Since the start of the decade, we've encouraged insurers and industry stakeholders to think about "Insurance 2020" as they formulate their strategies and try to turn change into opportunity. Insurance 2020’s central message is that whatever organizations are doing in the short term, they need to be looking at how to keep pace with the sweeping social, technological, environmental, economic and political (STEEP) developments ahead.

Now we’re at the mid-point between 2010 and 2020, and we thought it would be useful to review the developments we’ve seen to date and look ahead to the major trends coming up over the next five years and beyond.

Where are we now?

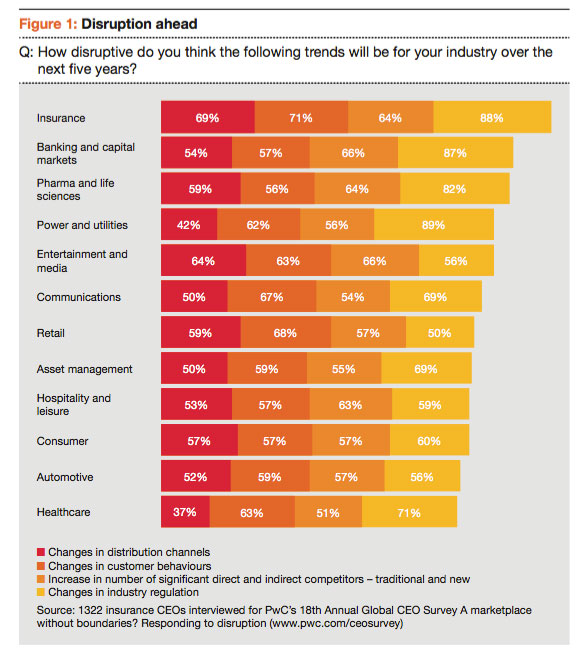

Insurance is an industry at the tipping point as it grapples with the impact of new technology, new distribution models, changing customer behavior and more exacting local, regional and global regulations. For some businesses, these developments are a potential source of disruption. Those taking part in our latest global CEO survey see more disruption ahead than CEOs in any other commercial sector (see Figure 1), underlining the need for strategic re-evaluation and possible re-orientation. Yet for others, change offers competitive advantage. A telling indication of the mixed mood within the industry is that although nearly 60% of insurance CEOs see more opportunities than three years ago, almost the same proportion (61%) see more threats.

The long-term opportunities for insurers in a world where people are living longer and have more wealth to protect are evident. But the opportunities are also bringing fresh competition, both from within the insurance industry and from a raft of new entrants coming in from outside. The entrants include companies from other financial services sectors, technology giants, healthcare companies, venture capital firms and nimble start-ups.

How are insurers feeling the impact of these developments?

Customer revolution

The insurance marketplace is becoming increasingly fragmented, with an aging population at one end of the spectrum and a less loyal and often hard to engage millennial generation at the other. The family structures and ethnic make-up within many markets are also becoming more varied and complex, which has implications for product design, marketing and sales. This splintering customer base and the need to develop relevant and engaging products and solutions present both a challenge and an opportunity for insurers. On the life, annuities and pensions side, insurers could design targeted plans for single parents or shift from living benefits to well-being or quality of life support for younger people. On the property and casualty (P&C) side, insurers could create partnerships with manufacturers and service companies. Insurers could also offer coverage for different lifestyles, offering flexible, pay-as-you-use insurance or providing top-up coverage for people in peer-to-peer insurance plans.

As the nature of the marketplace changes, so do customer expectations. Customers want insurers to offer them the same kind of easy access, show the same understanding of needs and provide the sorts of targeted products that they’ve become accustomed to from online retailers and other highly customer-centric sectors. Digital developments offer part of the answer by enabling insurers to deliver anytime, anywhere convenience, streamline operations and reach untapped segments. Insurers are also using digital developments to enhance customer profiling, develop sales leads, tailor financial solutions to individual needs and, for P&C businesses in particular, improve claims assessment and settlement. Further priorities include the development of a seamless multi-channel experience, which allows customers to engage when and how they want without having to relay the same information with each interaction. Because the margins between customer retention and loss are finer than ever, the challenge for insurers is how to develop the genuinely customer-centric culture, organizational capabilities and decision-making processes needed to keep pace with ever-more-exacting customer expectations.

Digitization

Most insurers have invested in digital distribution, with some now moving beyond direct digital sales to models that embed products and services in people’s lives (e.g., pay-as-you drive insurance).

A parallel development is the proliferation of new sources of information and analytical techniques, which are beginning to reshape customer targeting, risk underwriting and financial advice. Ever greater access to data doesn’t just increase the speed of servicing and lower costs but also opens the way for ever greater precision, customization and adaptation. As sensors and other digital intelligence become a more pervasive element of the "Internet of Things," savvy insurers can – and in some instances have – become trusted partners in areas ranging from health and well-being to home and commercial equipment care. Digital technology could extend the reach of life, annuities and pension coverage into largely untapped areas such as younger and lower-income segments.

Information advantage

Availability of both traditional and big data is exploding, with the resulting insights providing a valuable aid to customer-centricity and associated revenue growth. Yet many insurers are still finding it difficult to turn data into actionable insights. The keys to resolving this are as much about culture and organization as the application of technology. Making the most of the information and insight is also likely to require a move away from lengthy business planning to a faster and more flexible, data-led, iterative approach. Insurers would need to launch, test, obtain feedback and respond in a model similar to that used by many of today’s telecom and technology companies.

A combination of big data analytics, sensor technology and the communicating networks that make up the Internet of Things would allow insurers to anticipate risks and customer demands with far greater precision than ever before. The benefits would include not only keener pricing and sharper customer targeting but a decisive shift in insurers’ value model from reactive claims payer to preventative risk advisers.

The emerging game changer is the advance in analytics, from descriptive (what happened) and diagnostic (why it happened) analysis to predictive (what is likely to happen) and prescriptive (determining and ensuring the right outcome). This shift not only would enable insurers to anticipate what will happen and when, but also to respond actively. This offers great possibilities in areas ranging from more resilient supply chains and the elimination of design faults to stronger conversion rates for life insurers and more effective protection against fire and flood within property coverage.

Two-speed growth

These developments are coming to the fore against the backdrop of enduringly slow economic growth, continued low interest rates and soft P&C premiums within many developed markets. Interest rates will eventually begin to rise, which will cause some level of short-term disruption across the insurance sector, but over time higher interest rates will lead to higher levels of investment income.

On the P&C side, reserve releases have helped to bolster returns in a softening market. But redundant reserves are being depleted, making it harder to sustain reported returns.

The faster growing markets of South America, Asia, Africa and the Middle East (SAAAME) offer considerable long-term potential, though insurance penetration in 2013 was still only 2.7% of GDP in emerging markets and the share of global premiums only 17%. Penetration in their advanced counterparts was 8.3%. Rapid urbanization is set to be a key driver of growth within SAAAME markets, increasing the value of assets in need of protection. Urbanization also makes it harder for those from rural areas to call on the support of their extended families and hence increases take-up of life, annuities and pensions coverage. The corollary is the growing concentration of risk within these mega-metropolises.

Disruption and innovation

Many forward-looking insurers are developing new business models in areas ranging from tie-ups between reinsurance and investment management companies to a new generation of health, wealth and retirement solutions. The pace of change can only accelerate in the coming years as innovations become mainstream in areas ranging from wearables, the Internet of Things and automated driver assistance systems (ADAS) to partnerships with technology providers and crowd-sourced models of risk evaluation and transfer.

At the same time, a combination of digitization and new business models is disrupting the insurance marketplace by opening up new routes to market and new ways of engaging with customers. An increasing amount of standardized insurance will move over to mobile and Internet channels. But agents will still have a crucial role in helping businesses and retail customers to make sense of an ever-more-complex set of risks and to understand the trade-offs in managing them. On the life, annuities and pension side, this might include balancing the financial trade-offs between how much they want to live off now and their desired standard of living when they retire. On the P&C side, it would include designing effective aggregate protection for an increasingly broad and valuable array of assets and possessions.

Companies can bring innovations to market much faster and more easily than in the past. These companies include new entrants that are using advanced profiling techniques to target customers and cost-efficient digital distribution to undercut incumbent competitors. It’s too soon to say how successful these new entrants and start-ups will be, but they will undoubtedly provide further impetus to the changes in customer expectations and how insurers compete.

In the next two articles in this series, we look at how all these coalescing developments are likely to play out as we head toward 2020 and beyond and outline the strategic and operational implications for insurers. While we’ve set a nominal date of 2020, fast-moving businesses are already assessing and addressing these developments now as they look to keep pace with customer expectations and sharpen their competitive advantage.

What comes through strongly is the need for reinvention rather just adjustment if insurers want to sustain revenue and competitive relevance. As a result, many insurers will look very different by 2020 and certainly by 2025. As new entrants and new business models begin to change the industry landscape, it’s also important to not only scan for developments within insurance but also maintain a clear view of the challenges and opportunities coming from outside the industry.

For the full report from which this article is excerpted, click here.

How are insurers feeling the impact of these developments?

Customer revolution

The insurance marketplace is becoming increasingly fragmented, with an aging population at one end of the spectrum and a less loyal and often hard to engage millennial generation at the other. The family structures and ethnic make-up within many markets are also becoming more varied and complex, which has implications for product design, marketing and sales. This splintering customer base and the need to develop relevant and engaging products and solutions present both a challenge and an opportunity for insurers. On the life, annuities and pensions side, insurers could design targeted plans for single parents or shift from living benefits to well-being or quality of life support for younger people. On the property and casualty (P&C) side, insurers could create partnerships with manufacturers and service companies. Insurers could also offer coverage for different lifestyles, offering flexible, pay-as-you-use insurance or providing top-up coverage for people in peer-to-peer insurance plans.

As the nature of the marketplace changes, so do customer expectations. Customers want insurers to offer them the same kind of easy access, show the same understanding of needs and provide the sorts of targeted products that they’ve become accustomed to from online retailers and other highly customer-centric sectors. Digital developments offer part of the answer by enabling insurers to deliver anytime, anywhere convenience, streamline operations and reach untapped segments. Insurers are also using digital developments to enhance customer profiling, develop sales leads, tailor financial solutions to individual needs and, for P&C businesses in particular, improve claims assessment and settlement. Further priorities include the development of a seamless multi-channel experience, which allows customers to engage when and how they want without having to relay the same information with each interaction. Because the margins between customer retention and loss are finer than ever, the challenge for insurers is how to develop the genuinely customer-centric culture, organizational capabilities and decision-making processes needed to keep pace with ever-more-exacting customer expectations.

Digitization

Most insurers have invested in digital distribution, with some now moving beyond direct digital sales to models that embed products and services in people’s lives (e.g., pay-as-you drive insurance).

A parallel development is the proliferation of new sources of information and analytical techniques, which are beginning to reshape customer targeting, risk underwriting and financial advice. Ever greater access to data doesn’t just increase the speed of servicing and lower costs but also opens the way for ever greater precision, customization and adaptation. As sensors and other digital intelligence become a more pervasive element of the "Internet of Things," savvy insurers can – and in some instances have – become trusted partners in areas ranging from health and well-being to home and commercial equipment care. Digital technology could extend the reach of life, annuities and pension coverage into largely untapped areas such as younger and lower-income segments.

Information advantage

Availability of both traditional and big data is exploding, with the resulting insights providing a valuable aid to customer-centricity and associated revenue growth. Yet many insurers are still finding it difficult to turn data into actionable insights. The keys to resolving this are as much about culture and organization as the application of technology. Making the most of the information and insight is also likely to require a move away from lengthy business planning to a faster and more flexible, data-led, iterative approach. Insurers would need to launch, test, obtain feedback and respond in a model similar to that used by many of today’s telecom and technology companies.

A combination of big data analytics, sensor technology and the communicating networks that make up the Internet of Things would allow insurers to anticipate risks and customer demands with far greater precision than ever before. The benefits would include not only keener pricing and sharper customer targeting but a decisive shift in insurers’ value model from reactive claims payer to preventative risk advisers.

The emerging game changer is the advance in analytics, from descriptive (what happened) and diagnostic (why it happened) analysis to predictive (what is likely to happen) and prescriptive (determining and ensuring the right outcome). This shift not only would enable insurers to anticipate what will happen and when, but also to respond actively. This offers great possibilities in areas ranging from more resilient supply chains and the elimination of design faults to stronger conversion rates for life insurers and more effective protection against fire and flood within property coverage.

Two-speed growth

These developments are coming to the fore against the backdrop of enduringly slow economic growth, continued low interest rates and soft P&C premiums within many developed markets. Interest rates will eventually begin to rise, which will cause some level of short-term disruption across the insurance sector, but over time higher interest rates will lead to higher levels of investment income.

On the P&C side, reserve releases have helped to bolster returns in a softening market. But redundant reserves are being depleted, making it harder to sustain reported returns.

The faster growing markets of South America, Asia, Africa and the Middle East (SAAAME) offer considerable long-term potential, though insurance penetration in 2013 was still only 2.7% of GDP in emerging markets and the share of global premiums only 17%. Penetration in their advanced counterparts was 8.3%. Rapid urbanization is set to be a key driver of growth within SAAAME markets, increasing the value of assets in need of protection. Urbanization also makes it harder for those from rural areas to call on the support of their extended families and hence increases take-up of life, annuities and pensions coverage. The corollary is the growing concentration of risk within these mega-metropolises.

Disruption and innovation

Many forward-looking insurers are developing new business models in areas ranging from tie-ups between reinsurance and investment management companies to a new generation of health, wealth and retirement solutions. The pace of change can only accelerate in the coming years as innovations become mainstream in areas ranging from wearables, the Internet of Things and automated driver assistance systems (ADAS) to partnerships with technology providers and crowd-sourced models of risk evaluation and transfer.

At the same time, a combination of digitization and new business models is disrupting the insurance marketplace by opening up new routes to market and new ways of engaging with customers. An increasing amount of standardized insurance will move over to mobile and Internet channels. But agents will still have a crucial role in helping businesses and retail customers to make sense of an ever-more-complex set of risks and to understand the trade-offs in managing them. On the life, annuities and pension side, this might include balancing the financial trade-offs between how much they want to live off now and their desired standard of living when they retire. On the P&C side, it would include designing effective aggregate protection for an increasingly broad and valuable array of assets and possessions.

Companies can bring innovations to market much faster and more easily than in the past. These companies include new entrants that are using advanced profiling techniques to target customers and cost-efficient digital distribution to undercut incumbent competitors. It’s too soon to say how successful these new entrants and start-ups will be, but they will undoubtedly provide further impetus to the changes in customer expectations and how insurers compete.

In the next two articles in this series, we look at how all these coalescing developments are likely to play out as we head toward 2020 and beyond and outline the strategic and operational implications for insurers. While we’ve set a nominal date of 2020, fast-moving businesses are already assessing and addressing these developments now as they look to keep pace with customer expectations and sharpen their competitive advantage.

What comes through strongly is the need for reinvention rather just adjustment if insurers want to sustain revenue and competitive relevance. As a result, many insurers will look very different by 2020 and certainly by 2025. As new entrants and new business models begin to change the industry landscape, it’s also important to not only scan for developments within insurance but also maintain a clear view of the challenges and opportunities coming from outside the industry.

For the full report from which this article is excerpted, click here.

How are insurers feeling the impact of these developments?

Customer revolution

The insurance marketplace is becoming increasingly fragmented, with an aging population at one end of the spectrum and a less loyal and often hard to engage millennial generation at the other. The family structures and ethnic make-up within many markets are also becoming more varied and complex, which has implications for product design, marketing and sales. This splintering customer base and the need to develop relevant and engaging products and solutions present both a challenge and an opportunity for insurers. On the life, annuities and pensions side, insurers could design targeted plans for single parents or shift from living benefits to well-being or quality of life support for younger people. On the property and casualty (P&C) side, insurers could create partnerships with manufacturers and service companies. Insurers could also offer coverage for different lifestyles, offering flexible, pay-as-you-use insurance or providing top-up coverage for people in peer-to-peer insurance plans.

As the nature of the marketplace changes, so do customer expectations. Customers want insurers to offer them the same kind of easy access, show the same understanding of needs and provide the sorts of targeted products that they’ve become accustomed to from online retailers and other highly customer-centric sectors. Digital developments offer part of the answer by enabling insurers to deliver anytime, anywhere convenience, streamline operations and reach untapped segments. Insurers are also using digital developments to enhance customer profiling, develop sales leads, tailor financial solutions to individual needs and, for P&C businesses in particular, improve claims assessment and settlement. Further priorities include the development of a seamless multi-channel experience, which allows customers to engage when and how they want without having to relay the same information with each interaction. Because the margins between customer retention and loss are finer than ever, the challenge for insurers is how to develop the genuinely customer-centric culture, organizational capabilities and decision-making processes needed to keep pace with ever-more-exacting customer expectations.

Digitization

Most insurers have invested in digital distribution, with some now moving beyond direct digital sales to models that embed products and services in people’s lives (e.g., pay-as-you drive insurance).

A parallel development is the proliferation of new sources of information and analytical techniques, which are beginning to reshape customer targeting, risk underwriting and financial advice. Ever greater access to data doesn’t just increase the speed of servicing and lower costs but also opens the way for ever greater precision, customization and adaptation. As sensors and other digital intelligence become a more pervasive element of the "Internet of Things," savvy insurers can – and in some instances have – become trusted partners in areas ranging from health and well-being to home and commercial equipment care. Digital technology could extend the reach of life, annuities and pension coverage into largely untapped areas such as younger and lower-income segments.

Information advantage

Availability of both traditional and big data is exploding, with the resulting insights providing a valuable aid to customer-centricity and associated revenue growth. Yet many insurers are still finding it difficult to turn data into actionable insights. The keys to resolving this are as much about culture and organization as the application of technology. Making the most of the information and insight is also likely to require a move away from lengthy business planning to a faster and more flexible, data-led, iterative approach. Insurers would need to launch, test, obtain feedback and respond in a model similar to that used by many of today’s telecom and technology companies.

A combination of big data analytics, sensor technology and the communicating networks that make up the Internet of Things would allow insurers to anticipate risks and customer demands with far greater precision than ever before. The benefits would include not only keener pricing and sharper customer targeting but a decisive shift in insurers’ value model from reactive claims payer to preventative risk advisers.

The emerging game changer is the advance in analytics, from descriptive (what happened) and diagnostic (why it happened) analysis to predictive (what is likely to happen) and prescriptive (determining and ensuring the right outcome). This shift not only would enable insurers to anticipate what will happen and when, but also to respond actively. This offers great possibilities in areas ranging from more resilient supply chains and the elimination of design faults to stronger conversion rates for life insurers and more effective protection against fire and flood within property coverage.

Two-speed growth

These developments are coming to the fore against the backdrop of enduringly slow economic growth, continued low interest rates and soft P&C premiums within many developed markets. Interest rates will eventually begin to rise, which will cause some level of short-term disruption across the insurance sector, but over time higher interest rates will lead to higher levels of investment income.

On the P&C side, reserve releases have helped to bolster returns in a softening market. But redundant reserves are being depleted, making it harder to sustain reported returns.

The faster growing markets of South America, Asia, Africa and the Middle East (SAAAME) offer considerable long-term potential, though insurance penetration in 2013 was still only 2.7% of GDP in emerging markets and the share of global premiums only 17%. Penetration in their advanced counterparts was 8.3%. Rapid urbanization is set to be a key driver of growth within SAAAME markets, increasing the value of assets in need of protection. Urbanization also makes it harder for those from rural areas to call on the support of their extended families and hence increases take-up of life, annuities and pensions coverage. The corollary is the growing concentration of risk within these mega-metropolises.

Disruption and innovation

Many forward-looking insurers are developing new business models in areas ranging from tie-ups between reinsurance and investment management companies to a new generation of health, wealth and retirement solutions. The pace of change can only accelerate in the coming years as innovations become mainstream in areas ranging from wearables, the Internet of Things and automated driver assistance systems (ADAS) to partnerships with technology providers and crowd-sourced models of risk evaluation and transfer.

At the same time, a combination of digitization and new business models is disrupting the insurance marketplace by opening up new routes to market and new ways of engaging with customers. An increasing amount of standardized insurance will move over to mobile and Internet channels. But agents will still have a crucial role in helping businesses and retail customers to make sense of an ever-more-complex set of risks and to understand the trade-offs in managing them. On the life, annuities and pension side, this might include balancing the financial trade-offs between how much they want to live off now and their desired standard of living when they retire. On the P&C side, it would include designing effective aggregate protection for an increasingly broad and valuable array of assets and possessions.

Companies can bring innovations to market much faster and more easily than in the past. These companies include new entrants that are using advanced profiling techniques to target customers and cost-efficient digital distribution to undercut incumbent competitors. It’s too soon to say how successful these new entrants and start-ups will be, but they will undoubtedly provide further impetus to the changes in customer expectations and how insurers compete.

In the next two articles in this series, we look at how all these coalescing developments are likely to play out as we head toward 2020 and beyond and outline the strategic and operational implications for insurers. While we’ve set a nominal date of 2020, fast-moving businesses are already assessing and addressing these developments now as they look to keep pace with customer expectations and sharpen their competitive advantage.

What comes through strongly is the need for reinvention rather just adjustment if insurers want to sustain revenue and competitive relevance. As a result, many insurers will look very different by 2020 and certainly by 2025. As new entrants and new business models begin to change the industry landscape, it’s also important to not only scan for developments within insurance but also maintain a clear view of the challenges and opportunities coming from outside the industry.

For the full report from which this article is excerpted, click here.