Recently, Munich Re announced its plan to step into the U.S. inland flood market to offer a competitive flood coverage endorsement for participating carriers. This is the second notable entry of international capital into an arena dominated by the federal government.

Munich Re is known as a conservative giant of international reinsurance, so it might seem odd that it is joining the National Flood Insurance Program (NFIP) in covering U.S. flood. A quick look at the opportunity shows why the plan makes sense.

U.S. inland flood insurance is an untapped source of non-correlated premium unlike any other in the world. The market is dominated by an incumbent market maker that is in trouble because it offers an inferior product that cannot price risk correctly (this paper nicely summarizes the problems at NFIP). So, here is what the new entrants are seeing:

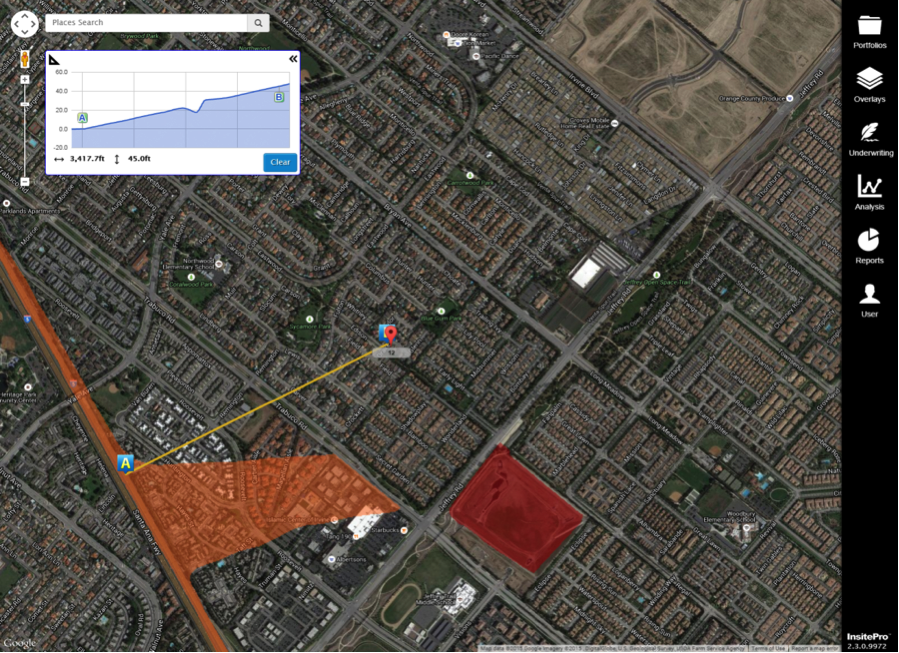

Screenshot of InsitePro, courtesy of Intermap Technologies. FEMA zones in red and orange

Screenshot of InsitePro, courtesy of Intermap Technologies. FEMA zones in red and orange

- Contrary to industry beliefs, flood is insurable. The tools are present to accurately segment risk.

- Carriers offering flood capacity will differentiate themselves from competitors. This will give them a leg up on the competition in a market that is highly homogeneous. Carriers not offering flood will likely disappear.

- The market is massive, with potentially 130 million homes and tens of billions of dollars at stake.

- The property is in Orange County, CA, where the climate is temperate and dry, almost borderline desert. El Niño might be coming, but that risk can be built in.

- Using InsitePro (see image below), you can see that the property is miles and miles away from any coastal areas, rivers or streams. More importantly, the home is elevated against its surroundings, so water flows away from the property, which is deemed low-risk.

- The area has no history of flooding, and this particular community has one of the most modern drainage systems in the state.

Screenshot of InsitePro, courtesy of Intermap Technologies. FEMA zones in red and orange

- Using Google Maps street view, we can estimate that the property is two to three feet above street level, which adds another layer of safety. Also, this view confirms that the area is essentially flat, so the property is not at the bottom of a bathtub.

- And, as with most homes in California, this property has no basement, so if water were to get into the house it would need to keep rising to cause further damage.