The 2025 Canadian Reinsurance Conference featured a panel discussion with representatives from an insurer (Manulife), a reinsurer (RGA), and a leading industry organization (LIMRA/LOMA) on the topic of bridging the life insurance coverage gap in Canada. This article summarizes that discussion – outlining the current situation, describing factors, and offering potential solutions.

The positive side of emerging challenges is they generally bring opportunities. That certainly holds true for today's Canadian life insurance industry.

The challenge: Canada is facing a significant life insurance coverage gap, with insurance ownership declining across the nation.

The opportunity: By identifying underlying issues, developing and prioritizing strategies to address them, and working together across all parts of the insurance value chain, the industry can build a more secure future for all Canadians.

A growing gap

First, a quick look at the numbers.

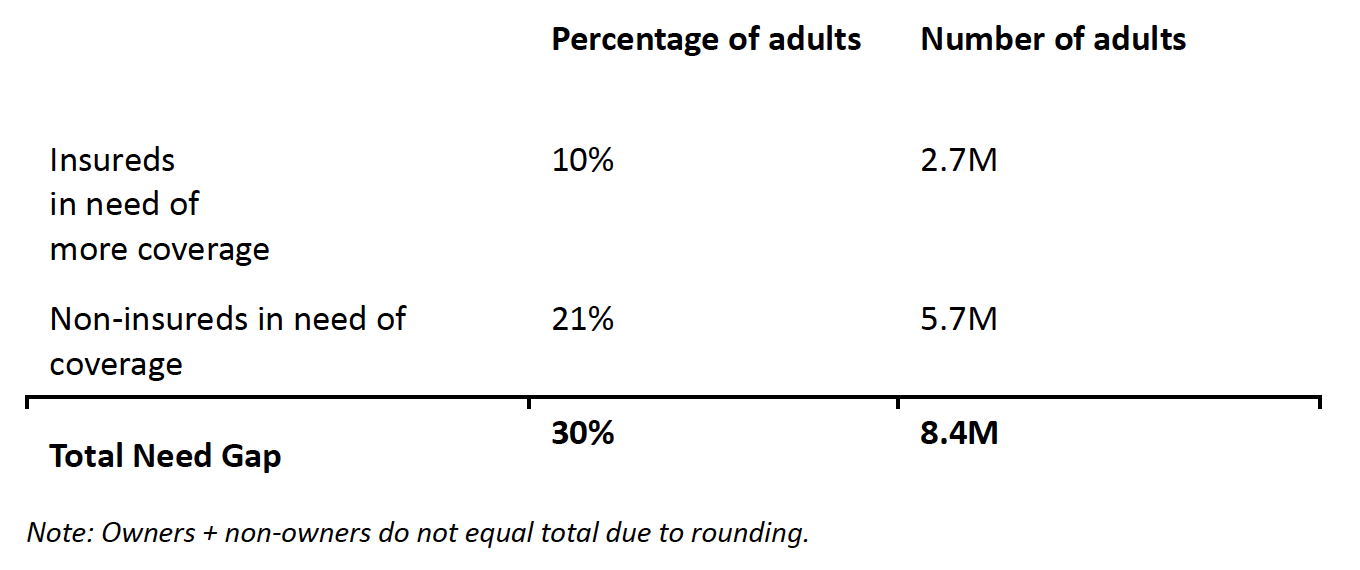

Figure 1: Life insurance gap in Canada

The gap spans all income levels but is most pronounced in households earning below $50,000 annually. Accordingly, the decline in insurance coverage is particularly evident in term policies, which dropped from 397,000 in 2019 to 340,000 in 2024. Meanwhile, 56% of 2024 premium sales were participating (whole life) policies, indicating a shift toward higher-end products. The result: While the current market generates relatively positive financial results, underlying declines in policy ownership suggest significant growth opportunities have yet to be realized

Underinsured rates are especially prevalent among younger generations, with Gen Z showing a 44% need gap, more than double that of Baby Boomers. Gender analysis reveals clear, though less prominent, disparities, with women having a 32% insurance need gap compared to 28% for men.

As insurance ownership drops, the need for financial protection only grows. Increasing housing costs and associated mortgage debt, for example, amplify the protective benefits of insurance coverage, especially for younger people taking on new loans. On the other end of the age spectrum, Canadian seniors already at risk of outliving their own retirement savings also risk leaving loved ones unprotected.

Consider this: The crowdsourced fundraising site GoFundMe, a popular source of support for individuals in need, recorded its highest annual payout total in 2024, reflecting the critical need for financial protection despite declining insurance ownership.

Contributing factors

Several connected factors contribute to the growing coverage gap.

Within the industry itself, a shift in focus toward high net worth clients has led to an emphasis on larger and more sophisticated policies. This trend, coupled with a decline in the number of insurance advisors, has resulted in reduced attention to the mass market and term policies. A lack of young advisors is particularly troubling as many industry veterans near retirement age.

Changing demographics and consumer attitudes also play a crucial role. Immigration, including an estimated 395,000 people coming to Canada in 2025, has increased the number of households who may need insurance coverage.

Post-pandemic shifts in consumer priorities and financial strains have further exacerbated the issue, with higher cost of living fueling competing priorities for after-tax dollars and making insurance seem less urgent. Younger generations are delaying life events – home ownership, marriage, children – that typically trigger insurance purchases. In addition, fallout from the pandemic-triggered "Great Resignation" and accompanying expansion of the gig economy, which saw a 44% surge in the number of digital gig workers in Canada in 2024, has left many without employer-sponsored plans.

Misperceptions about insurance remain prevalent. Only 32% of Canadians trust their insurer, according to Statistica Canada. Additionally, a general lack of awareness about life insurance benefits and costs reduces perceived value. Complex product offerings and jargon-filled communication can magnify this issue and create added barriers to insurance adoption.

Five keys to future growth

Addressing the life insurance coverage gap in Canada requires a multi-faceted approach.

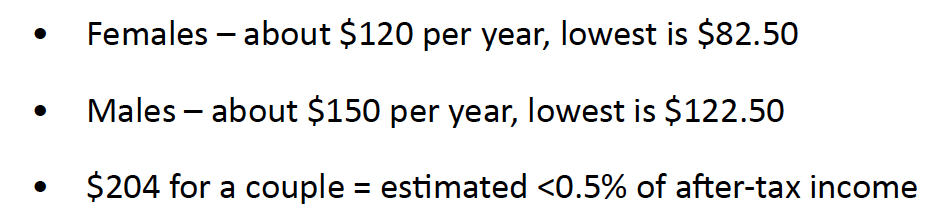

1. Education and awareness. This tactic should be at the forefront, with efforts to simplify insurance language, highlight affordable premiums (see Figure 2), and emphasize the universal benefits of life insurance – such as income replacement, debt protection, and legacy planning.

Figure 2: How much does life insurance really cost?

In a recent study, Canadians overestimate the cost of insurance by more than 300%. Actual premiums for $250,000 of life insurance coverage for 30-year-old nonsmokers in Canada (represents 5X income coverage for someone making $50,000 – a commonly recommended ratio):

2. Digital engagement. Expanding marketing efforts to platforms like TikTok, Instagram, and YouTube; developing user-friendly interfaces for needs analysis and applications; and implementing hybrid advice channels that combine online tools with advisor support can make insurance more accessible and appealing, especially for younger people. In LIMRA's Insurance Barometer Study, 46% of respondents indicated, "I would research life insurance online, but ultimately buy in person." Companies embedding immediate contact support with online tools are having success, and accelerated underwriting processes can remove additional barriers to entry.

3. Targeted strategies. Innovation in products and services tailored to changing life stages and demographics can make insurance more relevant and attractive to a broader range of Canadians. This includes developing "bite-sized" entry-level products for underserved markets, such as new Canadians and gig economy workers.

4. Advisor recruitment. The industry must focus on advisor recruitment and training, particularly from underserved communities. Promoting insurance advisor as a viable career path and conducting outreach through job fairs and community events can help address the shortage of advisors serving the mass market.

5. Industry collaboration. Partnerships with financial planners to include insurance in overall financial literacy efforts, collaborations with "finfluencers" in investment and banking sectors, and industry-wide initiatives to improve accessibility and trust, can create a more robust and inclusive insurance ecosystem.

A call to action

The opportunities are there – but only if we take collective action as an industry to seize them.

As the insurance landscape evolves, we must ensure we are meeting the needs of all customers. And the time to act is now. For example, protection for a mortgage is a common reason people acquire term insurance, and more than 1.2 million mortgages are renewing in 2025. This significant opportunity is just one of many.

Despite the urgent need for sufficient coverage and the continued advances in direct digital sales, insurance remains primarily a sold-not-bought product. Awareness of need without advice does not result in action; awareness with advice does result in action. To serve a broader population, the industry must reimagine distribution models and design innovative products that bridge the gap between awareness and action.

By diversifying the customer base and making financial protection accessible to all Canadians, the industry can fulfill its social responsibility while enhancing its resilience. Together, we can bridge the gap and create a more financially secure Canada for generations to come.