As consumers, we know that digital has transformed the way we discover, engage and transact with businesses in every industry. From ordering coffee on our mobile devices to running our smart homes on voice-command, we expect all of our experiences to be fast and seamless.

The insurance industry has gone through its own digital transformation over the past five years. With a general acceptance that digital is here to stay, most insurers have incorporated digital into their organizations, implementing ad hoc capabilities to make their business faster and cheaper, creating online tools to further engage their distribution channels, and implementing table stakes technology in areas such as marketing, digital portals, customer self-service capabilities, and automation of some back-end processes.

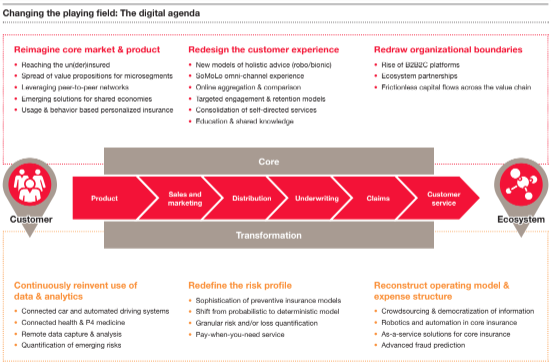

As we move into 2018, digital is continuing to reshape the way insurers do business. The ecosystem of available capabilities has grown exponentially and industry leaders are starting to leave behind the “fast-follower” mentality, reallocating their investments into core capabilities that give them a more customer-centric view, as well as ways to differentiate themselves in the market.

Industry leaders are starting to leave behind the “fast-follower” mentality, reallocating their investments into core capabilities that give them a more customer-centric view, as well as ways to differentiate themselves in the market.

From our perspective, insurers will take one of two paths:

Building a digital platform

Although we tend to understand digital transformation and modernization of technology platforms as sequential, multi-year events with multi-million dollar price tags, finite delivery dates and fixed realization periods, true modernization requires a foundational

shift in the organizational culture, operating model, and underlying architecture that enables business flexibility and agility.

Building a digital platform that will take your company into the future — not just respond to current needs — is critical to prolonged success.

Insurers are currently enabling access to data across various domains and dimensions, but the companies going the extra mile to design a futuristic platform architecture are the most likely to benefit in the long term. Future-oriented platform architectures should be able to:

Building a digital platform

Although we tend to understand digital transformation and modernization of technology platforms as sequential, multi-year events with multi-million dollar price tags, finite delivery dates and fixed realization periods, true modernization requires a foundational

shift in the organizational culture, operating model, and underlying architecture that enables business flexibility and agility.

Building a digital platform that will take your company into the future — not just respond to current needs — is critical to prolonged success.

Insurers are currently enabling access to data across various domains and dimensions, but the companies going the extra mile to design a futuristic platform architecture are the most likely to benefit in the long term. Future-oriented platform architectures should be able to:

- Continue as followers, investing in only select digital capabilities that support their existing business model. This is a bottom-up, project-driven approach that identifies select digital capabilities within different parts of the value chain.

- Take a digital-first mindset by better understanding the end-to-end customer experience and how business models need to evolve in order to increase growth and reduce costs. This is a top-down organization transformation with the goal of becoming a digital and data-driven organization which can continuously reassess the business and operating model.

- Build scalable systems, even for niche offerings,

- Deliver an end-to-end customer experience, and

- Change their business models to foster a test and learn environment that helps them improve how they go to market. These leaders will be the most likely to quickly adjust and grow as the industry continues to become more digital.

Building a digital platform

Although we tend to understand digital transformation and modernization of technology platforms as sequential, multi-year events with multi-million dollar price tags, finite delivery dates and fixed realization periods, true modernization requires a foundational

shift in the organizational culture, operating model, and underlying architecture that enables business flexibility and agility.

Building a digital platform that will take your company into the future — not just respond to current needs — is critical to prolonged success.

Insurers are currently enabling access to data across various domains and dimensions, but the companies going the extra mile to design a futuristic platform architecture are the most likely to benefit in the long term. Future-oriented platform architectures should be able to:

- Enable more granular services,

- Provide flexibility when reacting to traditional demands and responsiveness to disruptive emerging products,

- Support business models and technology needs beyond now standard core platform capabilities (e.g., policy, billing and claims systems).

- Feature consumer-centric architecture built on the core guiding principles of atomic components and services vs. monolithic applications,

- Enable reusability across constituent groups and processes vs. process-centric solutions,

- Assemble best-of-breed technologies, capabilities, and/or service models vs. being just a broker of services.

- Industry leaders are starting to leave behind the “follower” mentality, reallocating their investments into core capabilities that give them a more customer-centric view, as well as ways to differentiate themselves in the market. Whether you are a “fast- follower” (as opposed to just a follower) or a market innovator, you are likely to share essentially the same approach to establishing an agile organization.

- The companies that develop a meaningful competitive advantage will design and implement digital platforms that can handle disruption. They will build scalable systems, deliver an end-to-end customer experience, and change their business models to foster a test and learn environment that helps them improve how they go to market. These leaders will be the most likely to quickly adjust and grow as the industry continues to become more digital.

- With a strong, flexible framework in place, companies will be able to re-focus time and money into revenue-driving capabilities like external partnerships, invest in data-driven digital capabilities to improve customer value, and build back-end processes to support platform scalability.