Having worked in and around Asia for the past few years, I have seen microinsurance be a constant topic.

I always found the concept of microinsurance (and microfinance) very interesting. However, I didn’t fully understand it.

Fortunately, Peter Gross from MicroEnsure helped to give me more insights into this fascinating and extremely important concept.

The following article is based on my conversation with Peter.

Who Is Peter Gross?

Peter is currently the director of strategy with MicroEnsure. Peter started with MicroEnsure in 2010 as the general manager in Ghana. Previously, Peter had a variety of management roles in McMaster-Carr.

When I asked Peter about why he moved from a company like McMaster-Carr to MicroEnsure, his answer was simple: "I wanted to work in a social enterprise and use my business skills in a developing context."

Peter’s wife is also in public health, working for the Centers for Disease Control and Prevention (CDC).

Having an alignment of interests and values is important for any partnership, personal ones included. Hence, moving to Ghana to help with both the protection and providing of care was an easy decision for the couple.

What Is Microinsurance?

One of the comments that stuck with me most during my conversation with Peter is on the definition of microinsurance. He explained that he is trying to get away from that term and refer to it more as "insurance for emerging customers." The main reason is a desire to get away from the perception of "micro-price vs. micro-value."

These types of products are specifically designed for an underserved population that typically can’t get access. That is the core of microinsurance.

For people in these markets, Peter said, "Good-quality insurance is very important because they face more day-to-day risks than you and I.…. They get really excited about insurance and the role it plays to protect them."

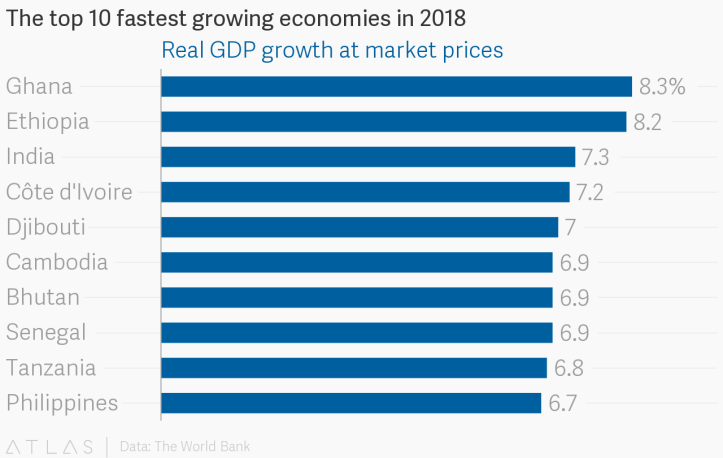

Microinsurance is primarily bought in some of the fastest-growing areas of the world, including these six countries from Africa and four from Asia:

[caption id="attachment_30091" align="alignnone" width="570"] Source: https://www.theatlas.com/charts/BJOKD67VG[/caption]

The blend of under-penetration plus fast growth shows a lot of opportunity for microinsurance in these areas, one which MicroEnsure is very aware of.

See also: A ‘Nudge’ Toward Microinsurance

What Is MicroEnsure?

MicroEnsure is a specialist provider of insurance for customers in emerging markets and has registered more than 55 million customers in 10 different countries in Asia and Africa.

MicroEnsure designs, builds and operates their business by having products that are simple to understand and with distribution partners that can help to reach the masses. They don’t carry the risk themselves and partner with more than 70 different insurers. Their biggest shareholder is AXA, alongside Omidyar Network, IFC and South Africa’s Sanlam.

Because the majority of the consumers in these markets do not have any insurance, Peter indicated to me that the marketing strategies that they deploy help them to introduce an insurance solution and meet an untapped need.

An example of this was when Peter first moved to Ghana. The company partnered with Tigo Telecom to offer free life insurance. The process worked like this:

Source: https://www.theatlas.com/charts/BJOKD67VG[/caption]

The blend of under-penetration plus fast growth shows a lot of opportunity for microinsurance in these areas, one which MicroEnsure is very aware of.

See also: A ‘Nudge’ Toward Microinsurance

What Is MicroEnsure?

MicroEnsure is a specialist provider of insurance for customers in emerging markets and has registered more than 55 million customers in 10 different countries in Asia and Africa.

MicroEnsure designs, builds and operates their business by having products that are simple to understand and with distribution partners that can help to reach the masses. They don’t carry the risk themselves and partner with more than 70 different insurers. Their biggest shareholder is AXA, alongside Omidyar Network, IFC and South Africa’s Sanlam.

Because the majority of the consumers in these markets do not have any insurance, Peter indicated to me that the marketing strategies that they deploy help them to introduce an insurance solution and meet an untapped need.

An example of this was when Peter first moved to Ghana. The company partnered with Tigo Telecom to offer free life insurance. The process worked like this:

Source: https://www.theatlas.com/charts/BJOKD67VG[/caption]

The blend of under-penetration plus fast growth shows a lot of opportunity for microinsurance in these areas, one which MicroEnsure is very aware of.

See also: A ‘Nudge’ Toward Microinsurance

What Is MicroEnsure?

MicroEnsure is a specialist provider of insurance for customers in emerging markets and has registered more than 55 million customers in 10 different countries in Asia and Africa.

MicroEnsure designs, builds and operates their business by having products that are simple to understand and with distribution partners that can help to reach the masses. They don’t carry the risk themselves and partner with more than 70 different insurers. Their biggest shareholder is AXA, alongside Omidyar Network, IFC and South Africa’s Sanlam.

Because the majority of the consumers in these markets do not have any insurance, Peter indicated to me that the marketing strategies that they deploy help them to introduce an insurance solution and meet an untapped need.

An example of this was when Peter first moved to Ghana. The company partnered with Tigo Telecom to offer free life insurance. The process worked like this:

- Customer dials *123 to sign up

- The more the customer spends on telecom services, the more insurance the customer receives (up to a maximum of $500)

- Identify a need

- Introduce a solution

- Make that solution readily available and accessible

- Introduce more solutions

- Make those solutions readily available and accessible

- Repeat

- BIMA, which just had an investment of $100 million from Allianz

- Ayo

- Acre Africa