Historically, in the U.S. Healthcare system, a primary way to differentiate oneself as a healthcare provider has been to have impressive physical assets such as newly built clinics/hospitals/wings and medical equipment. This is logical when the legacy reimbursement model has incentivized activity (procedures, tests, prescriptions) instead of positive health outcomes. Anything that can be done that will create more activity creates more billing opportunities.

However, the DIY Health Reform movement has recognized that the flawed fee-for-service reimbursement model has been responsible for healthcare's hyperinflation. Some of the most interesting healthcare provider startups such as MedLion, National Surgery Network, and One Medical Group are using information technology (IT) rather than expensive equipment/facilities to differentiate themselves and affordably deliver superior health outcomes.

In an earlier article — Healthcare Disruption: Pharma 3.0 Will Drive Shift from Life Science to HealthTech Investing — I discussed how Health Information Technology has primarily been applied to administrative functions such as claims processing rather than core clinical functions such as decision support. In contrast, today's innovative healthcare providers recognize the changing dynamic of healthcare requires a fundamental rethink of the customer experience as has happened in many, many other industries.

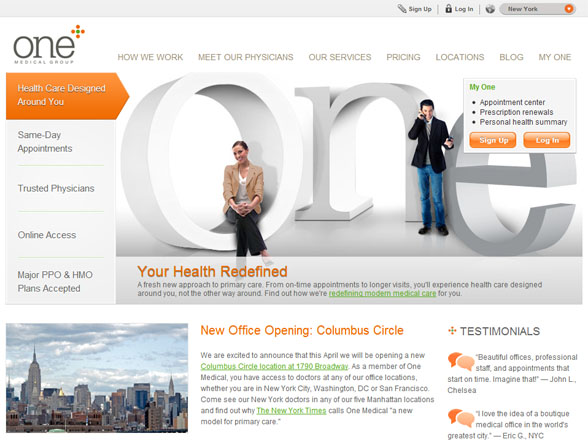

With one third of the workforce being permanent freelancers, contractors, consultants and entrepreneurs, individuals are compelled to directly buy healthcare rather than rely on their employer as they have in the past. The percentage of people directly buying their own healthcare will approach 50% as more employers opt out of providing health benefits as they get priced out (most have already reduced the percentage of the health premium they cover). Thus, consumerism is beginning to pervade healthcare like never before. In response, the aesthetic of providers' websites matters much more. For example, the website of Benchmark Capital-backed One Medical Group would make Philippe Starck proud (see screenshot below).

Of course, it needs to go beyond aesthetically pleasing websites. Whereas technology has historically brought incremental administrative efficiency in healthcare, organizations such as Qliance and OneMedical have utilized technology for radical transformation. It's no coincidence that they are backed by the founders of Amazon, aQuantive, Dell, Expedia, and venture firms such as Benchmark — all organizations that used technology to disrupt entire industries. Qliance evaluated 240 different U.S. based electronic medical systems before rejecting them as too billing centric rather than patient and health outcomes focused. Instead Qliance is creating competitive advantage by custom developing their software systems using off-the-shelf and custom-built software.

The aforementioned organizations are all disruptive startups bringing dramatically lower costs and better outcomes. What's going on at the large health system level where there's greater complexity including legacy processes and systems? Let's look at one example from the heart of Silicon Valley — Stanford Hospital & Clinics.

This was our opportunity to come up with ideal ways of working, not simply to replicate our very poor processes when we put in the new systems — because that's just a really expensive copy machine.

Stanford Hospital & Clinics is implementing a traditional health Information Technology system from one of the leading Health IT vendors — Epic Systems. Epic is appropriately named as, by all accounts, the implementations and cost are also epic. All the Epic projects I've heard about are eight and nine figures for the cost of the software and implementation. The scale of projects sound similar to the early days of Customer Relationship Management where it could only be implemented by very large organizations. The market leader for Customer Relationship Management was Siebel and those projects regularly ran seven to nine figures (reportedly 10 figures in the case of Epic's Kaiser implementation) which is obviously out of reach for small and medium sized organizations.

Disruptive pricing didn't come from Oracle or other large client-server vendors to extend this important category into smaller organizations. Instead it came from cloud-based Salesforce.com dramatically bringing costs down. Perhaps more interestingly, Salesforce created an open ecosystem inviting 3rd party developers to address the wide array of customer requirements for particular job functions and industries.

Healthcare has a similar diversity of conditions and communities that will necessitate a 3rd party ecosystem. I would predict that as the closed nature of legacy client-server Customer Relationship Management systems created an opportunity for Salesforce, the legacy client-server Health IT vendor systems are similarly closed and will create opportunities for modern, open architectures from a new generation of tech startups.

By definition, the legacy systems have been optimized around the flawed fee-for-service model that pervades healthcare today. In contrast, the disruptive new care and payment models that are exploding around the country require a new ecosystem of technology platforms. Out of necessity, the new healthcare delivery models have demanded custom built software, but this should change as those models reach critical mass. A market for off-the-shelf software for the next generation of HealthTech will develop.

A pharma executive explained to me the need to focus more on health technology. "Based on the 'patent cliff' in healthcare and the need for continued research and development, promotional budgets are becoming tighter; technology offers a less expensive way of interacting with our customers. Simultaneously, while many physician offices have been reticent to adopt technology, the incentives being put before them are now changing their perspective on technology ... pharma companies have an opportunity to take advantage of this." She went on to explain how that "no see docs" (i.e., physicians generally barring pharma reps from meeting with them) may be more open to new technologies delivered through reps that can help achieve better outcomes.

The scale of the plans for new business models emerging from major pharma, health product/device and health plan organizations will have these previously complementary organizations increasingly competing with each other. Perhaps more interestingly, they will begin competing with the very healthcare providers they have offered their products/services to. The notion of coopetition is familiar to those in tech but will likely become a term that is no longer foreign in healthcare. Just as we've seen Media become more like Merchants, I'd expect we'll see healthcare suppliers acting more like providers. We've already seen healthcare providers become health plans.

Newspapers provide a cautionary tale for healthcare providers. It was the non-obvious competitors that have cratered the newspaper businesses. In this related article, I draw parallels between the behaviors I observe today with health systems and the behavior of newspaper companies in the second half of the 90′s. Consider that the byproduct of Denmark's shift to a focus on outcomes over the last couple decades has resulted in half of their hospitals closing as they are simply not needed anymore.

Healthcare providers must reinvent themselves or they'll meet a similar fate to the Denmark hospitals that are now closed. A key part of their reinvention will be enabled by a new generation of technology solutions.