Over the past few weeks, I had the pleasure of meeting with a number of insurtech startups. Their mission? To create a customer-first company. One team is finding that customers believe insurance has more of a transparency challenge than a trust deficit – there is an increasing desire to know how their premium dollars are spent and how an insurance company views their risk.

Many of these meetings were held shortly after Evan Greenberg, CEO of Chubb, commented on broker commissions and fees in the commercial insurance market. Whether you agree with Greenberg’s comments, what really attracted customers’ attention is the lack of fee and commission transparency within the commercial insurance market. Furthermore, many insurtech articles stress that, for a long time, brokers have been able to capitalize on the industry’s lack of access and transparency. These articles rarely highlight existing customer rights, nor do they articulate how commissions and fees have evolved in the commercial insurance industry.

See also: More Transparency Needed on Premiums

Regulations in a number of jurisdictions make clear that insurance buyers are entitled to request the actual level of commission and fees earned by their service provider. For those jurisdictions where customer rights are not as clear, any customer is still within his rights to request this information as he is paying for services and products.

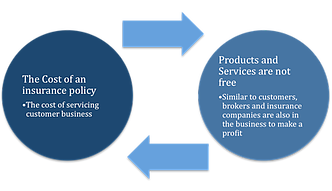

For the past 20 years, brokers have shied away from having a frank dialogue with customers about the true costs of servicing a customer’s insurance program for fear of losing business to competitors. This fear of adequately charging for broker services, combined with decreasing standard policy commissions, led many brokers to consider alternative ways to make up revenue shortfalls. Increased commissions and fees from insurance companies provided the answer via traditional placements or the creation of broker facilities. Simultaneously, customer service has been redefined over time – many brokers now focus on reducing customer premiums as a way of evidencing value to customers.

This focus is not a true service, nor is it really reducing overall costs as broker commissions and fees are passed on to customers through insurance premiums. These increasing costs hurt an insurance company's balance sheet. Just a quick reminder: A healthy balance sheet is required to pay claims!

Why does a healthy balance sheet matter? Have you ever experienced the insolvency of an insurer or reinsurer? Have you ever informed customers they may only receive five cents on the dollar for existing and future claims? Unfortunately, I had these experiences on a number of occasions during my early career as a claims manager -- and I hope to never have the experience again! Fortunately, insolvencies are now rare events, due in part to the prudential regulatory regimes applicable to insurers, but that does not mean there is a bottomless commercial insurance company treasure chest for ever-increasing commissions and fees.

Can insurtech companies lead the way forward?

Marketing materials stress that insurtech startups are “customer-focused,” and their propositions are characterized by “convenience, on-demand, personalization and transparency.” For some of the startups, the company website and buying process stress that “the business aims to provide transparency.”

Other startups list their fees on the company website and clearly evidence commissions on customer quotes. One insurtech broker has taken additional steps on the company website to 1) define profit commissions and 2) provide a schedule of profit commission schemes currently in place with insurance partners (none listed as of May 3, 2017).

This level of detail provides the customer with highlights of financial arrangements and improves financial transparency in the customer-broker-insurance company relationship.

The future of transparency?

Even though the insurtech industry has been progressing very swiftly, not every major insurtech startup is a roaring success. SME customers can now compare commercial insurance products and services on offer, while improving their knowledge of products and service costs.

See also: Is Transparency the Answer in Healthcare?

Commercial insurance brokers can lead transparency efforts by initiating frank conversations with customers about the true costs of products and customer-specific services and negotiate commissions and fees accordingly. However, as noted in my previous operations and product development articles, brokers, insurers and reinsurers must simultaneously review existing operations to create better efficiencies, reduce costs and improve customer services. These changes can be achieved through cutting-edge transformation programs, investment in new technologies or partnerships with insurtech companies.

Why is a simultaneous review important? Because customers are not only bearing the costs of current broker commissions and fees via premium payments, they are also bearing the high costs of supporting antiquated commercial insurance operations. Let’s improve all levels of service and transparency in the commercial insurance buying cycle and help customers make better informed decisions!

This level of detail provides the customer with highlights of financial arrangements and improves financial transparency in the customer-broker-insurance company relationship.

The future of transparency?

Even though the insurtech industry has been progressing very swiftly, not every major insurtech startup is a roaring success. SME customers can now compare commercial insurance products and services on offer, while improving their knowledge of products and service costs.

See also: Is Transparency the Answer in Healthcare?

Commercial insurance brokers can lead transparency efforts by initiating frank conversations with customers about the true costs of products and customer-specific services and negotiate commissions and fees accordingly. However, as noted in my previous operations and product development articles, brokers, insurers and reinsurers must simultaneously review existing operations to create better efficiencies, reduce costs and improve customer services. These changes can be achieved through cutting-edge transformation programs, investment in new technologies or partnerships with insurtech companies.

Why is a simultaneous review important? Because customers are not only bearing the costs of current broker commissions and fees via premium payments, they are also bearing the high costs of supporting antiquated commercial insurance operations. Let’s improve all levels of service and transparency in the commercial insurance buying cycle and help customers make better informed decisions!

This level of detail provides the customer with highlights of financial arrangements and improves financial transparency in the customer-broker-insurance company relationship.

The future of transparency?

Even though the insurtech industry has been progressing very swiftly, not every major insurtech startup is a roaring success. SME customers can now compare commercial insurance products and services on offer, while improving their knowledge of products and service costs.

See also: Is Transparency the Answer in Healthcare?

Commercial insurance brokers can lead transparency efforts by initiating frank conversations with customers about the true costs of products and customer-specific services and negotiate commissions and fees accordingly. However, as noted in my previous operations and product development articles, brokers, insurers and reinsurers must simultaneously review existing operations to create better efficiencies, reduce costs and improve customer services. These changes can be achieved through cutting-edge transformation programs, investment in new technologies or partnerships with insurtech companies.

Why is a simultaneous review important? Because customers are not only bearing the costs of current broker commissions and fees via premium payments, they are also bearing the high costs of supporting antiquated commercial insurance operations. Let’s improve all levels of service and transparency in the commercial insurance buying cycle and help customers make better informed decisions!