The biennial study on workers’ compensation premium rates issued by the Oregon Department of Consumer and Business Services (DCBS) was released last week, and, as always, is worthy of a review by those of us entrenched within the industry. The study ranks all 50 states and Washington, D.C., based on rates that were in effect Jan. 1, 2014. This year’s results show that major reforms don’t always gain the results that were intended or marketed to the industry; and while the results may not accurately reflect legislative intentions of the past, the report may be a better predictor of major reforms to come.

The study shows that, despite extensive reforms designed to lower costs, California now has the most expensive rates in the nation, followed by Connecticut. North Dakota had the least expensive rates. In the Northwest, Idaho’s rates were the 14th most expensive, followed by Washington. Oregon researchers also compared each state’s rates to the national median (midpoint) rate of $1.85 per $100 of payroll -- California, for instance, was almost twice the median

According to Mike Manley, one of the co-authors of the survey, “We continue to see a trend in the distribution of state index rates in our study clustering in the middle of the distribution. A record 21 states are within plus or minus 10% of the 2014 study median. This makes the rank values more volatile from one study to the next. I would recommend that states look also to their ‘Percent of study median’ figure for comparisons over time.”

Because states have various mixes of industries, the study calculates rates for each state using a standard mix of the 50 industries with the highest workers’ compensation claims costs in Oregon. Details about how the study was conducted can be found here. A summary of the study was posted Wednesday, Oct. 8; the full report will be published later this year.

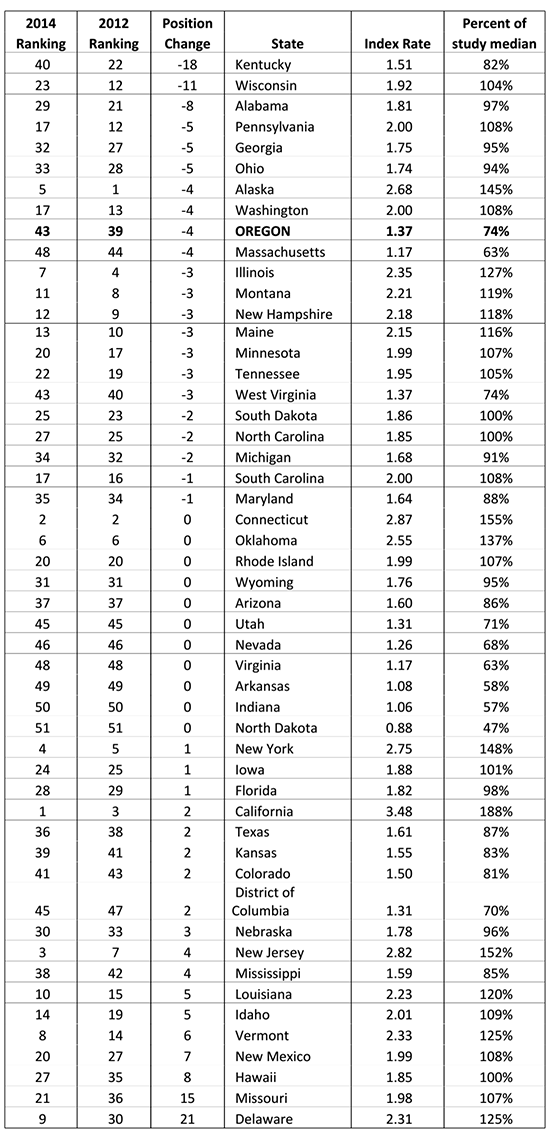

The summary report, available here, provides the complete ranking of the states premium rates. I have taken that data and added a comparative column that shows at a glance how far up or down the scale a state has moved since the last report in 2012. The table presents an interesting view, particularly juxtaposed with the knowledge of what states have undergone significant reforms in the past few years.

We can see that there were major drops in premium rank for both Kentucky and Wisconsin. Kentucky moved from 22nd-highest in the nation to 40th, improving by 18 positions. Wisconsin moved down 11 spots, from 12th-highest to 23rd. While Wisconsin did enact some changes in 2012, neither state is considered to have been a major reform state over the last few years.

For a couple of those states undergoing dramatic reforms, Oklahoma and Tennessee, it is too early to tell the effect, as they are just implementing changes this year. Others, however, including California and Kansas, saw premium costs as a comparative rise despite reforms intended to do otherwise. Illinois, another reform state, did see some positive movement, but it is probably not statistically significant given the weight of the costs and issues in that state.

I would postulate based on this report that people in New Mexico, Hawaii, Missouri and Delaware may be thinking of what changes should be in order, because they had dramatic negative movement on the scale this year. Even if past reforms overall are not creating significant improvement in these numbers, I am pretty sure they will be a better predictor of what states may be facing reform in the future.

Oregon has conducted these studies in even-numbered years since 1986, when Oregon’s rates were among the highest in the nation. The department reports the results to the Oregon legislature as a performance measure. Oregon’s relatively low rate today reflects the state’s workers’ compensation system reforms and its improvements in workplace safety and health.

Here are some key links for the study/workers’ compensation costs:

• To read a summary of the study, go here.

• Prior years’ summaries and full reports with details of study methods can be found here.

• Information on workers’ compensation costs in Oregon, including a map with these state rate rankings, is here.

We can see that there were major drops in premium rank for both Kentucky and Wisconsin. Kentucky moved from 22nd-highest in the nation to 40th, improving by 18 positions. Wisconsin moved down 11 spots, from 12th-highest to 23rd. While Wisconsin did enact some changes in 2012, neither state is considered to have been a major reform state over the last few years.

For a couple of those states undergoing dramatic reforms, Oklahoma and Tennessee, it is too early to tell the effect, as they are just implementing changes this year. Others, however, including California and Kansas, saw premium costs as a comparative rise despite reforms intended to do otherwise. Illinois, another reform state, did see some positive movement, but it is probably not statistically significant given the weight of the costs and issues in that state.

I would postulate based on this report that people in New Mexico, Hawaii, Missouri and Delaware may be thinking of what changes should be in order, because they had dramatic negative movement on the scale this year. Even if past reforms overall are not creating significant improvement in these numbers, I am pretty sure they will be a better predictor of what states may be facing reform in the future.

Oregon has conducted these studies in even-numbered years since 1986, when Oregon’s rates were among the highest in the nation. The department reports the results to the Oregon legislature as a performance measure. Oregon’s relatively low rate today reflects the state’s workers’ compensation system reforms and its improvements in workplace safety and health.

Here are some key links for the study/workers’ compensation costs:

• To read a summary of the study, go here.

• Prior years’ summaries and full reports with details of study methods can be found here.

• Information on workers’ compensation costs in Oregon, including a map with these state rate rankings, is here.

We can see that there were major drops in premium rank for both Kentucky and Wisconsin. Kentucky moved from 22nd-highest in the nation to 40th, improving by 18 positions. Wisconsin moved down 11 spots, from 12th-highest to 23rd. While Wisconsin did enact some changes in 2012, neither state is considered to have been a major reform state over the last few years.

For a couple of those states undergoing dramatic reforms, Oklahoma and Tennessee, it is too early to tell the effect, as they are just implementing changes this year. Others, however, including California and Kansas, saw premium costs as a comparative rise despite reforms intended to do otherwise. Illinois, another reform state, did see some positive movement, but it is probably not statistically significant given the weight of the costs and issues in that state.

I would postulate based on this report that people in New Mexico, Hawaii, Missouri and Delaware may be thinking of what changes should be in order, because they had dramatic negative movement on the scale this year. Even if past reforms overall are not creating significant improvement in these numbers, I am pretty sure they will be a better predictor of what states may be facing reform in the future.

Oregon has conducted these studies in even-numbered years since 1986, when Oregon’s rates were among the highest in the nation. The department reports the results to the Oregon legislature as a performance measure. Oregon’s relatively low rate today reflects the state’s workers’ compensation system reforms and its improvements in workplace safety and health.

Here are some key links for the study/workers’ compensation costs:

• To read a summary of the study, go here.

• Prior years’ summaries and full reports with details of study methods can be found here.

• Information on workers’ compensation costs in Oregon, including a map with these state rate rankings, is here.