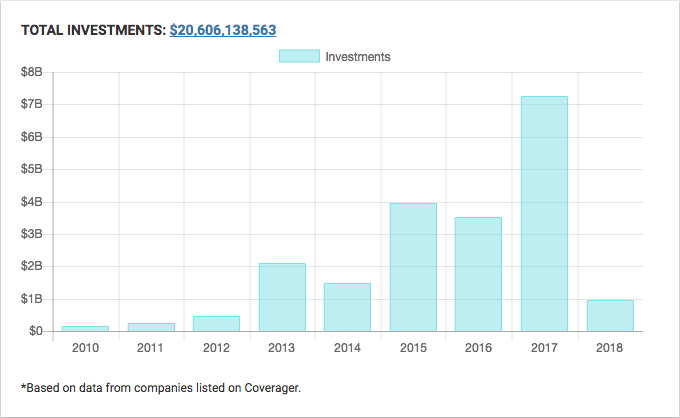

Over the past nine years, $20.6 billion has been invested into insurtech startups (data below as of March 21).

In 2016 and 2017 alone, this figure amounts to $10.7 billion.

I love it. There is nothing better than reading about a newly funded startup from a large VC firm.

It takes a ton of blood, sweat and tears to get an investment from a high-profile VC, and it is extremely rewarding for the startup that is able to secure funds from one.

These transactions tend to generate a lot of press (as they should). The money allows the startup to say, "We have proven ourselves by gaining some traction, have passed the intense due diligence of a VC firm and now have the runway to serve you." "You" in this sense typically means a carrier (in the case of a B2B insurtech startup).

There is another group of startups out there that do not get any funding press because they are self-funded.

These firms sometimes fall under the radar of carrier innovation teams that are scanning the market for meaningful solutions.

This article is NOT to take away from the funded companies. The majority of startups I work with are well-funded by VCs.

This article IS to educate on what a self-funded (i.e. bootstrapped) startup is, some advantages and challenges of working with one as well as how a carrier should assess a bootstrapped startup vs. a VC-funded one.

To help with this, I had the pleasure of interviewing Nick Mair, CEO and co-founder of Atticus DQPro. Atticus DQPro is a data monitoring platform designed specifically for the operational and regulatory needs of the insurance market. Atticus DQ Pro was bootstrapped from Nick’s first business, Atticus Associates, a consulting service to the London and specialty Insurance market.

What is a bootstrapped startup?

The self-funding can either come from a founder's personal finances or another revenue stream, such as consulting. A third approach is to fund a company based on the revenue from a product that you are building, though this can be harder to get off the ground. There are also circumstances whereby a company will bootstrap for a period of time to obtain more attractive fundraising terms (more on this later).

For Atticus DQPro, Nick had an established consulting business in the U.K. insurance market. The focus was on technological implementation and transformational change for carriers.

See also: Where Are the Insurtech Start-Ups?

By gaining on-the-ground understanding of how carriers work and what their problems were, Nick and his team were able to identify a solution for the specific need their clients were facing.

They got the idea and the funding from their consulting business.

What are some of the advantages to working with a bootstrapped insurtech startup?

"When you are bootstrapping, you are living on very limited amount of cash, and this means you are forced to solve a problem faster than a VC-funded outfit."

I found Nick’s statement to be quite interesting. Whether a startup is bootstrapped or VC funded, it must have a solution that is relevant to the carriers it is trying to work with. For those that have VC funding, their runway may be a bit longer. VCs are typically looking for a total return/liquidity event five to seven years from time of investment and good traction within one to three years. Bootstrappers do not have this same luxury.

"Many bootstrappers are looking to solve a real problem now rather than something truly disruptive," Nick said.

Nick explained that, from his experience, bootstrappers must get to product/market fit and real revenues faster. If they don’t (unless they have very deep pockets), then they could be out of business in less than a year.

Nick said bootstrappers are pushed to solve problems faster with the carriers they work with and then scale quickly after that.

Bootstrappers can mine opportunities that are not of interest to VCs because they’re sub-scale; e.g it’s a $5 million to $30 million opportunity rather than $100 million-plus. That window leaves a lot of niche problems for bootstrappers to fix without competition from funded startups. Nick said: "We can argue revolutionary change is required for our industry, but evolution can happen in parallel to solve real business problems now."

Lastly is the area of domain expertise. Many bootstrappers (as in the case with Nick) are industry specialists who have found a need within the domain and want to fix it. By contrast, many of the VC-funded startups come with founders with deep technology backgrounds. They have built great solutions that they believe can enhance or disrupt insurance yet lack the insurance industry domain expertise.

I do see this dynamic shifting. There are many more VC-funded startups with founders who come from within the insurance industry.

What are some of the challenges to working with a bootstrapped insurtech startup?

Not all VC-funded startups are looking for long-term disruptive solutions. Many have product/market fit solutions that solve the existing problems of today’s insurers.

These VC-funded startups can scale their teams (specifically in sales/business development) much more quickly than a bootstrapped model allows. Nick shared that this problem typically comes when the bootstrapper has around 10 clients and needs more resources to continue to market and deliver their product. This is typically the time that a bootstrapper needs to try to secure outside funding.

Nick’s view is that bootstrappers that can generate a decent annual recurring revenue (of roughly $1 million to $2 million) will be in a better position to get additional funding on more favorable terms (i.e. the startup already knows it has something that works and can be more confident when/if seeking additional funding to scale, through a VC, small private equity firm or carrier). Getting to that point and knowing when to make that call can be hard for a bootstrapper.

Another disadvantage of working with one is that the team is primarily the management team and advisory board. Having a VC-funded startup brings the experience of the firm that invested. A VC firm has massive skin in the game for the startups to succeed.

If the VCs are with a reputable firm, they have dealt with startups for a long time and likely had some good exits. They will be able to bring a perspective that the founders may not have and may not have access to within their own management team/advisory board.

What does this mean for carriers? Should they partner with a bootstrapped insurtech startup or a VC-funded one?

A few months ago, I wrote An insurance carrier’s guide to working with an insurtech startup. The first point is to "understand and prioritize your organization’s needs." I would like to reiterate this. A carrier must have a problem/area that needs to be addressed. If the startup fills this need, then I said to move to the next, which is due diligence.

If the startup is VC-funded, this is a good first step.

VCs have ridiculous due diligence processes (just ask any founder what the process is like). If a startup has secured a Series A or higher from a reputable VC firm, it has passed a certain test. The VC will have looked at the business plan, legal entity setup and founding team to the nth degree (among other things). A carrier must perform its own due diligence but has the assurance that someone else has also done a fair amount.

For a bootstrapped one, it is important to know where the funding is coming from and what sort of runway the startup has.

For both, it is important to know what sort of engagements they have done. If they are only in pilot stage with the carriers they are working with, this is OK. Ask what sort of results they can share with you from the pilots they have done/are doing to indicate whether that is the sort of result you are looking for.

Additionally, when looking at the team of the startup, it is extremely valuable if some of the founders/team members have actual insurance industry experience. This will add another element of understanding of the carrier’s business while working together.

Lastly, carriers should start with a pilot when working with a startup (whether funded or bootstrapped). This is a good way to validate the work the startup says it is going to do with you before going fully commercial.

Summary

There are tons of startups out there. It’s such an exciting time to be in this business and to be working with such smart and energetic people who are trying to make insurance better for consumers.

I have deep admiration and respect for all startups, whether they are funded by VCs or bootstrapped. It takes a lot of courage and perseverance to start a business, especially in one as highly regulated as ours.

See also: What’s Your Game Plan for Insurtech?

There are many reasons why a startup would be bootstrapped vs. raising funds.

The last point Nick made to me was that "self-funded can mean bootstrapped by design/choice rather than trying to get funded. Founder reasons can be keeping control, better work/life balance or greater freedom."

For those thinking about starting an insurtech startup, have a look at this article that Nick shared with me.

And for those carriers looking to partner with a startup, do your due diligence and make sure you are filling a need and putting the carrier in a better place as a result. VC-funded startups and bootstrapped ones are both good options, and you should consider both for your innovation efforts.

This article first appeared at Daily Fintech.

I love it. There is nothing better than reading about a newly funded startup from a large VC firm.

It takes a ton of blood, sweat and tears to get an investment from a high-profile VC, and it is extremely rewarding for the startup that is able to secure funds from one.

These transactions tend to generate a lot of press (as they should). The money allows the startup to say, "We have proven ourselves by gaining some traction, have passed the intense due diligence of a VC firm and now have the runway to serve you." "You" in this sense typically means a carrier (in the case of a B2B insurtech startup).

There is another group of startups out there that do not get any funding press because they are self-funded.

These firms sometimes fall under the radar of carrier innovation teams that are scanning the market for meaningful solutions.

This article is NOT to take away from the funded companies. The majority of startups I work with are well-funded by VCs.

This article IS to educate on what a self-funded (i.e. bootstrapped) startup is, some advantages and challenges of working with one as well as how a carrier should assess a bootstrapped startup vs. a VC-funded one.

To help with this, I had the pleasure of interviewing Nick Mair, CEO and co-founder of Atticus DQPro. Atticus DQPro is a data monitoring platform designed specifically for the operational and regulatory needs of the insurance market. Atticus DQ Pro was bootstrapped from Nick’s first business, Atticus Associates, a consulting service to the London and specialty Insurance market.

What is a bootstrapped startup?

The self-funding can either come from a founder's personal finances or another revenue stream, such as consulting. A third approach is to fund a company based on the revenue from a product that you are building, though this can be harder to get off the ground. There are also circumstances whereby a company will bootstrap for a period of time to obtain more attractive fundraising terms (more on this later).

For Atticus DQPro, Nick had an established consulting business in the U.K. insurance market. The focus was on technological implementation and transformational change for carriers.

See also: Where Are the Insurtech Start-Ups?

By gaining on-the-ground understanding of how carriers work and what their problems were, Nick and his team were able to identify a solution for the specific need their clients were facing.

They got the idea and the funding from their consulting business.

What are some of the advantages to working with a bootstrapped insurtech startup?

"When you are bootstrapping, you are living on very limited amount of cash, and this means you are forced to solve a problem faster than a VC-funded outfit."

I found Nick’s statement to be quite interesting. Whether a startup is bootstrapped or VC funded, it must have a solution that is relevant to the carriers it is trying to work with. For those that have VC funding, their runway may be a bit longer. VCs are typically looking for a total return/liquidity event five to seven years from time of investment and good traction within one to three years. Bootstrappers do not have this same luxury.

"Many bootstrappers are looking to solve a real problem now rather than something truly disruptive," Nick said.

Nick explained that, from his experience, bootstrappers must get to product/market fit and real revenues faster. If they don’t (unless they have very deep pockets), then they could be out of business in less than a year.

Nick said bootstrappers are pushed to solve problems faster with the carriers they work with and then scale quickly after that.

Bootstrappers can mine opportunities that are not of interest to VCs because they’re sub-scale; e.g it’s a $5 million to $30 million opportunity rather than $100 million-plus. That window leaves a lot of niche problems for bootstrappers to fix without competition from funded startups. Nick said: "We can argue revolutionary change is required for our industry, but evolution can happen in parallel to solve real business problems now."

Lastly is the area of domain expertise. Many bootstrappers (as in the case with Nick) are industry specialists who have found a need within the domain and want to fix it. By contrast, many of the VC-funded startups come with founders with deep technology backgrounds. They have built great solutions that they believe can enhance or disrupt insurance yet lack the insurance industry domain expertise.

I do see this dynamic shifting. There are many more VC-funded startups with founders who come from within the insurance industry.

What are some of the challenges to working with a bootstrapped insurtech startup?

Not all VC-funded startups are looking for long-term disruptive solutions. Many have product/market fit solutions that solve the existing problems of today’s insurers.

These VC-funded startups can scale their teams (specifically in sales/business development) much more quickly than a bootstrapped model allows. Nick shared that this problem typically comes when the bootstrapper has around 10 clients and needs more resources to continue to market and deliver their product. This is typically the time that a bootstrapper needs to try to secure outside funding.

Nick’s view is that bootstrappers that can generate a decent annual recurring revenue (of roughly $1 million to $2 million) will be in a better position to get additional funding on more favorable terms (i.e. the startup already knows it has something that works and can be more confident when/if seeking additional funding to scale, through a VC, small private equity firm or carrier). Getting to that point and knowing when to make that call can be hard for a bootstrapper.

Another disadvantage of working with one is that the team is primarily the management team and advisory board. Having a VC-funded startup brings the experience of the firm that invested. A VC firm has massive skin in the game for the startups to succeed.

If the VCs are with a reputable firm, they have dealt with startups for a long time and likely had some good exits. They will be able to bring a perspective that the founders may not have and may not have access to within their own management team/advisory board.

What does this mean for carriers? Should they partner with a bootstrapped insurtech startup or a VC-funded one?

A few months ago, I wrote An insurance carrier’s guide to working with an insurtech startup. The first point is to "understand and prioritize your organization’s needs." I would like to reiterate this. A carrier must have a problem/area that needs to be addressed. If the startup fills this need, then I said to move to the next, which is due diligence.

If the startup is VC-funded, this is a good first step.

VCs have ridiculous due diligence processes (just ask any founder what the process is like). If a startup has secured a Series A or higher from a reputable VC firm, it has passed a certain test. The VC will have looked at the business plan, legal entity setup and founding team to the nth degree (among other things). A carrier must perform its own due diligence but has the assurance that someone else has also done a fair amount.

For a bootstrapped one, it is important to know where the funding is coming from and what sort of runway the startup has.

For both, it is important to know what sort of engagements they have done. If they are only in pilot stage with the carriers they are working with, this is OK. Ask what sort of results they can share with you from the pilots they have done/are doing to indicate whether that is the sort of result you are looking for.

Additionally, when looking at the team of the startup, it is extremely valuable if some of the founders/team members have actual insurance industry experience. This will add another element of understanding of the carrier’s business while working together.

Lastly, carriers should start with a pilot when working with a startup (whether funded or bootstrapped). This is a good way to validate the work the startup says it is going to do with you before going fully commercial.

Summary

There are tons of startups out there. It’s such an exciting time to be in this business and to be working with such smart and energetic people who are trying to make insurance better for consumers.

I have deep admiration and respect for all startups, whether they are funded by VCs or bootstrapped. It takes a lot of courage and perseverance to start a business, especially in one as highly regulated as ours.

See also: What’s Your Game Plan for Insurtech?

There are many reasons why a startup would be bootstrapped vs. raising funds.

The last point Nick made to me was that "self-funded can mean bootstrapped by design/choice rather than trying to get funded. Founder reasons can be keeping control, better work/life balance or greater freedom."

For those thinking about starting an insurtech startup, have a look at this article that Nick shared with me.

And for those carriers looking to partner with a startup, do your due diligence and make sure you are filling a need and putting the carrier in a better place as a result. VC-funded startups and bootstrapped ones are both good options, and you should consider both for your innovation efforts.

This article first appeared at Daily Fintech.

I love it. There is nothing better than reading about a newly funded startup from a large VC firm.

It takes a ton of blood, sweat and tears to get an investment from a high-profile VC, and it is extremely rewarding for the startup that is able to secure funds from one.

These transactions tend to generate a lot of press (as they should). The money allows the startup to say, "We have proven ourselves by gaining some traction, have passed the intense due diligence of a VC firm and now have the runway to serve you." "You" in this sense typically means a carrier (in the case of a B2B insurtech startup).

There is another group of startups out there that do not get any funding press because they are self-funded.

These firms sometimes fall under the radar of carrier innovation teams that are scanning the market for meaningful solutions.

This article is NOT to take away from the funded companies. The majority of startups I work with are well-funded by VCs.

This article IS to educate on what a self-funded (i.e. bootstrapped) startup is, some advantages and challenges of working with one as well as how a carrier should assess a bootstrapped startup vs. a VC-funded one.

To help with this, I had the pleasure of interviewing Nick Mair, CEO and co-founder of Atticus DQPro. Atticus DQPro is a data monitoring platform designed specifically for the operational and regulatory needs of the insurance market. Atticus DQ Pro was bootstrapped from Nick’s first business, Atticus Associates, a consulting service to the London and specialty Insurance market.

What is a bootstrapped startup?

The self-funding can either come from a founder's personal finances or another revenue stream, such as consulting. A third approach is to fund a company based on the revenue from a product that you are building, though this can be harder to get off the ground. There are also circumstances whereby a company will bootstrap for a period of time to obtain more attractive fundraising terms (more on this later).

For Atticus DQPro, Nick had an established consulting business in the U.K. insurance market. The focus was on technological implementation and transformational change for carriers.

See also: Where Are the Insurtech Start-Ups?

By gaining on-the-ground understanding of how carriers work and what their problems were, Nick and his team were able to identify a solution for the specific need their clients were facing.

They got the idea and the funding from their consulting business.

What are some of the advantages to working with a bootstrapped insurtech startup?

"When you are bootstrapping, you are living on very limited amount of cash, and this means you are forced to solve a problem faster than a VC-funded outfit."

I found Nick’s statement to be quite interesting. Whether a startup is bootstrapped or VC funded, it must have a solution that is relevant to the carriers it is trying to work with. For those that have VC funding, their runway may be a bit longer. VCs are typically looking for a total return/liquidity event five to seven years from time of investment and good traction within one to three years. Bootstrappers do not have this same luxury.

"Many bootstrappers are looking to solve a real problem now rather than something truly disruptive," Nick said.

Nick explained that, from his experience, bootstrappers must get to product/market fit and real revenues faster. If they don’t (unless they have very deep pockets), then they could be out of business in less than a year.

Nick said bootstrappers are pushed to solve problems faster with the carriers they work with and then scale quickly after that.

Bootstrappers can mine opportunities that are not of interest to VCs because they’re sub-scale; e.g it’s a $5 million to $30 million opportunity rather than $100 million-plus. That window leaves a lot of niche problems for bootstrappers to fix without competition from funded startups. Nick said: "We can argue revolutionary change is required for our industry, but evolution can happen in parallel to solve real business problems now."

Lastly is the area of domain expertise. Many bootstrappers (as in the case with Nick) are industry specialists who have found a need within the domain and want to fix it. By contrast, many of the VC-funded startups come with founders with deep technology backgrounds. They have built great solutions that they believe can enhance or disrupt insurance yet lack the insurance industry domain expertise.

I do see this dynamic shifting. There are many more VC-funded startups with founders who come from within the insurance industry.

What are some of the challenges to working with a bootstrapped insurtech startup?

Not all VC-funded startups are looking for long-term disruptive solutions. Many have product/market fit solutions that solve the existing problems of today’s insurers.

These VC-funded startups can scale their teams (specifically in sales/business development) much more quickly than a bootstrapped model allows. Nick shared that this problem typically comes when the bootstrapper has around 10 clients and needs more resources to continue to market and deliver their product. This is typically the time that a bootstrapper needs to try to secure outside funding.

Nick’s view is that bootstrappers that can generate a decent annual recurring revenue (of roughly $1 million to $2 million) will be in a better position to get additional funding on more favorable terms (i.e. the startup already knows it has something that works and can be more confident when/if seeking additional funding to scale, through a VC, small private equity firm or carrier). Getting to that point and knowing when to make that call can be hard for a bootstrapper.

Another disadvantage of working with one is that the team is primarily the management team and advisory board. Having a VC-funded startup brings the experience of the firm that invested. A VC firm has massive skin in the game for the startups to succeed.

If the VCs are with a reputable firm, they have dealt with startups for a long time and likely had some good exits. They will be able to bring a perspective that the founders may not have and may not have access to within their own management team/advisory board.

What does this mean for carriers? Should they partner with a bootstrapped insurtech startup or a VC-funded one?

A few months ago, I wrote An insurance carrier’s guide to working with an insurtech startup. The first point is to "understand and prioritize your organization’s needs." I would like to reiterate this. A carrier must have a problem/area that needs to be addressed. If the startup fills this need, then I said to move to the next, which is due diligence.

If the startup is VC-funded, this is a good first step.

VCs have ridiculous due diligence processes (just ask any founder what the process is like). If a startup has secured a Series A or higher from a reputable VC firm, it has passed a certain test. The VC will have looked at the business plan, legal entity setup and founding team to the nth degree (among other things). A carrier must perform its own due diligence but has the assurance that someone else has also done a fair amount.

For a bootstrapped one, it is important to know where the funding is coming from and what sort of runway the startup has.

For both, it is important to know what sort of engagements they have done. If they are only in pilot stage with the carriers they are working with, this is OK. Ask what sort of results they can share with you from the pilots they have done/are doing to indicate whether that is the sort of result you are looking for.

Additionally, when looking at the team of the startup, it is extremely valuable if some of the founders/team members have actual insurance industry experience. This will add another element of understanding of the carrier’s business while working together.

Lastly, carriers should start with a pilot when working with a startup (whether funded or bootstrapped). This is a good way to validate the work the startup says it is going to do with you before going fully commercial.

Summary

There are tons of startups out there. It’s such an exciting time to be in this business and to be working with such smart and energetic people who are trying to make insurance better for consumers.

I have deep admiration and respect for all startups, whether they are funded by VCs or bootstrapped. It takes a lot of courage and perseverance to start a business, especially in one as highly regulated as ours.

See also: What’s Your Game Plan for Insurtech?

There are many reasons why a startup would be bootstrapped vs. raising funds.

The last point Nick made to me was that "self-funded can mean bootstrapped by design/choice rather than trying to get funded. Founder reasons can be keeping control, better work/life balance or greater freedom."

For those thinking about starting an insurtech startup, have a look at this article that Nick shared with me.

And for those carriers looking to partner with a startup, do your due diligence and make sure you are filling a need and putting the carrier in a better place as a result. VC-funded startups and bootstrapped ones are both good options, and you should consider both for your innovation efforts.

This article first appeared at Daily Fintech.