We have previously evaluated and discussed the financial performance and operating results of the insurtech trio Lemonade, Root and Metromile. Based on the analysis of the last available data, we think that:

Note: The expenses ratios are not significant because part of the expenses are paid by the parent companies and not reported on the Yellow Books.

There is a pricing war

We believe the insurtech trio is facing a pricing war. We find three data points in support of this view:

Note: The expenses ratios are not significant because part of the expenses are paid by the parent companies and not reported on the Yellow Books.

There is a pricing war

We believe the insurtech trio is facing a pricing war. We find three data points in support of this view:

Having looked at the top line, let’s switch our attention to the loss ratios. For an insurance carrier, the loss ratio is really the litmus test that assesses the strength and quality of the top-line numbers. Loss ratio is a fundamental insurance number, and the fact that all three players have improved this crucial metric is a sign of increased maturity for the “not so” fast-growing trio.

All three improved compared with the prior quarter. This bodes well for the trio. Of the three, Root continues to have the highest loss ratio at 91%, suggesting that between new sales and renewal it is still under-pricing risks.

See also: An Insurance Policy With Some ‘Magic’

The Q2-19 loss ratios are significantly better than what the three firms exhibited in Q2 of 2018, when Lemonade had a loss ratio of 120%, Metromile was at 95% and Root at 112%. The loss ratios are still far higher than the respective market segments.

Having looked at the top line, let’s switch our attention to the loss ratios. For an insurance carrier, the loss ratio is really the litmus test that assesses the strength and quality of the top-line numbers. Loss ratio is a fundamental insurance number, and the fact that all three players have improved this crucial metric is a sign of increased maturity for the “not so” fast-growing trio.

All three improved compared with the prior quarter. This bodes well for the trio. Of the three, Root continues to have the highest loss ratio at 91%, suggesting that between new sales and renewal it is still under-pricing risks.

See also: An Insurance Policy With Some ‘Magic’

The Q2-19 loss ratios are significantly better than what the three firms exhibited in Q2 of 2018, when Lemonade had a loss ratio of 120%, Metromile was at 95% and Root at 112%. The loss ratios are still far higher than the respective market segments.

Missing an edge and story with respect to gaining a sustainable competitive advantage

In our last article talking about insurtech direct-to-consumer (DTC) as a “price game,” we highlighted how the companies have not been able to make customers fall in love with anything other than “saving money.”

We would like to share some thoughts on the business models of these three full-stack carriers, investigating where and how their approaches might both enable and impede them in terms of gaining a sustainable competitive advantage. What might be the proverbial sling that the “insurtech Davids” can use against the entrenched Goliaths of State Farm, Geico, Progressive, Allstate, et al? Let’s explore.

If we consider the economics of an insurer, there are three areas where you can obtain a competitive advantage that can allow financing this kind of “pricing war”:

Missing an edge and story with respect to gaining a sustainable competitive advantage

In our last article talking about insurtech direct-to-consumer (DTC) as a “price game,” we highlighted how the companies have not been able to make customers fall in love with anything other than “saving money.”

We would like to share some thoughts on the business models of these three full-stack carriers, investigating where and how their approaches might both enable and impede them in terms of gaining a sustainable competitive advantage. What might be the proverbial sling that the “insurtech Davids” can use against the entrenched Goliaths of State Farm, Geico, Progressive, Allstate, et al? Let’s explore.

If we consider the economics of an insurer, there are three areas where you can obtain a competitive advantage that can allow financing this kind of “pricing war”:

Probably, hidden in the parent companies income statements, there is some additional investment income obtained investing the cash received by their investors.

However - as of today - the return obtained investing the floating is clearly a competitive disadvantage for the insurtech players.

Loss ratio

As explained in a previous article, the loss ratio is the key measure of the technical profitability of an insurance business . The U.S. P&C market showed $366 billion net losses incurred, which means almost 61% loss ratio (net of loss adjustment expenses). Can any insurtech element allow Metromile, Root or Lemonade to have a competitive advantage on the loss ratio?

Metromile and Root are telematics-based auto insurers. Matteo is a fan of the usage of telematics data on the auto business and an evangelist of these approaches through his IoT Insurance Observatory, an international think tank that has aggregated almost 60 Insurers, reinsurers and tech players between North America and Europe.

Based on the Observatory research, four value creation levers have been the most relevant in telematics success stories:

Probably, hidden in the parent companies income statements, there is some additional investment income obtained investing the cash received by their investors.

However - as of today - the return obtained investing the floating is clearly a competitive disadvantage for the insurtech players.

Loss ratio

As explained in a previous article, the loss ratio is the key measure of the technical profitability of an insurance business . The U.S. P&C market showed $366 billion net losses incurred, which means almost 61% loss ratio (net of loss adjustment expenses). Can any insurtech element allow Metromile, Root or Lemonade to have a competitive advantage on the loss ratio?

Metromile and Root are telematics-based auto insurers. Matteo is a fan of the usage of telematics data on the auto business and an evangelist of these approaches through his IoT Insurance Observatory, an international think tank that has aggregated almost 60 Insurers, reinsurers and tech players between North America and Europe.

Based on the Observatory research, four value creation levers have been the most relevant in telematics success stories:

- There is a pricing war

- The trio is missing an edge and story with respect to gaining a sustainable competitive advantage

Note: The expenses ratios are not significant because part of the expenses are paid by the parent companies and not reported on the Yellow Books.

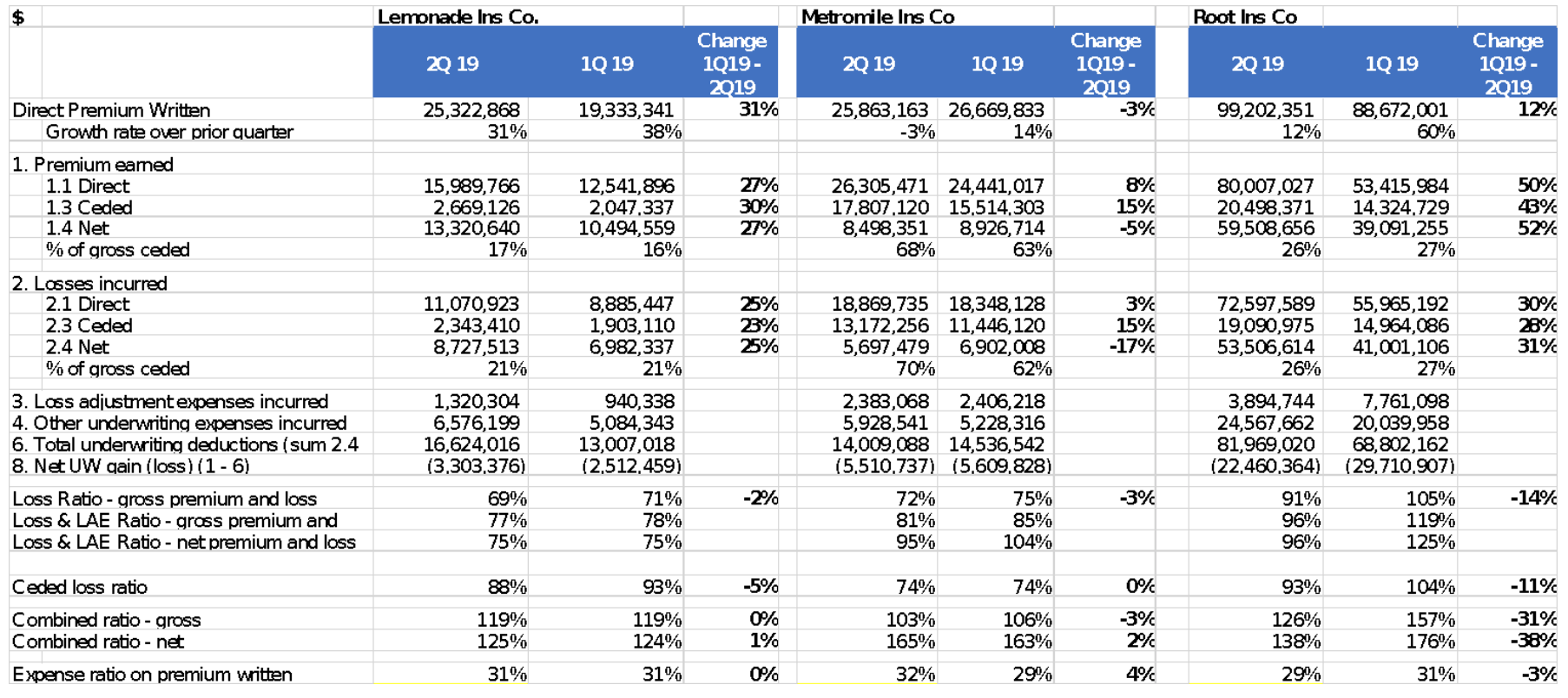

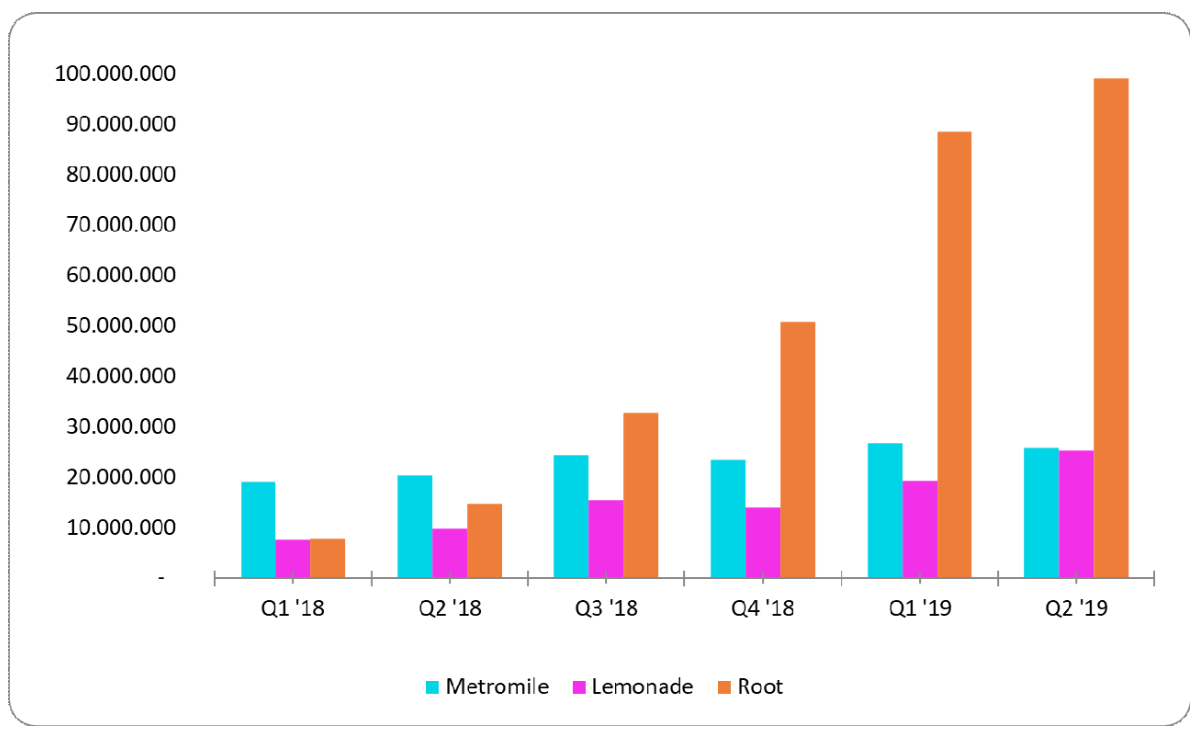

There is a pricing war

We believe the insurtech trio is facing a pricing war. We find three data points in support of this view:

- Viewed through the lens of growth rate, after a robust Q1-19 for all three players, Q2-19 presents a different story. We find the most interesting perspective by looking at the performance over the last year and half. Clearly, the premium evolution of Metromile is the less exciting story, as I previously wrote. The pay per mile doesn’t seem particularly effective in attracting customers. The “pay per mile” model introduces an element of uncertainty for segments of customers who want to save money and know what insurance coverage will cost them. The only comfortable customers are those who almost never use a car. (We will cover the customer experience and expectations for usage-based insurance in future articles.)

- Lemonade has shown consistent growth in the last two quarters and appears to be on target to meet the $100 million annual revenue target. This revenue target is a far cry from the “massive disruption effect” that was expected during its debut. The revenue curve is not yet showing the vaunted hockey stick.

- Root is the only of these three players with exponential growth in revenue. However, something happened in the second quarter, and growth slowed significantly as the loss ratio improved. As mentioned in our last article, insurtech D2C seems to be a “price game.”

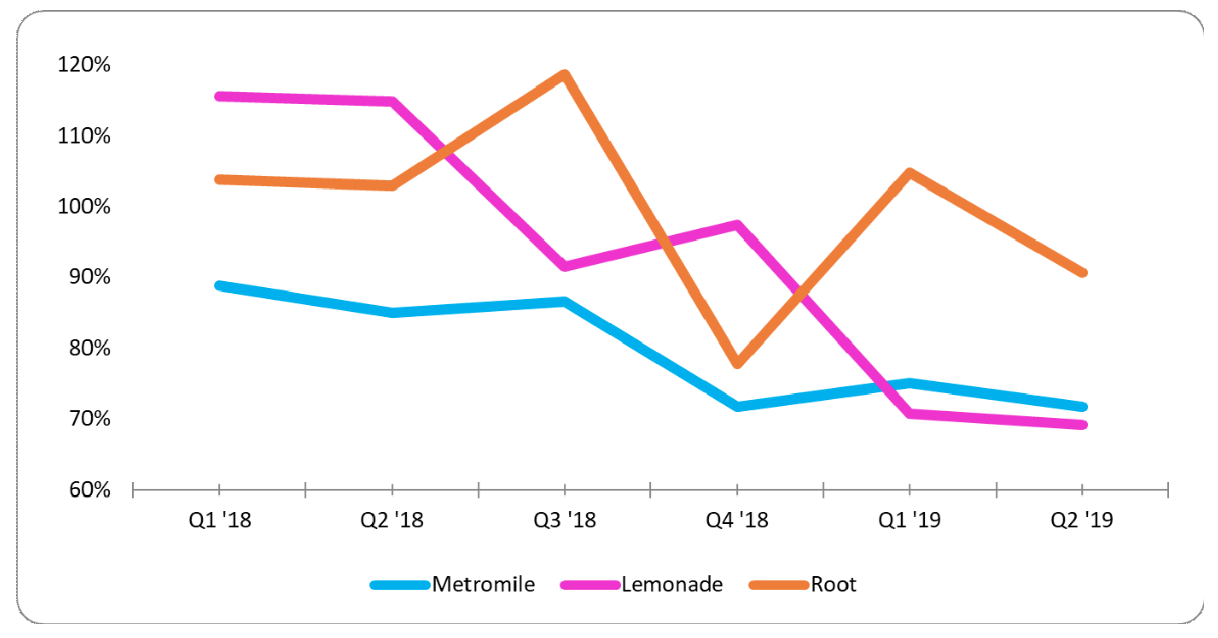

Having looked at the top line, let’s switch our attention to the loss ratios. For an insurance carrier, the loss ratio is really the litmus test that assesses the strength and quality of the top-line numbers. Loss ratio is a fundamental insurance number, and the fact that all three players have improved this crucial metric is a sign of increased maturity for the “not so” fast-growing trio.

All three improved compared with the prior quarter. This bodes well for the trio. Of the three, Root continues to have the highest loss ratio at 91%, suggesting that between new sales and renewal it is still under-pricing risks.

See also: An Insurance Policy With Some ‘Magic’

The Q2-19 loss ratios are significantly better than what the three firms exhibited in Q2 of 2018, when Lemonade had a loss ratio of 120%, Metromile was at 95% and Root at 112%. The loss ratios are still far higher than the respective market segments.

Missing an edge and story with respect to gaining a sustainable competitive advantage

In our last article talking about insurtech direct-to-consumer (DTC) as a “price game,” we highlighted how the companies have not been able to make customers fall in love with anything other than “saving money.”

We would like to share some thoughts on the business models of these three full-stack carriers, investigating where and how their approaches might both enable and impede them in terms of gaining a sustainable competitive advantage. What might be the proverbial sling that the “insurtech Davids” can use against the entrenched Goliaths of State Farm, Geico, Progressive, Allstate, et al? Let’s explore.

If we consider the economics of an insurer, there are three areas where you can obtain a competitive advantage that can allow financing this kind of “pricing war”:

- Investment income

- The loss ratio

- The administrative expenses

Probably, hidden in the parent companies income statements, there is some additional investment income obtained investing the cash received by their investors.

However - as of today - the return obtained investing the floating is clearly a competitive disadvantage for the insurtech players.

Loss ratio

As explained in a previous article, the loss ratio is the key measure of the technical profitability of an insurance business . The U.S. P&C market showed $366 billion net losses incurred, which means almost 61% loss ratio (net of loss adjustment expenses). Can any insurtech element allow Metromile, Root or Lemonade to have a competitive advantage on the loss ratio?

Metromile and Root are telematics-based auto insurers. Matteo is a fan of the usage of telematics data on the auto business and an evangelist of these approaches through his IoT Insurance Observatory, an international think tank that has aggregated almost 60 Insurers, reinsurers and tech players between North America and Europe.

Based on the Observatory research, four value creation levers have been the most relevant in telematics success stories:

- The telematics approach has demonstrated around the world a consistent ability to self-select risks. Simply said, bad drivers don’t want to be monitored;

- Some players such as UnipolSai and Groupama have achieved material results by improving claims management through telematics data;

- Some other players have been able to change drivers’ behaviors, e.g., the South African Discovery and the American Allstate;

- Many players have been able to charge fees to customers for telematics-based services, providing a revenue stream.