:

• “new consumer” behavior and expectations

• technology evolution, including mobility and the Internet of Things

• the digital data gold rush and the adoption of advanced analytics

• globalization integration, collaboration and supply chain consolidation in the automotive ecosystem

• collision repair industry consolidation

Over the last 30 years, the auto repair and automotive aftermarket segments were part of a steady and inevitable evolution. During this long-term progression, the auto physical damage industry adapted to a myriad of business innovations, technology enablers, program and process changes and product and service introductions. Some resisted these innovations as either real or perceived business disruptions or dis-intermediation while others embraced them as opportunities to be leveraged for business, market and strategic transformation.

The 2007/2008 “Black Swan” event, the U.S. recession, affected our entire economy and loomed large and ominous for a number of years. This became the foundation for today’s unmatched auto physical damage industry transformation. It triggered the start of unprecedented structural change within the U.S. and Canadian auto repair and aftermarket segments. This changing landscape became part of four distinct, yet connected, marketplace phases: contraction, consolidation, convergence and constructive transformation, which continue today.

Additionally, these four phases are being affected by a confluence of numerous, dynamic and impinging forces, which have both disruptive and transformational influences on today’s stakeholders. Some of the more influential external impact factors include:

• globalization

• private equity investment

• accident safety and avoidance technology

• predictive analytics

• telematics and integrated claims process models

• insurer multiple-shop operator, strategic performance-based, direct repair program (DRP) contracts

• new and hybrid direct repair program models

• OEM- certified networks’ influence in the repair process

• morphing demographics

• multi-system operators (MSOs), growing market dominance and insurance carrier acceptance

• repair segmentation

• national technician shortage

• complex vehicle technology and proliferation of advanced materials

• urbanization

• increased complexity in insurance company DRP participation requirements

Consequently, the traditional process of linear thinking, with its straightforward cause-and-effect structure, is giving way to a more realistic and more complex multi-dimensional thinking pattern that heightens the understanding of the frequency, acceleration and degree of change. It is important, in light of this, to build and leverage a strategic alliance ecosystem with customers, suppliers, competitors, investors and business partners to maintain and grow a collaborative brain trust. This shared commitment will help to co-create and foster constructive change within an organization in an attempt to influence its uncertain environment for the mutual benefit of all strategic partners.

Evidence of disruption in the auto insurance industry and its extensive supply chain is plentiful and portends even greater change. Long-standing leaders in the U.S. auto insurance industry have lost significant market share to more innovative consumer-centric carriers. Advanced analytics and telematics technologies have combined to enable new forms of insurance products, including usage-based insurance. The Internet of Things, including the connected car, will amplify this trend going forward and literally change the fundamental nature of insurance and risk management products, solutions and servicing. For example, consumers are now shopping for and purchasing auto insurance, and submitting and receiving claim payments, on their smartphones. Fueled by the entry of large and growing pools of private equity capital, rapid industry consolidation is occurring across several supply chain segments including the once highly fragmented collision repair industry and alternative parts supplier markets.

In this dynamic environment, we believe that the ultimate leaders and winners in 2015 and beyond will be those companies that most successfully focus and execute on the development of compelling personal mobility solutions; transform product development and distribution around the new consumer; leverage data and analytics across the enterprise; think, plan and execute globally; and aggressively collaborate, partner and affiliate as effectively as possible.

The new consumer, mobility and the internet of things

Today’s consumer is totally unlike that of the past, and they have created new challenges and opportunities for all participants in the automotive ecosystem, in particular for auto insurers. This new consumer, epitomized by Millennials, has embraced mobile technologies and the social media they support. This phenomenon has fundamentally changed how insurance is branded, marketed and sold. Moving forward, this same mobility will enable insurers to design completely new types of insurance products and manage risks much more effectively for policyholders and themselves.

The most disruptive group of mobility technologies is the rapidly emerging Internet of Things, much of which is controlled today by industry outsiders. The potential impact on numerous aspects and multiple lines of insurance, as well as on the rest of the auto ecosystem, is enormous.

Of related concern to the insurance industry should be the potential for these outsiders to leverage this valuable information to enter the business and become competitors. Some recent acquisitions include Facebook’s purchase of the fitness and location app Moves, Monsanto’s acquisition of crop insurance and data company Climate Corp. (which was started by former Google executives) and Google’s acquisitions of the connected home devices and security company Nest and the Israeli location-mapping service Waze. Verizon acquired Hughes Telematics in 2012.

The data generated by all of these businesses, which was never before so digitally available, can be combined with advanced analytics to accurately establish and manage individual and property risks. The ability to successfully acquire, control and effectively translate and use all of this data will determine the insurance industry’s digital gold rush winners and losers of the future.

Impact of OEM globalization

The impact of automotive industry globalization is pervasive within the automotive and aftermarket industries. It is one of the more significant continuing influential macro factors within the larger constellation and confluence of simultaneous conditions affecting the auto physical damage landscape. For example, the change caused by how vehicle manufacturers are aggressively re-engineering and consolidating their light vehicle platforms is evident in the worldwide auto manufacturing transformation underway; General Motors is planning to reduce in 10 years its current 26 global production platforms to just four by 2025. This globalization of cars and its many OEM implications will continue to drive significant change throughout the entire property and casualty auto insurance and auto physical damage aftermarket supply chain.

One of the key drivers of this manufacturing transformation is the National Highway Traffic Safety Administration’s CAFE standards, which require average manufacturer fleet fuel consumption to drastically improve from today’s 30.2 miles per gallon to 54.5 miles per gallon by 2025. By the 2016 model year alone, there will be approximately 250 new and different vehicle debuts and redesigns from both U.S. and foreign manufacturers. Ultimately, achieving strategic goals and objectives such as reducing fuel consumption and gas emissions by improving fuel economy and reducing the environment’s carbon footprint reflect the current megatrends end game.

As the OEMs drive to innovate globally, there will be intended and unintended outcomes involving the use of many new materials, engine downsizing, alternative powertrains, advanced integrated electronics, telematics and new repair technologies and processes, and producing light-weight vehicles. These innovations will be seen as a disruption by some, while being embraced by others who seek to leverage these global influences for future growth and competitive advantage.

Other ecosystem and supply chain industry consolidation

Another globalization perspective is being driven by increasing international trade and investment by private equity and strategic buyers involving an explosion in mergers and acquisitions within the property and casualty insurance and auto physical damage industries in the U.S. and throughout the world.

The following is a partial list of some of the more relevant recent M&A activity by U.S. and international companies in this ecosystem:

• CCC Information Services acquires telematics and UBI solutions provider DriveFactor

• Hartford-based Insurity acquires Montreal-based Oceanwide

• Patriot National’s Technology Solutions unit acquires Vikaran Solutions in Pune, India

• Uber acquires control of Metromile (PAYD) insurance, U.S.

• Google acquires CoverHound, an insurance aggregation website, U.S.

• Google’s Nest unit buys Dropcam

• Fosum buys Meadowland, a first-ever acquisition by a Chinese insurer of a U.S. insurer

• Alliant Insurance Services of the U.S. buys the U.S. agency business of Australia’s QBE

• Majesco acquired Cover-All Technologies and Agile Technologies, U.S.

• Symphony Technology Group acquires Aon e-Solutions from Aon (UK)

• ACE (Bahamas) buys Fireman’s Fund U.S. personal lines business

• Vista Equity acquires TIBCO for $4.3 billion, U.S.

• Onex (Canadian private equity firm) acquires York Risk Services for U.S. $1.325 billion, U.S.

• Element Financial (Canada) acquires U.S.-based PH&H fleet management business for U.S. $1.4 billion

• Mapfre Insurance, Spain, acquires Commerce Insurance and MiddleOak personal lines, U.S.

• QBE Insurance, Australia, acquires Balboa Insurance, U.S.

• Travelers Insurance, U.S., acquires Dominion Insurance, Canada

• Desjardins Insurance, Canada, acquires State Farm Canada, U.S.

• Boyd Group, Canada, acquirers Gerber Collision and Glass, U.S.

• OMERS, Canada, acquires Caliber Collision Centers, U.S.

• UniSelect, Canada, acquires Finish-Master, U.S.

• Solera, U.S., acquires Velexa Technologies, UK

• Solera, U.S., acquires CAP Automotive, UK

• Belron, South Africa, acquires Safelite Glass, U.S.

• LKQ, U.S., acquires EuroParts, UK

• UBM, UK, acquires Advanstar-Motor Age and Auto Body Repair News ABRN, U.S.

• The Carlyle Group (owners of Axalta and investors in Service King) acquires Nationwide Accident Repair Services of the UK

These acquisitions reflect the growing trend of an increasingly integrated global insurance and automotive economy resulting in an extension of business and market international strategies, introduction of new, innovative and disruptive technologies and processes, and brand expansion while also managing resource and risk diversification.

The digital data gold rush/ advanced analytics

We have entered a “digital Gold Rush” era – a modern version of the California Gold Rush of 1849 – with the gold being digital data, which is beginning to flow in torrents. This has huge implications for the insurance industry, and not least for property and casualty claims. Digitization is already having an impact across the claims technology and services supply chain, forcing supplier consolidation and compressing customer service cycle and response times to near real time. These forces will affect property and casualty claims technology, as well as information and services provider segments, which have historically been highly fragmented and privately owned and operated. National consolidation, volume aggregation and the infusion of sizable technology investments led by professional management teams offer significant medium-term rewards to the participants.

The most potentially disruptive group of digital technologies of all is the rapidly emerging “Internet of Things” or “M2M” (machine-to-machine) technology, with its potential impact across multiple lines of insurance. Of related concern to the industry should be the potential for non-traditional competitors to leverage M2M data and enter their business. An example is Google’s acquisition of the connected home devices and security company Nest Labs. The data acquired in all of these businesses, never before so digitally available, will be combined with advanced analytics to accurately establish and manage individual and property risks.

These powerful forces are all converging to drive mergers and acquisitions activity to unprecedented levels in the property and casualty insurance claims technology ecosystem, attracting increasing numbers of private equity and strategic investors, and providing attractive exit opportunities and strategic alternatives for participants, all while creating exciting new and innovative technology-enabled capabilities for insurers, agents, brokers and consumers.

Private equity and collision repair industry consolidation

The first two phases of the current collision repair industry structural transformation, contraction and consolidation, are part of a four-phase model consisting of contraction, consolidation, convergence and constructive transformation. These first two phases began to emerge and quickly expand after the start of the recession in December 2007. Simultaneously, private equity groups turned their attention to the collision repair industry; they looked under the hood and liked what they saw.

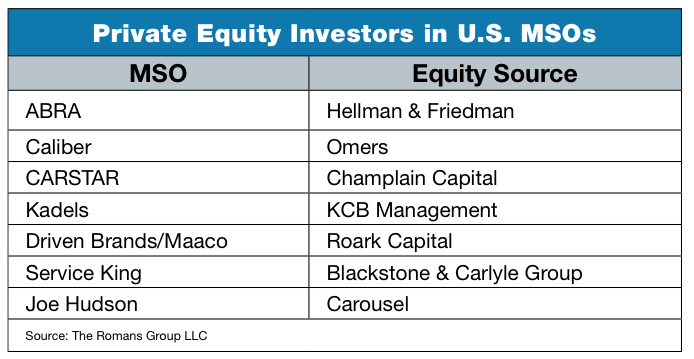

Private equity firms were on the hunt to find alternative investments that could yield comparative or better returns than were currently available during the trough and slow recession recovery between 2007 and today. Additionally, their interest is backed and driven by unprecedented amounts of strategic buyer, private equity and pension fund dry powder/cash-seeking investments that can drive higher valuations and returns on their capital invested. The current private equity investor groups competing in the consolidation of the auto repair industry are identified in the chart below.

There are a number of factors affecting the continued attractiveness of investing in the collision repair industry.

• the collision repair industry’s structural transformation is still early to mid-stage

• the stigma from consolidation’s failed first attempt during the early 2000s is now fully erased

• excess strategic and private equity capital continues to seek high-return, quick-turn investments, which are characterized by recurring revenue, free cash flow and attractive returns on invested capital

• aggressive MSO consolidator and private equity competition

• debt financing is inexpensive and available

• collision repair management teams realize the benefit of strategically partnering with investors to more quickly grow and develop market share

• $32 billion addressable collision repair industry size

• high barriers to new entrants associated with the MSO consolidator model

• business complexity

• mature management teams

• performance-based insurance DRP contract requirements

• brand recognition

• demonstrated economies of scale

• rising operational excellence with lean-based process environment

• replicable acquisition and integration models

• leveraging and expanding technology enablers

• insurance industry strategy aligned with MSO consolidator strategy

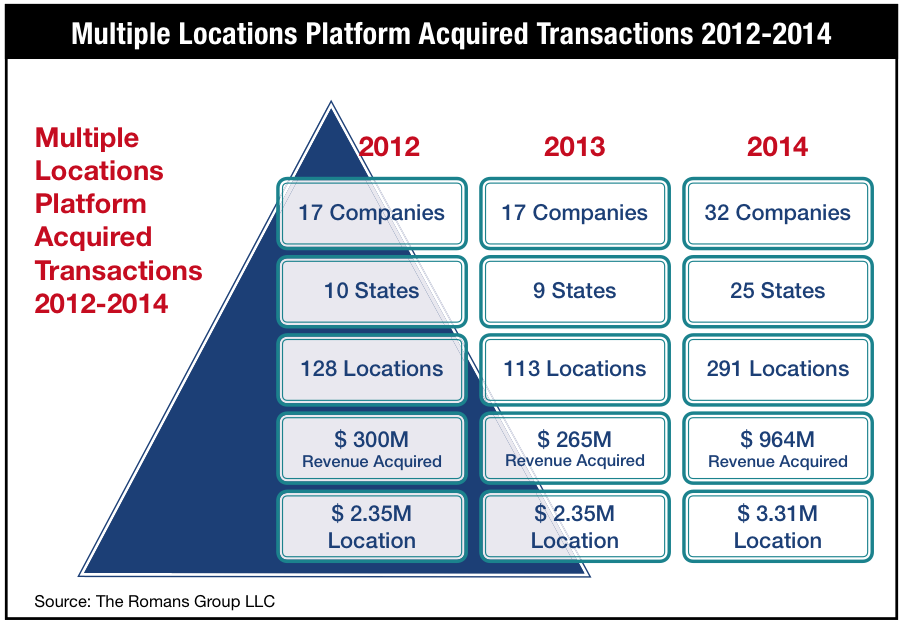

As consolidation continues to drive collision repair industry contraction, four MSO consolidators, ABRA, Boyd/ Gerber, Caliber and Service King stand out as the primary buyers or disruptors vying for multi-location and multi-region platform acquisitions. More nascent strategies are focused on market density and coverage through “build outs or tuck-ins,” acquisition of individual shops, constructing "green fields" and "brown fields" and utilizing franchise models in smaller tier markets.

The growth of MSO consolidators associated with these transactions has in all cases had private equity backing. When viewed in the context of an approximate $32 billion auto repair marketplace, there is room for further consolidation in what is still an oversupply of repairers within the approximately 33,000 U.S. auto repair locations.

The transfer of just more than $1.5 billion in multiple-location operator (MLO) platform transaction repair revenue from 2012-2014 excludes three large recapitalizations that included Caliber in 2013 and ABRA and Service King in 2014. If these recapitalizations were included, the total transfer of MSO consolidator revenue would have been slightly more than $3 billion, or approximately 10% of the industry’s annual revenue. Additionally, the MSO segment representing at least $20 million in annual revenue included 80 MSO organizations processing $6.3 billion in annual revenue at year-end 2014. How long private equity continues its aggressive funding of MSO consolidators is uncertain.

As consolidation continues to drive collision repair industry contraction, four MSO consolidators, ABRA, Boyd/ Gerber, Caliber and Service King stand out as the primary buyers or disruptors vying for multi-location and multi-region platform acquisitions. More nascent strategies are focused on market density and coverage through “build outs or tuck-ins,” acquisition of individual shops, constructing "green fields" and "brown fields" and utilizing franchise models in smaller tier markets.

The growth of MSO consolidators associated with these transactions has in all cases had private equity backing. When viewed in the context of an approximate $32 billion auto repair marketplace, there is room for further consolidation in what is still an oversupply of repairers within the approximately 33,000 U.S. auto repair locations.

The transfer of just more than $1.5 billion in multiple-location operator (MLO) platform transaction repair revenue from 2012-2014 excludes three large recapitalizations that included Caliber in 2013 and ABRA and Service King in 2014. If these recapitalizations were included, the total transfer of MSO consolidator revenue would have been slightly more than $3 billion, or approximately 10% of the industry’s annual revenue. Additionally, the MSO segment representing at least $20 million in annual revenue included 80 MSO organizations processing $6.3 billion in annual revenue at year-end 2014. How long private equity continues its aggressive funding of MSO consolidators is uncertain.

As consolidation continues to drive collision repair industry contraction, four MSO consolidators, ABRA, Boyd/ Gerber, Caliber and Service King stand out as the primary buyers or disruptors vying for multi-location and multi-region platform acquisitions. More nascent strategies are focused on market density and coverage through “build outs or tuck-ins,” acquisition of individual shops, constructing "green fields" and "brown fields" and utilizing franchise models in smaller tier markets.

The growth of MSO consolidators associated with these transactions has in all cases had private equity backing. When viewed in the context of an approximate $32 billion auto repair marketplace, there is room for further consolidation in what is still an oversupply of repairers within the approximately 33,000 U.S. auto repair locations.

The transfer of just more than $1.5 billion in multiple-location operator (MLO) platform transaction repair revenue from 2012-2014 excludes three large recapitalizations that included Caliber in 2013 and ABRA and Service King in 2014. If these recapitalizations were included, the total transfer of MSO consolidator revenue would have been slightly more than $3 billion, or approximately 10% of the industry’s annual revenue. Additionally, the MSO segment representing at least $20 million in annual revenue included 80 MSO organizations processing $6.3 billion in annual revenue at year-end 2014. How long private equity continues its aggressive funding of MSO consolidators is uncertain.

Supply chain consolidation in the auto insurance ecosystem

Beyond the collision repair segment, an unprecedented and powerful number of forces are converging to drive mergers and acquisitions activity in the North American property and casualty insurance claims and technology “ecosystem” to historically high levels, including:

• claims supply chain rationalization and consolidation

• rising adoption and deployment of big data and analytics solutions

• insurance product commoditization and the resulting business transformation

• an influx of private equity capital (already raised and seeking to be deployed in the sector)

• expectations of a continuation of a steadily improving economy with the prospect of lingering low interest rates

We expect these forces to amplify competition among well-capitalized strategic players and private equity participants who seek to create scalable and defensible positions in the industry. The implications for smaller, less capitalized, regional or technology- challenged competitors are meaningful.

Claims supply chain consolidation

The area in which we expect the greatest potential for increased activity in 2015 and beyond is within the claims supply chain. The property and casualty insurance claims ecosystem is composed of thousands of small local and independent firms as well as larger regional, national, and global vendors and business partners that provide mission-critical products and services to the claims operations of the property and casualty insurance industry, including:

• insurance technology and IT services, system integrators, core system and claims management software solutions and database and information providers, including communication, repair estimating and body shop management systems

• claims technology vendors (document management, compliance, data quality, payment systems, etc.)

• collision and auto glass repairers

• collision repair parts suppliers

• insurance replacement rental car providers

• third-party administrators and claims business process outsourcing firms

• claim services, including independent auto and property adjusters and appraisers and catastrophe services

• insurance defense attorneys

• auto and casualty claims management solution providers

• salvage vehicle auctioneers and towing services

• insurance staffing firms

• insurance claims investigation firms

One of the subsectors most affected by these factors is the highly fragmented and inefficient collision repair and parts business. Many of these are local, privately owned businesses with limited technology capabilities and management talent. National consolidation, often driven by private equity, can lead to expense rationalization, upgraded information technology systems, improved management and the ability to better respond to upstream customer pressure and improved pricing. By way of example, since its founding in 1998, LKQ (NASDAQ: LKQ) has consolidated the automotive repair alternative parts market in North America and elsewhere to become the largest provider of alternative collision replacement parts and a leading provider of recycled engines and transmissions, with annual revenue approaching $7 billion. In 2014, LKQ acquired Keystone Automotive, a leading distributor of aftermarket parts and equipment.

One of the subsectors most affected by these factors is the highly fragmented and inefficient collision repair and parts business. Many of these are local, privately owned businesses with limited technology capabilities and management talent. National consolidation, often driven by private equity, can lead to expense rationalization, upgraded information technology systems, improved management and the ability to better respond to upstream customer pressure and improved pricing. By way of example, since its founding in 1998, LKQ (NASDAQ: LKQ) has consolidated the automotive repair alternative parts market in North America and elsewhere to become the largest provider of alternative collision replacement parts and a leading provider of recycled engines and transmissions, with annual revenue approaching $7 billion. In 2014, LKQ acquired Keystone Automotive, a leading distributor of aftermarket parts and equipment.

One of the subsectors most affected by these factors is the highly fragmented and inefficient collision repair and parts business. Many of these are local, privately owned businesses with limited technology capabilities and management talent. National consolidation, often driven by private equity, can lead to expense rationalization, upgraded information technology systems, improved management and the ability to better respond to upstream customer pressure and improved pricing. By way of example, since its founding in 1998, LKQ (NASDAQ: LKQ) has consolidated the automotive repair alternative parts market in North America and elsewhere to become the largest provider of alternative collision replacement parts and a leading provider of recycled engines and transmissions, with annual revenue approaching $7 billion. In 2014, LKQ acquired Keystone Automotive, a leading distributor of aftermarket parts and equipment.

Additionally, one of the other important trends is the development of an electronic parts procurement and e-commerce solution for the large $15 billion, and still highly fragmented and inefficient, North American auto repair parts supply chain.

For smaller providers in the claims supply chain, now may be the time to consider combining with a larger, better-capitalized player, especially given the trend toward vendor management by insurance companies. A “going it alone” strategy will be increasingly risky as larger, national players will garner more market share by offering better pricing, superior technology solutions and greater geographic coverage than “mom and pop” operations.

Claims information provider expansion and consolidation

North American insurance industry auto and property claims operations, including their auto collision repair and property partners, primarily use the products and services of three claims information providers, each of which has expanded its offerings into automotive claims-related markets.

CCC Information Services: Private equity-backed CCC Information Services (Leonard Green & Partners plus TPG Capital), a database, software, analytics and solutions provider to the auto insurance claims and collision repair markets, recently acquired Auto Injury Solutions, a provider of auto injury medical review solutions. This follows the earlier acquisition of Injury Sciences, which provides insurance carriers with scientifically based analytic tools to help identify fraudulent and exaggerated injury claims associated with automobile accidents. In December 2014, CCC acquired the assets of Actual Systems of America, including its interest in Pinnacle Software, an automotive recycler and yard management system provider, which will enhance its fast-growing TRUE Parts alternative collision repair parts procurement platform. In May 2015, the company further extended its insurance claims solution capabilities by acquiring telematics driving data and analytics provider DriveFactor.

Mitchell International: In 2014, Mitchell International, a provider of technology, connectivity and information solutions to the property and casualty claims and collision repair industries, acquired pharmacy claims management software vendor Cogent Works as well as Fairpay Solutions. Fairpay’s service offering includes workers’ compensation, liability and auto cost containment and payment integrity services. These assets will expand Mitchell’s solution suite of property and casualty insurance-focused bill review and out-of-network negotiation services as it complements its 2012 acquisition of National Health Quest. Mitchell was acquired in 2013 by KKR & Co. (NYSE:KKR).

Solera, Inc.: The breathtaking series of recent U.S. and foreign automotive service industry and data acquisitions in 2014 by Solera (NYSE:SLH) includes the Czech and Slovakian vehicle valuation provider IBS Automotive, the UK vehicle valuation firm CAP Automotive, the insurance and services division of PGW (including LYNX, GTS and Glaxis), the claims-related business of UK-based Sherwood Group (Valexa Technolgies), AutoPoint (U.S.) and AutoSoft (Italy). HyperQuest (U.S.) was acquired in 2013 along with Distribution Services Technologies and Services Repair Solutions (U.S.), Serinfo (Chile), Pusula Otomotiv (Turkey), Ezi- Works/CarQuote (Australia) and APU Solutions in 2012. Since its initial public offering in 2007 (originally backed by private equity firm GTCR), Solera has completed 30 acquisitions globally and grown its revenue to more than $1 billion.

Over the next 12 months, we expect these information providers to expand in several directions through internal product development supplemented by strategic acquisitions. This expansion will likely include:

• deeper integration with claims management core systems

• introduction of new tools and services utilizing advanced analytics for use cases across the entire auto and property claims process

• deeper and wider integration with third-party companies in the auto and property claims supply chain, specifically including collision repair parts procurement

• further development of auto casualty and workers’ compensation medical management networks and services and cost containment solutions.

Predictions for 2015 and beyond

• The macro influencers of contraction, consolidation and convergence, combined with the intensity and high velocity of change among the confluence of simultaneous events, will continue to overlay and affect the structural change and the continuing constructive transformation currently happening within the entire automotive ecosystem.

• Property and casualty insurance carriers will develop new forms of highly customized and contextual insurance coverage tied to policyholders’ real-time needs.

• Property and casualty insurance carriers will sell micro-insurance and risk management services to customers based on digital connections to their bodies, automobiles, homes and other personal property; collectively composing the Internet of Things,

• Insurance carrier supply chain partners will increasingly assume claims servicing and resolution responsibilities and may well assume some or all of the associated risks in exchange for guaranteed transaction volume.

• Direct repair assignments through customer choice among the top 10 property and casualty auto insurers continue to grow, and many now have an assignment conversion rate of more than 50% to their DRP providers

• Analytics will evolve to change every aspect of insurance, including marketing, distribution, underwriting, pricing, claims and billing

• The pace and scope of supply chain consolidation within the auto insurance ecosystem will accelerate sharply in 2015 as existing players move to protect and grow their market shares. New, well-capitalized and more consumer-savvy players will enter the market with an array of powerful digital assets. Investors will continue to gravitate to the space, betting on attractive short-term upsides and adding fuel to the fire.

• MSO consolidators will continue to execute on their platform acquisition growth and development strategies. They will supplement their multi-regional and national growth with a combination of single repair center acquisitions, Brown field and green field build outs and franchise expansion to improve coverage and density in existing major and smaller markets.

• The traditional insurer-repairer business model, which is focused on an estimate exchange process, is likely to be transformed within three years and supplanted by a process driven by mobile technologies coupled with predictive analytics. This will reduce and eventually eliminate the need for repairer-carrier estimate exchanges for an increasingly higher percentage of claims.

Conclusions

• The ultimate leaders and winners in 2015 and beyond will be those companies that most successfully focus and execute upon the new realities identified in this report. They will also leverage a strategic alliance ecosystem in which they team up for success. They will accomplish this with customers, suppliers, competitors, investors and business partners as part of a collaborative brain trust where all are committed to co-create and change their organizations and their uncertain environments to their individual and mutual benefit.

• In this dynamic environment, we believe that the ultimate leaders and winners in 2015 and beyond will be those companies that most successfully focus and execute on the development of compelling personal mobility solutions and transform product development and distribution around the new consumer. They will leverage data and analytics across the enterprise, think, plan and execute globally and aggressively collaborate, partner and affiliate as effectively as possible.

• The auto parts supply chain, one of the most fragmented of all segments in the ecosystem, and until now characterized by numerous competing parts search and procurement platforms, will finally begin to consolidate in the hands of just a few well-capitalized, highly experienced and strategically positioned information and software providers.

• The ability to successfully acquire, control and effectively translate and leverage all of these new streams of data into actionable information and insights will determine the insurance industry’s digital gold rush winners and losers of the future.

• The area in which we expect the greatest potential for increased disruption in 2015 and beyond is within the claims supply chain.

• For smaller providers in the claims supply chain, now may be the time to consider combining with a larger, better-capitalized player, especially given the trend toward vendor management by insurance companies. A “going it alone” strategy will be increasingly risky as larger, national players will garner more market share by offering better pricing, superior technology solutions and greater geographic coverage than “mom and pop” operations.

• Many of the trends associated with the beginning of a slow, long-term, downward slope of future accident frequency such as the proliferation of accident avoidance technology, urbanization, car sharing, Uber, connected vehicles and telematics are already cooked into the expanding equation and future auto insurance and repair model reflecting reduced auto accidents and fewer repairable vehicles with new and hybrid insurance coverage offered by fewer surviving insurers.

This was originally published in the U.S. in ABRN in the July 2015 edition and in Canada in Collision Repair Magazine in the August 2015 edition.